- Energy Storage Solutions

- Graphene Battery Market

Graphene Battery Market Size, Share, and Growth Forecast 2025 - 2032

Graphene Battery Market By Battery Type (Lithium-ion, Graphene Supercapacitor, Lithium-Sulfur Graphene, Other), Application (Automotive, Consumer Electronics, Power, Industrial, Other), and Regional Analysis for 2025 - 2032

Graphene Battery Market Size and Trend Analysis

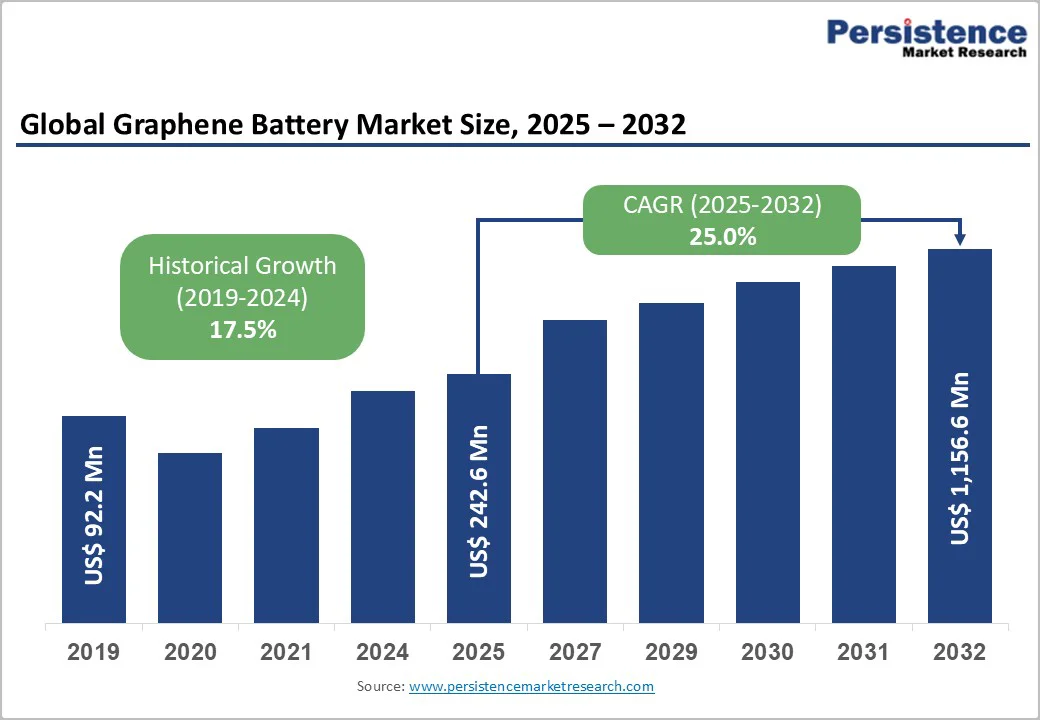

The global graphene battery market size is likely to be valued at US$242.6 Million in 2025 and is expected to reach US$1,156.6 Million by 2032, growing at a CAGR of 25% during the forecast period from 2025 to 2032, driven by the surging demand for high-performance energy storage solutions in electric vehicles (EVs) and renewable energy systems, fueled by graphene's superior conductivity and energy density that enable faster charging and longer lifespans compared to traditional batteries.

Supported by rising sustainability priorities, global clean energy investments reached US$1.8 Trillion in 2024, with a notable share funneled into advanced battery technologies, according to the International Energy Agency. The incorporation of graphene is further boosting battery safety, energy density, and thermal stability, addressing core limitations of Li-ion systems and accelerating their adoption in both automotive and consumer electronics markets.

Key Industry Highlights

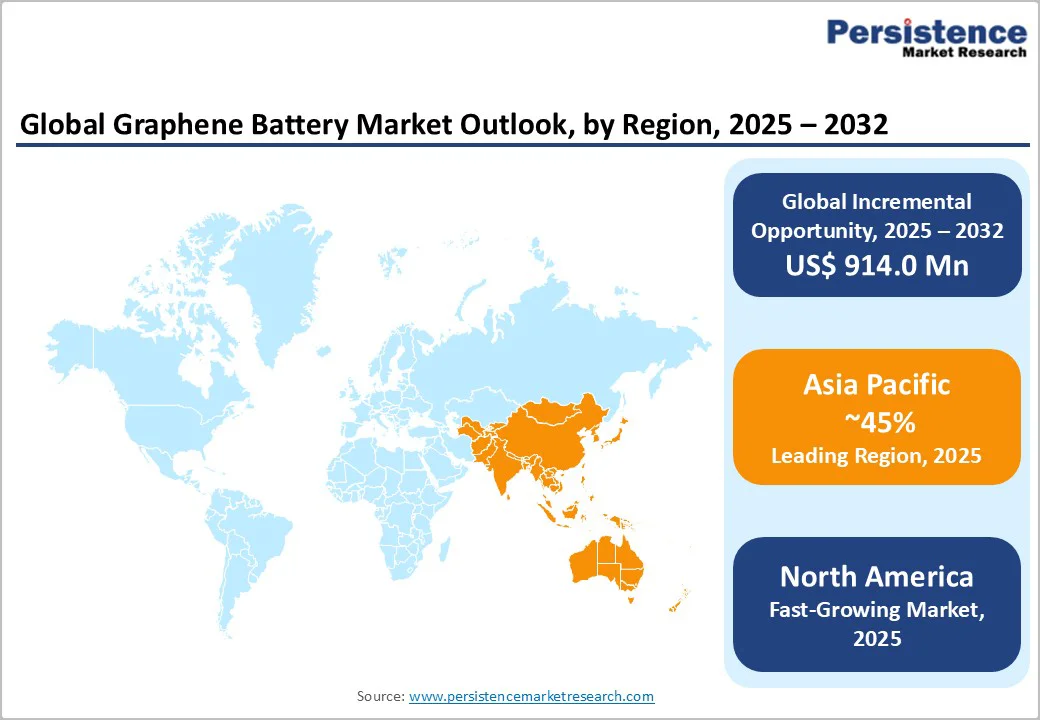

- Regional Leader: Asia Pacific leads the market with around 45% of the market share, propelled by China's manufacturing dominance and CNY1.5 Trillion (US$210 Billion) investments, enabling rapid EV adoption and 40% export surges in advanced batteries.

- Fastest Growing Region: North America emerged as the fastest-growing region in the graphene battery market, due to strong U.S. innovation ecosystems and US$370 Billion in clean energy incentives, driving EV and aerospace applications with superior R&D infrastructure.

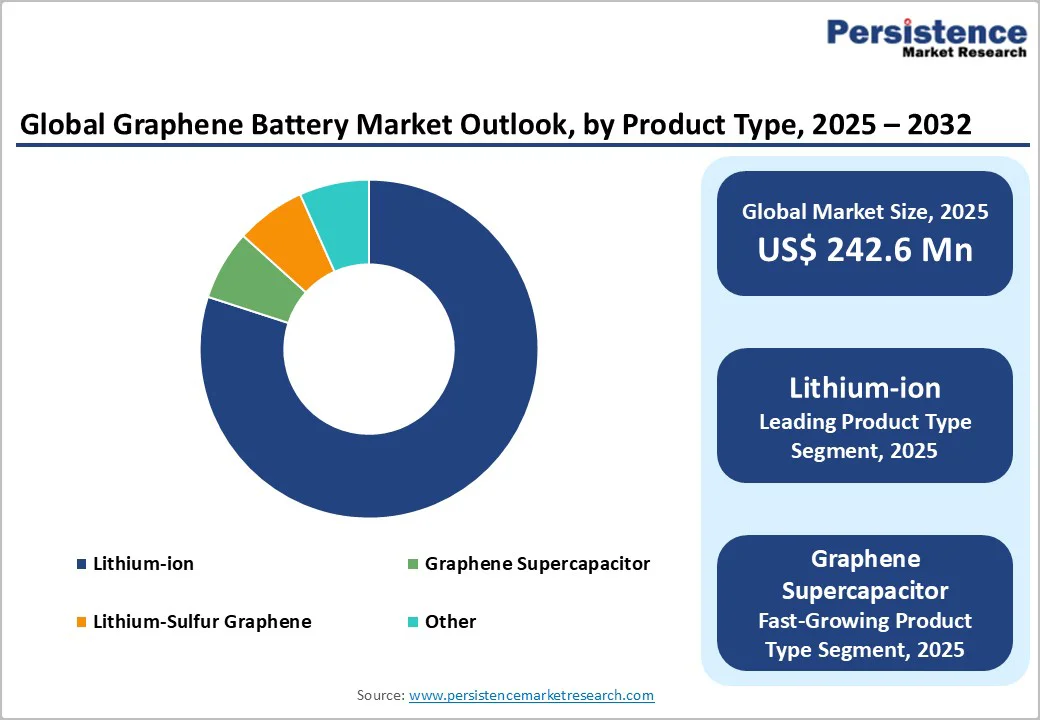

- Leading Segment: The lithium-ion segment dominates battery type, capturing 80% share through enhanced conductivity and 60x faster charging, ideal for high-demand portable and automotive uses.

- Fastest-growing Segment: Graphene Supercapacitor stands as the fastest-growing battery type segment, fueled by needs for instant power bursts in renewables, with growth exceeding 30% CAGR amid grid storage expansions.

- Growth Opportunities: Key opportunity lies in EV integrations, where graphene doubles energy density to 500 Wh/kg, addressing range anxiety and capturing 25% of the EV battery market by 2030.

| Key Insights | Details |

|---|---|

|

Graphene Battery Market Size (2025E) |

US$242.6 Mn |

|

Market Value Forecast (2032F) |

US$1,156.6 Mn |

|

Projected Growth CAGR (2025-2032) |

25.0% |

|

Historical Market Growth (2019-2024) |

17.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surging Demand for Electric Vehicles

The escalating adoption of EVs worldwide is a pivotal driver for the graphene battery market, propelled by the need for batteries offering higher energy density and rapid charging capabilities. Graphene integration allows batteries to achieve up to five times faster charging speeds while maintaining stable performance, significantly reducing range anxiety for consumers.

According to the International Energy Agency, global EV sales surpassed 14 million units in 2024, a 35% increase from the previous year, with graphene-enhanced batteries enabling longer driving ranges, up to 45% more capacity than standard lithium-ion variants. This shift is further supported by government incentives, such as the U.S. Inflation Reduction Act, which allocates over US$370 Billion for clean energy, directly boosting R&D in advanced battery technologies and fostering market expansion. The positive impact is evident in the EV battery market, where graphene's lightweight properties contribute to improved vehicle efficiency and reduced emissions, convincing stakeholders of its transformative potential for sustainable mobility.

Advancements in Renewable Energy Integration

Rapid progress in renewable energy storage is another key driver, as graphene batteries provide superior efficiency in capturing and releasing intermittent solar and wind power. Their high thermal conductivity, up to 1,400 W m?¹ K?¹, ensures better heat dissipation, enhancing safety and longevity in grid-scale applications.

The International Renewable Energy Agency reports that renewable capacity additions hit 510 GW in 2024, underscoring the demand for reliable storage solutions that graphene fulfills by extending battery life cycles by over 2,000 charges without degradation. This driver positively influences market growth by enabling seamless integration with existing infrastructure, reducing energy costs by up to 30% in large-scale deployments, and supporting global net-zero goals as outlined in the Paris Agreement.

Barrier Analysis - High Production Costs and Scalability Challenges

Elevated manufacturing expenses remain a significant barrier, as producing high-quality graphene requires sophisticated processes such as chemical vapor deposition, costing up to 10 times more than conventional materials. This limits scalability, with current global production capacity at only 1,000 tons annually, far below the 10,000 tons needed for widespread adoption, according to the European Commission's Joint Research Centre. These costs inflate battery prices by 20-30%, deterring price-sensitive sectors such as consumer electronics and hindering market penetration in developing regions. The restraint's negative impact is compounded by supply chain dependencies on raw graphite, primarily from China, which controls 80% of global supplies, exposing manufacturers to geopolitical risks and price volatility that could slow commercialization efforts.

Technical Integration and Material Purity Issues

Achieving consistent graphene purity for battery integration poses another challenge, as defects in the material can reduce conductivity by up to 50%, leading to performance inconsistencies. Research from Swansea University indicates that impurities during synthesis affect up to 30% of production batches, increasing failure rates in high-demand applications such as aerospace.

Such technical hurdles negatively affect market confidence, delaying regulatory approvals and raising safety concerns, with incidents of thermal instability reported in early prototypes, ultimately impeding the transition from lab-scale to industrial production. The absence of standardized manufacturing protocols and quality assessment methodologies complicates efforts by companies such as Global Graphene Group and Graphene Manufacturing Group to establish reproducible production processes that meet automotive and industrial battery specifications.

Opportunity Analysis - Government Initiatives and Policy Support Accelerating Technology Development

Substantial growth opportunities are emerging from government-backed initiatives promoting advanced battery research and domestic manufacturing capabilities, with programs such as India's FAME II scheme and the European Green Deal providing financial incentives and regulatory frameworks favorable to graphene battery development. The Queensland Government awarded AU$2 Million (US$1,294,400) in funding to Graphene Manufacturing Group for pilot plant development, exemplifying public sector commitment to advancing next-generation energy storage technologies.

Integration with Renewable Energy Policies

Government policies promoting renewables offer substantial opportunities, as graphene batteries enhance grid stability by storing excess energy with minimal loss. The EU's Green Deal targets 45% renewable energy by 2030, driving demand for storage solutions that graphene provides through its recyclability and 35% longer lifespan, per International Renewable Energy Agency data.

Nanotech Energy announced agreements to supply over 1 GWh of battery energy storage systems to distribution partners in Greece through 2028, indicating substantial market appetite for graphene-based solutions in stationary applications. Lead acid battery market participants are increasingly exploring graphene additives to enhance performance characteristics, while lithium-sulfur graphene batteries offer theoretical energy densities several times higher than conventional systems, positioning them as ideal candidates for large-scale renewable energy storage.

Category-wise Analysis

Battery Type Insights

The lithium-ion segment leads the battery type category with an approximate 80% market share, driven by its compatibility with the existing manufacturing infrastructure and enhanced performance through graphene additives. This dominance stems from graphene's role in boosting conductivity, allowing faster charging, up to 60 times quicker than conventional variants, and higher energy density, making it ideal for portable and automotive uses.

Statistics from IEEE Spectrum highlight that lithium-ion graphene batteries retain over 70% capacity after 2,000 cycles at 60°C, far surpassing standard models, which justifies their leadership amid rising EV demands. The technology's commercial viability stems from its compatibility with existing manufacturing equipment and processes, allowing producers such as Samsung SDI, which showcased its comprehensive battery lineup, including all solid-state and 46-phi cylindrical batteries at industry exhibitions, to leverage current production capabilities while incrementally incorporating graphene materials. The segment's maturity, supported by R&D investments exceeding US$500 Million annually from institutions such as MIT, ensures reliable scalability and positions it as the cornerstone for innovations in the Li-ion battery market.

Application Analysis

The automotive segment dominates the application category, holding around 55% market share, propelled by the need for lightweight, high-capacity batteries in electric vehicles. Graphene enables up to 45% capacity increase and fivefold faster charging, addressing range limitations and aligning with global emission standards such as the EU's CO2 targets.

Data from the U.S. Department of Energy shows automotive applications benefiting from graphene's thermal stability, reducing overheating risks by 50% in high-speed operations, which underpins its lead over other uses. This segment's growth is further validated by 14 million EV sales in 2024, reinforcing automotive as the primary driver for graphene battery adoption in high-stakes mobility solutions.

Regional Insights

North America Graphene Battery Trends

North America spearheads innovation in the graphene battery landscape, with the U.S. leading through robust R&D ecosystems and regulatory support for clean energy. Organizations such as NASA and the National Renewable Energy Laboratory are pushing innovation forward. For example, the SABERS project has reached an energy density of 500 Wh/kg for aviation batteries, improving both safety and efficiency. The Inflation Reduction Act has spurred US$370 Billion in investments, fostering collaborations between startups and automakers to integrate graphene in EVs, reducing charging times by 80%.

This region's focus on sustainability is evident in pilot projects for grid storage, where graphene batteries support renewable integration, backed by ARPA-E grants totaling US$200 Million in 2024 for next-gen tech.

Europe Graphene Battery Trends

Europe's graphene battery trends are shaped by stringent regulations and harmonized policies, with Germany and the U.K. at the forefront due to their automotive prowess and sustainability mandates. The EU Battery Regulation 2023/1542 enforces carbon footprint limits and recycling quotas, promoting graphene for its low-impact production and extended lifespans up to 35% longer than alternatives. In Germany, BASF's cathode initiatives align with the Green Deal, targeting 45% renewables by 2030 and driving graphene adoption in EVs, as seen in Volkswagen's prototypes with 30% better efficiency.

France and Spain contribute through joint ventures under the Graphene Flagship Program, investing €1 Billion (US$1.16 Billion) since 2013 in material science, enhancing battery safety via improved thermal management. These efforts ensure regulatory alignment, boosting market dynamics across the region.

Asia Pacific Graphene Battery Trends

Asia Pacific commands the graphene battery market through manufacturing prowess and rapid EV adoption, led by China, Japan, and India, leveraging policy incentives. China dominates with 67% regional share, supported by CNY1.5 Trillion (US$211.7 Billion) in energy storage plans, where graphene enhances lithium-sulfur batteries for EVs, achieving 50% higher densities. Japan's tech giants such as Panasonic integrate graphene for consumer electronics, with R&D yielding 5x faster charging, backed by government subsidies for clean tech.

Huawei Technologies Co., Ltd. and other regional technology leaders are investing heavily in battery research, while supportive policies in markets such as Japan and South Korea, combined with sophisticated consumer electronics industries demanding high-performance batteries, position Asia Pacific as the critical battleground for graphene battery market expansion.

Competitive Landscape

The global graphene battery market exhibits a moderately fragmented competitive structure characterized by a mix of established battery manufacturers, specialized graphene material producers, and emerging technology startups pursuing differentiated commercialization strategies across various application segments.

Concentration is low, as innovation drives competition, with companies pursuing expansion through strategic partnerships and patent filings, resulting in 5,000 graphene-related patents in 2024 alone. Leaders differentiate via proprietary synthesis methods, such as scalable foils for safety, while emerging models emphasize vertical integration for cost reduction. R&D trends focus on hybrid tech, with investments surpassing US$1 Billion globally, fostering a dynamic landscape ripe for consolidation.

Key Industry Developments

- February 2025: Samsung SDI won the InterBattery Awards 2025 for its 50-Ampere high-power cylindrical battery cell featuring fast-charging technology enabling 80% charge in 15 minutes, with the battery scheduled to launch in the second quarter of 2025, demonstrating continuous innovation in high-performance battery solutions.

- March 2024: Graphene Manufacturing Group secured AU$2 Million (US$1,290,000) funding grant from the Queensland Government for battery pilot plant development, advancing its graphene aluminum-ion battery technology from laboratory development toward commercial-scale production capabilities.

- February 2023: NASA SABERS project advances the solid-state graphene battery, achieving 500 Wh/kg density, doubling lithium-ion performance for EVs and aviation, with tests showing operation at extreme temperatures.

Companies Covered in Graphene Battery Market

- Samsung SDI

- Huawei Technologies Co., Ltd.

- Cabot Corporation

- Nanotech Energy

- VoltaXplore

- Global Graphene Group

- Graphene NanoChem

- Cerebral Energy

- Ascent Solar Technologies

- Soldion Technology

- Sicona

- Graphene Manufacturing Group

Frequently Asked Questions

The graphene battery market is valued at US$242.6 Million in 2025 and expected to reach US$1,156.6 Million by 2032, growing at a 25.0% CAGR driven by EV and renewable demands.

Surging EV adoption, with 14 million units sold in 2024, drives demand as graphene enables 5x faster charging and 45% higher capacity for sustainable mobility.

Lithium-ion leads with 80% share, justified by graphene's conductivity boost for faster charging and longevity in EVs and electronics.

Asia Pacific leads, driven by China's manufacturing scale and investments totaling US$230 Billion in battery tech through 2030.

EV advancements offer key potential, with graphene doubling density to 500 Wh/kg, targeting 25% of the EV battery market by 2030 amid global sustainability pushes.