- Specialty & Fine Chemicals

- Cellulose Ethers & Derivatives Market

Cellulose Ethers & Derivatives Market Size, Share, and Growth Forecast 2026 - 2033

Cellulose Ethers & Derivatives Market by Product Type (Methyl Cellulose & Derivatives, Carboxymethyl Cellulose, Hydroxypropyl Methyl Cellulose, Hydroxyethyl Cellulose, Others), Application (Construction, Pharmaceutical, Personal Care, Food & Beverages, Paints & Coatings, Others), and Regional Analysis 2026 - 2033

Cellulose Ethers & Derivatives Market Size and Trend Analysis

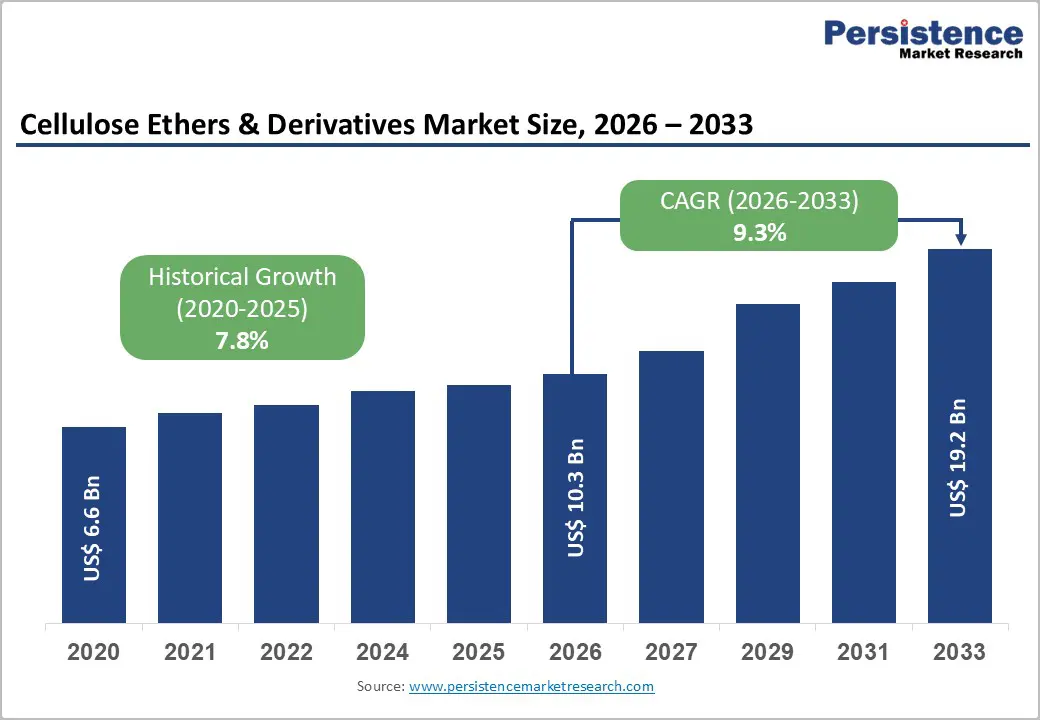

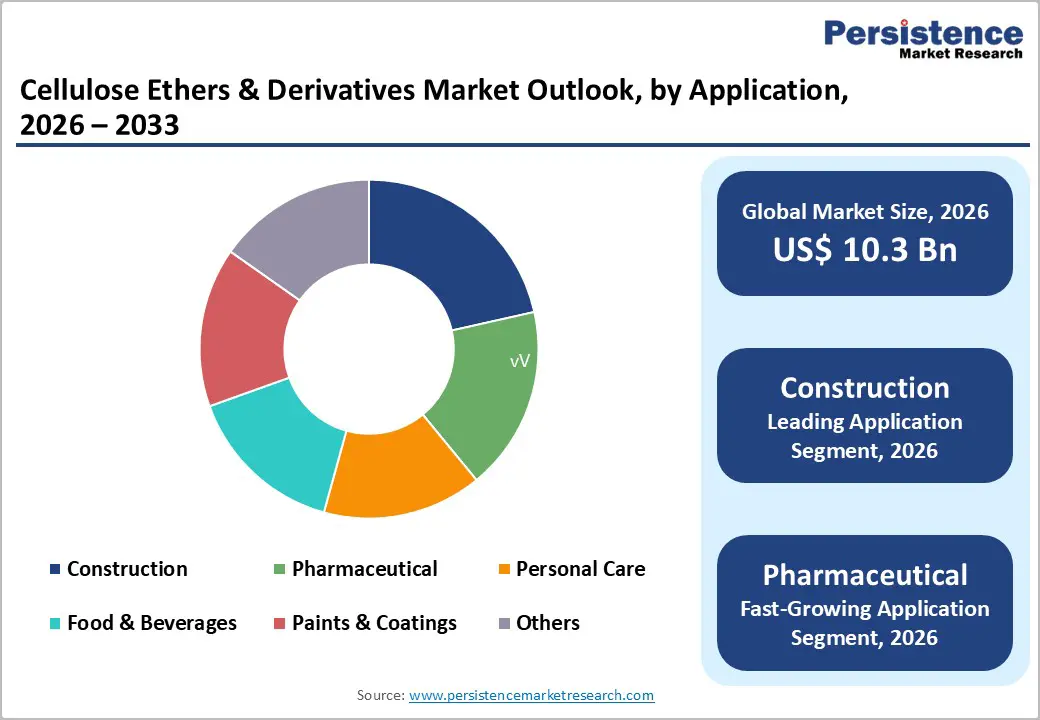

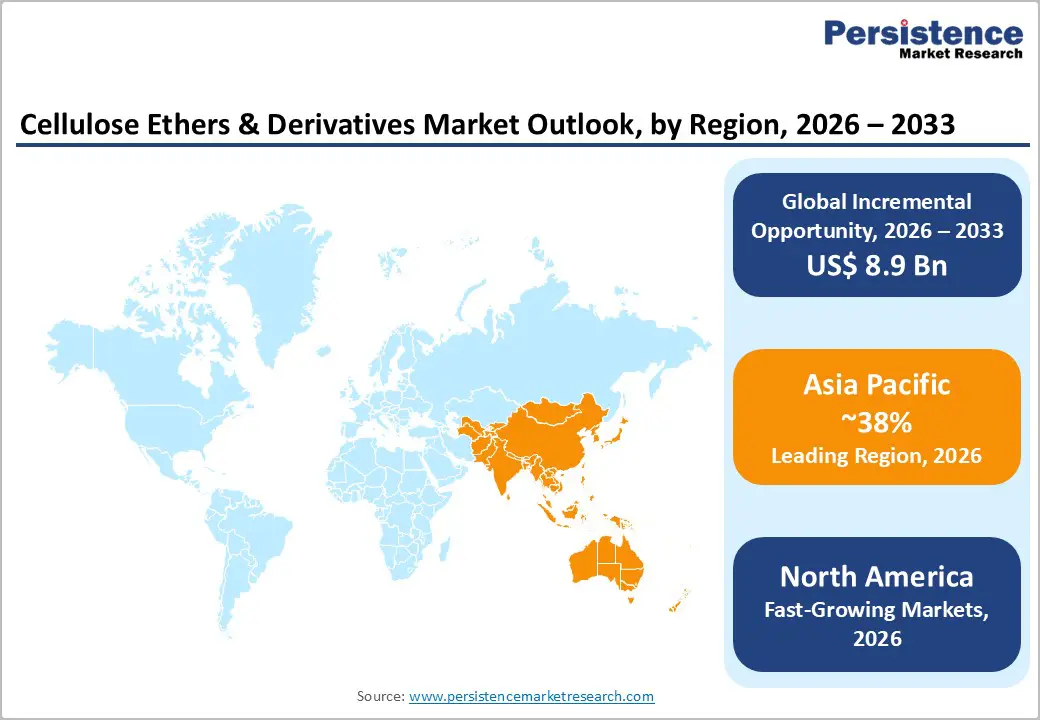

The global cellulose ethers & derivatives market size is expected to be valued at US$ 10.3 billion in 2026 and projected to reach US$ 19.2 billion by 2033, growing at a CAGR of 9.3% between 2026 and 2033.

Growth is driven by rising demand from construction and pharmaceutical industries, where cellulose ethers function as essential thickeners, stabilizers, and binding agents. Rapid urbanization is accelerating infrastructure development, increasing the consumption of advanced construction additives. At the same time, pharmaceutical manufacturers widely use cellulose derivatives in tablet formulations and controlled-release drug delivery systems. Increasing healthcare expenditure and expanding pharmaceutical production worldwide continue to strengthen demand for high-performance cellulose-based ingredients across multiple industrial applications.

Key Industry Highlights:

- Leading Region: Asia Pacific leads the cellulose ethers & derivatives market with 38% share in 2025, supported by strong construction activity and expanding chemical manufacturing across China and India.

- Leading Application: Construction dominates the market with 42% share in 2025, driven by the extensive use of cellulose ethers in mortars, tile adhesives, and cement-based building materials.

- Leading Product Type: Hydroxypropyl Methyl Cellulose (HPMC) accounted for the largest share at 35% in 2025, widely used for its superior water-retention and binding properties in construction and pharmaceutical formulations.

- Fastest Growing Region: North America is emerging as the fastest-growing region, supported by expanding pharmaceutical manufacturing and rising demand for advanced construction additives.

- Key Opportunity: Increasing adoption of bio-based cellulose derivatives in personal care and cosmetic formulations is creating strong opportunities amid rising demand for clean-label and sustainable ingredients.

| Key Insights | Details |

|---|---|

|

Cellulose Ethers & Derivatives Size (2026E) |

US$ 10.3 billion |

|

Market Value Forecast (2033F) |

US$ 19.2 billion |

|

Projected Growth CAGR(2026-2033) |

9.3% |

|

Historical Market Growth (2020-2025) |

7.8% |

Market Dynamics

Drivers - Rapid Expansion of Global Construction Activities Increasing Demand for Cellulose Ether Additives

Rapid urbanization and infrastructure expansion across developing and developed economies are significantly increasing the demand for cellulose ethers used as water-retention agents, thickeners, and stabilizers in cement-based materials. These additives enhance the workability, adhesion, and durability of mortars, plasters, and tile adhesives, making them essential in modern construction practices where efficiency and performance are critical.

Large-scale infrastructure programs and residential construction projects continue to boost the consumption of advanced construction chemicals. Urban development initiatives and transportation infrastructure projects across Asia, the Middle East, and parts of Africa are expanding the use of dry-mix mortars and specialty cement products. As builders increasingly prioritize materials that improve application consistency and structural performance, cellulose ether derivatives remain key formulation components in construction materials.

Growing Use of Cellulose Derivatives in Pharmaceutical Drug Formulations and Controlled Release Systems

Rising pharmaceutical production and increasing demand for effective drug delivery systems are driving the use of cellulose ethers and derivatives in medical formulations. These materials function as binders, stabilizers, and controlled-release agents in tablets, capsules, and suspensions, helping maintain dosage stability and improving the performance of oral medications.

The growing prevalence of chronic diseases and expanding global access to healthcare are increasing pharmaceutical manufacturing activity worldwide. Drug developers are adopting multifunctional excipients that improve bioavailability and formulation consistency. Cellulose derivatives such as carboxymethyl cellulose and hydroxypropyl methylcellulose are widely used because of their biocompatibility, safety profile, and ability to support large-scale pharmaceutical production while maintaining formulation stability.

Restraints - Volatility in Cellulose Raw Material Supply and Pricing Driving Production Cost Pressures

Fluctuations in the availability and pricing of cellulose raw materials such as wood pulp and cotton linters create cost uncertainty for manufacturers of cellulose ethers and derivatives. Since these materials serve as the primary feedstock, any disruption in forestry production, agricultural output, or global supply chains can directly affect production costs and operational stability.

Rising raw material prices often force manufacturers to adjust product pricing, which can reduce competitiveness in price-sensitive industries such as paints, coatings, and certain construction materials. Smaller producers are particularly vulnerable to these fluctuations due to limited procurement capacity and lower margins, making it challenging to maintain consistent production levels and long-term supply commitments.

High Regulatory Compliance Requirements for Food and Pharmaceutical Grade Products

Strict regulatory standards governing the production and application of cellulose derivatives in pharmaceutical and food products present a significant barrier for manufacturers. Regulatory authorities require extensive testing, documentation, and quality assurance processes to ensure the safety, purity, and consistency of excipients used in medical and food formulations.

Meeting these regulatory requirements often requires substantial investments in advanced production systems, quality control infrastructure, and certification procedures. Smaller manufacturers may struggle to meet these standards, which limits market entry and slows product approvals. Continuous updates to environmental and safety regulations also increase operational complexity, raising compliance costs and affecting overall profitability across the industry.

Opportunities - Rising Demand for Natural and Bio-Based Ingredients in Personal Care and Cosmetic Formulations

Growing consumer preference for natural, biodegradable, and plant-based ingredients is creating strong opportunities for cellulose ethers and derivatives in personal care and cosmetic products. These materials are widely used as thickeners, stabilizers, and film-forming agents in products such as creams, lotions, shampoos, and gels due to their gentle skin compatibility and sustainable origin.

Cosmetic brands are increasingly adopting clean-label formulations that replace synthetic additives with bio-based alternatives. Cellulose derivatives derived from renewable plant sources align well with sustainability trends and environmentally responsible product development. As global beauty and personal care manufacturers continue emphasizing eco-friendly formulations and transparency in ingredient sourcing, demand for cellulose-based functional ingredients is expected to expand across premium and mass-market cosmetic segments.

Increasing Adoption of Sustainable and Green Building Materials in Construction Projects

The global push toward sustainable construction practices is opening new growth opportunities for cellulose ether manufacturers. Governments and construction organizations are encouraging the use of environmentally friendly additives that reduce emissions and improve energy efficiency in building materials, where cellulose derivatives play an important functional role.

Cellulose ethers are widely incorporated into eco-friendly mortars, plasters, and tile adhesives because they enhance water retention, durability, and application efficiency while remaining non-toxic and biodegradable. As green building certifications and sustainable infrastructure initiatives gain momentum worldwide, construction companies are increasingly integrating environmentally responsible materials, creating a favorable environment for expanded adoption of cellulose-based construction additives.

Category-wise Insights

By Product Type

Hydroxypropyl Methyl Cellulose (HPMC) dominates the cellulose ethers and derivatives market, accounting for approximately 35% of the market share in 2025. Its widespread use is driven by strong water-retention, thickening, and film-forming capabilities that improve the performance of cement-based materials and pharmaceutical formulations. In construction applications, HPMC enhances workability, adhesion, and crack resistance in mortars, tile adhesives, and plasters, making it a preferred additive for modern building materials.

Hydroxyethyl Cellulose (HEC) is emerging as one of the fastest-growing product categories due to its increasing use in paints, coatings, and personal care formulations. The compound provides excellent rheology control and stabilizing properties, which help improve texture, consistency, and shelf stability in liquid formulations. Rising demand for advanced coatings and cosmetic products is accelerating the adoption of HEC across multiple industries.

By Application

Construction leads the cellulose ethers and derivatives market, holding around 42% share in 2025. The sector extensively uses these materials in dry-mix mortars, gypsum plasters, and cement-based formulations where they improve water retention, bonding strength, and application efficiency. Rapid urbanization, housing developments, and infrastructure expansion are significantly increasing the consumption of construction chemicals that enhance durability and workability in building materials.

The pharmaceutical segment is emerging as the fastest-growing application area as drug manufacturers increasingly adopt cellulose derivatives in tablet coatings, binders, and controlled-release drug delivery systems. Their biocompatibility, stability, and ability to regulate drug release make them highly suitable for modern pharmaceutical formulations. Expanding healthcare access and rising global pharmaceutical production continue to support the growing use of these functional excipients.

Regional Insights

North America Cellulose Ethers & Derivatives Market Trends

North America holds a significant position in the cellulose ethers and derivatives market, accounting for around 31% of global demand. The region benefits from well-established pharmaceutical manufacturing, advanced construction practices, and strong adoption of high-performance chemical additives. The United States remains the primary contributor, supported by continuous residential renovation, commercial infrastructure upgrades, and growing pharmaceutical research activities.

Increasing demand for advanced construction materials and high-quality pharmaceutical excipients continues to drive regional consumption. Cellulose derivatives are widely used in drywall compounds, tile adhesives, and cement-based formulations to improve durability and workability. At the same time, pharmaceutical companies are expanding the use of cellulose-based excipients in drug delivery systems and tablet formulations, supporting innovation and strengthening the region’s role in high-value specialty chemical applications.

Europe Cellulose Ethers & Derivatives Market Trends

Europe represents a mature but steadily expanding market for cellulose ethers and derivatives, with the region expected to grow at a CAGR of about 6.1% during the forecast period. Strong regulatory frameworks, advanced construction technologies, and a well-developed pharmaceutical sector support stable demand for cellulose-based functional additives across multiple industries.

The region is also witnessing growing adoption of environmentally sustainable construction materials and specialty coatings. Cellulose derivatives are widely incorporated into eco-friendly building products, paints, and personal care formulations because of their biodegradable and low-toxicity characteristics. Increasing emphasis on sustainable manufacturing practices and strict quality standards across European industries continues to encourage innovation and the development of high-performance cellulose-based materials.

Asia Pacific Cellulose Ethers & Derivatives Market Trends

Asia Pacific dominates the global cellulose ethers and derivatives market, accounting for approximately 38% of total demand in 2025. The region’s strong position is supported by rapid industrialization, large-scale infrastructure development, and the presence of major chemical manufacturing hubs. Countries such as China, India, and Japan contribute significantly to regional production and consumption.

Urban expansion and increasing infrastructure investment across emerging economies continue to strengthen demand for construction chemicals and building additives. In addition, the region’s growing pharmaceutical and personal care industries are expanding the use of cellulose derivatives in formulations and cosmetic products. The availability of raw materials, cost-effective manufacturing capabilities, and increasing domestic consumption further support the expansion of cellulose ether production and application across Asia Pacific.

Competitive Landscape

The cellulose ethers and derivatives market is characterized by moderate consolidation, with several established manufacturers maintaining strong positions through integrated production capabilities and global distribution networks. Companies are increasingly focusing on expanding manufacturing facilities, particularly in regions with growing construction and pharmaceutical demand. Investment in advanced processing technologies and improved product performance remains a key strategy to strengthen competitiveness.

Market participants are prioritizing research and development to create bio-based and environmentally sustainable cellulose derivatives. Innovation in formulation performance, sustainability certifications, and environmentally responsible production practices is becoming an important differentiator. At the same time, the presence of numerous regional and mid-sized producers keeps the competitive environment dynamic, encouraging continuous product development and strategic collaborations across the industry.

Key Developments:

- In June 2025, Dow Inc. introduced eco-friendly hydroxypropyl methylcellulose (HPMC) grades designed to align with sustainability requirements under the EU Green Deal, targeting improved performance and environmental compliance for construction materials such as tile adhesives, mortars, and advanced dry-mix formulations.

- In March 2024, Ashland Global Holdings Inc. expanded its pharmaceutical-grade carboxymethyl cellulose production facility in Ireland to strengthen supply for pharmaceutical excipients. The expansion increased manufacturing capacity and supported growing global demand for high-purity cellulose derivatives used in drug formulations.

- In October 2024, Shin-Etsu Chemical Co., Ltd. introduced new high-viscosity cellulose ether grades for paints and coatings, developed through a collaboration with BASF SE, aiming to enhance rheology control, stability, and formulation performance in advanced coating applications.

Companies Covered in Cellulose Ethers & Derivatives Market

- Ashland Global Holdings Inc.

- Dow Inc.

- Shin-Etsu Chemical Co., Ltd.

- Nouryon

- CP Kelco

- Lotte Fine Chemical

- AkzoNobel

- Daicel Corporation

- J.M. Huber Corporation

- Shandong Head Co., Ltd.

- DKS Co., Ltd.

- Celanese Corporation

- Eastman Chemical Company

- Rayonier Advanced Materials

- Borregaard

Frequently Asked Questions

The global cellulose ethers & derivatives market is projected to be valued at US$ 10.3 billion in 2026, growing to US$ 19.2 billion by 2033 at a 9.3% CAGR.

Growth is primarily driven by expanding construction and pharmaceutical industries, with construction accounting for 42% share in 2025 due to rising demand for advanced building additives.

Asia Pacific leads with 38% share in 2025, supported by strong manufacturing capacity and large-scale construction activity across major economies.

A major opportunity lies in the growing adoption of bio-based cellulose derivatives in personal care products, driven by increasing demand for sustainable and clean-label formulations.

Leading companies include Dow Inc., Ashland Global Holdings Inc., Shin-Etsu Chemical Co., Ltd., Daicel Corporation, and Nouryon, focusing on product innovation and global capacity expansion.