- Specialty & Fine Chemicals

- Cellulose Derivative Excipient Market

Cellulose Derivative Excipient Market Size, Share, and Growth Forecast 2026 – 2033

Cellulose Derivative Excipient Market by Product Type (Hypromellose, Microcrystalline Cellulose, Hydroxypropyl Cellulose, CMC, Methyl Cellulose, Ethyl Cellulose), Function (Pharmaceutical Coatings, Bio-adhesives, Drug Delivery Systems, Binders & Disintegrants, Other), Application (Pharmaceuticals, Food & Beverages, Cosmetics & Personal Care, Others), and Regional Analysis for 2026–2033

Cellulose Derivative Excipient Market Size and Trend Analysis

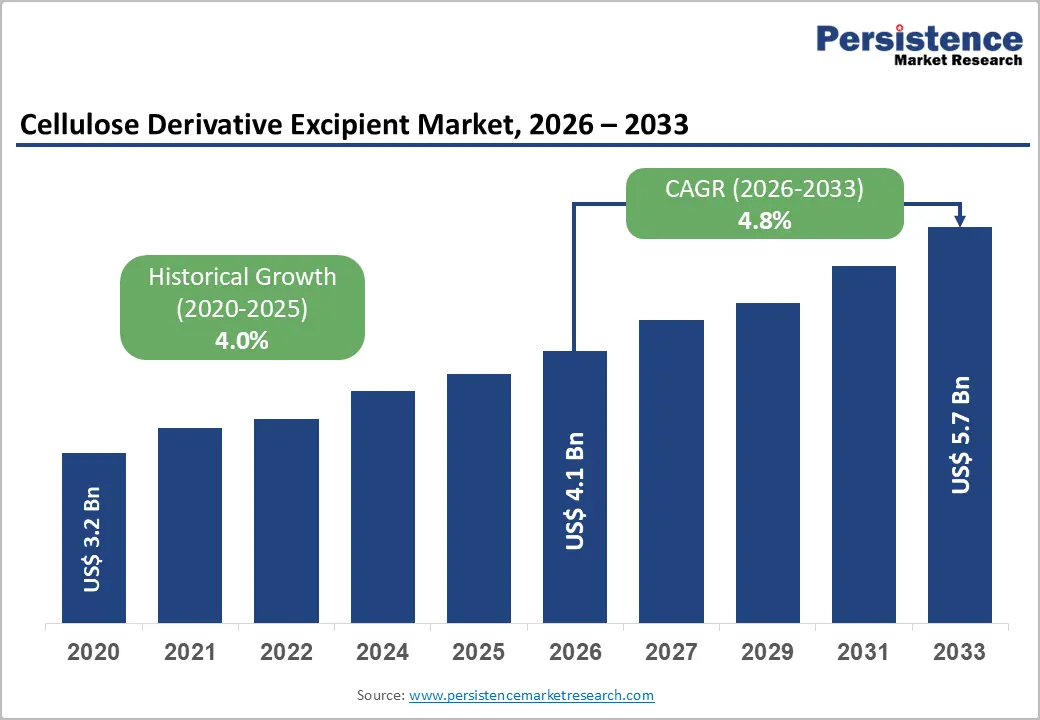

The global cellulose derivative excipient market is valued at US$ 4.1 billion in 2026 and is projected to reach US$ 5.7 billion, growing at a CAGR of 4.8% between 2026 and 2033.

The market's steady expansion is driven by surging global pharmaceutical output, where cellulose derivatives serve as indispensable functional excipients that enhance drug bioavailability, tablet integrity, and controlled-release performance. Robust demand from generic drug manufacturers in emerging economies, coupled with stricter regulatory requirements for excipient quality under frameworks such as ICH Q8 and USP/NF, further reinforces consistent market growth. Additionally, broadening applications in food texturizers and personal care formulations contribute incremental demand, sustaining multi-sector momentum through the forecast period.

Key Industry Highlights:

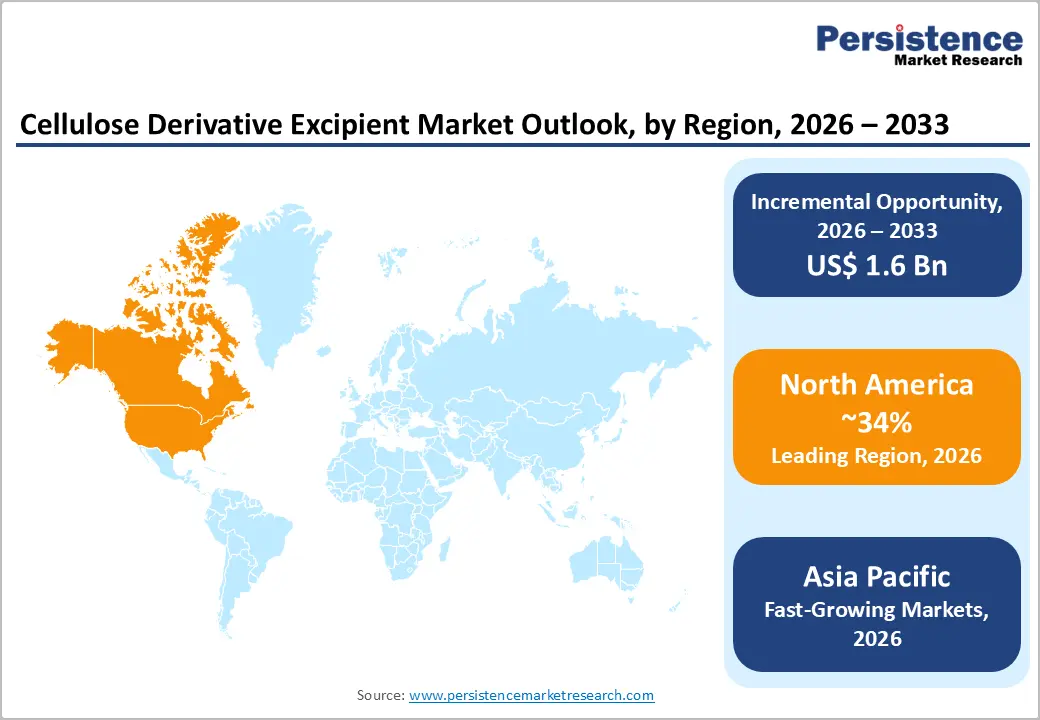

- Leading Region: North America leads the cellulose derivative excipient market with approximately 34% revenue share, driven by mature pharmaceutical manufacturing, FDA regulatory requirements, and the presence of key producers such as Ashland Global Holdings and Colorcon Inc.

- Fastest Growing Region: Asia Pacific is the fast-growing, expanding at an estimated CAGR of 6.1%, supported by rapid generic pharmaceutical expansion in China and India, growing food processing industries, and increasing domestic excipient manufacturing capacities.

- Dominant Segment: Hypromellose (HPMC) is the dominant product type with approximately 35% share, underpinned by its versatility in film coating, controlled-release matrices, and HPMC capsule applications across global pharmaceutical formulations.

- Fast-Growing Segment: The drug delivery systems function segment is among the fast-growing, propelled by increasing adoption of extended-release oral formulations, amorphous solid dispersions, and HPMC-based matrix technologies by pharmaceutical innovators and generic manufacturers alike.

- Key Opportunity: Expanding plant-based food and clean-label ingredient markets present a strategic growth avenue, with cellulose derivatives such as HPMC and CMC gaining traction as GRAS-certified texturizers and fat replacers in vegan food formulations globally.

DRO Analysis

Drivers- Rising Pharmaceutical Production and Generic Drug Expansion

Global pharmaceutical production volumes have expanded materially over the past decade, with the World Health Organization (WHO) noting a significant scale-up of generic medicine supply in low- and middle-income countries. Cellulose derivatives such as Hypromellose (HPMC) and Microcrystalline Cellulose (MCC) are ubiquitous in solid dosage formulations, acting as binders, film-coating polymers, and controlled-release matrices.

According to the U.S. Food and Drug Administration (FDA), generic drugs account for approximately 90% of all U.S. prescriptions dispensed, a proportion that directly translates to high and recurring excipient demand. As patent cliffs accelerate generic launches globally, demand for performance-grade cellulose derivative excipients is set to rise commensurately.

Stringent Pharmaceutical Regulatory Requirements Elevating Excipient Quality Standards

Regulatory bodies worldwide, including the European Medicines Agency (EMA) and the U.S. FDA, have progressively tightened excipient quality standards under GMP guidelines and pharmacopoeial monographs such as those published in the European Pharmacopoeia (Ph. Eur.) and United States Pharmacopeia (USP).

The International Pharmaceutical Excipients Council (IPEC) has further promoted excipient Good Manufacturing Practice certification, compelling drug manufacturers to source cellulose derivatives from audited, high-compliance suppliers. This regulatory dynamic rewards established producers with superior documentation and quality systems, simultaneously raising barriers to entry and stimulating market growth among premium-grade excipient manufacturers.

Restraints - Raw Material Price Volatility and Supply Chain Disruptions

Cellulose derivatives are derived primarily from wood pulp and cotton linters, commodities that are subject to price fluctuations driven by forestry regulations, weather events, and competing end-use demand.

According to the Food and Agriculture Organization (FAO), global wood pulp production has faced periodic supply constraints, amplified by increasing sustainability mandates in Northern European and North American forest-management regimes. Supply chain disruptions witnessed during 2021–2022 underscored the sector's vulnerability to logistics bottlenecks and energy cost spikes in chemical processing. Such cost pressures compress margins for excipient producers and may translate into price increases that dampen purchasing volumes, particularly among cost-sensitive generic pharmaceutical and food-ingredient buyers.

Complex Manufacturing Processes and High Capital Investment Requirements

The production of pharmaceutical-grade cellulose derivatives involves multi-stage chemical modification processes, etherification, purification, and drying, that demand specialized reactor systems and rigorous quality control protocols. Capital expenditure for greenfield cellulose derivative facilities can be substantial, often exceeding USD 50–100 million for integrated plants, limiting market participation to well-capitalized incumbents.

Smaller manufacturers in developing regions face challenges in achieving USP/Ph. Eur. compliance without significant technical upgrading, creating a structural entry barrier. Furthermore, scale-up from laboratory to commercial production is technically complex, elongating time-to-market for novel cellulose derivatives and restricting the pace of product innovation.

Opportunities - Growth in Oral Drug Delivery Systems and Modified-Release Formulations

The global shift toward oral solid dosage forms, particularly modified-release and enteric-coated formulations, represents a significant opportunity for cellulose derivative excipient manufacturers. The U.S. FDA has approved a growing number of extended-release drug products under NDA and ANDA pathways, with HPMC-based matrices being a preferred enabling technology.

The global drug delivery systems sector continues to exhibit robust growth, with oral drug delivery accounting for the dominant share of formulation innovation. Cellulose-based hydrophilic matrix technology enables precise drug release kinetics that reduce dosing frequency and improve patient compliance, making these excipients strategically indispensable in next-generation pharmaceutical development pipelines.

Expanding Applications in Plant-Based and Clean-Label Food Formulations

Consumer demand for clean-label, plant-derived, and vegan-friendly food ingredients is accelerating globally. Cellulose derivatives such as Hydroxypropyl Methylcellulose (HPMC) and Carboxymethyl Cellulose (CMC) are increasingly used as fat replacers, texturizers, and emulsifiers in plant-based meat analogues, dairy alternatives, and low-calorie food products.

The European Food Safety Authority (EFSA) and the U.S. FDA both recognize these derivatives as GRAS (Generally Recognized as Safe), providing regulatory confidence for food-industry adoption. With the global plant-based food market expanding rapidly, driven by sustainability awareness and dietary health trends, cellulose derivative producers have a compelling avenue to diversify revenue streams beyond their traditional pharmaceutical customer base.

Category-wise Analysis

Product Type Insights

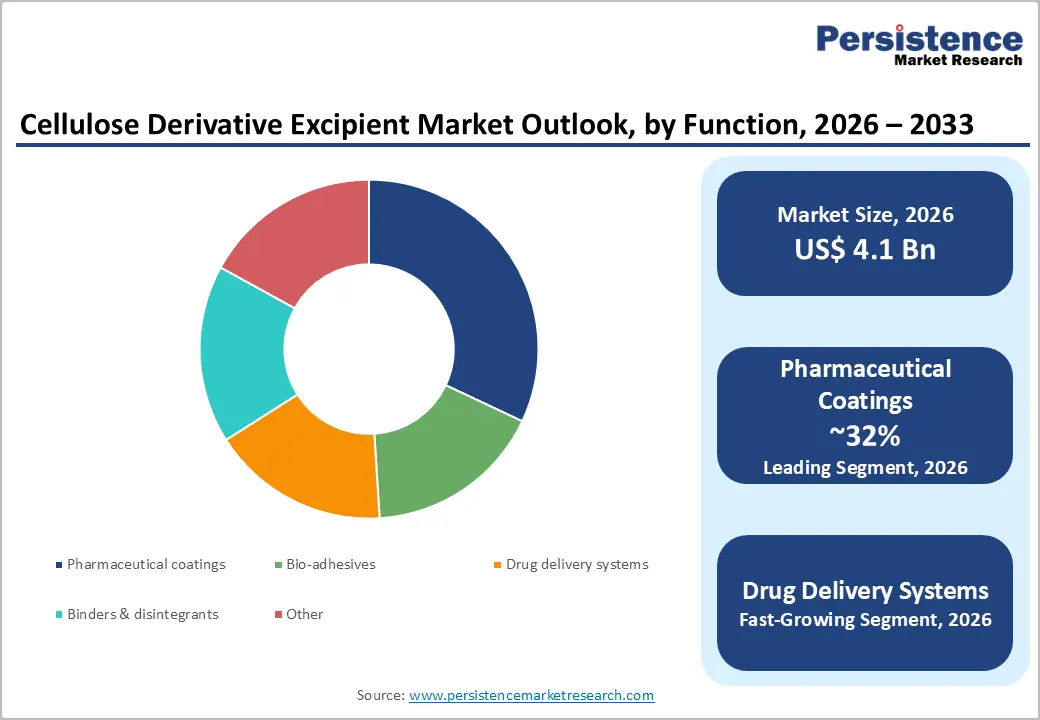

Among all product type segments, hypromellose (HPMC) holds the leading position, commanding approximately 35% of the cellulose derivative excipient market. HPMC's dominance is attributable to its unparalleled versatility across multiple pharmaceutical functions, film coating, matrix-based controlled release, capsule shells, and ophthalmic formulations, as well as its inclusion in all major pharmacopoeial compendia, including USP, Ph. Eur., and JP (Japanese Pharmacopoeia). Its excellent water solubility, non-ionic character, and thermal gelation properties make it a preferred polymer in sustained-release tablet formulations. Additionally, the shift toward vegetarian HPMC capsules as alternatives to gelatin capsules has opened a secondary demand avenue, further reinforcing HPMC's market leadership.

Function Insights

The pharmaceutical coatings segment leads the function category, accounting for an estimated 32% share in 2026. Pharmaceutical film coating is a high-value application where cellulose derivatives, particularly HPMC and ethyl cellulose, are used to mask taste, improve tablet aesthetics, provide moisture protection, and enable enteric or sustained-release characteristics. The FDA and EMA both specify excipient quality benchmarks in coating applications, ensuring that premium cellulose grades remain preferred. Growing output of solid oral dosage forms and increasing adoption of film coating over sugar coating are reinforcing this segment's dominance. Innovation in aqueous coating systems using HPMC-based formulations continues to stimulate R&D investment in this function segment.

Application Insights

The pharmaceuticals application segment dominates with approximately 62% of total revenue in 2026. This leadership stems from the broad functional utility of cellulose derivatives across solid dosage forms, semi-solid topical formulations, and ophthalmic products. Cellulose excipients are compendially recognized and included in thousands of approved drug formulations globally.

Growth in the pharmaceutical segment is further underpinned by increasing chronic disease prevalence, aging demographics, and rising healthcare expenditure in markets such as the United States, Germany, China, and India. The Food & Beverages segment ranks second, benefiting from growing demand for cellulose-based stabilizers and texture agents in processed food products.

Regional Analysis

North America Cellulose Derivative Excipient Market Trends & Analysis

North America represents a substantial regional market for cellulose derivative excipients, accounting for approximately 34% of global revenue. The region's leadership is underpinned by its mature pharmaceutical manufacturing base, concentrated in the United States, which hosts the world's largest generic and branded drug markets. However, the implementation of U.S. tariffs on chemical imports, particularly from Asia, has created some supply-chain realignment pressure, with domestic producers potentially benefiting from import substitution but also facing higher input costs for wood pulp sourced internationally.

U.S. Cellulose Derivative Excipient Market Size

The United States accounts for approximately 28% of the global cellulose derivative excipient market revenue in 2026. Driven by a $550 billion pharmaceutical industry and high per capita prescription rates, demand for excipients remains structurally strong. Robust regulatory infrastructure through the U.S. FDA's drug approval processes drives consistent demand for pharmacopoeial-grade excipients.

Europe Cellulose Derivative Excipient Market Trends, Drivers, & Insights

Europe is the second-largest market, with Germany, the U.K., and France serving as primary demand centers. European sustainability directives, such as the EU Green Deal and bio-based economy initiatives, are encouraging the substitution of synthetic additives with bio-derived cellulose derivatives in food and personal care applications. Geopolitical factors, including tensions arising from the Russia-Ukraine conflict, have affected wood pulp logistics from Eastern European sourcing regions, creating some supply risk.

Germany Cellulose Derivative Excipient Market Size

Germany, home to BASF SE and major pharmaceutical manufacturers, commands an estimated 8% of global market revenue. The country's chemical sector leadership and strong pharmaceutical exports underpin robust cellulose excipient consumption. Germany's progressive adoption of REACH compliance requirements also influences excipient procurement standards.

U.K. Cellulose Derivative Excipient Market Size

The United Kingdom represents a portion of the European market. Post-Brexit regulatory alignment with the MHRA framework has created some procurement complexity, though the country's pharmaceutical sector, anchored by companies such as AstraZeneca and GSK, continues to drive consistent excipient demand.

France Cellulose Derivative Excipient Market Size

France contributes approximately nearly a fraction of the European cellulose derivative excipient market. The country's focus on specialty pharmaceutical formulations and presence of companies such as Roquette Frères as a global excipient supplier positions France as both a production and consumption hub within the European landscape.

Asia Pacific Cellulose Derivative Excipient Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market, expanding at an estimated CAGR of 6.1% during the forecast period. The region's growth is driven by rapid pharmaceutical industry expansion in China and India, the world's largest generic drug manufacturing hubs, as well as growing food processing industries across Southeast Asia. Recent U.S. tariff actions targeting Chinese chemical exports have prompted some supply-chain diversification, with Indian and Southeast Asian producers gaining market access opportunities.

China Cellulose Derivative Excipient Market Size

China is likely to register a leading share in 2026. Domestic producers such as Anhui Sunhere Pharmaceutical and Lotte Fine Chemicals serve both the local pharmaceutical sector and global export markets. The National Medical Products Administration has strengthened excipient regulation, elevating quality benchmarks and spurring consolidation among local manufacturers.

India Cellulose Derivative Excipient Market Size

India accounts for a leading regional market revenue and is among the fastest-growing markets. India's status as the world's largest generic drug exporter, supplying over 20% of global generic medicine volumes per the Pharmaceuticals Export Promotion Council of India (Pharmexcil), ensures high demand for cellulose excipients. Sigachi Industries and Accent Microcell are notable domestic producers catering to both local and export demand.

Japan Cellulose Derivative Excipient Market Size

Japan is home to several leading global producers, including Shin-Etsu Chemical and Asahi Kasei Corporation, both globally recognized leaders in pharmaceutical-grade cellulose derivatives. Japan's aging population and high pharmaceutical consumption per capita sustain a stable, quality-driven demand environment.

Competitive Landscape

The global cellulose derivative excipient market exhibits a moderately consolidated competitive structure, where the top five players collectively account for approximately 55–60% of global revenue. Market leaders such as Shin-Etsu Chemical, Ashland Global Holdings, and DuPont de Nemours differentiate through proprietary manufacturing technologies, pharmacopoeial compliance across multiple global compendia, and extensive technical support services.

Key strategies include vertical integration from pulp sourcing, capacity expansions in the Asia Pacific, and strategic acquisitions to broaden product portfolios. Emerging manufacturers from India and China are intensifying price-based competition in commodity excipient grades, while multinationals focus on specialty and high-purity segments to maintain margin superiority.

Key Developments:

- March 2026: BASF announced collaboration initiatives and portfolio expansion focused on sustainable material solutions and advanced specialty chemicals. Such developments strengthen BASF’s innovation capabilities and broader pharmaceutical and specialty ingredient ecosystem, supporting future opportunities in excipient and formulation-related applications across healthcare and life sciences markets.

- October 2025: Biogrund announced an exclusive distribution agreement with Shin-Etsu for pharmaceutical excipients in Spain, effective January 2026. The partnership expands access to cellulose-derived excipients such as HPMC, HPMC-AS, and L-HPC, strengthening regional supply capabilities and supporting formulation development for solid oral dosage products in the pharmaceutical market.

- October 2025: Ashland announced the appointment of Tilley Distribution as its exclusive U.S. distribution partner for food and beverage ingredients. The agreement includes Ashland’s cellulose-based products, such as CMC, methylcellulose, HPMC, and HPC, expanding market reach and strengthening supply availability for cellulose-derived specialty ingredient applications across food, nutraceutical, and related industries.

Global Cellulose Derivative Excipient Market – Key Insights &Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 3.2 Bn |

|

Current Market Value (2026) |

US$ 4.1 Bn |

|

Projected Market Value (2033) |

US$ 5.7 Bn |

|

CAGR (2026–2033) |

4.8% |

|

Leading Region |

North America, ~34% |

|

Dominant Segment |

Hypromellose (HPMC), ~35% |

|

Top-ranking Function Segment |

Pharmaceutical Coatings, ~32% |

|

Incremental Opportunity (2026–2033) |

US$ 1.6 Bn |

Companies Covered in Cellulose Derivative Excipient Market

- Shin-Etsu Chemical

- Ashland Global Holdings

- JRS Pharma GmbH

- DuPont de Nemours

- BASF SE

- Colorcon Inc.

- CP Kelco

- Asahi Kasei Corporation

- Nippon Paper Industries

- IFF (International Flavors & Fragrances)

- Roquette Frères

- Sigachi Industries

- Lotte Fine Chemicals

- Accent Microcell

- Anhui Sunhere Pharmaceutical

- Dow Inc. (Dow Pharma Solutions)

- Nouryon

- SE Tylose GmbH & Co. KG

Frequently Asked Questions

The global Cellulose Derivative Excipient market is valued at US$ 4.1 Bn in 2026 and is projected to reach US$ 5.7 Bn by 2033, recording a CAGR of 4.8% during the 2026–2033 forecast period.

The primary demand drivers include rising global pharmaceutical production, especially generic drug manufacturing, where cellulose derivatives serve as essential binders, film-coaters, and controlled-release polymers. Additionally, stringent regulatory quality standards from the U.S. FDA, EMA, and pharmacopoeial bodies such as USP and Ph. Eur. compel pharmaceutical manufacturers to source high-grade excipients from certified suppliers.

Hypromellose (HPMC) is the leading product segment, accounting for approximately 35% of the market. Its dominance is driven by wide pharmacopoeial recognition, multifunctional utility in film coating and controlled-release matrices, and growing adoption in HPMC-based vegetarian capsule formulations across global pharmaceutical manufacturing.

North America is the leading region, accounting for approximately 34% of global revenue in 2026. The region's leadership is supported by its large pharmaceutical industry, mature regulatory infrastructure through the U.S. FDA, and the presence of major excipient producers, including Ashland Global Holdings and Colorcon Inc.

Key opportunities include the expanding oral drug delivery and modified-release formulation market, where HPMC-based controlled-release matrices are increasingly adopted for next-generation drug products. Additionally, surging demand for plant-based and clean-label food ingredients is creating new application avenues for HPMC and CMC as GRAS-certified texturizers and fat replacers in vegan food formulations.

Leading companies in the cellulose derivative excipient market include Shin-Etsu Chemical, Ashland Global Holdings, JRS Pharma GmbH, DuPont de Nemours, BASF SE, Colorcon Inc., CP Kelco, Asahi Kasei Corporation, Nippon Paper Industries, IFF, Roquette Frères, Sigachi Industries, Lotte Fine Chemicals, Accent Microcell, and Anhui Sunhere Pharmaceutical.