- Display Technologies

- Flexible Electronics Market

Flexible Electronics Market Size, Share, and Growth Forecast 2026 - 2033

Flexible Electronics Market by Product Type (Flexible Displays, Flexible Sensors, Flexible Batteries, Flexible Printed Circuits, Others), Material (Polymers, Thin-Film Materials, Metal Foils, Nanomaterials, Hybrid Materials), Technology (Printed Electronics, Roll-to-Roll Processing, Thin-Film Deposition, Organic Electronics, Hybrid Integration), Application, Industry, and Regional Analysis, 2026 - 2033

Flexible Electronics Market Size and Trend Analysis

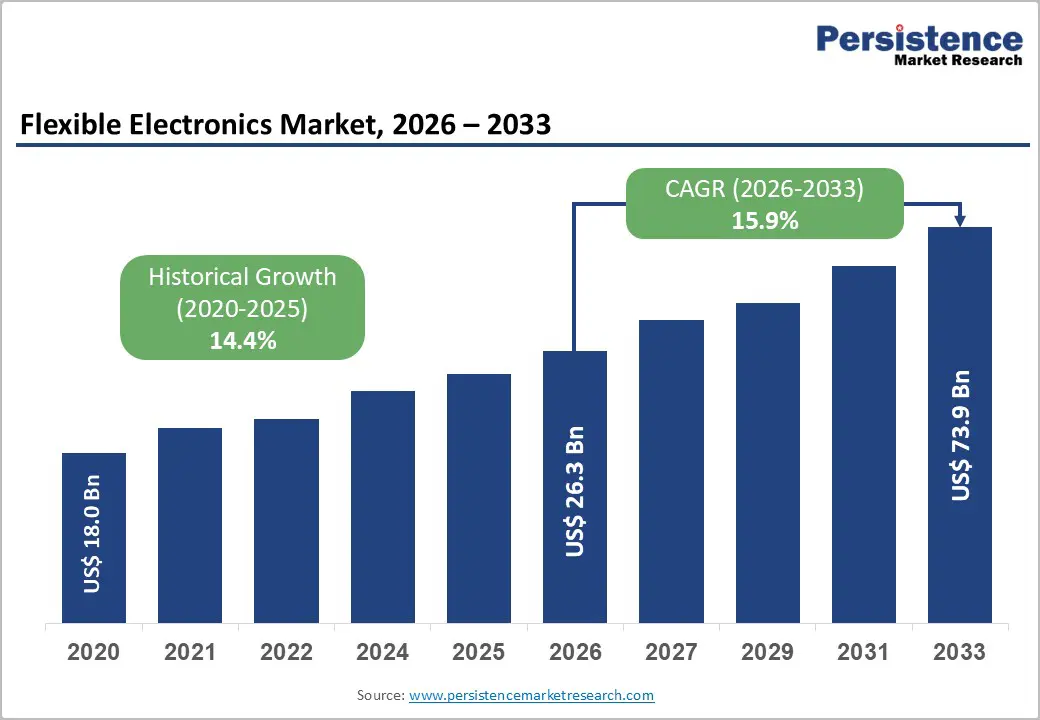

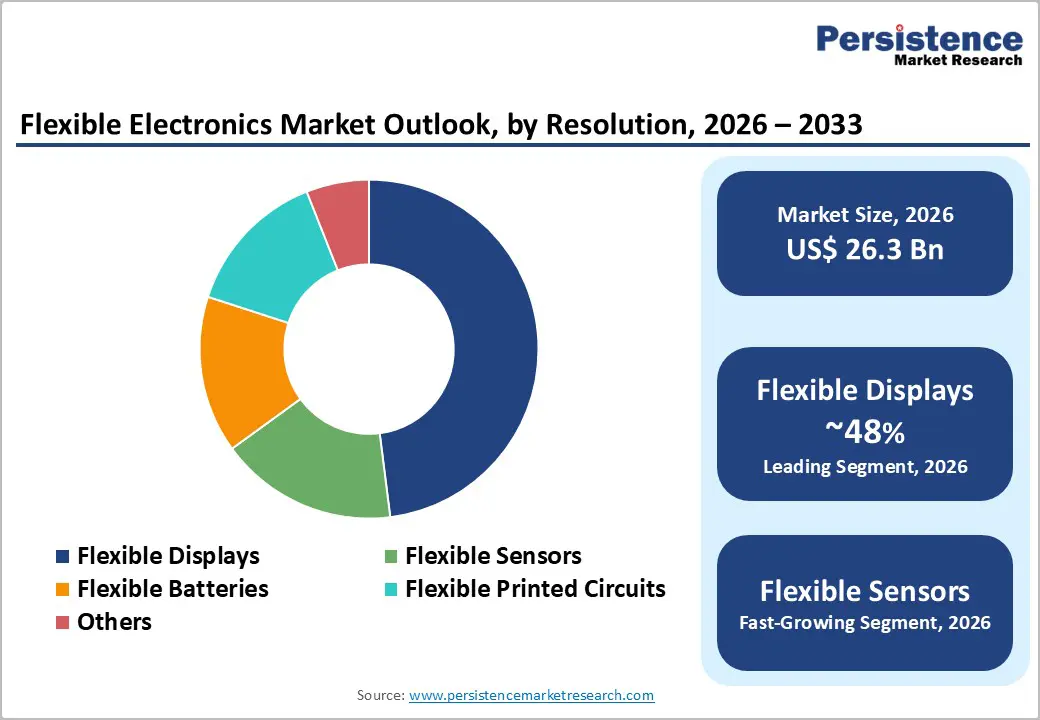

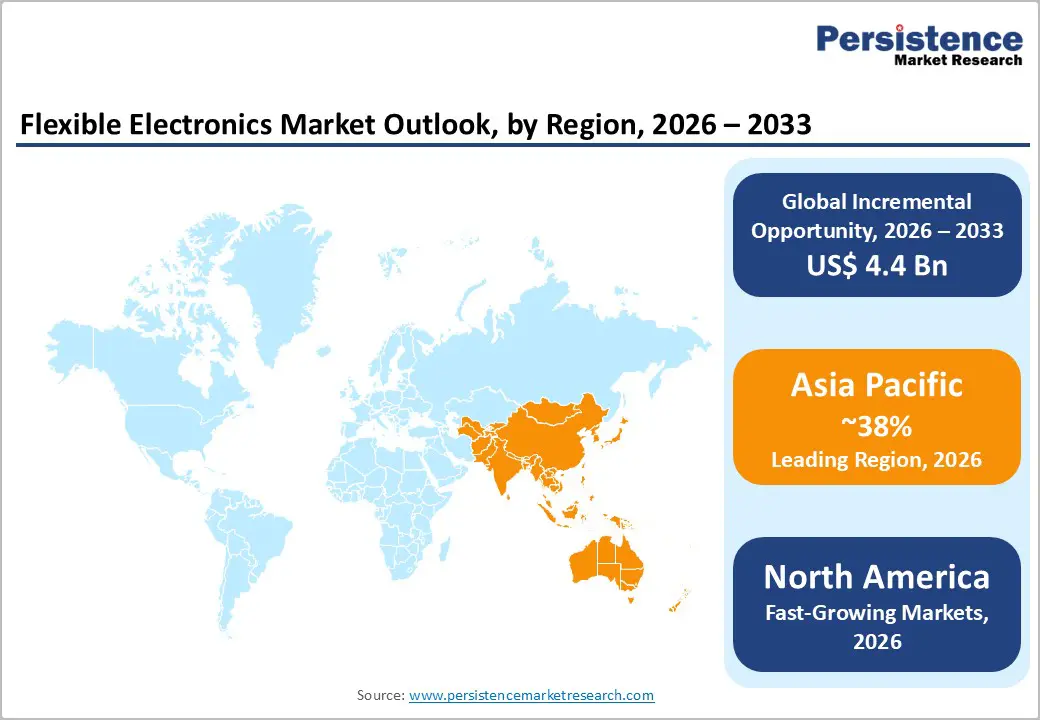

The global flexible electronics market is projected to reach US$ 26.3 billion in 2026 and US$ 73.9 billion by 2033, growing at a CAGR of 15.9% over the forecast period. The accelerating demand for miniaturized, energy-efficient consumer devices and the integration of Internet of Things (IoT) ecosystems are the primary forces driving this expansion.

Key Industry Highlights:

- Leading Region: Asia-Pacific dominates the market, holding a 38% share, owing to global production capacity and consumer demand.

- Fastest Growing Region: North America is the fastest-growing region, driven by rapid adoption in digital healthcare and military R&D.

- Dominant Segment: Consumer Electronics is the dominant segment with 55% share, sustained by global smartphone and wearable sales.

- Fastest Growing Segment: Healthcare is the fastest growing segment with 17% CAGR, accelerated by remote patient monitoring and smart patch adoption.

- Key Market Opportunity: Smart Packaging. High-volume potential for logistics tracking and food safety.

| Key Insights | Details |

|---|---|

| Flexible Electronics Market Size (2026E) | US$ 26.3 Billion |

| Market Value Forecast (2033F) | US$ 73.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 15.9% |

| Historical Market Growth (2020 - 2025) | 14.4% |

Market Dynamics

Drivers - Growing adoption of skin-conformal medical wearables accelerates demand for flexible sensors, circuits, and real-time digital health monitoring solutions

The rapid growth of wearable health technology is a major driver for the flexible electronics market. Demand for remote patient monitoring devices is rising as healthcare systems shift toward preventive and continuous care models. Flexible sensors and batteries play a vital role in next-generation medical wearables, including smart patches, fitness trackers, and continuous glucose monitoring systems. These devices must conform comfortably to human skin to deliver accurate and reliable health data.

Unlike rigid electronic components, flexible substrates allow seamless integration into clothing or direct skin application without restricting movement or causing discomfort. This improves patient compliance and data accuracy. According to the World Health Organization, the growing prevalence of chronic diseases such as diabetes and cardiovascular disorders is accelerating the adoption of digital health solutions. As a result, healthcare providers are increasingly investing in flexible circuits and biological sensors that combine comfort, durability, and real-time diagnostic precision, creating sustained long-term market demand.

Rising use of intelligent packaging and smart labels enhances supply chain visibility, driving the adoption of printed flexible electronic components

The expansion of smart packaging and logistics solutions is strongly driving the adoption of flexible electronics across the retail and supply chain industries. Companies are increasingly replacing traditional barcodes with printed smart labels, thin-film transistors, and flexible sensors to gain real-time visibility into product condition, location, and freshness. This trend is especially prominent in the food and pharmaceutical sectors, where maintaining temperature control and product integrity is critical.

Flexible electronics enable continuous monitoring throughout transportation and storage, reducing spoilage and compliance risks. Industry insights from the Association for Packaging and Processing Technologies indicate a growing shift toward intelligent packaging that interacts with smartphones via NFC. These smart packages improve consumer engagement, enhance brand transparency, and support better inventory decisions. Additionally, improved tracking capabilities help minimize waste and operational losses. As costs decline, low-cost printed flexible electronic components are increasingly being adopted at scale across global supply chains.

Restraint - Moisture sensitivity and costly encapsulation requirements limit the durability, lifespan, and affordability of flexible electronic devices

Technical challenges related to encapsulation and durability remain a major restraint for the flexible electronics market. Many flexible electronic devices rely on organic materials that are highly sensitive to environmental factors, including moisture, oxygen, and heat. This sensitivity significantly reduces device lifespan when compared to traditional rigid silicon-based electronics. Flexible OLED displays and photovoltaic cells are particularly susceptible to degradation in the absence of appropriate protective barriers. Developing advanced encapsulation solutions that provide strong protection while remaining thin, flexible, and crack-resistant is a complex engineering challenge.

High-performance barrier films are expensive and increase overall production costs. As a result, the final product price becomes higher, limiting adoption in cost-sensitive markets such as entry-level consumer electronics. These durability concerns also affect product reliability, thereby slowing adoption in applications where a long operational life is critical. Until cost-effective and scalable encapsulation solutions are developed, market expansion may remain constrained.

High capital requirements and complex roll-to-roll manufacturing processes restrict scalability and limit new market entrants

Despite its long-term potential, the manufacturing process for flexible electronics remains complex and challenging. While roll-to-roll processing promises lower costs and high-volume production, achieving consistent quality at scale is difficult in practice. Precise alignment and registration of multiple functional layers on continuously moving flexible substrates require advanced control systems and high capital investment. Even minor defects, such as misalignment, ink spreading, or pinholes, during printing can lead to significant production losses.

These yield issues significantly increase manufacturing risk and cost. Additionally, maintaining uniform performance across large batches remains a technical hurdle. As a result, smaller companies often struggle to compete with established players that have the financial resources to invest in advanced production infrastructure. Industry leaders such as Samsung and LG Electronics benefit from scale and process expertise, creating high entry barriers. These manufacturing complexities limit market diversification and slow innovation from new entrants.

Opportunities - Rising consumer demand for foldable, rollable displays creates opportunities for advanced flexible materials and durable display technologies

The rapid evolution of foldable and rollable consumer devices presents a major growth opportunity for the flexible electronics market. Consumers increasingly demand larger displays combined with compact, portable form factors, pushing manufacturers to innovate beyond traditional device designs. Smartphone, laptop, and television manufacturers are investing heavily in scrollable and multi-fold display technologies to differentiate their premium products. Leading companies such as LG Electronics are already commercializing rollable displays, signaling strong future demand.

The key opportunity lies in developing durable materials, advanced hinge mechanisms, and ultra-thin glass composites that can withstand repeated folding without performance loss. Addressing common issues such as visible creases, material fatigue, and optical distortion is critical. Companies that successfully deliver reliable, crease-free displays with long life cycles will gain a competitive edge. As premium device adoption grows, flexible electronics suppliers stand to capture significant value across high-margin consumer segments.

Smart cockpit designs and lightweight vehicle requirements drive the integration of flexible displays and printed electronics in automotive interiors

The automotive industry represents a high-potential opportunity for flexible electronics, particularly as vehicles evolve into digitally enhanced smart cockpits. Modern vehicle designs emphasize sleek, curved interiors with minimal physical controls, creating demand for flexible displays and touch-sensitive surfaces. Flexible electronics can be seamlessly integrated into dashboards, door panels, steering wheels, and A-pillars, replacing bulky mechanical buttons. This enables intuitive human-machine interfaces while enhancing interior aesthetics.

Electric vehicle manufacturers, in particular, are adopting flexible electronics to improve energy efficiency and reduce overall vehicle weight. Printed circuits and flexible displays are lighter than traditional copper wiring and rigid screens, supporting longer driving ranges. Additionally, regulatory pressure from regions such as the European Union encourages lightweight vehicle designs. As automotive OEMs prioritize digitalization and user experience, flexible electronics offer a compelling solution that combines design freedom, functionality, and performance benefits.

Category-wise Analysis

Product Type Insights

Flexible displays dominate the product type segment, accounting for approximately 48% of the overall market share. This leadership is primarily driven by the widespread adoption of OLED technology in smartphones, smartwatches, and wearable devices. Leading OEMs have increasingly integrated curved and foldable displays into flagship products to stand out in a highly competitive consumer electronics market. Continuous improvements in resolution, brightness, and color accuracy have made flexible displays comparable in quality to traditional rigid screens.

Manufacturing these displays on plastic substrates rather than glass significantly reduces breakage risk, thereby improving durability and user experience. Flexible displays also enable innovative device designs, supporting thinner profiles and lightweight construction. As consumer demand for premium and differentiated devices continues to rise, manufacturers are expected to further standardize flexible displays across product lines. This ongoing innovation solidifies flexible displays as the most influential and commercially successful segment.

Material Insights

Polymers dominate the materials category, accounting for approximately 42% of the total market volume. Materials such as polyimide (PI) and polyethylene terephthalate (PET) are widely used due to their excellent thermal stability, flexibility, and cost-effectiveness. These polymers can withstand high processing temperatures while maintaining mechanical strength, making them ideal substrates for flexible electronics.

Unlike glass or metal foils, polymer substrates are fully compatible with roll-to-roll manufacturing, enabling large-scale and efficient production. Their lightweight nature is particularly important for applications such as wearables, aerospace components, and portable consumer devices, where reducing weight improves performance and comfort. Polymers also offer design versatility, allowing electronics to be bent, rolled, or folded without damage. As manufacturers continue to seek scalable and economical solutions, polymers are expected to remain the foundational material supporting innovation and growth across the flexible electronics industry.

Technology Insights

Printed electronics is the fastest-growing technology segment within the flexible electronics market. Although thin-film deposition currently holds a strong share due to its widespread use in display manufacturing, printed electronics are gaining momentum because of their cost and sustainability advantages. This technology enables direct printing of conductive inks, sensors, and antennas onto flexible substrates, eliminating complex lithography and etching processes used in traditional semiconductor manufacturing. As a result, production costs are significantly reduced, and material waste is minimized.

Printed electronics are particularly well-suited for high-volume, low-complexity applications such as IoT sensors, RFID tags, and smart packaging components. The ability to economically manufacture billions of devices supports rapid scalability. Growing demand for connected devices across industries further accelerates adoption. As performance improves and production yields increase, printed electronics are expected to play a critical role in expanding flexible electronics into mass-market applications.

Application Insights

Consumer electronics represent the largest application segment, accounting for approximately 55% of total market demand. This dominance is driven by the massive global sales volume of smartphones, tablets, wearables, and e-readers. Flexible electronics are no longer limited to displays; they now include flexible batteries, sensors, and circuits that enable slimmer, lighter, and more ergonomic device designs.

Major technology companies follow rapid annual product refresh cycles, ensuring consistent and recurring demand for advanced components. Additionally, emerging product categories such as hearables, augmented reality, and virtual reality headsets rely heavily on lightweight and contoured electronics for user comfort and performance. Flexible components allow manufacturers to deliver innovative form factors while improving durability. As consumers increasingly prioritize portability and aesthetics, flexible electronics continue to play a central role in shaping next-generation consumer devices, reinforcing the segment’s long-term leadership.

End-user Insights

Healthcare is emerging as one of the fastest-growing end-use industries for flexible electronics. Although smaller than consumer electronics, the segment is expanding rapidly due to the digital transformation of healthcare. Healthcare providers are increasingly adopting non-invasive monitoring solutions such as electronic skin patches and smart bandages that can track vital signs, wound healing, and drug delivery. Flexible electronics enable continuous, real-time data collection without restricting patient movement or comfort.

Clinical studies indicate that continuous monitoring significantly reduces hospital readmissions and improves patient outcomes. These measurable benefits are driving hospitals, insurers, and healthcare systems to invest in wearable medical technologies. Flexible electronics also support remote care models, reducing overall healthcare costs. As aging populations and the prevalence of chronic diseases increase globally, demand for flexible, patient-friendly medical devices is expected to accelerate, making healthcare a key long-term growth engine.

Regional Insights

North America Flexible Electronics Market Trends

North America remains a leading hub for innovation and research in the flexible electronics market, with the United States at the forefront. The region benefits from a strong ecosystem of technology startups, academic institutions, and research centers such as Palo Alto Research Center (PARC). These organizations drive advancements in printed electronics, sensing materials, and flexible logic systems. A notable regional trend is strong investment in defense and aerospace applications, supported by funding from the U.S. Department of Defense.

Research initiatives focus on lightweight flexible solar panels, wearable communication systems, and energy-efficient devices for military use. Additionally, North America’s advanced healthcare infrastructure accelerates the adoption of medical wearables and remote monitoring technologies. The presence of major technology companies and venture capital in Silicon Valley enables the rapid commercialization of innovations, strengthening the region’s leadership in high-value flexible electronics development.

Europe Flexible Electronics Market Trends

Europe is positioning itself as a key player in flexible electronics by emphasizing sustainability and industrial applications. Countries such as Germany and the United Kingdom lead adoption, driven by strong automotive and manufacturing sectors. Strict environmental regulations, including EU directives on electronic waste, are encouraging the development of organic, recyclable, and biodegradable flexible electronics. The automotive industry plays a major role, with European luxury car manufacturers integrating flexible displays and touch-sensitive surfaces into vehicle interiors to enhance user experience.

Europe also leads in structural electronics, where electronic functions are embedded directly into building materials, vehicle components, and industrial structures. This approach reduces component count, simplifies assembly, and improves efficiency. Strong collaboration between industry, research institutions, and government programs supports innovation. As sustainability becomes a global priority, Europe’s focus on eco-friendly flexible electronics is expected to drive long-term growth.

Asia Pacific Flexible Electronics Market Trends

The Asia Pacific region dominates global flexible electronics manufacturing and holds the largest volume share. Countries such as China, South Korea, and Japan host major display, battery, and semiconductor manufacturers, including Samsung and LG Electronics. The region continues to expand production capacity for OLED displays and flexible batteries to meet rising global demand. Government support plays a crucial role, particularly in China, where subsidies encourage domestic production of semiconductor materials and flexible substrates.

These initiatives aim to strengthen supply chain independence and technological leadership. The region’s large consumer base allows rapid testing and adoption of new device form factors, such as foldable smartphones and wearable technologies. High consumer acceptance accelerates product refinement and commercialization. With strong manufacturing capabilities, skilled labor, and government backing, Asia Pacific is expected to remain the backbone of global flexible electronics production.

Competitive Landscape

The flexible electronics market exhibits a mixed structure, with high consolidation in premium segments and fragmentation in specialized component areas. High-value segments such as flexible displays and batteries are dominated by large players like Samsung and LG Electronics, due to the massive capital investment required for OLED fabrication facilities. These companies benefit from economies of scale, advanced process expertise, and strong intellectual property portfolios. In contrast, niche segments such as printed sensors and flexible circuits have lower entry barriers, resulting in a fragmented competitive landscape.

Specialized companies like Blue Spark Technologies and E Ink Holdings compete through innovation and application-specific expertise. Industry strategies are increasingly focused on vertical integration, where material suppliers collaborate closely with device manufacturers to improve yields and performance. Research and development efforts are shifting toward hybrid electronics that combine rigid chips with flexible substrates, enabling high performance with enhanced design flexibility.

Key Market Developments:

- January, 2026: Samsung Display introduced AI-enabled foldable OLED panels at CES 2026, featuring a 20% reduction in crease depth and low-power variable refresh rate technology. These advancements improve durability, visual quality, and energy efficiency for next-generation foldable consumer devices.

- January, 2024: Blue Spark Technologies launched VitalTraq, a multi-sensor remote patient monitoring platform designed for home-based care. The system leverages proprietary flexible batteries and sensors to deliver continuous, clinical-grade vital sign monitoring, supporting preventive and remote healthcare models.

- April, 2025: E Ink Holdings Inc. partnered with BMW to integrate Prism 3 color-changing film into vehicle exteriors, enabling dynamic color and pattern changes. This collaboration enhances vehicle customization, energy efficiency, and functional signaling applications in next-generation automotive design.

Companies Covered in Flexible Electronics Market

- AU Optronics Corp.

- Blue Spark Technologies

- Cymbet Corporation

- E Ink Holdings Inc.

- Enfucell Softbattery

- 3M

- First Solar

- General Electric

- ITN Energy Systems Inc.

- LG Electronics

- MFLEX

- Palo Alto Research Center LLC (PARC)

- SAMSUNG

- SOLAR FRONTIER K.K.

Frequently Asked Questions

The global market is projected to reach a value of US$ 73.9 Billion by the end of 2033.

Key drivers include the rising adoption of wearable health devices, the expansion of IoT ecosystems, and the demand for lightweight, durable components in automotive and aerospace sectors.

Flexible Displays hold the dominant share, largely driven by the widespread production of OLED screens for smartphones, smartwatches, and next-generation televisions.

Asia Pacific is expected to lead the market due to its massive electronics manufacturing infrastructure, particularly in China, South Korea, and Taiwan.

The development of smart packaging solutions utilizing printed electronics for real-time logistics tracking and food safety monitoring represents a significant revenue opportunity.

Major players include Samsung, LG Electronics, E Ink Holdings Inc., Blue Spark Technologies, 3M, and AU Optronics Corp., among others.