- Healthcare Services

- Chronic Wound Care Market

Chronic Wound Care Market Size, Share and Growth Forecast, 2026 - 2033

Chronic Wound Care Market by Wound Type (Diabetic Ulcers, Pressure Ulcers, Venous Ulcers), Product (Advanced Wound Dressing, Wound Care Devices, Active Therapy), End User (Hospitals and Wound Care Centers), and Regional Analysis for 2026 - 2033

Chronic Wound Care Market Share and Trends Analysis

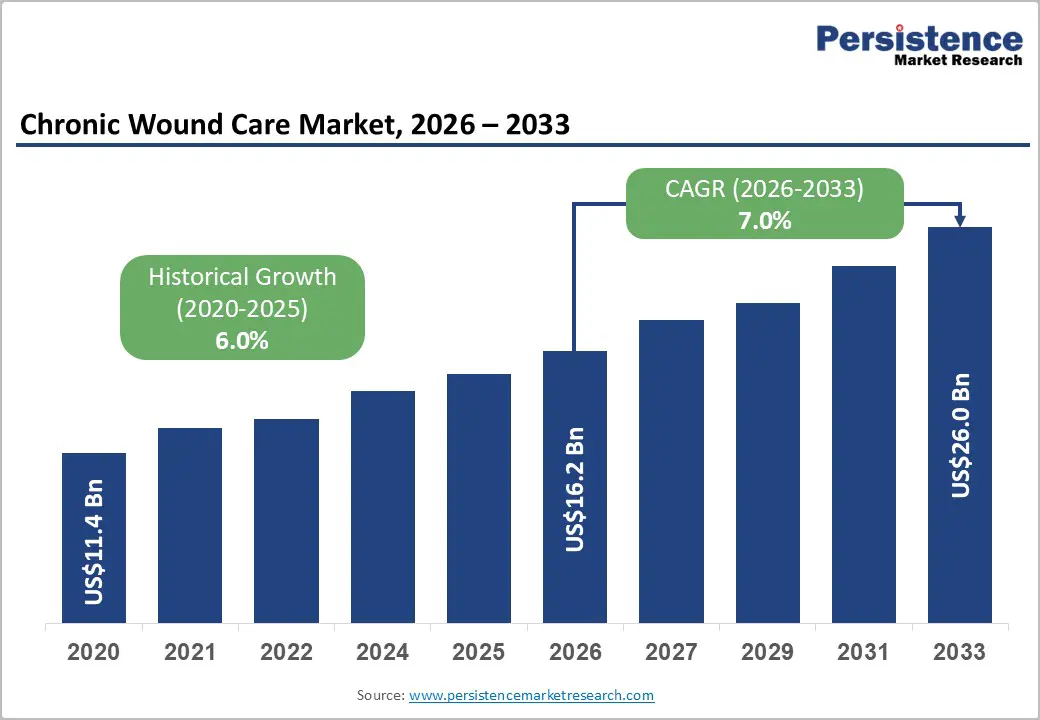

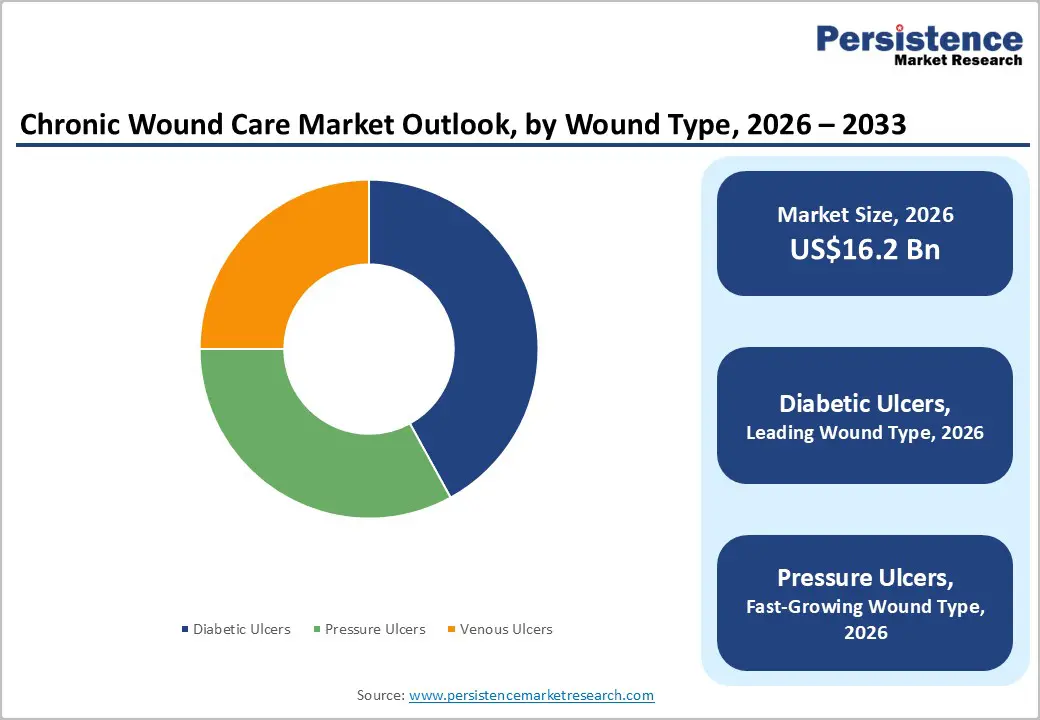

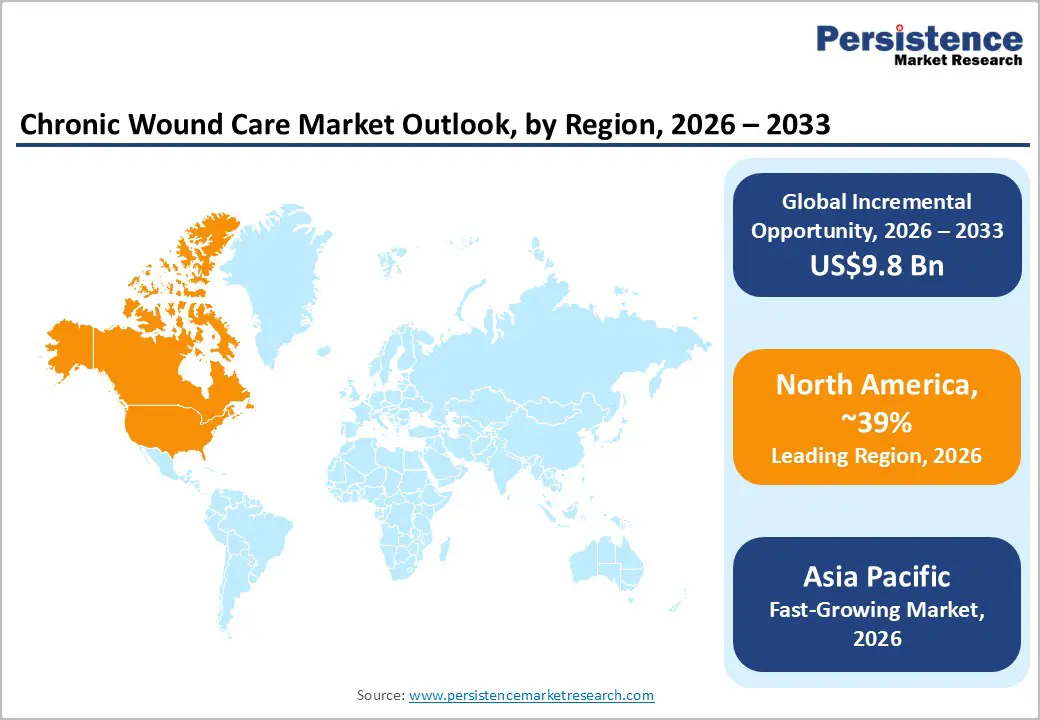

The global chronic wound care market size is likely to be valued at US$16.2 billion in 2026 and is projected to reach US$26.0 billion by 2033, growing at a CAGR of 7.0% during the forecast period from 2026 to 2033, driven by the increasing prevalence of diabetes, aging populations, and the rising incidence of pressure injuries and vascular disorders globally.

Expanding adoption of advanced wound care technologies, including advanced wound dressings, negative pressure wound therapy, and bioactive therapies, continues to improve healing outcomes and reduce hospitalization rates. Government healthcare initiatives focused on reducing chronic wound burden and improving long-term care management are also strengthening market penetration across hospitals and wound care centers.

Key Industry Highlights:

- Type Segment Insights: Diabetic ulcers are projected to dominate with nearly a 42% share in 2026, while pressure ulcers are anticipated to be the fastest-growing segment through 2033 due to increasing elderly and immobile patient populations globally.

- Product Segment Insights: Advanced wound dressing products are expected to lead with approximately a 46% share in 2026, whereas active therapy is likely to register the fastest growth through 2033, owing to rising adoption of regenerative and biologic wound healing technologies.

- End-user Segment Insights: Hospitals are expected to account for nearly a 58% share in 2026, due to higher chronic wound treatment volumes, while wound care centers are projected to witness the fastest growth through 2033, supported by increasing outpatient wound management demand.

- Regional Leadership: North America is expected to dominate with around a 39% share in 2026, while Asia Pacific is projected to remain the fastest-growing regional market through 2033 due to expanding healthcare infrastructure and rising diabetic populations.

- Competitive Environment: Market players are focusing on AI-enabled wound monitoring, regenerative therapies, and portable wound care devices, with leading companies strengthening market presence through product innovation and strategic partnerships.

DRO Analysis

Driver - Rising Global Burden of Diabetes and Aging Population Accelerating Demand for Chronic Wound Treatment

The increasing incidence of diabetes and age-related mobility disorders remains the primary growth driver for the chronic wound care market. According to the International Diabetes Federation (IDF), over 640 million adults are projected to live with diabetes by 2030, significantly increasing the prevalence of diabetic foot ulcers and associated complications.

The World Health Organization (WHO) also estimates that the global population aged 60 years and above will exceed 1.4 billion by 2030, creating a larger patient pool vulnerable to pressure ulcers and venous leg ulcers.

These demographic trends are driving demand for wound care devices, antimicrobial dressings, and long-term wound management solutions. Healthcare systems are increasingly prioritizing early intervention and preventive wound care strategies to reduce amputation rates, hospital stays, and treatment costs, thereby accelerating adoption of advanced chronic wound therapies across acute and homecare settings.

Restraint - High Treatment Costs and Reimbursement Variability Limiting Adoption in Developing Economies

Despite technological progress, the high cost of advanced wound care products continues to limit broader adoption, particularly in low- and middle-income countries. Advanced biologic dressings, active therapies, and negative-pressure wound therapy systems often require repeated clinical interventions and long treatment cycles, increasing overall patient costs.

According to the U.S. Agency for Healthcare Research and Quality (AHRQ), chronic wound treatment can cost healthcare systems billions annually due to prolonged hospitalization and recurring complications. In several developing regions, limited reimbursement coverage and insufficient wound care infrastructure delay timely treatment access. Small healthcare providers also face procurement challenges due to elevated product pricing and limited skilled personnel trained in specialized wound management. These structural barriers create uneven market penetration and slow adoption of premium wound care technologies outside developed healthcare markets.

Opportunity - Expansion of Home-Based Wound Management and Digital Wound Monitoring, Creating New Revenue Streams

The rapid shift toward outpatient and home-based healthcare presents a major opportunity for the wound management market. Rising healthcare costs and hospital capacity constraints are encouraging providers to adopt remote wound assessment technologies and portable wound care systems. Digital wound imaging platforms integrated with artificial intelligence are improving monitoring accuracy and enabling earlier clinical intervention.

According to the Centers for Medicare & Medicaid Services (CMS), reimbursement support for home healthcare services has expanded steadily in recent years, supporting decentralized chronic wound treatment models. Emerging economies across Asia Pacific and Latin America are also investing in community-based wound care infrastructure to address growing diabetic populations. Companies developing smart dressings, telehealth-enabled monitoring systems, and portable negative pressure wound therapy devices are expected to benefit from increasing demand for cost-efficient and patient-centric wound care solutions.

Category-wise Analysis

Wound Type Insights

Diabetic ulcers are projected to remain the leading segment in the chronic wound care market, accounting for nearly 42% of revenue in 2026. Rising diabetes prevalence, obesity, and poor glycemic control continue to increase diabetic foot complications globally. Hospitals are expanding diabetic wound management programs to reduce infection risks and lower-limb amputations. In 2025, several U.S. healthcare providers strengthened early-intervention diabetic ulcer care pathways to improve recovery outcomes and reduce readmission rates.

Pressure ulcers are expected to witness the fastest growth through 2033, supported by rising elderly populations and increasing long-term care admissions. The growing incidence of immobility-related wounds in hospitals and rehabilitation centers is accelerating demand for preventive wound management solutions. Healthcare providers are investing in pressure redistribution systems, moisture-control products, and digital monitoring technologies. Expansion of home healthcare services across Europe and Asia is further supporting specialized pressure ulcer treatment demand.

Product Insights

Advanced wound dressing products are expected to dominate with approximately 46% market share in 2026, driven by strong demand for foam dressings, hydrocolloids, alginates, and antimicrobial products. These dressings offer improved infection control, moisture balance, and faster healing compared to conventional gauze products. Manufacturers introduced next-generation antimicrobial foam dressings in 2025 to strengthen chronic wound infection management. Increasing focus on reducing hospital stays and treatment complications continues to support segment growth.

The active therapy segment is projected to register the fastest growth through 2033 due to rising adoption of biologics, skin substitutes, and regenerative wound healing therapies. These solutions are increasingly used for difficult-to-heal diabetic and venous ulcers, where traditional treatments show slower recovery outcomes. Research investments in tissue engineering and cellular repair technologies are expanding clinical applications globally. In 2025, strategic partnerships between wound care and regenerative medicine companies accelerated innovation in bioengineered wound healing products.

End-user Insights

Hospitals are expected to remain the leading end-user segment, contributing nearly 58% of revenue in 2026 due to high chronic wound treatment volumes and advanced clinical infrastructure. Acute care hospitals continue to manage a large share of diabetic ulcers, surgical wounds, and severe pressure injuries requiring continuous monitoring. Investments in multidisciplinary wound care departments and infection prevention programs are strengthening hospital treatment capacity. In 2025, several North American healthcare systems expanded specialized wound management units to improve patient recovery efficiency.

Wound care centers are anticipated to witness the fastest growth through 2033 as patients increasingly prefer specialized outpatient treatment services offering faster and cost-efficient care. Growing awareness regarding early wound intervention and expansion of ambulatory healthcare infrastructure are supporting segment growth. The adoption of digital wound imaging, telehealth support, and portable wound therapy systems is improving outpatient treatment effectiveness. In 2025, multiple outpatient wound management providers expanded regional clinic networks across Europe and Asia to address rising chronic wound cases.

Regional Insights

North America Chronic Wound Care Market Trends

North America is projected to account for nearly 39% of the global market share in 2026, driven by high diabetes prevalence, advanced healthcare infrastructure, and strong reimbursement systems. The region continues to witness rapid adoption of advanced wound care technologies, including regenerative therapies, antimicrobial dressings, and portable wound management systems. Rising healthcare spending and growing preference for home-based wound treatment are further supporting regional market expansion.

U.S. Chronic Wound Care Market Trends

The U.S. is expected to contribute nearly 72% of the North America market due to its large diabetic population and high chronic wound treatment expenditure. According to the CDC, over 38 million Americans are living with diabetes, significantly increasing diabetic ulcer treatment demand. In 2025, several U.S. healthcare providers expanded AI-enabled wound monitoring and outpatient wound care programs to improve recovery outcomes and reduce hospital readmissions.

Canada Chronic Wound Care Market Trends

Canada is expected to account for approximately 28% of the regional market share in 2026, supported by rising investments in elderly care and community healthcare services. Growing adoption of portable wound therapy systems and specialized homecare wound management is strengthening treatment accessibility. Government-backed long-term care expansion initiatives and increasing healthcare expenditure continue to support chronic wound treatment demand across the country.

Europe Chronic Wound Care Market Trends

Europe remains a major market for wound management solutions, supported by aging populations, universal healthcare systems, and increasing chronic disease burden. Demand for antimicrobial dressings, compression therapy products, and biologic wound healing solutions continues to rise across the region. The EU Medical Device Regulation (EU MDR) is also strengthening product quality standards and clinical safety compliance.

Germany Chronic Wound Care Market Trends

Germany is projected to account for nearly 28% of the Europe market in 2026 due to strong hospital infrastructure and high healthcare expenditure. The country continues to invest in advanced wound care technologies and elderly patient management programs. In 2025, German healthcare providers increased the adoption of outpatient wound treatment models to reduce hospitalization costs and improve chronic wound recovery timelines.

U.K. Chronic Wound Care Market Trends

The U.K. is expected to contribute around 21% of the regional market in 2026, driven by expanding community-based wound care initiatives under the National Health Service (NHS). Rising pressure ulcer cases among elderly patients are increasing the demand for preventive wound management solutions. The country is also witnessing stronger adoption of digital wound assessment platforms to improve treatment monitoring and patient outcomes.

Asia Pacific Chronic Wound Care Market Trends

Asia Pacific is expected to witness the fastest growth through 2033 due to rising diabetic populations, improving healthcare infrastructure, and increasing healthcare expenditure across emerging economies. The region is also strengthening its position as a manufacturing hub for wound care consumables and medical devices due to lower production costs and expanding local capabilities. Government chronic disease management programs are further supporting market growth.

China Chronic Wound Care Market Trends

China is estimated to hold nearly 38% of the Asia Pacific market share in 2026, supported by its growing elderly population and rising prevalence of diabetes-related ulcers. The country continues to invest in hospital modernization, advanced wound care adoption, and domestic medical device production. In 2025, several Chinese healthcare groups expanded specialized diabetic foot treatment centers to address increasing chronic wound patient volumes.

India Chronic Wound Care Market Trends

India is set to account for approximately 19% of the regional market share in 2026 and is witnessing strong growth due to rising diabetes incidence and expanding private healthcare infrastructure. Increasing awareness regarding diabetic foot management and improving access to outpatient wound care services are supporting treatment demand. Government healthcare investment programs and expanding domestic medical device manufacturing are also improving the affordability and accessibility of chronic wound care solutions.

Competitive Landscape

The global chronic wound care market is moderately consolidated, with leading players including Smith+Nephew, 3M Health Care, Convatec Group, and Mölnlycke Health Care accounting for a significant share of global revenue. These companies compete through strong advanced wound care portfolios, hospital partnerships, and investments in regenerative therapies, antimicrobial dressings, and portable wound management systems. Continuous R&D and expansion of digital wound monitoring technologies remain key competitive strategies.

Meanwhile, companies such as Organogenesis, Integra LifeSciences, and Coloplast are focusing on regenerative medicine and outpatient wound care solutions. High regulatory compliance and product development costs continue to create barriers for new entrants. However, rising demand for home-based wound care and digital wound assessment is opening opportunities for regional and technology-focused players.

Key Industry Developments:

- In March 2025, Smith+Nephew launched the CENTRIO PRP system in the U.S. to strengthen its regenerative wound healing portfolio. This enhances biologic treatment options for chronic and exuding wounds, improving healing outcomes in complex cases.

- In June 2025-January 2026, Convatec Group received regulatory approval for ConvaNiox™ antimicrobial dressing targeting hard-to-heal wounds such as diabetic ulcers. The innovation improves infection control and biofilm management, strengthening advanced chronic wound care capabilities.

Companies Covered in Chronic Wound Care Market

- Smith+Nephew

- 3M Health Care

- Convatec Group

- Mölnlycke Health Care

- Coloplast

- Integra LifeSciences

- Medtronic

- B. Braun

- Paul Hartmann AG

- Organogenesis

- MiMedx Group

- Cardinal Health

- Essity

- Hollister Incorporated

Frequently Asked Questions

The global chronic wound care market is projected to reach US$16.2 billion in 2026.

Rising diabetes prevalence, aging populations, and growing demand for advanced wound care solutions drive the market.

The chronic wound care market is expected to grow at a CAGR of 7.0% from 2026 to 2033.

Companies are expanding opportunities through regenerative therapies, AI-enabled wound monitoring, and home-based wound management solutions.

Smith+Nephew, 3M Health Care, Convatec Group, and Mölnlycke Health Care are key players in the chronic wound care market.