- Telecommunications

- Carrier Ethernet Access Devices Market

Carrier Ethernet Access Devices Market Size, Share, and Growth Forecast, 2026 - 2033

Carrier Ethernet Access Devices Market by Device Type (Switches, Routers, Hubs), End-User (Telecommunications, IT & Networking, Enterprises, Government), Deployment Mode (On-premises, Cloud), and Regional Analysis for 2026-2033

Carrier Ethernet Access Devices Market Share and Trends Analysis

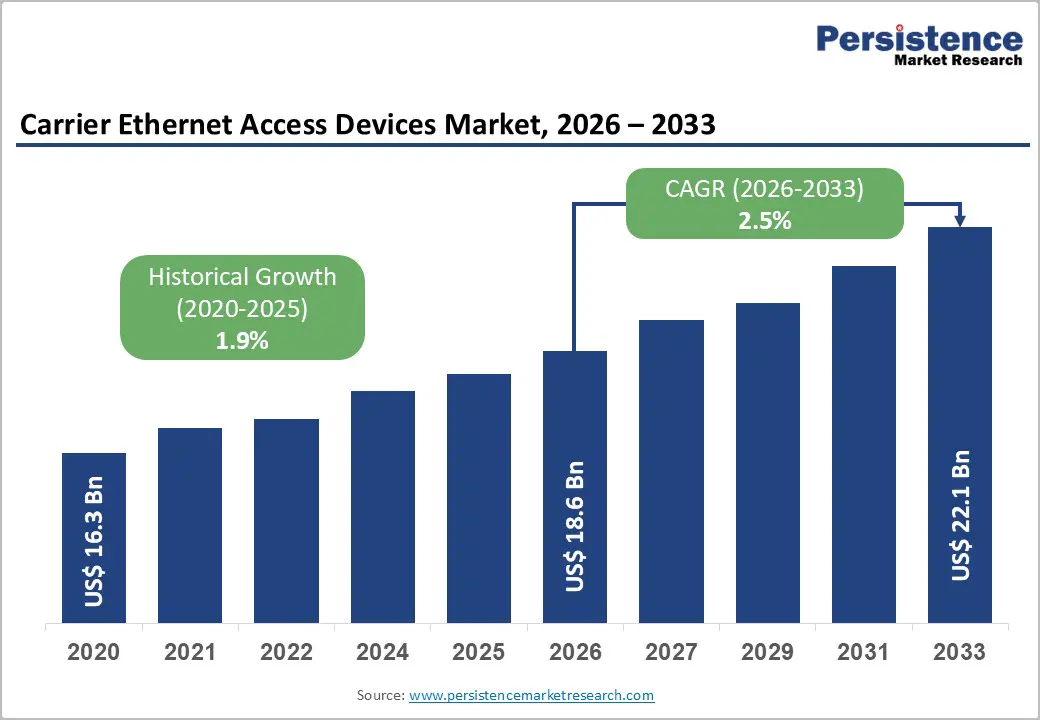

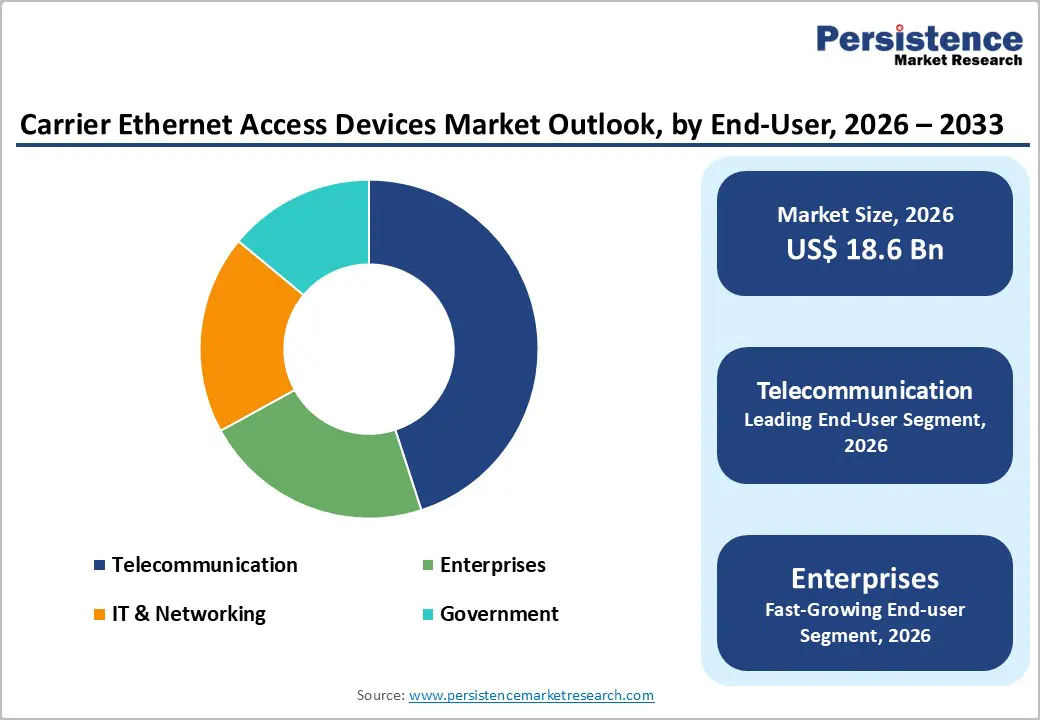

The global carrier ethernet access devices market size is likely to be valued at US$ 18.6 billion in 2026, and is projected to reach US$ 22.1 billion by 2033, growing at a CAGR of 2.5% during the forecast period 2026−2033.

The market's steady growth trajectory is underpinned by accelerating enterprise digital transformation initiatives, widespread 5G infrastructure deployment, and the escalating demand for high-bandwidth, low-latency connectivity across industries. Network operators and enterprises are increasingly replacing legacy time division multiplexing (TDM)-based architectures with scalable Ethernet-based access solutions that deliver superior performance at lower operational costs.

Carrier Ethernet access devices (CEADs) serve as critical junction points between service provider networks and end-user environments, enabling the delivery of Metro Ethernet, business broadband, and cloud interconnect services. The proliferation of cloud-native applications, software-defined networking (SDN), and network function virtualization (NFV) is reshaping procurement patterns, with buyers prioritizing programmability, centralized management, and multi-service capability alongside traditional bandwidth and reliability metrics.

Key Industry Highlights

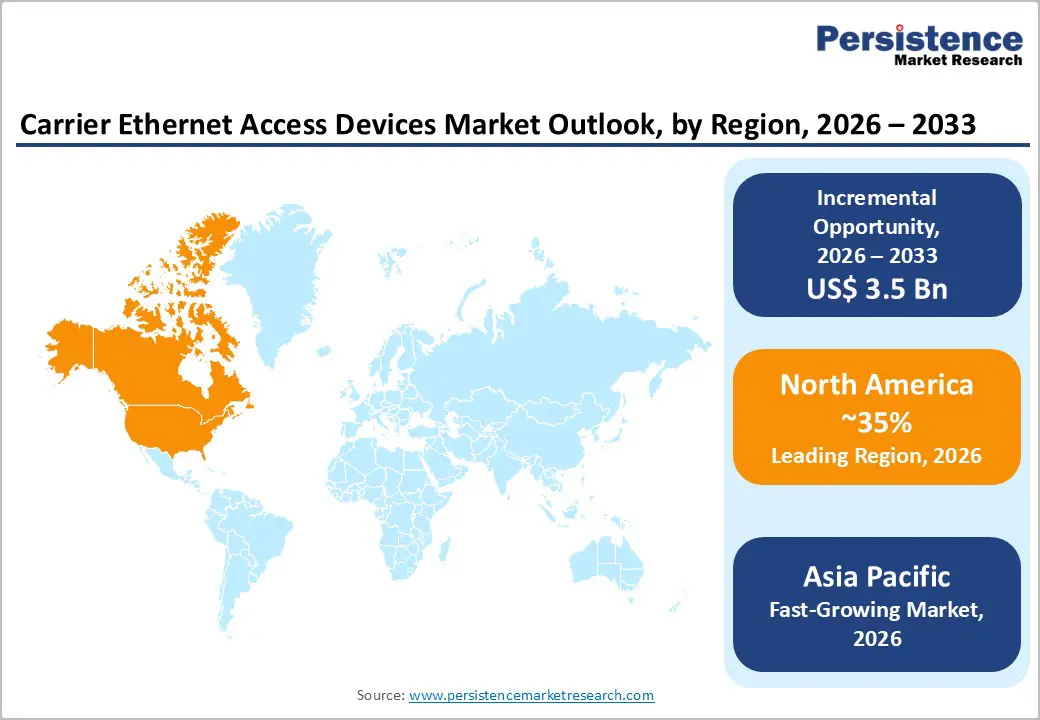

- Dominant Region: North America is expected to command about 35% market share in 2026, aided by its advanced technological ecosystem and high concentration of market players.

- Fastest-growing Region: The Asia Pacific market is set to be the fastest-growing during the 2026-2033 forecast period, due to the rapid digital transformation occurring in China and India.

- Leading & Fastest-growing Device Type: Switches are slated to lead with approximately 58% revenue share in 2026, while routers are likely to be the fastest-growing segment through 2033.

- Leading & Fastest-growing Application: Telecommunication is poised to capture roughly 45% revenue share in 2026, whereas enterprises are expected to grow the fastest over the 2026-2033 forecast period.

- Key Driver: Global 5G network rollouts are generating substantial demand for high-capacity Ethernet access infrastructure, prompting telecom operators to invest heavily in these networks.

- Key Opportunity: The convergence of operational technology and information technology networks is driving fresh demand for rugged CEADs in industrial settings.

| Key Insights | Details |

|---|---|

|

Carrier Ethernet Access Devices Market Size (2026E) |

US$ 18.6 Bn |

|

Market Value Forecast (2033F) |

US$ 22.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

2.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

1.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerating 5G Infrastructure Deployment and Backhaul Demand

Global 5G deployments are escalating the demand for carrier Ethernet access devices (CEADs) that support fronthaul and backhaul in dense small cell networks. Telecom operators are investing in fiber based Ethernet infrastructure to meet capacity and latency requirements, with each site requiring multiple access ports. Policy support from the Federal Communications Commission (FCC) through Open Radio Access Network (ORAN) initiatives and the European Union (EU) Gigabit Connectivity Plan is accelerating adoption of open and scalable architectures. This environment is strengthening procurement of carrier grade Ethernet solutions and expanding network upgrade cycles.

Operators are prioritizing low latency and high reliability as data traffic rises from mobile usage and Internet of Things (IoT) applications. CEADs are enabling seamless integration between edge nodes and core networks, which supports real time services such as autonomous mobility and remote healthcare. Open RAN frameworks are reducing vendor lock in and increasing supplier competition, while fiber investments are ensuring long term scalability. This shift is positioning Ethernet access infrastructure as a critical layer in next generation telecom networks and is supporting sustained innovation and deployment efficiency.

Enterprise Digital Transformation and Cloud Adoption

Enterprise investment in digital infrastructure is driving demand for high performance network upgrades. Organizations are migrating workloads to hybrid and multi cloud environments, which require deterministic Ethernet with strict service level agreement (SLA) guarantees. CEADs are delivering low latency and high availability for applications such as unified communications, financial systems, and industrial automation. Standards from the Metro Ethernet Forum (MEF), including CE 2.0 and MEF 3.0, are enhancing interoperability and service consistency across distributed enterprise networks.

Network transformation is accelerating as firms prioritize real time data exchange and operational resilience. CEADs are integrating with wide area network (WAN) architectures to support seamless connectivity across locations. Providers are deploying certified solutions that meet enterprise performance requirements, while edge demarcation is improving flexibility in hybrid setups. This approach is enabling secure access for remote workforces and reducing downtime through enforced SLAs. As traffic volumes grow, enterprises are strengthening infrastructure readiness for emerging use cases such as edge computing, which is reinforcing long term efficiency and scalability.

Competition from Integrated Networking Platforms and SD-WAN

Software-defined wide area network (SD WAN) platforms are reshaping enterprise access by shifting from hardware centric carrier Ethernet access devices to software driven architectures on standard infrastructure. Organizations are prioritizing simplified management across branch and remote sites, using policy based traffic routing over multiple links. SD WAN overlays are supporting cloud applications such as collaboration tools and software-as-a-service (SaaS) platforms, while integrated security and optimization features are reducing system complexity. This transition is enabling faster deployment and lower operational overhead for mid-sized enterprises.

Convergence between SD WAN and Ethernet is redefining CEAD positioning across segments. Large enterprises are retaining CEADs for latency sensitive workloads, while cost focused users are adopting virtualized solutions for agility. Vendors are embedding SD WAN capabilities into CEAD platforms to maintain relevance and expand functionality. Service providers are offering managed hybrid models that combine both technologies, which balances performance with flexibility. This shift is driving a move toward software centric network strategies, encouraging partnerships and enabling scalable infrastructure aligned with evolving digital requirements.

Technological Intricacy and Integration Challenges

Emerging network requirements are challenging CEADs as operators demand higher bandwidth and lower latency. Integration with legacy infrastructure such as TDM systems is creating compatibility issues, which is slowing deployment. Manufacturers are investing in interoperability testing and extended development cycles to ensure stable performance across mixed environments. Service providers are also training teams to manage complex rollouts, which is increasing implementation time and cost. This dynamic is forcing companies to balance innovation with operational reliability.

Rapid technological change is intensifying these constraints as standards and architectures evolve. Vendors are advancing firmware and automation to support legacy systems and simplify configuration, while collaborating with organizations such as the MEF to improve alignment. Enterprises are prioritizing solutions with proven backward compatibility to reduce risk and total cost of ownership. Phased migration strategies are helping manage uncertainty, while adaptable suppliers are strengthening positioning through flexible, scalable offerings.

Industrial IoT and Smart Infrastructure Applications

Convergence of operational technology (OT) and information technology (IT) networks is driving demand for rugged carrier Ethernet access devices CEADs in industrial environments. Smart factories, utilities, and transport systems require deterministic connectivity, which CEADs deliver through time sensitive networking (TSN) capabilities. These devices operate reliably under extreme conditions such as temperature variation and vibration, enabling applications such as smart grids and real time traffic coordination. Manufacturers are deploying CEADs across Industry 4.0 architectures to connect machines and ensure synchronized data flows, which is extending Ethernet adoption beyond traditional enterprise settings.

Adoption is accelerating as OT-IT integration matures across critical sectors. CEADs are supporting low latency automation in logistics, energy, and transportation networks, while standards from organizations such as the International Electrotechnical Commission (IEC) are guiding certification and interoperability. Operators are consolidating infrastructure to reduce costs and improve monitoring, while edge analytics is enabling predictive maintenance. Vendors are strengthening offerings with industrial grade security features to address cyber risks. This shift is positioning CEADs as essential infrastructure for resilient and scalable industrial connectivity.

Growing Emphasis on Digital Transformation across Various Sectors

Digital transformation across sectors such as healthcare, education, and manufacturing is heightening the requirement of advanced CEADs. Organizations are deploying digital systems that require reliable, high capacity connectivity to support real time data exchange. Hospitals are connecting medical equipment for continuous monitoring, schools are enabling virtual learning through high speed networks, and factories are integrating sensors with centralized controls for efficient production. CEADs are bridging legacy infrastructure with modern platforms, which is improving interoperability and enabling scalable network performance.

Smart city programs and IoT deployments are expanding this demand into urban infrastructure. Municipal networks are using CEADs to support traffic systems, public safety, and utility monitoring with low latency connectivity. Governments are partnering with telecom providers to extend fiber networks, while enterprises are leveraging these frameworks for private 5G use cases. Vendors are developing outdoor ready and automated solutions to simplify large scale deployments. This expansion is diversifying revenue streams and is positioning CEADs as a foundational layer for resilient and connected ecosystems

Category-wise Analysis

Device Type Insights

Switches are poised to dominate in 2026, projected to capture nearly 58% of the carrier Ethernet access devices market revenue share, as they manage data traffic efficiently and reduce network congestion. These systems are directing packets across networks with low latency, which supports high throughput environments such as data centers and industrial facilities. Operators are adopting switches for their scalability and reliability, especially as traffic rises from cloud services and IoT deployments. This capability is enabling seamless network expansion and is positioning switches as core infrastructure for carrier grade performance.

Routers are likely to emerge as the fastest-growing devices from 2026 to 2033, on account of rising network complexity and security needs. Ethernet routers are enabling communication between networks while supporting functions such as Network Address Translation (NAT) and Dynamic Host Configuration Protocol (DHCP). Organizations are deploying advanced routers to manage dynamic traffic, enforce security policies, and support cloud and IoT connectivity. Their programmability and integration capabilities are strengthening secure edge networking, which is driving adoption across enterprise and service provider environments.

End-User Insights

Telecommunication is slated to command an approximate 45% of the CEAD market revenue share in 2026, driven by sustained investment in network expansion and service quality. Operators are deploying carrier Ethernet access devices to strengthen backhaul capacity for 5G networks and manage rising data traffic from mobile users. These systems are supporting reliable delivery of voice, video, and data across regions, while enabling broadband expansion. Continuous infrastructure upgrades are helping service providers maintain performance during peak demand and secure long term market positioning.

Enterprises are expected to register the highest CAGR during the 2026-2033 forecast period, powered by the speedy scaling of digital operations across industries. Businesses are using CEADs to connect distributed sites, support cloud computing, and enable secure communication across teams. Adoption is rising with hybrid work models and increasing reliance on real time applications such as video conferencing and cloud platforms. Organizations are prioritizing network reliability, low latency, and security to maintain operational continuity, which is driving demand for scalable Ethernet access solutions.

Regional Insights

North America Carrier Ethernet Access Devices Market Trends

North America is predicted to account for about 35% of the carrier Ethernet access devices market share in 2026, supported by a mature telecom ecosystem and strong innovation base. The region hosts major vendors and service providers, which is accelerating development of advanced network equipment. Continuous upgrades to fiber infrastructure and early adoption of 5G and edge computing are driving demand for high performance access solutions. Public investment in broadband expansion is also improving connectivity across underserved areas, which is strengthening regional market growth.

Digital transformation across the United States and Canada is reinforcing this momentum through smart city programs and enterprise modernization. Organizations are deploying CEADs to support hybrid cloud environments, remote operations, and critical infrastructure such as traffic and utility networks. Policy support for open standards is increasing competition and innovation, while investment in automation and network security is enhancing solution capabilities. Strong enforcement of SLA standards is building trust in carrier grade performance, which is sustaining long term procurement and global partnerships.

Europe Carrier Ethernet Access Devices Market Trends

Europe represents a mature market for carrier Ethernet access devices, supported by consistent demand from telecom operators, enterprises, and public agencies. Strict regulatory frameworks such as the General Data Protection Regulation (GDPR) are driving adoption of secure and compliant networking solutions. Organizations are deploying CEADs to protect data flows and ensure reliable connectivity across distributed operations. Ongoing fiber upgrades and broadband expansion are reinforcing demand, while strong compliance standards are sustaining procurement of carrier grade equipment.

Infrastructure modernization and sustainability priorities are shaping market evolution across the region. CEADs are enabling interoperable cross border networks, while vendors are developing energy efficient devices to align with green data center initiatives. Policymakers are promoting circular economy practices, which is encouraging recyclable hardware and optimized software design. Enterprises are adopting solutions that support carbon reduction targets and long term efficiency. This focus on security, sustainability, and performance is supporting stable growth and strengthening Europe’s position in advanced networking infrastructure.

Asia Pacific Carrier Ethernet Access Devices Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for carrier Ethernet access devices between 2026 and 2033, driven by large-scale digital transformation in countries China and India. Governments are investing in nationwide digital infrastructure, while rapid internet penetration is expanding connectivity across urban and rural areas. Telecom operators are deploying fiber networks to support high-speed services, and local manufacturers are scaling production to meet rising demand. Enterprises are integrating CEADs into telecom backhaul and enterprise networks, which is strengthening adoption across diverse economies.

5G rollout and IoT expansion are accelerating network upgrades across industrial and urban environments. CEADs are enabling low-latency data exchange in smart factories, logistics systems, and large cities, which is supporting advanced use cases. Policymakers are encouraging local manufacturing, while enterprises are adopting hybrid models that combine private 5G with cloud platforms. Suppliers are developing cost-efficient solutions for large-scale deployment, and regional capabilities are supporting global exports. This ecosystem is broadening end-user segments and is positioning Asia Pacific as a key driver of long-term market growth.

Competitive Landscape

The global carrier Ethernet access devices market structure is moderately consolidated, with leading players such as Cisco Systems, Juniper Networks, ADTRAN, Calix, and Huawei Technologies accounting for about 35 to 40% share. These firms are competing through advanced product portfolios, strong brand positioning, and continuous innovation to address evolving telecom and enterprise requirements.

Market dynamics are intensifying as emerging players introduce cost-efficient solutions and target price-sensitive segments. This pressure is accelerating product development cycles among established vendors, with increased focus on SDN integration and edge automation. Strategic partnerships are expanding geographic reach and enhancing service capabilities, which is enabling vendors to capture opportunities across both telecom and enterprise domains.

Key Industry Developments

- In January 2026, Mplify revamped its Carrier Ethernet certification program by rebranding MEF 3.0 into “Carrier Ethernet for Business” and introducing a new “Carrier Ethernet for AI” track to address evolving enterprise and AI-driven networking needs. The updated framework includes ongoing maintenance and optional retesting to keep certifications current, ensuring continued relevance, interoperability, and validated performance.

- In November 2025, Ekinops was selected by Denmark's leading telecom provider TDC Net to upgrade its Carrier Ethernet Customer Services using the company's latest MEF 3.0-certified EADs, models 1647 and 1651, which support up to 10 Gbps speeds with advanced traffic management, QoS, and OAM features.

- In November 2025, Arqit Quantum launched the SKA Central Controller (SKA-CC), a software platform designed to streamline quantum-safe network deployments for managed service providers across telecom, cloud, and AI environments. It enables secure Network-as-a-Service (NaaS) with multi-tenant VPN controls, quantum-safe encryption for OSI Layers 1-7, mobile VPNs, Private 5G, and IoT/OT security, using lightweight agents for dynamic key generation and Zero Trust access.

Companies Covered in Carrier Ethernet Access Devices Market

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- ADTRAN Holdings, Inc.

- Calix, Inc.

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Nokia Corporation

- Ericsson AB

- NETGEAR, Inc.

- RAD Data Communications

- CIENA Corporation

- Lumentum Operations LLC

- FiberHome Telecommunication Technologies

- Ribbon Communications Inc.

Frequently Asked Questions

The global carrier Ethernet access devices market is projected to reach US$ 18.6 billion in 2026.

The market is driven by 5G deployments and cloud expansion, which demand high-capacity Ethernet backhaul, and massive digital infrastructure investments that boost carrier-grade access equipment adoption.

The market is poised to witness a CAGR of 2.5% from 2026 to 2033.

Major opportunities lie in industrial OT-IT convergence that is generating rugged TSN device needs, and growth in smart cities and IoT are expanding Ethernet into new urban applications.

Cisco Systems, Juniper Networks, ADTRAN, Calix, and Huawei Technologies are some of the key players in the market.