- Pharmaceuticals

- Acute Migraine Treatment Market

Acute Migraine Treatment Market Size, Share, and Growth Forecast, 2026-2033

Acute Migraine Treatment Market by Drug Class (Triptans, CGRP Antagonists, Ditans, Ergot Alkaloids, Analgesics), Route of Administration (Oral, Nasal, Injectable, Intravenous), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis for 2026-2033

Acute Migraine Treatment Market Share and Trends Analysis

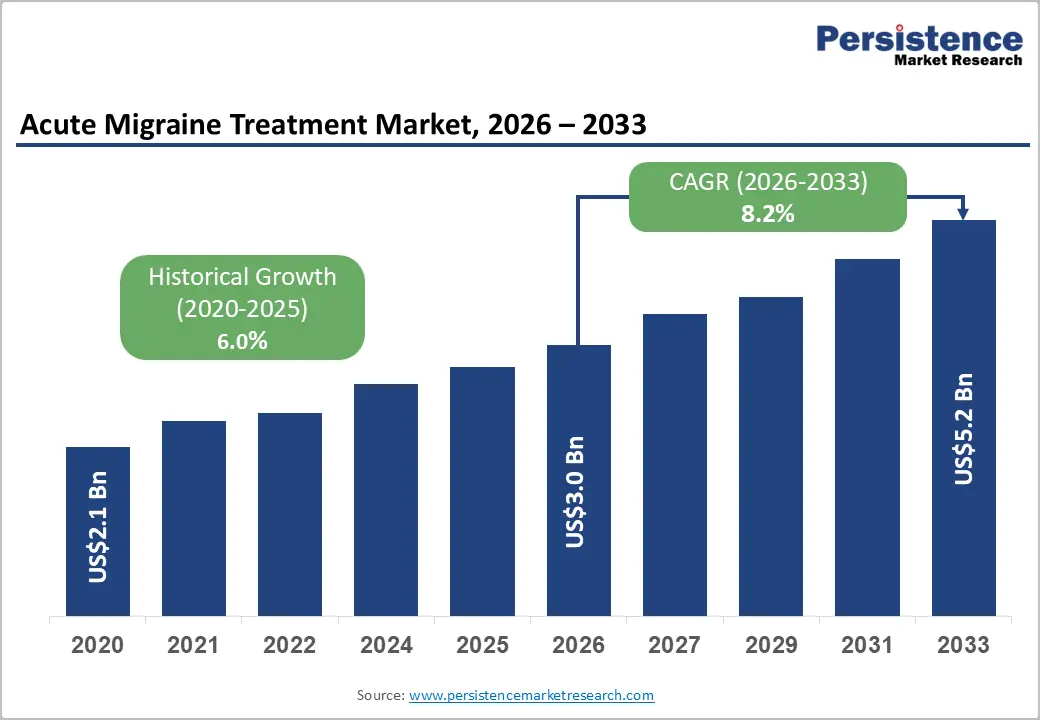

The global acute migraine treatment market size is likely to be valued at US$ 3.0 billion in 2026, and is projected to reach US$ 5.2 billion by 2033, growing at a CAGR of 8.2% during the forecast period 2026–2033.

Market growth is driven by the rising global prevalence of migraine disorders, expansion of CGRP-targeted therapies, and increased healthcare access through digital pharmacy platforms. According to the World Health Organization (WHO) and the Global Burden of Disease Study, migraine ranks among the leading causes of disability worldwide, affecting more than 1 billion people globally. In parallel, pharmaceutical innovation and broader insurance coverage for migraine medications are accelerating adoption of newer drug classes such as calcitonin gene-related peptide (CGRP) receptor antagonists and ditans, which offer improved efficacy and tolerability compared with legacy therapies.

Key Industry Highlights

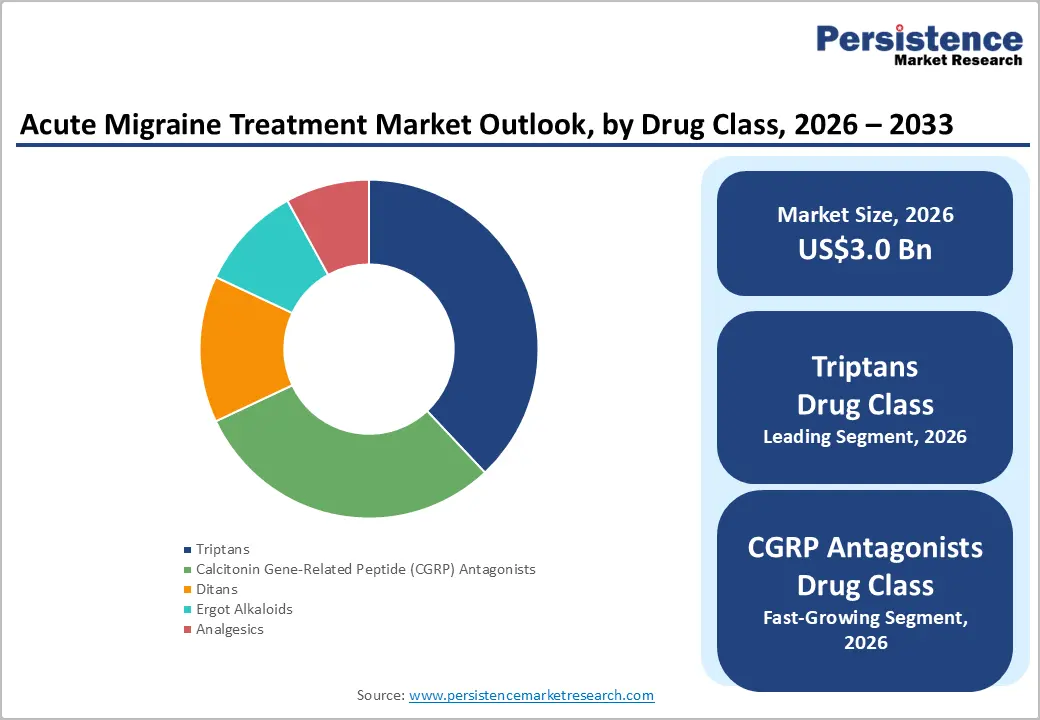

- Dominant Drug Class: Triptans are likely to capture about 38% revenue share in 2026, while CGRP antagonists are set to grow the fastest at 10.1% CAGR through 2033, supported by targeted migraine mechanisms.

- Leading Route of Administration: Oral medications are expected to lead with an estimated 56% share in 2026, while injectables are projected to be the fastest-growing at 9.4% CAGR during 2026–2033, reflecting a high demand for rapid relief and biologic migraine treatments.

- Dominant Distribution Channel: Retail pharmacies are anticipated to dominate with about 53% revenue share in 2026, while online pharmacies are likely to represent the fastest-growing channel at 10.3% CAGR through 2033, driven by telemedicine expansion.

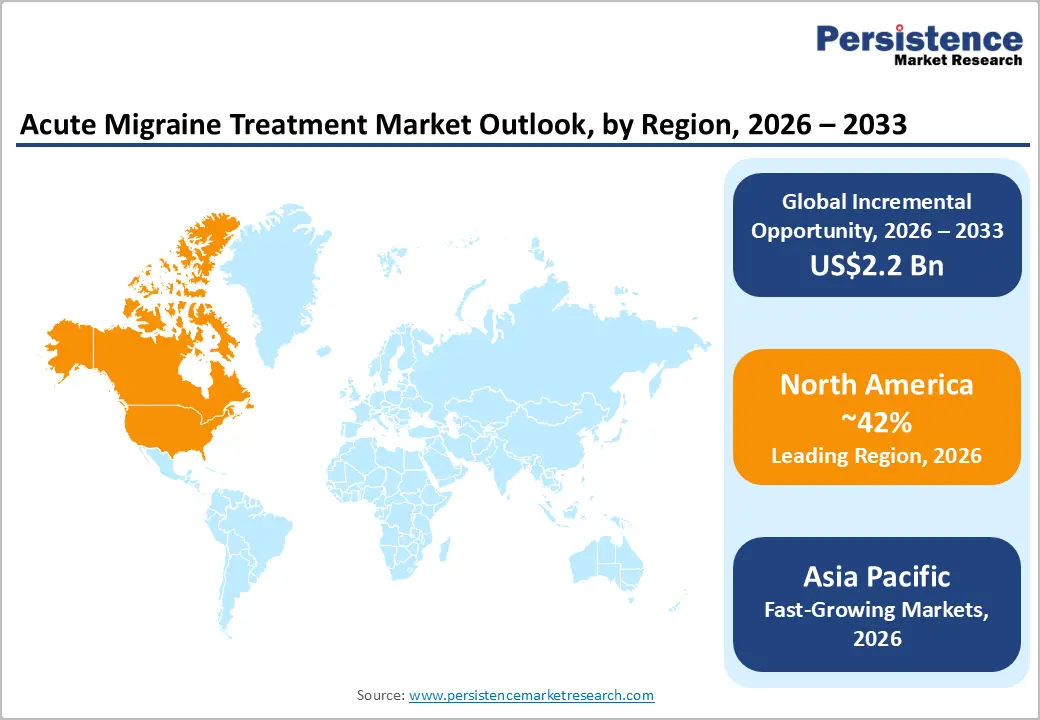

- Regional Leadership: North America is poised to lead with an estimated 42% share in 2026, while Asia Pacific is expected to register the fastest growth at 9.3% CAGR through 2033, supported by expanding healthcare access in China, India, and Southeast Asia.

- May 2025: The U.S. Food and Drug Administration (FDA) approved Satsuma’s STS101, a nasal powder formulation of dihydroergotamine, offering a fast-acting, non-oral treatment option for acute migraine.

| Key Insights | Details |

|---|---|

| Acute Migraine Treatment Market Size (2026E) | US$ 3.0 Bn |

| Market Value Forecast (2033F) | US$ 5.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Global Prevalence of Migraine Disorders

The increasing burden of migraine is a primary factor driving demand in the acute migraine treatment market. According to the WHO and the Institute for Health Metrics and Evaluation (IHME), migraine affects approximately 14–15% of the global population, making it one of the most prevalent neurological conditions worldwide. The Global Burden of Disease Study consistently ranks migraine among the top causes of years lived with disability (YLDs) in individuals aged 15–49. This high disease burden continues to elevate the clinical and economic importance of effective migraine management across global healthcare systems.

Higher diagnosis rates and improved neurological awareness are translating into greater demand for acute migraine medications, including triptans, CGRP antagonists, and ditans. The expansion of neurology clinics, specialized headache centers, and telemedicine consultations is enabling earlier diagnosis and treatment initiation. In parallel, public health campaigns and improved patient education are encouraging individuals to seek timely medical care. As healthcare providers emphasize patient-centered management of neurological disorders, pharmaceutical manufacturers are witnessing sustained growth in prescription volumes across both developed and emerging markets.

Innovation in CGRP-Targeted Therapies and Expanding Treatment Accessibility

Technological advancement in CGRP inhibitors has transformed the migraine therapeutics market, providing new treatment options for patients who do not respond well to traditional therapies. The U.S. FDA and the European Medicines Agency (EMA) have approved multiple CGRP-based therapies in recent years, reflecting a growing pipeline of targeted neurological drugs. These therapies act directly on the migraine signaling pathway, helping reduce neurogenic inflammation and vascular changes associated with migraine attacks.

Clinical trials reported in peer-reviewed journals such as The Lancet Neurology demonstrate that CGRP-targeted drugs can significantly reduce migraine attack severity and recurrence. At the same time, the rapid growth of online pharmacies and digital health platforms is improving patient access to migraine medications worldwide. Supported by the expansion of telemedicine services, digital pharmaceutical platforms allow patients to obtain prescriptions for acute migraine drugs through remote consultations.

In countries including the United States, India, and China, evolving regulatory frameworks supporting e-pharmacy services are strengthening distribution channels and improving medication adherence through convenient home delivery models.

High Cost of Novel Migraine Therapies

While innovative drugs have improved treatment outcomes, the high cost of CGRP antagonists and advanced migraine therapeutics remains a major barrier. Pharmaceutical cost analyses published by health technology assessment agencies indicate that CGRP-based therapies can cost several thousand dollars annually per patient in certain markets. For example, CGRP inhibitor therapies such as fremanezumab (Ajovy) require repeated injections and specialized biologic manufacturing, contributing to their premium pricing structure. These cost dynamics continue to influence payer negotiations and reimbursement decisions across several healthcare systems.

Such pricing structures limit accessibility, particularly in middle-income countries where reimbursement frameworks remain limited. Public healthcare systems frequently prioritize generic therapies such as triptans or analgesics, delaying adoption of premium treatments. In many healthcare markets, reimbursement approvals for novel migraine drugs can take several years after regulatory authorization. This cost barrier constrains market penetration and slows overall growth of advanced acute migraine drug therapies, particularly in regions where healthcare budgets remain tightly controlled and cost-effectiveness evaluations determine treatment availability.

Adverse Effects and Treatment Limitations

Some traditional acute migraine medications, particularly ergot alkaloids and triptans, may cause side effects including cardiovascular complications, nausea, and medication-overuse headaches. Clinical safety concerns highlighted by regulatory agencies such as the U.S. FDA and the EMA have resulted in stricter prescribing guidelines for certain patient groups. Regulatory safety labels for triptan-based drugs warn against their use in individuals with ischemic heart disease, stroke history, or uncontrolled hypertension, which requires physicians to carefully evaluate patient risk profiles before prescribing these therapies.

Regulatory oversight and post-market safety monitoring also continue to influence treatment adoption. In 2025, the U.S. FDA issued updated safety information for several migraine medications, emphasizing monitoring requirements for adverse reactions such as hypersensitivity and cardiovascular effects associated with certain drug classes, as reported by leading healthcare coverage and major clinical updates released by the FDA. Additionally, certain patient populations, including individuals with cardiovascular disease or high vascular risk, may not be suitable candidates for specific migraine drugs. These limitations create a clinical gap that can restrict broader adoption and influence prescribing decisions within the acute migraine treatment market.

Lucrative Opportunities Abound in Developing Healthcare Markets

Emerging economies represent a major growth opportunity for the acute migraine treatment market. According to World Bank healthcare expenditure data, healthcare spending in Asia-Pacific and Latin America has been growing at rates exceeding global averages. Rapid urbanization, expanding middle-class populations, and rising healthcare awareness are strengthening demand for neurological treatments across these regions. As healthcare infrastructure improves, more patients are gaining access to specialized medical services for migraine diagnosis and treatment, creating favorable conditions for pharmaceutical companies expanding into developing healthcare systems.

Countries such as India, China, Indonesia, and Brazil are witnessing rising neurological disease awareness alongside expanding pharmaceutical distribution networks. Government initiatives aimed at strengthening public healthcare systems and expanding insurance coverage are enabling more patients to access migraine treatment medications. These opportunities are further reinforced by global regulatory developments supporting easier treatment access. For example, the U.S. FDA approved Brekiya, a self-administered auto-injector therapy for acute migraine treatment in 2025, enabling patients to administer the medication at home rather than in hospital settings. Such simplified delivery technologies demonstrate how future migraine therapies can improve accessibility in regions where hospital infrastructure and specialist availability remain limited.

Advancement of Personalized Therapies and Digital Migraine Care

Advances in precision medicine and neurological biomarkers are opening new avenues for personalized migraine treatment strategies. Research initiatives supported by organizations such as the National Institutes of Health (NIH) and the European Brain Council are exploring genetic and molecular markers that influence migraine susceptibility. These studies are improving scientific understanding of migraine pathways and enabling the development of targeted therapies tailored to individual patient profiles. Personalized treatment strategies have the potential to significantly improve therapeutic outcomes and reduce the trial-and-error approach often associated with migraine management.

The integration of digital therapeutics, wearable technologies, and remote monitoring tools further expands this opportunity. In April 2025, the U.S. FDA granted marketing authorization to CT-132, the first prescription digital therapeutic designed to prevent episodic migraine, allowing the smartphone-based therapy to be used alongside traditional drug treatments. Industry innovations are also accelerating in the wearable health ecosystem. In 2026, a partnership between wearable technology developers and digital therapeutic providers introduced migraine monitoring features that analyze biomarkers such as sleep quality, stress levels, and heart rate variability to identify migraine triggers in real time. These developments highlight the emerging convergence between pharmaceutical treatments, digital therapeutics, and biometric monitoring technologies, creating a more proactive and personalized ecosystem for migraine care.

Category-wise Analysis

Drug Class Insights

Triptans are estimated to hold around 38% of the acute migraine treatment market revenue share in 2026. These serotonin receptor agonists constrict cranial blood vessels and inhibit inflammatory signals, providing effective relief for many patients with acute migraines. Their long history of clinical use, broad physician familiarity, and extensive presence across retail and hospital pharmacies contribute to their ongoing dominance. Recent expansion in tablet based migraine treatments in 2025, particularly in the UK, where uptake of new acute migraine tablets has tripled within a year following national approval, underscores the sustained patient and physician preference for targeted oral options with rapid symptom relief.

CGRP antagonists are positioned as the fastest growing drug class, projected to expand at roughly 10.1% CAGR through 2033. These therapies act on the calcitonin gene related peptide pathway, a central component in migraine pathophysiology, and offer improved tolerability compared with some legacy treatments. Growth is being reinforced by broader clinical acceptance and regulatory support, including increased real world use following expert recommendations in 2025 emphasizing early adoption of CGRP targeted therapies in standard migraine care.

As more patients and clinicians recognize their benefits and as formulary coverage expands, CGRP antagonists are expected to capture a larger share of acute migraine prescriptions over the forecast period.

Route of Administration

Oral is likely to remain the dominant route of administration, with an estimated 56% of the acute migraine treatment market share in 2026, owing to its convenience, familiarity, and wide availability across outpatient settings. Most triptans, gepants, and several newer acute therapies are available as tablets or capsules, enabling patients to self manage migraine attacks without clinical intervention. The rapid increase in oral migraine prescriptions following broader approvals in 2025, including expanded use of oral gepants across primary care practices, demonstrates that physicians and patients continue to value simple, ingestible treatment forms that align with established care pathways.

In contrast, injectable therapies are projected to be the fastest growing route, with an approximate 9.4% CAGR from 2026 to 2033. Recent FDA approvals in 2025 for self administered migraine autoinjectors, such as the Brekiya dihydroergotamine autoinjector, illustrate how injectable delivery is evolving to meet patient needs for rapid onset and ease of use. These products simplify administration during acute episodes and extend injectable therapy beyond clinic settings to home use, enhancing patient autonomy.

Such technological advancements are expanding the role of injectable treatments in acute migraine care, particularly for severe or hard to treat attacks.

Regional Insights

North America Acute Migraine Treatment Market Trends

North America is anticipated to lead by capturing an estimated 42.5% of the acute migraine treatment market value in 2026 due to advanced healthcare infrastructure and high diagnosis rates for neurological disorders. The United States is the primary driver, supported by regulatory approvals from the U.S. FDA for novel acute migraine drugs, including combination therapies and rapid relief formulations. In April 2025, the FDA-approved Atzumi nasal powder (dihydroergotamine) for acute migraine relief, offering a non invasive, rapid acting treatment option that expands patient choices and supports broader adoption of advanced therapies.

In addition to regulatory support, strong insurance coverage and reimbursement frameworks through private health plans and public programs such as Medicare enhance patient access to prescription migraine treatments. Strategic clinical developments are also evident: in June 2025, AbbVie reported that its migraine drug Qulipta outperformed a commonly used generic in late stage trials, reinforcing industry confidence in innovative therapies and encouraging prescriber uptake. These factors, combined with intense R&D investment from pharmaceutical companies headquartered in North America, sustain the region’s leadership position in both revenue and therapeutic innovation within the acute migraine treatment landscape.

Europe Acute Migraine Treatment Market Trends

Europe represents a significant and mature market for acute migraine therapies, driven by well established healthcare systems and strong neurological disease awareness across Germany, the United Kingdom, France, and Spain. The EMA continues to play a central role in harmonizing drug approvals, enabling broad access to innovative acute migraine treatments across multiple European Union (EU) member states under unified regulatory standards. In 2025, the EMA’s safety recommendations and updated clinical guidance helped refine triptan prescribing practices, particularly considering safety profiles in vulnerable populations, which strengthened physician confidence in tailored migraine care.

Government reimbursement programs and national health services, such as the National Health Service (NHS) in the UK and statutory health insurance in Germany, support patient access to both traditional and newer migraine medications. National initiatives enhancing neurological care and awareness campaigns have further elevated diagnosis rates and treatment adoption. Germany’s commitment to expanding digital health tools for migraine management, including physician approved smart health apps reimbursed under national schemes, reflects a broader trend toward integrating digital support with therapeutic access. These systemic advances underscore Europe’s strategic relevance as a high value therapeutic market with strong prospects for sustained uptake of next generation acute migraine treatments.

Asia Pacific Acute Migraine Treatment Market Trends

Asia Pacific is projected to be the fastest growing regional market for acute migraine treatments, with an approximate CAGR of 9.1% through 2033, supported by expanding healthcare access, rapid urbanization, and rising neurological disease awareness. China and Japan are key contributors owing to their large patient populations and ongoing investments in healthcare modernization. Regulatory frameworks in Japan have continued to support timely approvals of newer migraine drugs, and improved clinical infrastructure is enabling broader utilization of advanced therapies. Under national bulk procurement programs, China has also begun promoting greater affordability of migraine medications.

Emerging markets such as India and ASEAN are experiencing robust growth as rising incomes and increasing health insurance penetration improve access to migraine care. Moreover, digital health expansion and telemedicine adoption have accelerated treatment delivery in remote areas. The combination of enhanced diagnostic services, growing retail pharmacy networks, and expanding specialty headache clinics is helping to close treatment gaps. China’s government initiatives to stimulate local pharmaceutical manufacturing and support specialty drug access reflect broader regional ambitions to strengthen neurological care ecosystems, positioning Asia Pacific as a critical growth engine for acute migraine therapies.

Competitive Landscape

The global acute migraine treatment market structure is moderately consolidated, dominated by the likes of Pfizer, AbbVie, Eli Lilly, Teva Pharmaceuticals, and Amgen. These pharmaceutical giants leverage strong physician networks, extensive neurological drug portfolios, and advanced R&D capabilities. Their focus spans triptans, CGRP antagonists, and emerging rapid-onset therapies, alongside patient-friendly delivery systems such as autoinjectors, nasal sprays, and combination formulations. Continuous investment in clinical trials and biotechnology partnerships supports innovation, strengthens market positioning, and enhances their ability to launch therapies efficiently in multiple regions.

Regional and specialty companies, including Biohaven Pharmaceuticals, Promius Pharma, and MediciNova, target niche segments such as refractory migraine, digital health integration, and emerging markets. High regulatory complexity, rigorous clinical trial requirements, and treatment cost barriers limit new entrants, while software-driven digital health solutions and telemedicine platforms are opening avenues for innovative drug-delivery models. Market consolidation is expected to gradually increase as global leaders acquire smaller players, expand geographically, and form strategic collaborations to accelerate adoption of next-generation migraine therapeutics and strengthen competitive advantage.

Key Industry Developments

- In March 2026, Akums Drugs & Pharmaceuticals launched the world’s first lasmiditan dispersible tablets, offering a faster, patient-friendly solution for acute migraine relief with improved ease of use during attacks. The formulation uses rapid disintegration technology to enhance absorption and compliance, addressing challenges such as nausea.

- In February 2026, Pfizer, in collaboration with the American Headache Society, began offering Quality Improvement grants to enhance migraine diagnosis, treatment, and early care pathways, with submission deadlines in 2026 for programs in the US, Canada, and Japan.

- In February 2025, Miist secured US$ 7 million to accelerate its rapid-acting inhaled migraine therapy (MST 02), aimed at delivering faster relief through innovative aerosol drug particle technology.

Companies Covered in Acute Migraine Treatment Market

- Pfizer Inc.

- AbbVie Inc.

- Eli Lilly and Company

- Amgen Inc.

- GlaxoSmithKline plc

- Novartis AG

- Teva Pharmaceutical Industries Ltd.

- AstraZeneca plc

- Bayer AG

- Johnson & Johnson

- Biohaven Ltd.

- Dr. Reddy’s Laboratories

- Sun Pharmaceutical Industries Ltd.

- H. Lundbeck A/S

Frequently Asked Questions

The global acute migraine treatment market is projected to reach US$ 3.0 billion in 2026.

Rising migraine prevalence and adoption of CGRP-targeted therapies are driving market growth.

The market is poised to witness a CAGR of 8.2% from 2026 to 2033.

Emerging healthcare markets and personalized migraine therapies provide significant growth potential.

Pfizer, AbbVie, Eli Lilly, Teva Pharmaceuticals, and Amgen are some of the key players leading the market.