- Nutraceuticals & Functional Foods

- Customized Premixes Market

Customized Premixes Market Size, Share, and Growth Forecast, 2026 - 2033

Customized Premixes Market by Nutrient Type (Vitamins, Minerals, Amino Acids, Nutraceuticals), Application (Food & Beverages, Dietary Supplements, Pharmaceuticals, Animal Feed), Form (Liquid, Powder), and Regional Analysis for 2026-2033

Customized Premixes Market Share and Trends Analysis

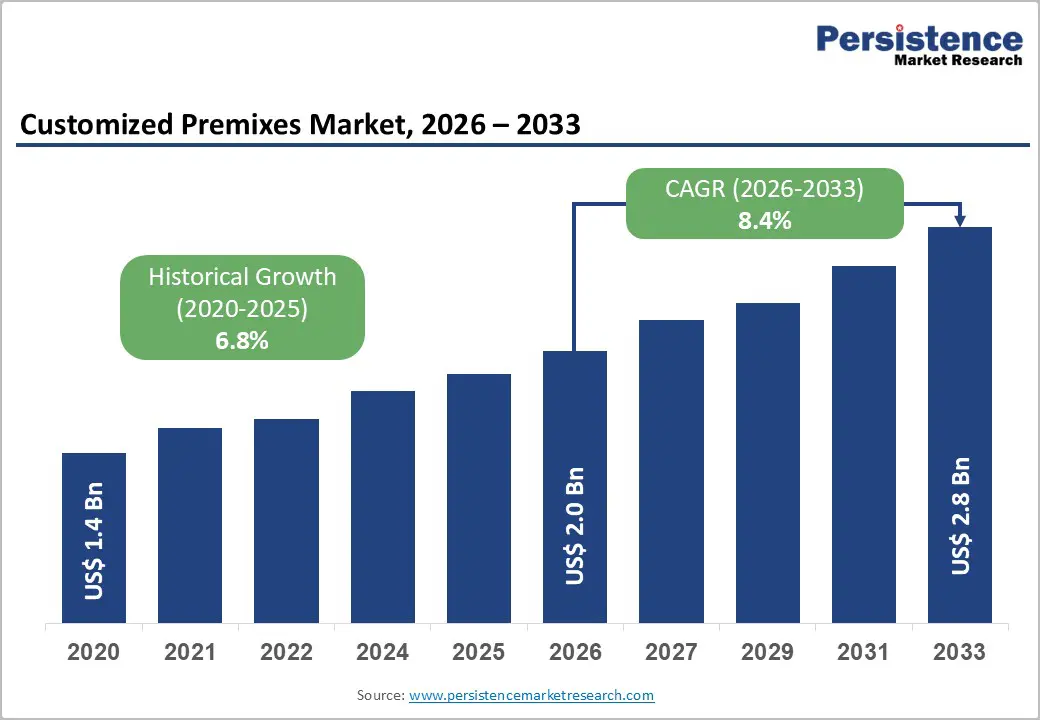

The global customized premixes market size is likely to be valued at US$ 2.0 billion in 2026, and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 8.4% during the forecast period 2026−2033. Growth is being supported by surging demand for fortified food and beverage products across both developed and emerging economies. Consumers are becoming more aware of micronutrient deficiencies such as iron, vitamin D, and vitamin B complex shortages, and they are actively seeking preventive nutrition solutions. Governments and regulatory bodies are implementing structured food fortification programs, particularly for staple foods such as flour, rice, and edible oils.

These initiatives are increasing institutional demand for customized vitamin and mineral blends tailored to local dietary gaps. The market is increasingly aligning with preventive healthcare strategies and personalized nutrition trends. Food and beverage manufacturers are integrating tailored micronutrient combinations into functional foods, dairy products, and ready-to-drink beverages to meet specific health positioning claims. Dietary supplement companies are expanding product portfolios with condition-specific premixes targeting immunity, bone health, and metabolic support. Pharmaceutical manufacturers are incorporating precision nutrient blends into therapeutic formulations where compliance with regulatory standards is critical. As consumer awareness is improving and regulatory oversight is strengthening, manufacturers are investing in advanced blending technologies, quality assurance systems, and traceability platforms.

Key Industry Highlights

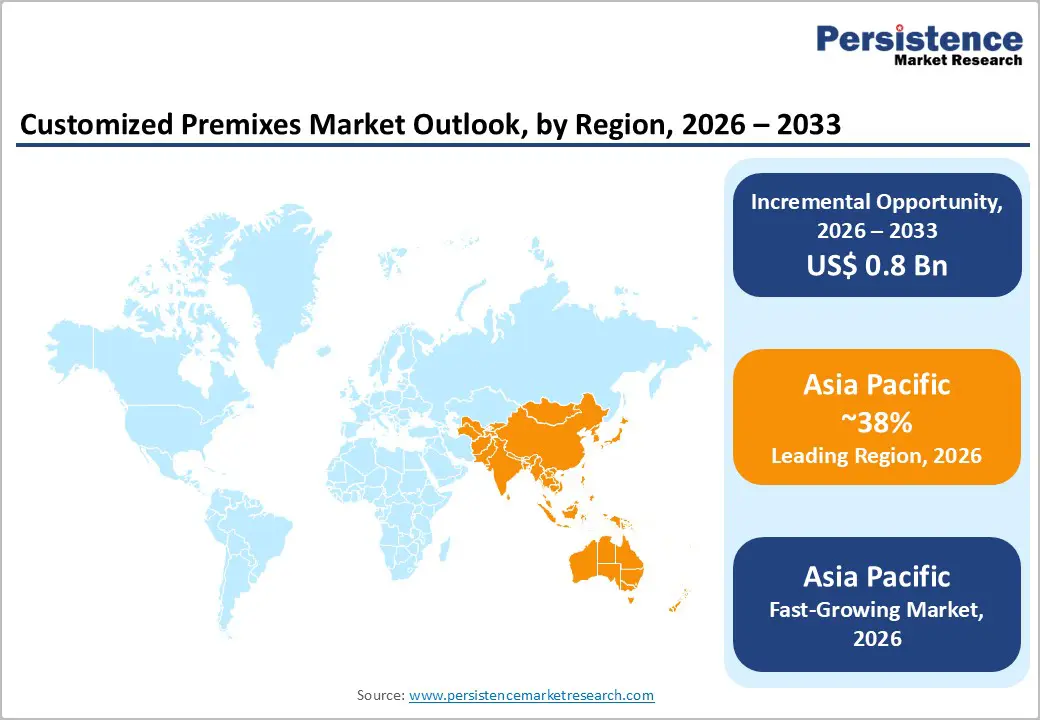

- Regional Dominance: Asia Pacific is set to be the dominant and the fastest-growing market with a projected 38% market share in 2026, supported by the presence of large underserved populations and strong government nutrition initiatives.

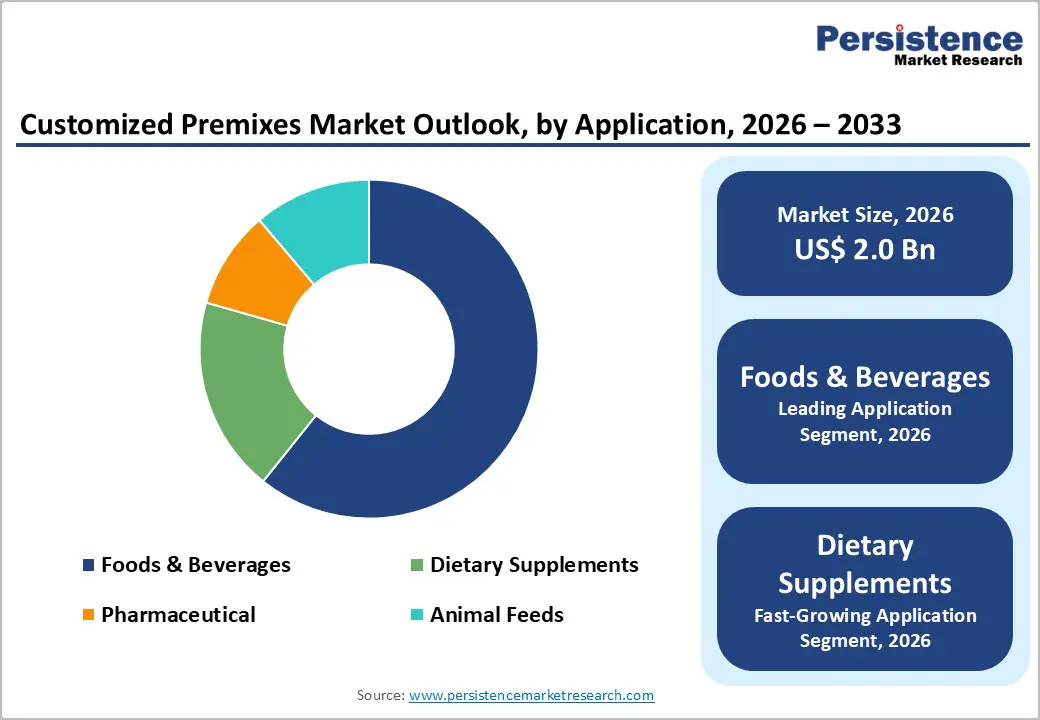

- Application Leadership: Food & beverages is likely to hold an estimated revenue share of 65% in 2026, while dietary supplements are expected to be the fastest-growing segment through 2033.

- Leading & Fastest-growing Form: Powdered premixes are poised to lead with an approximate 75% market share in 2026, whereas liquid variants are anticipated to be the fastest-growing during the 2026-2033 forecast period.

- Market Driver: Rising demand for functional foods and government fortification mandates are accelerating the adoption of customized premixes, with technological advances in nutrient delivery systems enabling precise and stable formulations.

- Market Opportunity: Personalized nutrition platforms are stoking premium small-batch manufacturing demand, while the Asia Pacific market offers volume growth through mandatory staple fortification programs.

| Key Insights | Details |

|---|---|

| Customized Premixes Market Size (2026E) | US$ 2.0 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 1.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Micronutrient Deficiencies

According to the World Health Organization (WHO), over 2 billion people worldwide suffer from micronutrient deficiencies, particularly iron, vitamin A, and iodine deficiencies. These gaps in dietary intake undermine immune function, cognitive development, and productivity, affecting vulnerable groups such as children, women of reproductive age, and low-income populations. The Global Nutrition Report underscores the scale of malnutrition, emphasizing that it is not limited to low-income countries but also affects emerging and developed economies through both undernutrition and poor-quality diets. This context is prompting policymakers, donors, and industry stakeholders to increasingly view food fortification as a practical, scalable tool within broader nutrition and health strategies.

In this environment, government-led fortification programs, such as India’s National Nutrition Mission and parallel initiatives across Southeast Asia and Africa, are playing a catalytic role in reshaping food systems. Regulators in these regions require the addition of essential nutrients to staple products such as flour, rice, oils, and salt, which encourages food manufacturers to reformulate portfolios and embed fortification into their core product development strategies. As companies respond, they rely on customized premixes to provide precise, compliant blends that align with local deficiency patterns, stability needs, sensory expectations, and regulatory specifications. Tailored premix solutions reduce formulation risk, shorten development timelines, and support consistent quality, thereby turning public health mandates into structured market opportunities and long-term competitive advantages.

Regulatory Complexity and Regional Variation in Fortification Standards

Manufacturers encounter substantial hurdles in the customized premixes market because regulatory frameworks differ widely across regions. The European Food Safety Authority (EFSA), U.S. Food and Drug Administration (FDA), and Food Safety and Standards Authority of India (FSSAI) establish unique standards for nutrient fortification. These variations in maximum permitted levels for vitamins and minerals force companies to develop separate formulations for each market. Therefore, maintain diverse product portfolios, which complicates inventory control and raises operational complexity for global supply chains.

Regulatory demands extend beyond fortification limits to include labeling protocols, health claim validations, and approved nutrient sources. Compliance requires specialized expertise and extensive documentation tailored to each jurisdiction. Frequent regulatory updates, such as revised permitted levels or expanded mandatory fortification requirements, introduce ongoing uncertainty. This landscape underscores the value of investing in dedicated regulatory intelligence teams and flexible manufacturing systems. Such proactive measures enable companies to convert compliance challenges into competitive advantages through faster market adaptation and reduced reformulation expenses.

Personalized Nutrition and Direct-to-Consumer Models

Personalized nutrition is emerging as a structural growth avenue for customized premixes within direct-to-consumer supplement brands and digital health platforms. Companies are using genetic testing, microbiome analysis, and detailed health assessments to generate individualized nutrient recommendations. These business models are requiring agile premix manufacturing that supports small-batch production and frequent reformulation cycles. Traditional large-scale blending facilities are not always meeting these responsiveness requirements. Manufacturers that are investing in flexible production lines and modular blending systems are positioning themselves to serve this evolving demand. Rapid prototyping capabilities are enabling faster product validation and shorter commercialization timelines. As new digital-first supplement brands are entering the market, premix suppliers that are offering formulation support and regulatory guidance are securing premium, long-term supply agreements.

This transition from standardized mass production to precision-driven customization is unlocking stronger pricing leverage and margin expansion opportunities. Digital platforms are connecting consumers directly with personalized supplement providers, and this shift is reducing reliance on conventional retail distribution. Premix manufacturers that are adapting to lower minimum order quantities and accelerated development cycles are gaining entry into these technology-enabled ecosystems. Subscription-based delivery models are generating recurring revenue and are strengthening demand visibility for ingredient suppliers. Companies that are forming strategic partnerships with digital health innovators are aligning themselves with data-driven nutrition science. By integrating formulation expertise with technology-enabled consumer insights, premix suppliers are strengthening differentiation and are building durable competitive advantage in a rapidly evolving nutrition landscape.

Category-wise Analysis

Nutrient Type Insights

Vitamins are projected to account for about 48% of the customized premixes market revenue share in 2026. Their dominance is being supported by extensive use in food fortification and dietary supplement applications across global markets. Premixes containing vitamin A, vitamin D, vitamin B complex, and vitamin C are witnessing steady demand due to mandatory fortification mandates in staple foods and strong consumer preference for multivitamin formulations. Regulatory authorities are maintaining clear compliance frameworks for vitamin inclusion levels, which is supporting formulation consistency and market stability. Scientific validation of health benefits is reinforcing consumer trust, while established manufacturing processes are enabling cost-efficient large-scale production. As governments are continuing to promote preventive nutrition strategies, vitamin premixes are remaining central to public health initiatives and commercial product development.

Minerals are likely to emerge as the fastest-growing product segment between 2026 and 2033, as awareness of micronutrient deficiencies is increasing across both developing and developed economies. Iron, calcium, zinc, and magnesium fortification is gaining policy support following recommendations from the WHO and national anemia control programs. Functional beverage manufacturers and sports nutrition brands are incorporating mineral blends to address bone health, hydration balance, and metabolic support. Advances in chelation technologies and enhanced bioavailability systems are improving nutrient absorption and are reducing sensory challenges in complex food matrices. These technical improvements are enabling broader application beyond traditional vehicles such as fortified flour and dairy.

Application Insights

Food and beverages are anticipated to capture nearly 65% of the customized premix market revenues in 2026. Demand is finding support from mandatory fortification policies for staple foods and by large-scale production across bakery products, dairy items, breakfast cereals, and beverages. Established retail and food service distribution networks are ensuring wide product penetration and consistent volume throughput. Manufacturers are increasingly incorporating tailored premix blends into functional food categories such as energy bars, fortified snacks, and ready-to-drink nutritional beverages. This diversification is extending application beyond traditional flour and oil fortification programs. As consumer awareness of preventive health is rising, food producers are reformulating portfolios to include micronutrient enrichment while maintaining taste and shelf stability.

Dietary supplements are set to be the fastest-growing application from 2026 to 2033, fueled by aging demographics and a stronger focus on preventive healthcare. Consumers are seeking targeted solutions for immunity, cognitive performance, joint mobility, and sports recovery, and this demand is driving precise formulation requirements. Supplement manufacturers are requesting highly customized nutrient combinations with specific dosage accuracy and compatibility across delivery systems such as tablets, capsules, gummies, and powders. Clean label positioning and traceability standards are becoming more important in purchase decisions. Direct-to-consumer distribution models and electronic commerce platforms are enabling niche product launches and data-driven marketing strategies. Personalized nutrition services are further expanding the need for adaptable premix solutions.

Form Insights

Powder formats are forecast to hold an estimated 75% of the customized premixes market share in 2026. The leadership of this segment stems from the ease of handling, extended shelf stability, and cost efficiency in storage and transportation offered by powdered premixes. This format can integrate smoothly into dry food matrices, beverage concentrates, and dietary supplement formulations using conventional blending equipment. Manufacturers are benefiting from simplified quality control procedures and lower moisture sensitivity compared with liquid alternatives. The risk of nutrient degradation is remaining relatively controlled under proper storage conditions, which is supporting consistent product performance. Powder systems are also aligning well with existing food processing infrastructure, allowing large-scale producers to incorporate micronutrients without significant capital modification. Suppliers that are maintaining tight particle size distribution and uniform micronutrient dispersion are strengthening reliability in high-volume production environments.

Liquid premixes are poised to register the highest 2026-2033 CAGR, as the demand for ready-to-drink beverages and liquid supplements skyrockets. Food and beverage producers are seeking homogeneous nutrient distribution in dairy products, sports drinks, and functional beverages, and liquid systems are enabling improved dispersion. These formats are eliminating dust formation during processing and are improving workplace safety and automation efficiency. Advances in emulsification technology and enhanced stability systems are extending shelf life and preserving nutrient integrity. Specialized packaging solutions are supporting cold chain management and protecting against oxidation. Applications in infant formula and performance beverages are driving adoption, and manufacturers are accepting higher pricing due to improved processing precision and batch consistency.

Regional Insights

Asia Pacific Customized Premixes Market Trends

Asia Pacific is predicted to be leading as well as the fastest-growing market for customized premixes, anticipated to control approximately 38% share in 2026. China, India, Japan, and ASEAN countries are fueling this expansion through large populations, rising middle-class incomes, and government fortification initiatives. Public health programs mandate nutrient addition to staple foods such as rice, wheat flour, cooking oil, and salt. Regional manufacturers benefit from cost-effective production, access to raw materials, and growing domestic demand paired with export potential. Executives recognize this region as a critical growth engine that balances volume opportunities with premium application development.

China commands the strongest market position, driven by nutrition improvement campaigns and expanding dietary supplement adoption. Sophisticated food processing infrastructure supports advanced premix applications, particularly in infant formula where manufacturers meet rigorous quality benchmarks. India demonstrates remarkable potential through mandatory fortification reaching broad populations. Japan excels in senior nutrition, functional foods, and sports supplements, where consumers willingly pay premiums for science-backed formulations. ASEAN members such as Indonesia, Thailand, and Vietnam are accelerating growth via large-scale urbanization and targeted implementation of anti-malnutrition programs. Companies should establish regional manufacturing hubs to leverage competitive labor costs, favorable investment climates, and diverse regulatory frameworks while building direct relationships with local food processors and health authorities.

Europe Customized Premixes Market Trends

Europe maintains a strong position in the global market for customized premixes. Germany, the U.K., France, and Spain collectively drive the majority of regional demand. Regulatory harmonization under EFSA guidelines creates consistent frameworks for nutrient fortification across member states. Mandatory programs in several countries require nutrient addition to staple foods. Consumers actively seek functional foods and preventive health products, supporting steady market expansion. Manufacturers benefit from advanced food processing infrastructure and established distribution networks serving both domestic and export markets.

Germany leads consumption through its pharmaceutical and nutraceutical manufacturing capabilities. The U.K. excels in sports nutrition and senior wellness applications. France demonstrates strength in infant nutrition and organic supplements. Spain accelerates growth in fortified bakery products and functional beverages aligned with Mediterranean dietary preferences. EU Regulation 1925/2006 establishes maximum permitted levels for vitamins and minerals, although individual countries maintain distinct mandatory fortification requirements. The region pioneer’s sustainability initiatives, with manufacturers increasingly adopting recyclable packaging and carbon-neutral production processes. Organizations will need to pursue research partnerships with academic institutions to validate bioavailability claims and target Eastern European markets where rising incomes and dietary westernization create accelerated demand opportunities.

North America Customized Premixes Market Trends

North America occupies a prominent position in the customized premixes market, with the U.S. contributing the majority of regional demand. Structured fortification initiatives and high dietary supplement consumption are sustaining consistent volume requirements across food and nutraceutical applications. The U.S. FDA is providing regulatory clarity through defined dietary reference intakes and transparent guidance on voluntary nutrient addition. This framework is accelerating product development timelines and reducing approval uncertainty for manufacturers. Advanced food processing infrastructure and integrated logistics networks are enabling efficient distribution of customized formulations across bakery, dairy, beverage, and supplement categories. Companies are leveraging established retail chains and digital marketplaces to expand reach across diverse consumer segments.

Strengthening demand for customized premixes in sports nutrition, senior health products, and functional foods that incorporate botanical extracts are broadening growth prospects of the regional market. The Generally Recognized as Safe (GRAS) notification pathway and the Dietary Supplement Health and Education Act (DSHEA) are balancing innovation with consumer protection, and this regulatory environment is fostering steady portfolio expansion. Clean label positioning, organic certifications, and non-genetically modified organism (non-GMO) claims are shaping procurement strategies. Competitive intensity is featuring multinational ingredient suppliers alongside specialized premix providers focused on natural and condition-specific blends. Manufacturers are strengthening supply chain control through selective vertical integration and are investing in bioavailability enhancement technologies to improve nutrient absorption. Electronic commerce platforms are enabling direct-to-consumer engagement and personalized nutrition offerings, and companies that are aligning formulation capabilities with digital health trends are reinforcing long-term growth potential in the region.

Competitive Landscape

The global customized premixes market exhibits a moderately fragmented structure, with leading multinational companies collectively accounting for approximately 35-40% of total revenues. Key participants such as DSM-Firmenich, BASF SE, Glanbia Nutritionals, Archer Daniels Midland Company, and Kerry Group plc are maintaining significant influence through broad product portfolios and global distribution capabilities. These organizations are leveraging research and development investment, strategic partnerships, and geographic expansion to strengthen their competitive positions. They are delivering application-specific formulations tailored to food, beverage, pharmaceutical, and nutraceutical manufacturers, and they are integrating technical support services to enhance customer retention. Scale advantages in procurement, quality assurance, and regulatory compliance are enabling these companies to secure long-term supply agreements with multinational brands.

On the other hand, smaller firms are focusing on niche applications, such as organic premixes, plant-based nutrient blends, and condition-specific formulations, to differentiate their offerings. Competitive intensity is increasing as companies are pursuing portfolio diversification and localized production to meet region-specific regulatory requirements. Innovation pipelines are emphasizing improved bioavailability, clean label compliance, and customized micronutrient ratios. Market participants are expanding contract manufacturing capabilities and investing in digital formulation platforms to enhance responsiveness. This combination of scale-driven multinational presence and specialized regional expertise is sustaining moderate fragmentation while fostering continuous product and service innovation across the customized premixes ecosystem.

Key Industry Developments

- In November 2025, Trouw Nutrition opened its CEBPET factory in Arujá, São Paulo, Brazil a 3,000-square-meter facility dedicated to pet food blends and premixes to quintuple service capacity and support Brazil's position as the world's third-largest pet food producer.

- In September 2025, Fermenta Biotech Limited received an Indian Patent for its proprietary process to manufacture plant-based Vitamin D3, bolstering its intellectual property portfolio and leadership in sustainable, vegan nutritional ingredients.

- In May 2025, ACG launched its Personalised Capsule Machine (PCM), a patented manufacturing solution that combines real-time health data, precise dosing, and automated capsule production to create custom supplement capsules tailored to individual needs.

Companies Covered in Customized Premixes Market

- DSM-Firmenich

- BASF SE

- Glanbia Nutritionals

- ADM (Archer Daniels Midland)

- Kerry Group

- Corbion N.V.

- Farbest Brands

- Prinova Group LLC

- Jubilant Life Sciences

- SternVitamin GmbH & Co. KG

- Barentz International

- Watson Inc.

- Hexagon Nutrition Pvt. Ltd.

- Vitablend Nederland B.V.

- Zagro

Frequently Asked Questions

The global customized premixes market is projected to reach US$ 2.0 billion in 2026.

Soaring demand for functional foods, government fortification mandates, and technological advances in nutrient delivery systems are driving market expansion.

The market is poised to witness a CAGR of 8.4% from 2026 to 2033.

Personalized nutrition platforms, emerging Asia-Pacific fortification programs, and clinical nutrition applications offer highest growth potential.

DSM-Firmenich, BASF SE, Glanbia Nutritionals, Archer Daniels Midland and Kerry Group are some of the key players in the market.