- Metals & Minerals

- Electrodeposited Copper Foil Market

Electrodeposited Copper Foil Market Size, Share, and Growth Forecast, 2025 - 2032

Electrodeposited Copper Foil Market by Product Type (Single-Sided Copper Foils, Double-Sided Copper Foils), Copper Thickness (Thin Copper Foils (<20 μm), Standard Copper Foils (20–70 μm), Thick Copper Foils (>70 μm)), End Use (Printed Circuit Boards (PCBs), Lithium-ion Batteries, Electromagnetic Shielding, Others (including RFID Antennas and Solar Panels)), and Regional Analysis for 2025 - 2032

Electrodeposited Copper Foil Market Size and Trends Analysis

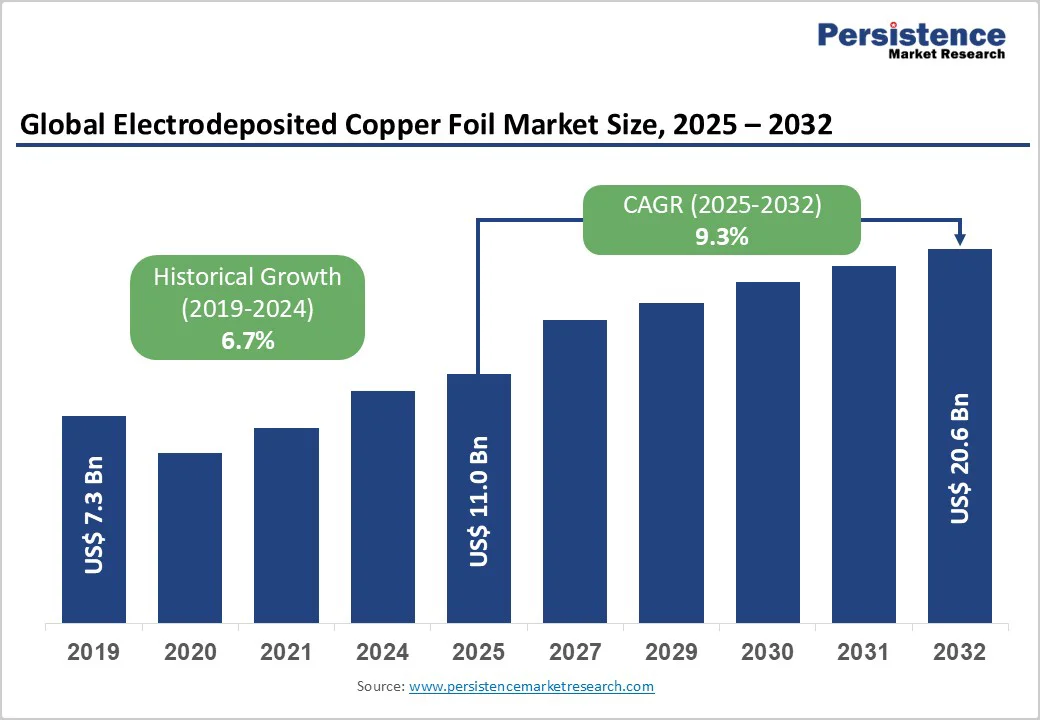

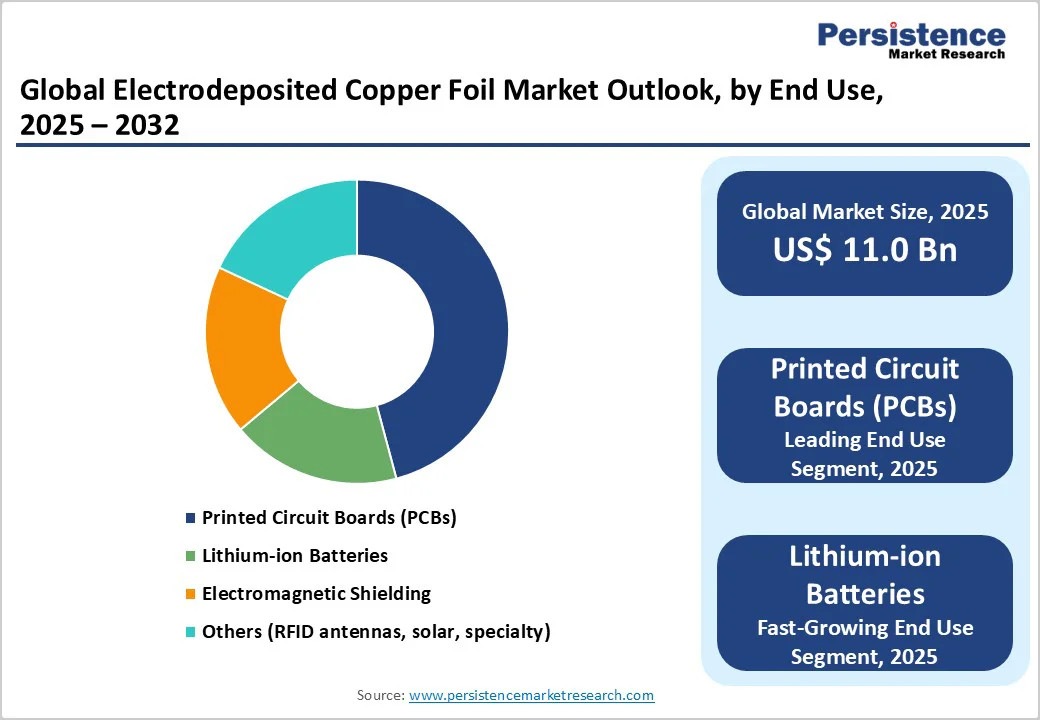

The Global Electrodeposited Copper Foil Market size was valued at US$11.0 billion in 2025 and is projected to reach US$20.6 billion by 2032, reflecting a CAGR of 9.3% between 2025 and 2032.

This robust expansion reflects the market's pivotal role in enabling the global energy transition and digital transformation. The electrodeposited copper foil industry has evolved from a niche supplier of electronic materials into a strategic enabler of sustainable mobility and advanced computing infrastructure.

Market momentum is primarily driven by the unprecedented surge in electric vehicle battery manufacturing, which pushed global EV sales to 17 million units in 2024, a 25% year-on-year increase, directly propelling battery demand beyond the 1 TWh milestone for the first time.

The proliferation of 5G infrastructure, high-performance computing systems, and miniaturised consumer electronics continues to intensify demand for ultra-thin, high-conductivity copper foils with superior thermal management properties.

The market witnessed a fundamental shift in 2024 when battery pack prices fell below the critical USD 100/kWh threshold, making electric vehicles cost-competitive with conventional cars and accelerating adoption rates across all major automotive markets.

This convergence of technological maturation, favourable economics, and supportive regulatory frameworks positions electrodeposited copper foil as an indispensable material in the transition toward electrified transportation and renewable energy storage ecosystems.

Key Industry Highlights:

- Double-sided copper foils hold a dominant 65.5% share, critical for multilayer PCB manufacturing, while single-sided foils grow rapidly in battery applications.

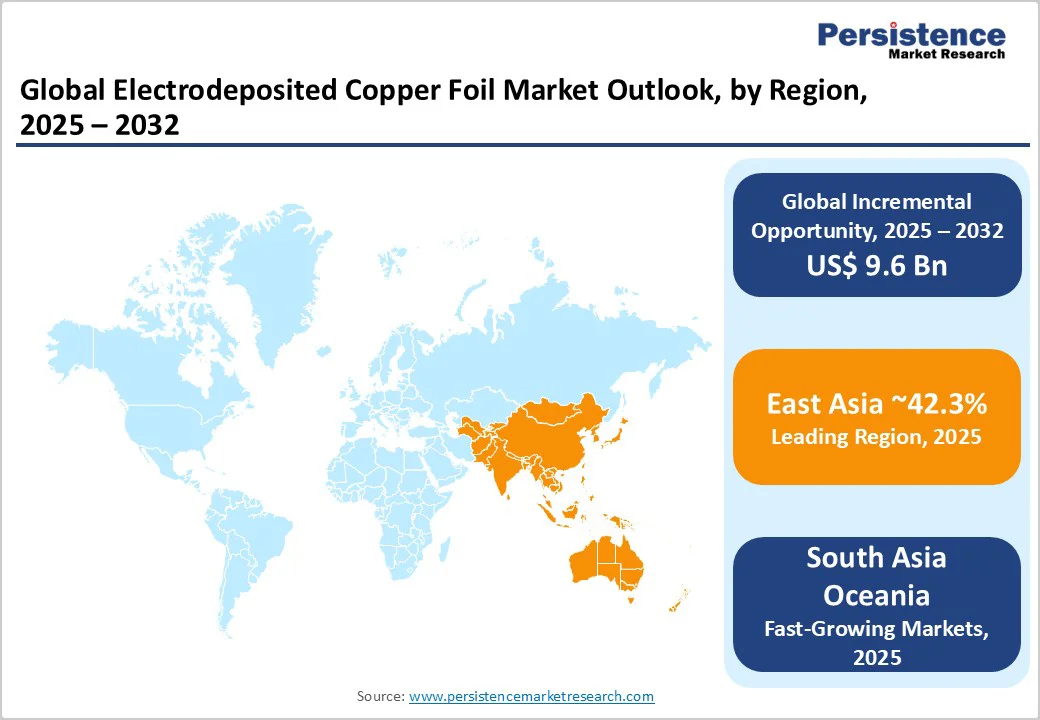

- East Asia dominates with ~42.3% market share, led by China (80% of global capacity), Japan, and South Korea, driven by electronics, automotive, and battery manufacturing.

- North America holds ~15% share, supported by EV electrification and domestic electronics, while South Asia & Oceania account for ~13.8% share, led by India’s EV and electronics expansion.

- Emerging technologies like solid-state batteries, silicon-based anodes, and vehicle-to-grid systems create opportunities for specialised ultra-thin and high-strength copper foils.

- Printed circuit boards (PCBs) lead end-use applications with approximately 55.7% market share in 2025, underpinning copper foil consumption across electronics and automotive sectors.

| Key Insights | Details |

|---|---|

|

Electrodeposited Copper Foil Market Size (2025E) |

US$11.0 Bn |

|

Market Value Forecast (2032F) |

US$20.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

9.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.7% |

Market Dynamics

Growth Drivers

Accelerated Electric Vehicle Production and Lithium-Ion Battery Deployment

The exponential growth of electric vehicle manufacturing represents the most significant catalyst reshaping the electrodeposited copper foil market landscape.

In 2024, global EV battery demand surpassed 750 GWh, a 40% increase from 2022. Copper foil, serving as the critical anode current collector, accounted for approximately 10-13% of battery cell mass and 8-10% of total battery costs.

The United States and Europe experienced the fastest regional growth rates, exceeding 40% year-on-year, while China contributed nearly 60% of total global EV sales volume. Government-backed electrification initiatives continue to provide structural support, including the U.S. Inflation Reduction Act offering tax credits for domestic battery manufacturing, the European Union's target of 100% zero-emission vehicle sales by 2035, and India's FAME India Scheme Phase II, accelerating EV adoption with 45% year-on-year retail growth reaching 167,629 units in April 2025.

The International Energy Agency projects that batteries in EVs will directly contribute to approximately 20% of CO2 emissions reductions required by 2030 on the pathway to net-zero emissions, with copper foil demand for EV batteries increasing sevenfold by the decade's end.

The shift toward thinner copper foils from conventional 8-10 μm to ultra-thin 4.5-6 μm variants enables lithium-ion batteries to achieve 5-11% higher energy density, translating to extended driving ranges and improved vehicle performance.

This technical evolution, combined with the proliferation of energy storage systems for grid-scale renewable integration projected to reach 1,200 GW by 2030, establishes electric mobility and stationary storage as enduring growth pillars for the electrodeposited copper foil industry.

Expansion of High-Performance Electronics and 5G Infrastructure

The relentless advancement of semiconductor technology and telecommunications infrastructure is a driver of demand for electrodeposited copper foil.

Global semiconductor market sales reached a record USD 627.6 billion in 2024, representing 19.1% growth from USD 526.8 billion in 2023, with logic products generating USD 212.6 billion and memory products surging 78.9% to USD 165.1 billion, demonstrating an insatiable appetite for advanced computing capabilities that rely heavily on printed circuit boards incorporating copper foil conductors.

India's PCB market alone is expanding at an exceptional CAGR, driven by the development of the domestic electronics manufacturing ecosystem, automotive electronics integration, and the buildout of 5G telecommunications infrastructure.

The deployment of 5G networks worldwide necessitates specialised copper foils with reduced transmission loss at high frequencies, achieved through proprietary surface-treatment technologies that suppress microconvexities to enable reliable high-speed data communication, exceeding 100 million antenna units projected by 2025.

Multi-layer PCBs, which accounted for over 60% of global PCB production in 2023, require advanced copper foils supporting increasingly complex circuit densities for smartphones, automotive electronic control units, networking equipment, and data centre infrastructure.

Battery storage capacity in the power sector expanded by over 40 GW in 2023, double the previous year's addition, split between utility-scale projects and behind-the-meter systems, both of which require copper foil components for energy storage solutions.

Market Restraining Factors

Raw Material Price Volatility and Supply Chain Vulnerabilities

Copper cathode price fluctuations pose substantial margin pressure on electrodeposited copper foil manufacturers. Copper prices demonstrated 15-20% annual volatility in recent years, driven by global supply chain disruptions, mining production constraints, and shifting trade policies.

In 2023 specifically, global copper prices surged from approximately USD 8,200 per ton to USD 9,600 per ton, increasing upstream material costs by 17%. Latin American and African mining operations experienced production cuts totalling over 400 kilotons due to labour strikes and operational challenges, constraining the primary copper supply.

This unpredictability complicates long-term pricing agreements, particularly for cost-sensitive battery and electronics manufacturers that demand stable pricing structures. The copper foil industry's reliance on a limited number of copper suppliers creates additional supply chain vulnerabilities, as any disruptions due to geopolitical tensions, natural disasters, or trade restrictions significantly impact material availability and cost structures.

Container shortages in 2023 raised shipping costs by 30% for foil exporters, causing 4-6 week delivery delays per container route and limiting consistent output. These logistical constraints force manufacturers to maintain higher inventory buffers, increasing working capital requirements and reducing operational efficiency.

The electrodeposited copper foil manufacturing process is highly energy-intensive, and fluctuations in electricity prices directly affect production economics and profitability. The combination of raw material price volatility, supply chain vulnerabilities, and energy cost fluctuations creates an operating environment in which producers face persistent margin compression that can undermine investment returns and expansion initiatives.

Key Market Opportunities

Expansion into Advanced Battery Technologies and Next-Generation Applications

The development of solid-state batteries, silicon-based anodes, and ultra-high-energy-density systems creates substantial opportunities for specialised copper foil variants with enhanced performance characteristics.

In 2025, Jiayuan Technology launched double-sided nickel-plated copper foil specifically designed to address high-temperature and corrosion challenges in advanced battery chemistries, while also developing copper foil tailored for semi-solid-state battery applications. The adoption of new anode active materials such as silicon oxide (SiOx) and silicon carbide (SiC) requires copper foils with modified mechanical properties, higher tensile strength exceeding 50 kgf/mm2, and specialised surface treatments to accommodate the significant volume expansion during charging cycles.

Battery manufacturers increasingly require copper foil that is thinner, wider, and supplied in longer rolls to improve manufacturing efficiency and reduce production costs, creating opportunities for suppliers who can deliver these advanced specifications.

The grid-scale energy storage market deployed over 3 GWh of battery capacity in Europe and North America during 2023, requiring tens of kilotons of copper foil, with demand projected to grow substantially as renewable energy integration accelerates.

Vehicle-to-Grid (V2G) technology, which enables bidirectional power flow between electric vehicles and electricity grids, represents an emerging application where copper foil ensures efficient power transfer and helps manage electricity flow as EV fleets integrate into smart grid systems.

The development of flexible electronics, wearable devices, and foldable displays, which grew by 22% in developed markets during 2023, demands ultra-thin rolled copper foil with superior flexibility and mechanical reliability.

These next-generation applications command premium pricing and offer differentiation opportunities for manufacturers that can meet stringent technical specifications.

Technological Advancement in Material Engineering

Geographic diversification and regional manufacturing localisation in the global electrodeposited copper foil market present critical investment opportunities driven by supply chain resilience needs and regional content regulations.

Leading OEMs in Europe and North America are establishing local production facilities, targeting 20,000 to 50,000 tons of annual capacity to reduce logistics delays and meet domestic content rules.

Despite North America’s 44.8% year-on-year semiconductor sales growth, supply shortages persist, prompting capacity expansions by producers like Circuit Foil and SK Nexilis. Southeast Asian markets, including Malaysia, Vietnam, and Thailand, offer generous 5–7-year tax holidays to lure copper foil investments supporting the battery and electronics sectors.

New plants like Volta Energy Solution’s 25,000-ton facility in Quebec (2025) and proposed 10,000-ton lines in Texas and Ohio (2026-2027) reflect this shift. Strategic joint ventures link copper foil production directly to battery output, while major government incentives such as India's PLI scheme and the U.S. Inflation Reduction Act encourage domestic production aligned with electrification goals.

These developments reduce dependency on imports, bolster supply chain security, and fulfill rising regional demand in electronics and EV sectors.

Sustainability Leadership Through Circular Economy and Recycling Innovation

The integration of recycled copper and closed-loop manufacturing offers a significant strategic opportunity for the electrodeposited copper foil market to strengthen sustainability leadership.

Furukawa Electric, validated under UL 2809, produces electrolytic copper foil with 100% recycled copper, substantially reducing CO2 emissions compared to virgin copper by leveraging lower energy consumption in recycling.

JX Nippon Mining & Metals has launched 100% recycled copper products and innovative mass-balance schemes that ensure traceability and circularity. The direct use of scrap is gaining traction outside China, mitigating exposure to volatile copper prices.

Battery recycling capacity, projected to reach 1,500 GWh by 2030, will supply secondary copper, promoting circular economy models. Renewable energy integration in production, greener chemical use, and water recycling enhance environmental profiles and compliance with tightening European and North American regulations.

Such innovations not only improve environmental performance but also bolster business resilience and appeal to sustainability-conscious customers.

Category-wise Analysis

Packaging Type Insights

Double-sided copper foils hold a dominant 65.5% market share, driven by their critical function in multilayer printed circuit board (PCB) manufacturing and electronics assembly. Their roughened surfaces on both sides provide superior adhesion with substrates, essential for accommodating the dense, compact components in modern multilayer PCBs.

The boom in smartphones, automotive electronic control units, 5G networking equipment, and data centre systems relies heavily on these foils as a conductive foundation.

Automotive electronics particularly benefit from the space-saving compact designs enabled by double-sided foils. Single-sided copper foils represent the fastest-growing segment, fueled by lithium-ion battery manufacturing for electric vehicles and energy storage. These foils feature a smooth drum-side surface, critical for coating anode active materials such as graphite, thereby maximising battery efficiency.

Ultrafine variants as thin as 4.5-5 μm enhance battery capacity by increasing active material proportion. With global EV battery demand surpassing 750 GWh in 2024 and expected to increase sevenfold by 2030, single-sided copper foils enjoy rapid market expansion, supporting long battery lifespans and superior workability in EV applications.

This product segmentation reflects shifting priorities from traditional electronics to electrification and energy storage, underscoring the dynamic evolution of the copper foil market.

End Use Industry Insights

The printed circuit boards (PCBs) segment leads the electrodeposited copper foil market with approximately 55.7% market share, reflecting PCBs' essential role as the foundation of nearly all electronic devices.

They connect and support components with copper foil circuit pathways, enabling smartphones, tablets, laptops, telecommunications (including 5G infrastructure), automotive electronics, industrial automation, medical, and aerospace systems.

The fastest-growing segment is lithium-ion batteries, driven by the shift to electrification and energy storage. Copper foil, serving as the anode current collector, accounts for 10-13% of the battery cell mass and 8-10% of the total cost, making it critical to performance.

Global lithium battery copper foil shipments reached 52,900 metric tons in October 2024, while China's monthly output increased to 61,700 metric tons, reflecting the rise in EV adoption. Ultra-thin foils (4.5-6 μm) enable up to 11% improvements in energy density, directly extending EV driving range and allaying range anxiety.

Grid-scale and residential battery systems are scaling swiftly, with over 40 GW of battery storage added globally in 2023, doubling 2022's installation rate, creating sustained demand for battery-grade copper foils. Major battery manufacturers like Contemporary Amperex Technology Limited (CATL) continue to expand capacity, cementing lithium-ion batteries as the most dynamic segment of electrodeposited copper foil growth.

Regional Insights and Trends

East Asia

East Asia accounts for approximately 42.3% of the global electrodeposited copper foil market, driven by extensive electronics manufacturing, battery production, and automotive industries in China, Japan, and South Korea.

China, the largest contributor, accounts for around 80% of global capacity as of the end of 2024, with lithium battery copper foil capacity at 1.44 million metric tons and electronic circuit foil at 980,000 metric tons. Key manufacturing hubs in Jiangxi, Guangdong, and Taiwan supply both domestic and international markets.

China’s integrated supply chain includes about 90% of the world’s cathode and over 97% of anode active material production, supporting gigafactories involved in battery cell assembly.

Japan maintains technological leadership with companies like Mitsui Mining and Furukawa Electric, focusing on advanced, ultra-thin foils for high-performance applications. South Korea, led by firms such as SK Nexilis, is expanding capacity to 250,000 tons by 2026, driven by government policy and industry transformation.

Regional EV adoption and automotive electrification underpin consistent demand for copper foil for batteries and printed circuit boards, enabling East Asia to maintain its dominant market position and technological prominence.

South Asia Oceania Market Trend

South Asia & Oceania hold a 13.8% share of the global electrodeposited copper foil market, propelled by expanding electronics manufacturing and rising electric vehicle adoption, with India leading industrial growth.

India's EV and electronics sectors grew 22% year-over-year in 2023, supported by major companies like Hindalco, Sterlite Copper, Bhagyanagar India, and international entrants such as JX Nippon Mining & Metals, which expanded operations.

Despite over 50% import dependence on copper raw materials, significant opportunities arise from government initiatives, including the Production-Linked Incentive (PLI) scheme, National Electricity Plan battery targets, and foreign investment facilitation. The automotive sector’s electrification drives demand as EVs require extensive battery and PCB copper foil content.

Technological partnerships with firms like IIT Mumbai and Japanese companies advance India's foil production capabilities and narrow the technology gap. Domestic manufacturers diversify into ultra-thin foils for high-density electronics and lithium-ion batteries, addressing rising local demand.

Challenges remain with limited domestic ore output and an underdeveloped secondary copper recycling infrastructure. The upcoming enforcement of the Extended Producer Responsibility (EPR) regime for copper in 2025 aims to enhance circular economy practices, improving resource security and sustainability in the region.

North America Market Trend

North America holds a 15% share of the global electrodeposited copper foil market, driven by strong consumption supporting automotive electrification, domestic electronics manufacturing, and renewable energy infrastructure.

In 2023, U.S. electric vehicle battery demand grew 17% year-over-year, reaching approximately 100 gigawatt-hours, alongside ambitious plans to triple domestic chip production by 2032 to bolster supply chain resilience. Battery factory expansions by Panasonic, Samsung, SK On, and automakers like Ford and Toyota aim to increase U.S. production capacity by 90% from 2024 levels.

Policy incentives under the Inflation Reduction Act, including tax credits tied to domestic content, encourage investment in localised copper foil production. Investment in new facilities such as Volta Energy Solutions' USD 750 million copper foil plant in Quebec demonstrates a commitment to strengthening North American supply chains.

This market environment emphasises the need for continued investment and innovation to capture emerging growth opportunities while mitigating supply chain risks.

Competitive Landscape

The global electrodeposited copper foil market is moderately consolidated, dominated by a handful of large, technologically advanced producers catering to PCBs, lithium-ion batteries, and high-end electronics. Key players include Furukawa Electric Co., Ltd., Fukuda Metal Foil & Power Co., Ltd., Circuit Foil, Doosan Corporation Electro, JX Nippon Mining & Metals, and LS Mtron Ltd. Competition is driven by capacity expansions, technological innovation, and sustainability initiatives, including recycled copper foils and ultra-thin high-performance variants.

Emerging regional players in Southeast Asia are increasing market fragmentation by offering cost-competitive production. Strategic collaborations with battery manufacturers and government incentives further shape competitive positioning.

Key Industry Developments

- On January 9, 2025, Fukuda Metal Foil & Powder Co., Ltd. announced that UL Solutions validated several electrodeposited copper foil types (SV, HD, UN, HS, HTE, STD) as made from 100% recycled copper, aligned with ISO 14021 standards. This certification strengthens Fukuda’s sustainability credentials and positions its eco-friendly foils for the growing demand in PCBs, lithium-ion batteries, and other electronics applications.

- On August 20, 2025, Mitsui Mining & Smelting Co., Ltd. announced a 45% expansion of VSP™ electro-deposited copper foil production at its Taiwan and Malaysia plants, increasing capacity from 580 tons to 840 tons per month by September 2026. The high-frequency copper foils used in servers, routers, switches, and AI server infrastructure address the growing demand for reduced transmission loss in advanced communication equipment, reflecting accelerated market adoption in high-performance electronics.

Companies Covered in Electrodeposited Copper Foil Market

- Industrie De Nora S.p.A.

- Doosan Corporation Electro

- Furukawa Electric Co., Ltd.

- Fukuda Metal Foil & Powder Co., Ltd.

- Circuit Foil

- Chang Chun Group

- LS Mtron Ltd.

- Mitsui Mining & Smelting Co., Ltd.

- JX Nippon Mining & Metals Corporation

- ILJIN Materials Co., Ltd.

- Targray Technology International, Inc.

- Nippon Denkai, Ltd.

- All Foils, Inc.

- Oak-Mitsui Technologies LLC

- Rogers Corporation

- Total Materia

- Tex Technology Inc.

Frequently Asked Questions

The global Electrodeposited Copper Foil market is projected to be valued at US$ 10.1 Bn in 2025.

The Printed Circuit Boards (PCBs) segment is expected to hold around 55.7% market share by end-use industry in 2025, driven by the rapid expansion of consumer electronics, automotive electronics, industrial automation, medical devices, aerospace systems, and 5G infrastructure requiring advanced multi-layer PCBs incorporating high-performance copper foils.

The Electrodeposited Copper Foil market is expected to witness a CAGR of 9.3% from 2025 to 2032.

The electrodeposited copper foil market is driven by rapid EV and lithium-ion battery adoption, expansion of high-performance electronics, 5G infrastructure, and growing demand for advanced PCBs and energy storage systems.

Key market opportunities lie in advanced battery technologies, next-generation electronics, regional manufacturing expansion, and sustainable recycled copper solutions, driving growth and differentiation.