- Pharmaceuticals

- Acute Spinal Cord Injury Market

Acute Spinal Cord Injury Market Analysis, Size, Trends, Growth and Forecast 2026-2033

Acute Spinal Cord Injury Market by Injury Type (Complete Spinal Cord Injury, Incomplete Spinal Cord Injury), Treatment Type (Corticosteroid therapy, Others), End-user (Hospitals and Clinics, Trauma Centers), and Regional Analysis 2026–2033

Acute Spinal Cord Injury Market Size and Trends Analysis

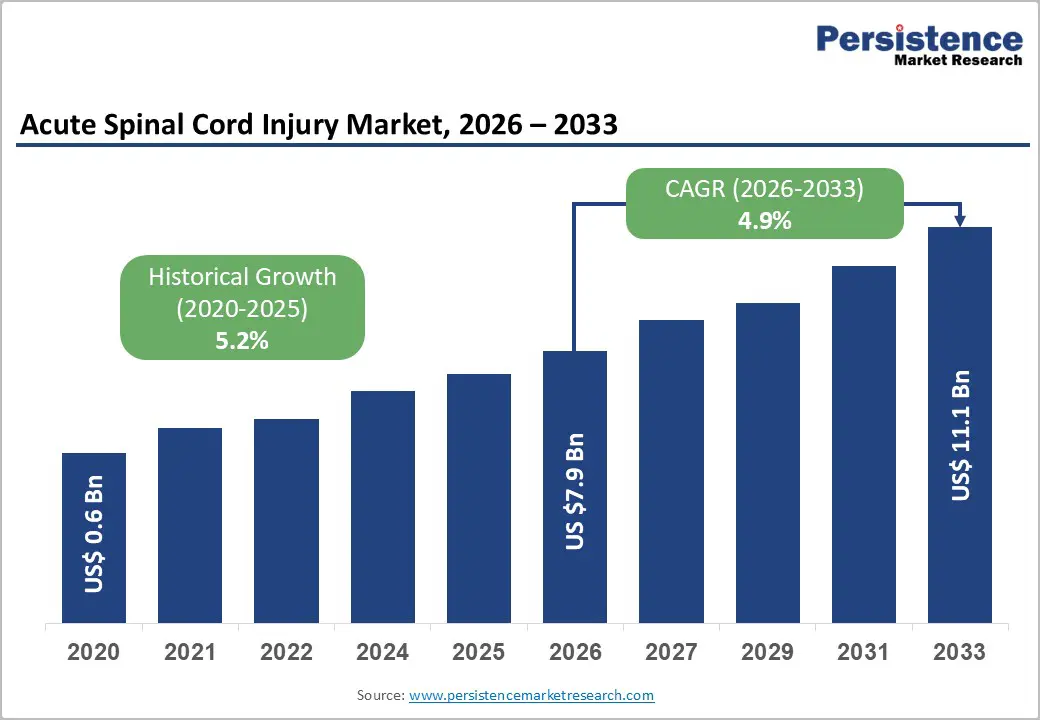

The global acute spinal cord injury market is likely to be valued at US$7.9 billion in 2026 and is expected to reach US$11.1 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by a rising global incidence of traumatic spinal cord injuries (tSCI) resulting from road traffic accidents and geriatric falls, alongside a shift toward neuro-regenerative therapies. The increasing clinical demand for specialized trauma care and neuroprotective pharmacologic agents remains the cornerstone of market expansion. The acute SCI therapeutic landscape is shifting from symptomatic management toward functional-recovery-focused interventions, positioning the market for sustainable growth over the forecast period.

Key Industry Highlight

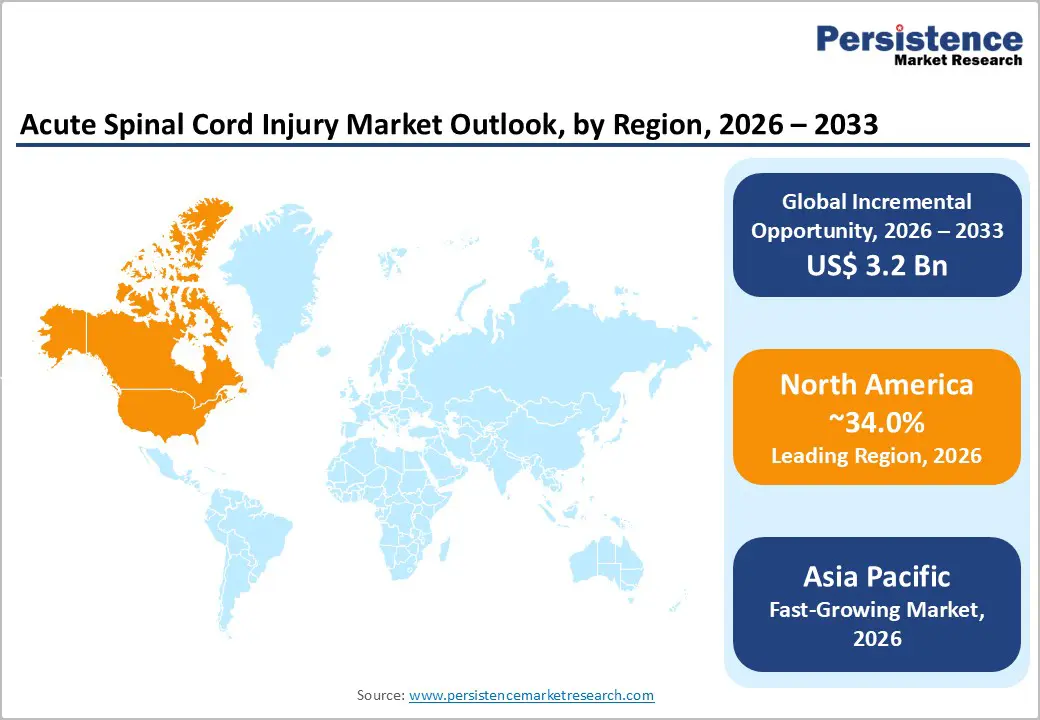

- Leading Market Region: North America is projected to lead the market, accounting for 34% in 2026, owing to advanced trauma care systems, strong clinical adoption of surgical interventions, and early integration of neuroregenerative and neuromodulation technologies across hospital networks.

- Fastest-growing Region: Asia-Pacific is projected to be the fastest-growing market, driven by rapid urbanization, rising road-traffic injuries, and expanding healthcare access in China, India, and ASEAN nations.

- Leading Treatment Type: Corticosteroid therapy is expected to account for approximately 49% of the market share in 2026, owing to its established role as a first-line intervention in acute spinal cord injury care.

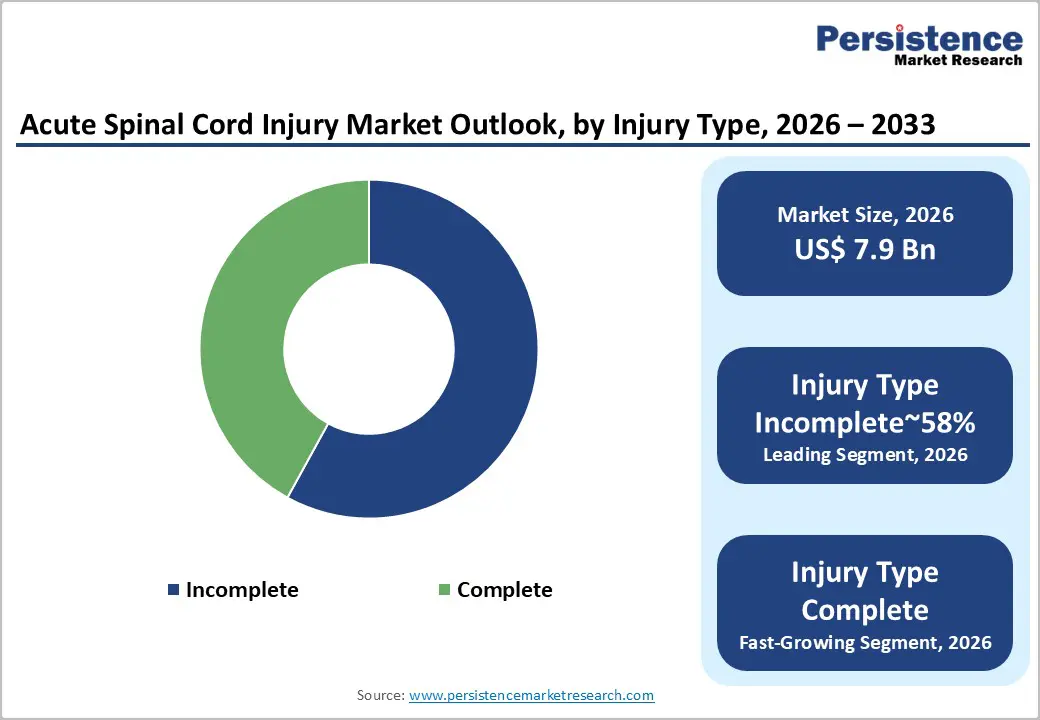

- Leading Injury Type: The incomplete spinal cord injury segment is expected to lead, with a 60% market share in 2026, owing to its higher prevalence and greater rehabilitation demand.

- Market Driver: The rising incidence of spinal cord injuries, combined with rapid technological advances in surgical techniques, robotic assistance, and neuroregenerative therapies, is driving sustained market expansion.

- Market Restraint: High treatment costs, limited availability of specialized trauma centres, and complex long-term rehabilitation requirements continue to constrain broader market penetration.

- Leading End-user: Hospitals and clinics are expected to account for 59% of the market in 2026, owing to their central role in acute spinal cord injury care.

- Key Opportunity: Advancements in neuro-regenerative agents, brain-computer interface technologies, and minimally invasive surgical solutions present significant opportunities to improve functional recovery outcomes.

- Key Industry Developments: Regulatory prioritization of neuro-regenerative drugs and neurotechnology platforms, along with increasing consolidation among major players and innovation from biotech firms, is reshaping the competitive landscape. The FDA granted Orphan Drug Designation to Kringle’s recombinant human HGF (hepatocyte growth factor) for acute spinal cord injury, a strategic milestone that provides seven years of market exclusivity and incentivizes global pharmaceutical partnerships for neuro-regenerative biologics.

| Global Market Attributes | Key Insights |

|---|---|

| Acute Spinal Cord Injury Market Size (2026E) | US$7.9 Bn |

| Market Value Forecast (2033F) | US$11.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements and Innovation in Treatment Modalities

Technological advancements are becoming a key transformative force in the acute spinal cord injury market, moving treatment goals from mere stabilization and compensation to a focus on achieving functional neurological recovery. Regulatory validation of advanced neuromodulation platforms has materially altered clinical expectations, reinforcing SCI as a modifiable condition rather than a permanently static outcome. Electrical stimulation systems are expanding therapeutic relevance beyond acute windows, while parallel progress in regenerative medicine is broadening the intervention landscape. These developments are reshaping capital-allocation priorities across diagnostics, intervention, and rehabilitation, thereby strengthening long-term demand visibility for technology-enabled SCI solutions.

Regulatory and clinical evidence substantiate this shift. The U.S. Food and Drug Administration approved ONWARD Medical’s ARC-EX external spinal cord stimulation system in late 2024, followed by home-use clearance in 2025, formally validating transcutaneous neuromodulation for functional improvement. Peer-reviewed regenerative research further supports stem cell–driven neural repair mechanisms, including axonal growth and vascular remodeling. Concurrent investment in gene therapy, brain-computer interfaces, and robotic rehabilitation platforms reinforces a multi-modality innovation cycle, structurally expanding addressable treatment pathways across the SCI care continuum.

Rising Motorization and Road Traffic Injuries in Emerging Economies

Rising motorization in emerging economies is expected to remain a primary structural driver of acute spinal cord injury incidence, as rapid urbanization and highway expansion continue to outpace parallel improvements in vehicle safety standards and trauma response systems. In middle-income markets, increased road density and higher traffic exposure are translating into elevated spinal trauma risk among younger, economically productive populations. This dynamic reinforces sustained demand for acute SCI interventions, particularly in regions where preventive infrastructure, enforcement mechanisms, and post-crash care coordination remain uneven, thereby making road traffic injuries a persistent demand driver.

Official surveillance and burden-of-disease evidence substantiate this demand driver. The Ministry of Road Transport and Highways, Government of India, reports a sharp year-on-year rise in road accidents in its latest annual assessment, underscoring deteriorating traffic risk dynamics. Complementary epidemiological data from the Global Burden of Disease study, published by the National Institutes of Health, identify India as a major contributor to global SCI incidence, with road injuries as the dominant causal factor. Together, these datasets validate road trauma as a traceable, structurally embedded growth catalyst for the acute SCI market.

Regenerative Medicine and Stem Cell Therapy Expansion

The regenerative medicine sector for acute spinal cord injury (SCI) is undergoing a paradigm shift as stem cell and gene therapies transition from experimental models to clinical realities. This "white-space" opportunity is being aggressively pursued by first-mover participants, as evidenced by the U.S. FDA’s June 2025 decision to grant Orphan Drug Designation to Kringle Pharma’s KP-100IT, a recombinant human hepatocyte growth factor designed to suppress secondary injury and promote axonal regeneration in acute-phase patients.

The integration of biomarkers and CRISPR-mediated engineering is facilitating a transition toward personalized SCI repair, attracting significant capital from biotechnology investors. A landmark industry highlight illustrating this technological convergence occurred in December 2024, when ONWARD Medical received FDA De Novo classification for its ARC-EX System, the world's first non-invasive spinal cord stimulation technology proven to restore hand strength and sensation, providing a critical neuro-rehabilitative framework for future regenerative biologics.

Category-wise Analysis

Injury Type Insights

The incomplete spinal cord injury segment is expected to remain the leading segment, accounting for an estimated 60% market share in 2026, supported by higher clinical prevalence and structurally greater rehabilitation demand. Partial neurological preservation increases eligibility for staged surgical intervention, prolonged pharmacologic management, and extended rehabilitation pathways, reinforcing sustained revenue intensity across acute and post-acute care settings. Advances in trauma response systems and diagnostic accuracy continue to reduce full cord transection, structurally shifting injury classification toward incomplete impairment and strengthening utilization density within specialized hospital infrastructure.

Complete spinal cord injury is likely to be the fastest-growing segment, driven by increasing clinical emphasis on regenerative and neuro-modulatory treatment strategies targeting severe neurological deficits. Elevated unmet therapeutic need, combined with expanding interventional scope and evolving care protocols, is expected to accelerate adoption within specialized treatment settings. Growth in this segment is structurally innovation-led rather than volume-driven, reflecting a strategic prioritization of recovery-oriented modalities over baseline incidence expansion.

Treatment Type Insights

Corticosteroid therapy is expected to remain the leading treatment type, accounting for approximately 49% of the treatment segment share in 2026, reflecting its entrenched position as a first-line intervention in acute spinal cord injury management. Its dominance is structurally supported by standardized clinical protocols, established anti-inflammatory and neuroprotective mechanisms, and broad acceptance of reimbursement across trauma care systems. Early administration within defined therapeutic windows remains integral to mitigating secondary injury cascades, embedding corticosteroids as baseline therapy within hospital and trauma center algorithms. While utilization patterns indicate maturity, the segment continues to provide revenue stability because of its universal applicability during the acute phase of injury management.

Surgical intervention is positioned as the fastest-growing treatment segment, driven by its direct role in addressing mechanical compression, spinal instability, and structural trauma sequelae. The ongoing adoption of minimally invasive techniques, robotic-assisted platforms, and advanced fixation systems is improving procedural precision while reducing operative morbidity. High per-procedure economic value reinforces hospital investment incentives, while integration with pharmacologic and rehabilitative pathways strengthens surgery’s strategic importance as a growth-oriented complement to established medical therapy within comprehensive acute care frameworks.

End-user Insights

Hospitals and clinics are expected to lead, accounting for a market share of 59% in 2026, due to their central role in acute spinal cord injury management. Segment dominance is structurally driven by concentration of advanced diagnostic imaging, surgical capability, intensive care infrastructure, and integrated rehabilitation services within hospital-based settings. High-volume trauma hospitals and specialized spinal units continue to anchor care delivery through standardized SCI protocols and multidisciplinary coordination, aligning with payer emphasis on outcome optimization and care centralization. This positioning sustains stable utilization flows and reinforces hospitals as the primary revenue-generating setting across the acute and early post-acute treatment continuum.

Trauma centers and specialty clinics are expected to be the fastest-growing end-user segment, reflecting a structural shift toward long-term management and rehabilitation in outpatient settings. Advances in remote monitoring, outpatient neurostimulation, and home-enabled rehabilitation technologies are expanding the clinical scope of non-hospital settings. As acute stabilization phases shorten, care pathways increasingly transition toward decentralized models, strengthening the strategic relevance of ambulatory platforms within comprehensive spinal cord injury management frameworks.

Region-wise Analysis

North America Acute Spinal Cord Injury Market Trends

North America is expected to remain the largest regional market, accounting for an estimated 34% of the global share in 2026, underpinned by advanced trauma care networks, high healthcare expenditure, and a robust regulatory framework. The U.S. drives regional leadership through FDA incentives such as Breakthrough Device and Orphan Drug programs, which are accelerating the adoption of novel interventions, including brain-computer interfaces and neurostimulation platforms. High SCI prevalence, coupled with concentrated investment in clinical trial infrastructure and patient registries, reinforces North America’s structural advantage in both early-stage innovation and high-value acute care delivery, supporting sustained revenue capture and technology integration across hospital and rehabilitation settings.

Regulatory milestones are materially shaping the market trajectory, exemplified by the December 2024 approval and the November 2025 home-use clearance of ONWARD Medical’s ARC-EX system, which establishes functional improvement as a validated treatment endpoint. Complementary development of fast-track and orphan-designated therapies, alongside a reimbursement landscape encompassing Medicare, private insurance, and veterans’ benefits, structurally enhances market access and adoption potential. Together, these factors position North America as the primary global hub for both commercialization and clinical validation of advanced SCI therapeutics, combining policy, infrastructure, and innovation to reinforce long-term regional dominance.

Europe Acute Spinal Cord Injury Market Trends

Europe is expected to remain the second-largest regional market, led by Germany, France, and the U.K., with growth structurally supported by harmonized regulatory oversight under the EU Medical Device Regulation (MDR). The regulatory framework enforces rigorous clinical evidence standards for spinal implants, enhancing safety and market credibility while shaping adoption patterns. Strongly socialized healthcare systems provide consistent reimbursement for long-term rehabilitation and neurotechnologies, thereby reinforcing structural demand stability across acute and chronic SCI care pathways.

Market expansion is further supported by the rising prevalence of degenerative spinal conditions, the growing adoption of non-fusion surgical procedures, and targeted investment in regenerative medicine through the EU Horizon and national research initiatives. Organizational infrastructure, such as the European Spinal Cord Injury Federation, facilitates research coordination, protocol standardization, and the dissemination of clinical best practices, thereby enabling the adoption of advanced diagnostics and therapeutics. Government-led spine care improvement programs complement these trends, structurally enhancing both technology uptake and patient access across diverse healthcare systems in Europe.

Asia Pacific Acute Spinal Cord Injury Market Trends

Asia Pacific is expected to remain the fastest-growing regional market, driven by rapid urbanization, rising road traffic injuries, and expanding healthcare access across China, India, and ASEAN nations. China’s manufacturing capabilities enable cost-effective spinal implants, broadening surgical accessibility, while Japan’s regulatory approval of STEMIRAC positions the country as a leader in stem cell-based neuroregenerative therapies. These structural factors collectively accelerate the adoption of both surgical and regenerative interventions across the region.

Growth is further reinforced by manufacturing cost advantages that enable sustainable pricing of therapeutic devices and regenerative products, supporting regional production and global supply chain integration. Government-led healthcare initiatives, investments in specialized neurological care, and venture capital influx into life sciences sectors enhance market development. Emerging opportunities in ASEAN healthcare infrastructure, rising SCI prevalence, and technology-enabled care pathways are expected to sustain medium-term expansion, establishing the Asia Pacific as a strategic growth and innovation hub within the global acute SCI market.

Competitive Landscape

The acute spinal cord injury market reflects a fragmented to moderately consolidated competitive landscape, shaped by both global incumbents and innovation-driven specialists. Established medical device leaders such as Medtronic, Stryker, and Zimmer Biomet anchor the market through surgical solutions and strong hospital penetration, while pharmaceutical players such as Novartis and Pfizer participate via targeted drug development and acquisitions. Alongside them, specialized biotechnology firms including ONWARD Medical, NervGen Pharma, and Kringle Pharma are reshaping competition through regenerative and neurotechnology-focused therapies. Companies increasingly prioritize functional recovery over symptomatic management, driving venture investment and innovation-led competition.

Key Industry Developments

- In June 2025, NervGen Pharma announced positive topline results from its Phase 1b/2a CONNECT SCI study, revealing that its lead candidate, NVG-291, produced statistically significant improvements in both motor and sensory function in patients with chronic spinal cord injury.

- In December 2024, ONWARD Medical received U.S. FDA De Novo classification for its ARC-EX System, marking it as the first and only technology approved to enhance hand strength and sensation in individuals with spinal cord injury.

- In January 2024, Neuralink successfully implanted its N1 device in a quadriplegic patient, allowing the user to control a computer cursor solely through thought.

Companies Covered in Acute Spinal Cord Injury Market

- Medtronic PLC

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Novartis AG

- ONWARD Medical

- Kringle Pharma Inc.

- NervGen Pharma Corp.

- Acorda Therapeutics

- Asterias Biotherapeutics

- BioArctic AB

- Pfizer Inc.

- ReNetX Bio

- InVivo Therapeutics

- Oxygen Biotherapeutics

- BioTime Inc.

Frequently Asked Questions

The global acute spinal cord injury market is likely to be valued at US$7.9 billion in 2026 and is projected to reach US$11.1 billion by 2033.

North America leads the acute spinal cord injury market, holding the largest share of approximately 34% in 2026.

The global acute spinal cord injury market is expected to grow at a CAGR of 4.9% between 2026 and 2033.

Key players include Medtronic, Stryker, Zimmer Biomet, Kringle Pharma Inc., NervGen Pharma Corp., and Acorda Therapeutics.

Advancements in neuro-regenerative agents, brain-computer interface technologies, and minimally invasive surgical solutions present significant opportunities to improve functional recovery outcomes.