- Pharmaceuticals

- Chronic Cough Market

Chronic Cough Market Size, Share, and Growth Forecast, 2026 - 2033

Chronic Cough Market by Drug Class (Antihistamines, Corticosteroids, Decongestants, Combination Drug), Route of Administration (Injections, Oral, Nasal, Other), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis for 2026-2033

Chronic Cough Market Share and Trends Analysis

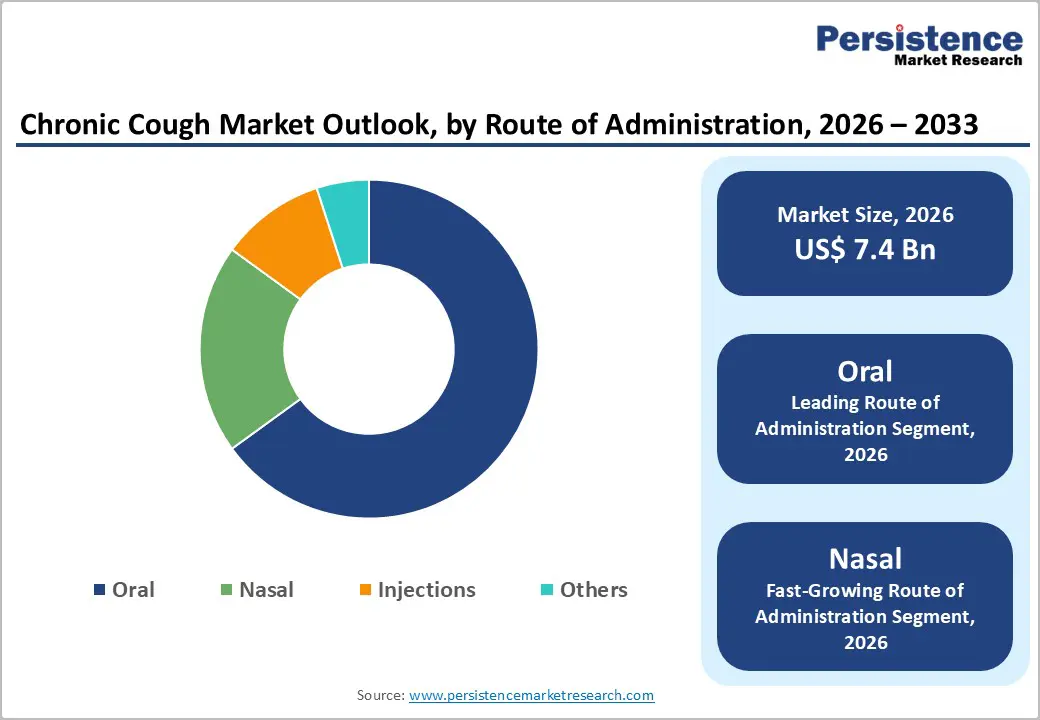

The global chronic cough market size is likely to be valued at US$7.4 billion in 2026, and is projected to reach US$12.0 billion by 2033, growing at a CAGR of 6.2% during the forecast period 2026−2033.

This growth trajectory reflects increasing disease prevalence, particularly among aging populations, alongside heightened clinical awareness of chronic cough as a distinct pathological condition requiring targeted therapeutic intervention. The market expansion is further propelled by robust pharmaceutical pipeline development, with multiple investigational therapies advancing through late-stage clinical trials addressing unmet medical needs in refractory chronic cough management. Evolving diagnostic protocols and improved patient access to specialized pulmonology services across developed and emerging markets contribute to accelerating treatment adoption rates.

Key Industry Highlights

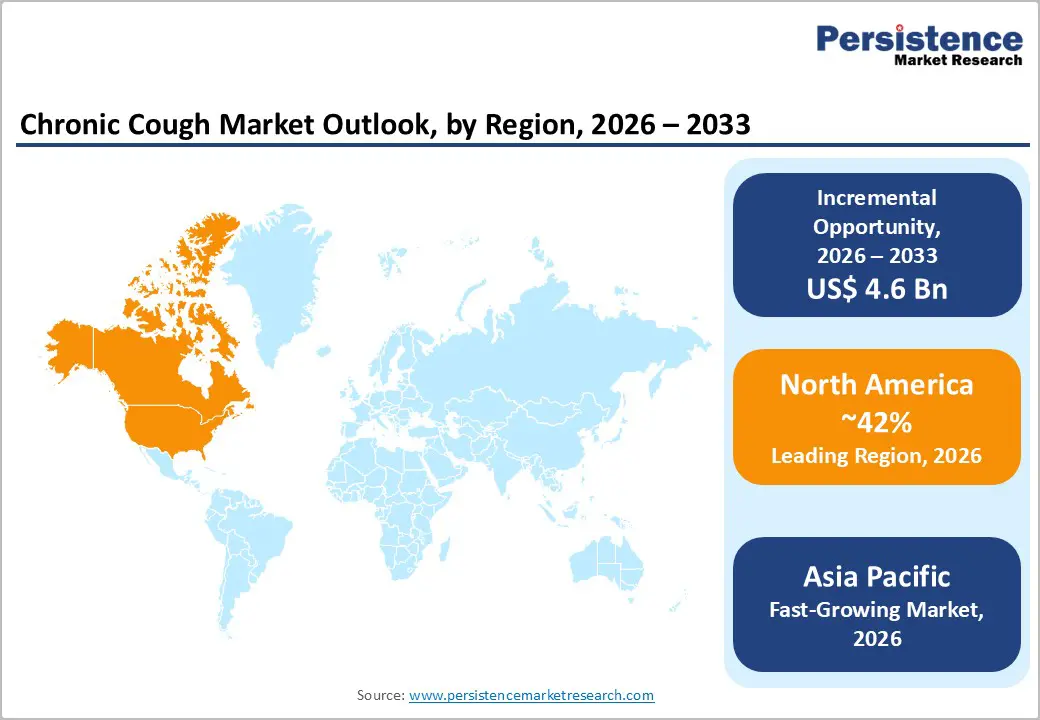

- Dominant Region: North America is expected to command about 42% market share in 2026, fueled by a high disease awareness among both healthcare providers and patients.

- Fastest-growing Market: Asia Pacific is set to be the fastest-growing market through 2033, owing to a massive patient base and government-led healthcare reform initiatives.

- Leading Route of Administration: Oral is poised to dominate with approximately 65% of the revenue share in 2026, favored for its convenience, high compliance, and ease of self-management.

- Fastest-growing Route of Administration: Nasal is likely to be the fastest-growing segment during the 2026-2033 forecast period, due to innovations targeting upper airway inflammation and postnasal drip.

- February 2025: Kyorin Pharma partnered with Hyfe to develop and commercialize an AI-enabled digital therapeutic (DTx) for chronic cough in Japan, combining behavioral cough suppression therapy with smartphone-based cough monitoring.

| Report Attribute | Details |

|---|---|

|

Chronic Cough Market Size (2026E) |

US$ 7.4 Bn |

|

Market Value Forecast (2033F) |

US$ 12.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Healthcare Expenditure and Insurance Coverage

Global healthcare spending has grown consistently, reaching approximately $9.8 trillion in 2024, according to the World Health Organization (WHO). Respiratory therapeutics claim a substantial portion of pharmaceutical budgets in this expanding landscape. Developed markets, such as the U.S. and the European Union (EU), actively extend insurance coverage for chronic cough therapies. Payers recognize how the condition impairs quality of life and triggers indirect expenses, such as productivity declines from missed workdays. Health authorities prioritize interventions that deliver clear benefits to patients and economies alike.

Patients in the emerging markets of Asia Pacific are witnessing rapid increases in insurance access, which is transforming care delivery for respiratory conditions. In large economies such as China, national health programs are broadening their scope to encompass nearly all citizens, thereby enhancing the availability of advanced medications. Patients gain easier entry to specialized therapies that address persistent cough symptoms effectively. Healthcare providers respond by integrating these options into routine practice, which fuels demand across high-density populations. This trend is expected to boost treatment adoption significantly, as insurers refine reimbursement policies to favor proven solutions.

Advancements in Novel Therapeutic Mechanisms

Pharmaceutical companies actively pursue innovative treatments that target precise cough reflex pathways. They develop agents such as Proton-gated ion channel 3 (P2X3) receptor antagonists and Transient Receptor Potential Vanilloid 1 (TRPV1) antagonists to interrupt nerve hypersensitivity effectively. These approaches fill critical gaps in refractory chronic cough management, where standard therapies often fall short. Researchers have been validating their potential through rigorous testing, which reveals consistent symptom improvements for patients. Developers prioritize these mechanisms to build robust pipelines that outpace generic alternatives.

This pioneering therapy, designed exclusively for refractory cases, confirms viability for focused interventions. Firms now intensify research and development efforts on comparable solutions, which will have redefined care protocols by the next decade. Specialists adopt these advances swiftly, integrating them into clinical practice to optimize patient outcomes. Such momentum shifts industry focus toward precision medicine, empowering underserved groups with tailored options and fostering long-term adherence across global markets.

Diagnostic Complexity and Misclassification Epidemic

Chronic cough diagnosis lacks uniform standards worldwide, as clinicians rely on patient-reported duration rather than reliable biomarkers or approved testing methods. Healthcare providers often initiate care with assumptions about related issues such as asthma, gastroesophageal reflux disease (GERD), or upper airway conditions without thorough assessments. This approach leads to repeated trials of unsuitable remedies, which prolongs patient suffering and slows adoption of advanced options. Specialists struggle to pinpoint root causes accurately, which hampers timely interventions and creates barriers for emerging treatments in clinical settings.

The U.S. Food and Drug Administration (FDA) has not yet cleared dedicated devices for cough reflex evaluation, leaving practitioners with limited tools for precise identification. Overlaps with other respiratory disorders further cloud judgment, as patients frequently present multiple issues simultaneously. Pharmaceutical developers face obstacles in trial execution and outcome measurement, which complicates efforts to demonstrate therapy value. Standardized protocols will have clarified these challenges, enabling sharper patient targeting and streamlined market entry. Such advances promise to reduce trial-and-error cycles, boost confidence in prescriptions, and unlock growth for precision therapies across diverse care environments.

Competition from Non-Pharmacological Interventions and Behavioral Therapies

Non-pharmacological options are gaining traction as evidence mounts for speech pathology, behavioral cough control, and physical therapy methods. Clinicians apply these techniques to help patients manage symptoms through targeted exercises and habit adjustments. The UK's National Health Service (NHS) promotes such approaches as initial steps because they avoid medication risks and expenses. Multidisciplinary clinics blend respiratory physiotherapy with other services, which yields high patient approval in everyday practice. Developers are now launching digital applications that guide users via remote sessions, offering affordable alternatives to traditional drugs.

Payers enforce requirements for therapy attempts before approving prescriptions, which aligns with cost-control goals in modern healthcare systems. Providers operating under value-based care frameworks prioritize economical solutions that deliver results without ongoing costs. This shift pressures pharmaceutical firms to prove superiority in resistant scenarios only. Integrated care models will have elevated these interventions as standard starters, reshaping treatment pathways across regions. Drug makers respond by exploring hybrid strategies, such as combining therapies with medications to enhance outcomes and secure reimbursement. Such adaptations ensure relevance amid evolving preferences for sustainable, patient-centered care.

Development of Combination Therapies and Personalized Treatment Protocols

Combinations of advanced chronic cough suppressants with treatments for root causes such as GERD or upper airway irritation are making notable headway in the healthcare space. These pairings aim to deliver better results than single options by addressing both symptoms and triggers simultaneously. Institutions advance precision medicine through reflex sensitivity assessments and biomarker analysis, which guide doctors toward ideal choices for each patient. Developers can integrate these tools into unified systems that link testing directly to therapy, streamlining care delivery in respiratory practice.

Pharmaceutical firms position themselves for stronger market roles by adopting these integrated methods. They create platforms that pair diagnostics with drugs, which enhances effectiveness and justifies higher value propositions. Clinicians favor such bundles because they personalize interventions and reduce trial periods for patients. Providers have the option of embedding these approaches widely, transforming how specialists manage persistent cough cases. Companies gain loyalty through proven superiority, as combinations outperform standalone regimens in real-world settings. This evolution fosters sustainable growth, aligns with payer demands for evidence-based solutions, and elevates outcomes across diverse populations seeking lasting relief.

Telemedicine Integration and Digital Health Solutions

Telehealth adoption has accelerated as providers embrace remote solutions for chronic cough care, especially after the pandemic. Digital platforms use smartphone apps and wearable devices to track cough patterns objectively. These tools deliver real-time data that helps clinicians adjust treatments precisely and monitor progress effectively. Patients are benefiting immensely from convenient access, which encourages consistent engagement with care plans in home settings. Pharmaceutical companies can also integrate these technologies with drug therapies to create seamless ecosystems.

Developers can offer novel subscription services that combine monitoring with medication delivery, enabling remote dose adjustments and adherence checks. This approach strengthens patient relationships and opens steady revenue channels outside one-time sales. Healthcare systems will have normalized such models, prioritizing outcomes over volume. Firms that lead in this space gain edges through data insights, which refine future innovations and align with insurer preferences for efficient interventions. Specialists are reporting higher satisfaction as these tools bridge gaps in follow-ups, fostering loyalty and transforming episodic care into ongoing partnerships across global markets.

Category-wise Analysis

Route of Administration Insights

Oral administration is expected to command an approximate 65% of the chronic cough market revenue share in 2026, since both patients and providers favor its convenience, high compliance, and ease of self-management for extended treatment durations. Pharmaceutical companies formulate most therapies, such as combination drugs and antihistamines, specifically for this route, which guarantees widespread availability through retail and hospital pharmacies. This approach aligns perfectly with outpatient care models by reducing the need for frequent clinic visits and enabling seamless integration into daily routines. Its non-invasive nature further enhances patient adherence, solidifying oral delivery as the preferred standard across diverse healthcare settings.

Nasal administration are likely to be the fastest-growing segment during the 2026-2033 forecast period. This route is expanding rapidly in the market for chronic cough treatments, powered by innovations targeting upper airway inflammation and postnasal drip, which rank among the most common cough triggers. Spray formulations deliver quick onset and localized action, making them ideal for allergic conditions and seasonal flare-ups that demand fast relief. Patients appreciate the non-invasive application, which boosts daily compliance without disrupting routines. Telehealth integration propels further growth by enabling remote consultations and prescriptions, especially in urban areas with high digital access. Pharmaceutical firms are prioritizing these advancements to capture demand in outpatient settings, enhancing overall treatment efficacy.

End-user Insights

Hospital pharmacies are poised to lead with an estimated 55% of the chronic cough market share in 2026. These facilities are known to expertly manage severe refractory cases that demand advanced diagnostics and input from multiple specialists, such as pulmonologists and allergists. Centralized procurement processes guarantee bulk availability of specialized drugs like neuromodulators, which prove essential for complex patients. These facilities support seamless transitions between inpatient care and outpatient follow-up, ensuring continuity in treatment plans. High-volume dispensing also enables hospitals to negotiate favorable pricing, reinforcing their role as primary hubs for innovative therapies in institutional settings.

Online pharmacies are projected to be the fastest-growing between 2026 and 2033, driven by convenient home delivery, competitive pricing, and digital consultations tailored to long-term patient needs. Customers value the discretion and speed of service, which eliminates travel barriers for repeat prescriptions of maintenance therapies. Post-pandemic shifts accelerate this momentum through automated reminders, subscription refills, and app-based tracking that enhance medication adherence significantly. These platforms thrive particularly in urban regions with robust internet access, where tech-savvy individuals prioritize seamless experiences. Retailers can also leverage data analytics to personalize offerings, further solidifying their edge in outpatient care.

Regional Insights

North America Chronic Cough Market Trends

North America is set to command a significant portion of the chronic cough market share at approximately 42% in 2026. The U.S. drives regional dominance with robust awareness among clinicians and patients, which prompts early interventions and specialist referrals. Pulmonologists coordinate care effectively, ensuring timely access to innovative options. The U.S. FDA supports this momentum through streamlined approval processes for novel agents, such as gefapixant, which sets benchmarks for pipeline advancements. Insurers expand coverage for specialized treatments, easing patient entry despite administrative steps such as prior approvals.

Pharmaceutical firms concentrate research efforts in key hubs, fostering breakthroughs in respiratory care. Direct marketing campaigns educate consumers, spurring demand for effective solutions. Canada complements growth via universal healthcare access, though regional formularies introduce variations in reimbursement. Specialized clinics emerge in major cities, while digital tools bridge gaps in remote communities. Aging populations will have amplified needs across the region, compelling providers to integrate telehealth and multidisciplinary models. Insurers prioritize value-driven options, which reshape competitive dynamics and sustain long-term expansion in this mature landscape.

Europe Chronic Cough Market Trends

Europe has secured a strong position in the global market for chronic cough treatments. Germany leads the regional market on the back of its universal insurance plans and dense specialist networks that ensure prompt diagnostics. The U.K. contributes substantially despite NHS funding limits and National Institute for Health and Care Excellence (NICE) reviews, which scrutinize high-cost innovations. France and Spain advance through enhanced programs for ongoing conditions, boosting treatment uptake across diverse populations. The European Medicines Agency (EMA) streamlines approvals for continent-wide access, though national payers introduce delays in funding decisions.

Health technology assessors demand proof of real-life benefits and patient well-being gains, shaping launch tactics for developers. Population aging is another key factor favoring the Europe chronic market growth, as older individuals face heightened respiratory risks from environmental exposures. Regulators enforce air quality standards, which heighten public focus on lung health. The European Respiratory Society delivers training that sharpens clinician skills in identifying causes. Post-Brexit U.K. pathways will have sped certain introductions, while Eastern expansions and rural telehealth fill care voids. Firms target these shifts to build loyalty, aligning products with value-focused systems that prioritize outcomes over volume in fragmented landscapes.

Asia Pacific Chronic Cough Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for chronic cough through 2033, aided by urbanization and industrialization, which have heightened respiratory challenges due to skyrocketing pollution levels. China steers regional progress with its vast population, expanding urban middle class, and ambitious healthcare reforms that prioritize specialist services. Japan sustains steady contributions through superior diagnostics, modern facilities, and a rapidly aging society that demands ongoing management solutions. India unlocks exceptional potential via improved access, heightened awareness of air pollution in cities, and private sector investments that target unmet rural needs from indoor exposures.

Governments boost healthcare budgets, which enhance the availability of advanced treatments across diverse economies. Local manufacturers leverage cost efficiencies to produce affordable generics and innovative options, broadening reach to underserved groups. Regulatory differences create hurdles, as approval processes vary by country, yet they spur adaptive strategies for market entry. Public-private collaborations in India and Southeast Asia accelerate infrastructure growth, while training initiatives address clinician gaps. Tiered pricing models will have tailored offerings to income levels, and regional trial hubs will have sped therapy validations. Firms that navigate these dynamics secure loyalty through accessible, effective care that aligns with evolving public health priorities.

Competitive Landscape

The global chronic cough market structure is moderately consolidated, dominated by leading players such as Merck & Co., Inc., GlaxoSmithKline plc, Bayer AG, Novartis AG, and AstraZeneca plc. These players collectively capture 55-60% of the market share. Emerging competitive dynamics shape the chronic cough market as biotechnology firms leverage platform technologies to accelerate analog development for targeted therapies, such as P2X3 antagonists. Contract development and manufacturing organizations (CDMOs) partner with smaller innovators to streamline production and scale novel formulations efficiently.

Regional pharmaceutical players pursue licensing agreements for advanced molecules, securing exclusive rights in high-growth territories such as Asia Pacific. These strategies have enabled agile responses to regulatory changes and unmet needs, fostering pipeline diversity. Companies gain edges through collaborative models that combine innovation speed with localized market expertise, positioning them for sustained leadership amid rising demand for precision treatments.

Key Industry Developments

- In January 2026, Nocion Therapeutics extended its Series B financing to US$ 93 million, bringing total funding to US$ 173 million, to advance late-stage development of taplucainium, a novel inhaled sodium channel blocker for chronic cough.

- In November 2025, the European Commission granted marketing authorization for brensocatib, the first approved treatment for non-cystic fibrosis bronchiectasis (NCFB), which leads to chronic cough and airflow obstruction, addressing a major unmet medical need for patients aged 12 years and older across the EU.

- In June 2025, a randomized, double-blind trial led by the Sungkyunkwan University School of Medicine found that the potassium-competitive acid blocker (P-CAB) fexuprazan demonstrated comparable efficacy and safety to the proton pump inhibitor (PPI) esomeprazole in improving chronic cough and reflux symptoms in patients with gastro-oesophageal reflux disease (GORD) over eight weeks.

Companies Covered in Chronic Cough Market

- Merck & Co., Inc.

- GlaxoSmithKline plc

- Bayer AG

- Novartis AG

- AstraZeneca plc

- Shionogi & Co., Ltd.

- Bellus Health Inc.

- Verona Pharma plc

- Afferent Pharmaceuticals

- NeRRe Therapeutics

- Respivant Sciences GmbH

- Boehringer Ingelheim GmbH

- Pfizer Inc.

- Sanofi S.A.

- Teva Pharmaceutical Industries Ltd.

Frequently Asked Questions

The global chronic cough market is projected to reach US$ 7.4 billion in 2026.

Rising respiratory disorder prevalence, aging populations, and therapeutic advancements are fueling the market.

The market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Major opportunities lie in emerging economies where the incidence of chronic cough is surging due to escalating air pollution, digital health integration, and combination therapies.

Merck, GlaxoSmithKline, Bayer AG, Novartis AG, and AstraZeneca are some of the key players in the market.