- Pharmaceuticals

- Acute Kidney Injury Treatment Market

Acute Kidney Injury Treatment Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Acute Kidney Injury Treatment Market by Product (Dialysis and Drug Therapy), Injury (Pre-renal Injury, Intrinsic Renal Injury, and Post-renal Injury), End-user (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 - 2033

Acute Kidney Injury Treatment Market Share and Trends Analysis

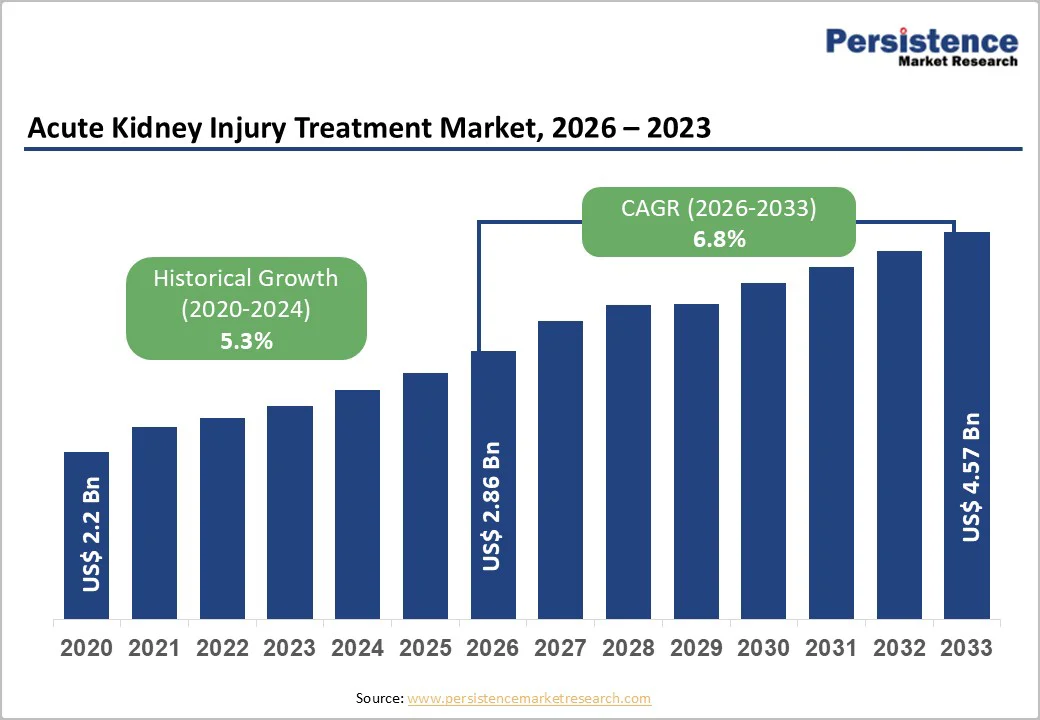

The global acute kidney injury treatment market size is estimated to grow from US$ 2.9 billion in 2026 to US$ 4.6 billion by 2033. The market is projected to record a CAGR of 6.8% from 2026 to 2033. Global demand for acute kidney injury (AKI) treatment continues to accelerate due to the rising prevalence of chronic comorbidities such as diabetes, hypertension, cardiovascular diseases, sepsis, and major surgical complications, which significantly increase AKI burden worldwide.

Increasing hospital and ICU admissions, higher exposure to nephrotoxic medications, and the need for renal replacement therapy (RRT) are fueling market demand. Advancements in CRRT systems, biomarker-based early diagnostics, portable dialysis devices, and kidney-protective drug therapeutics are enhancing clinical decision-making and patient recovery outcomes. Additionally, growing investments in critical-care infrastructure, improved reimbursement policies, and increasing clinical research and trials in AKI therapeutics are further strengthening global market expansion.

Key Industry Highlights:

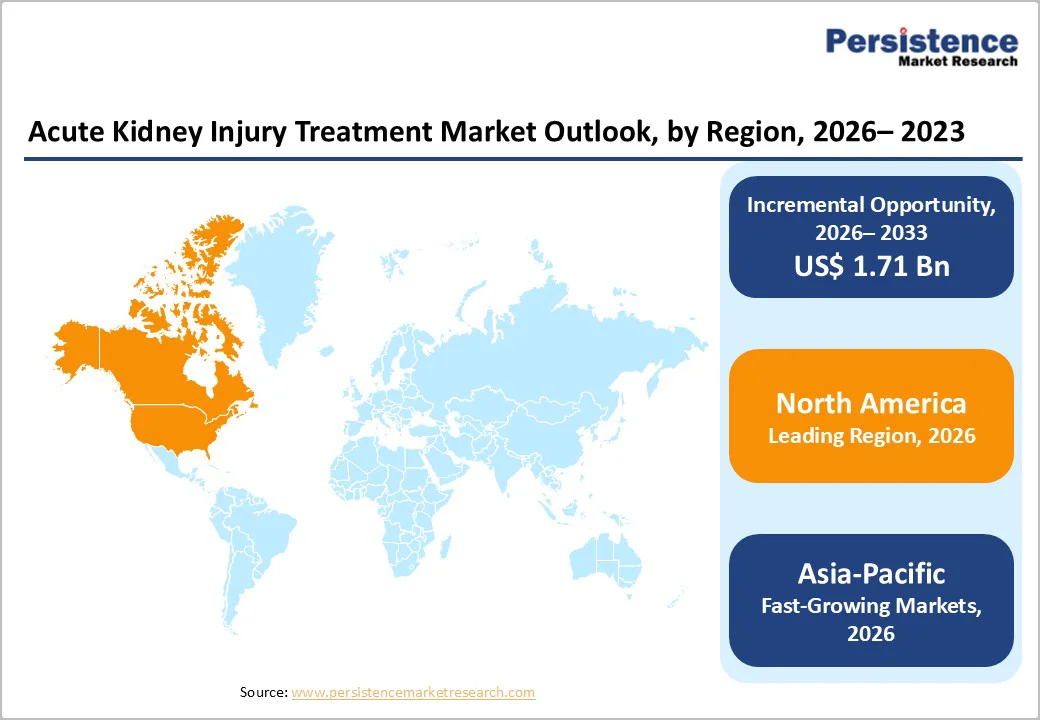

- Leading Region: North America dominates the global acute kidney injury treatment market, accounting for 47.8% of the market, driven by high AKI prevalence in ICU and hospitalized populations, advanced critical-care infrastructure, robust reimbursement frameworks, and rapid adoption of CRRT and biomarker-driven early-detection systems.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, supported by rising CKD and sepsis incidence, expanding ICU bed capacity, expanding access to CRRT and SLED technologies, rapid healthcare modernization, and growing clinician awareness of early AKI intervention.

- Leading Product Segment: Continuous renal replacement therapy (CRRT) leads the product category, owing to its clinical superiority in hemodynamically unstable ICU patients, its increasing use in sepsis-induced AKI, and its widespread adoption across tertiary care hospitals globally.

- Fastest-Growing Product Segment: Intermittent hemodialysis (IHD) is the fastest-growing segment, driven by its cost-effectiveness, wider availability in developing markets, improved device portability, and rising preference for flexible renal replacement scheduling.

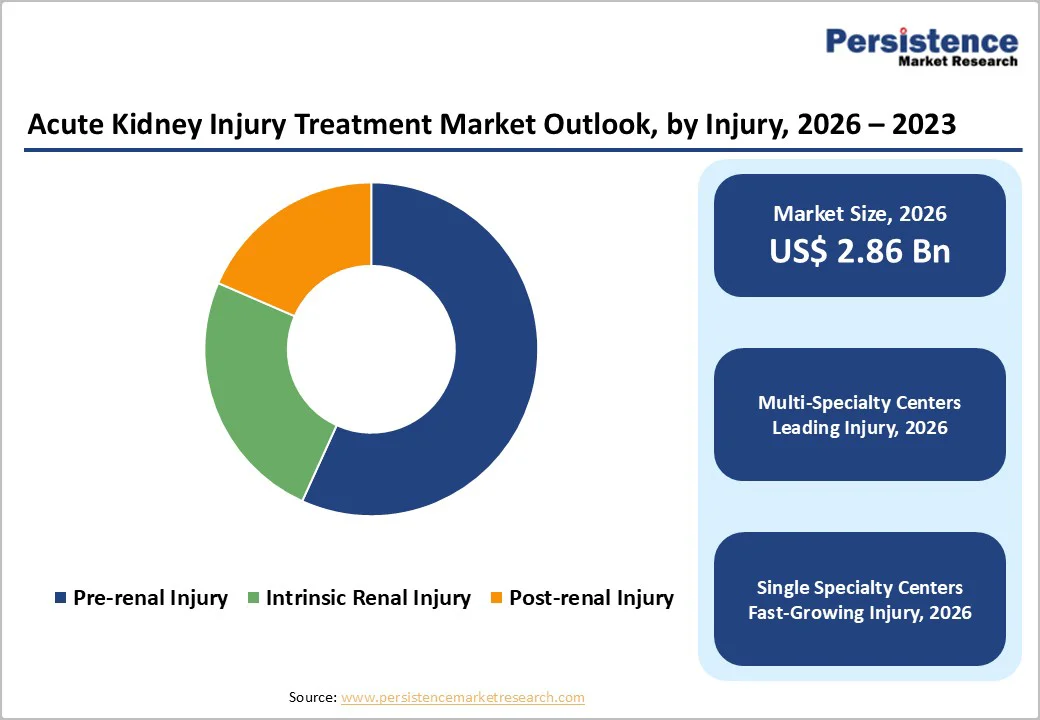

- Leading Injury Segment: Pre-renal injury dominates the injury segmentation, attributed to the high incidence of hypovolemia, sepsis, dehydration, and cardiac complications leading to reduced renal blood flow.

- Fastest-Growing Injury Segment: Intrinsic renal injury represents the fastest-growing category, driven by increasing drug-induced nephrotoxicity, ischemic tubular damage, and expanding research on targeted pharmacological therapies.

| Key Insights | Details |

|---|---|

|

Acute Kidney Injury Treatment Market Size (2026E) |

US$ 2.86 Bn |

|

Market Value Forecast (2033F) |

US$ 4.57 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.8% |

Market Dynamics

Driver - Growing Demand for Cost-Effective and Outpatient Surgical Interventions

Rising AKI incidence in hospital and critical-care settings is significantly escalating demand for early diagnostics, continuous renal replacement therapies (CRRT), and advanced monitoring technologies. Higher exposure to sepsis, major surgeries, nephrotoxic medications, and an ageing inpatient population with diabetes and hypertension has increased AKI occurrence and complexity. Post-COVID hospitalization patterns have further intensified renal complications, contributing to longer ICU stays and greater dependency on renal support systems. For instance, in 2024, a study published in BMC Pediatrics reported that AKI occurred in 20.19% of hospitalized neonates (128 of 634 cases) and demonstrated an incidence rate of 14.9 per 1,000 neonate-day observations, highlighting the rising burden of AKI in clinical settings.

Additionally, faster adoption of advanced diagnostics and kidney injury biomarkers is driving the acute kidney injury (AKI) treatment market. Traditional diagnostic methods based on serum creatinine and urine output often detect kidney damage only after substantial functional loss has occurred, leading to delayed therapeutic intervention and higher progression to severe AKI or dialysis dependence. The shift toward novel biomarkers such as NGAL, KIM-1, IL-18, TIMP-2, and IGFBP-7 is enabling clinicians to identify kidney stress and tubular injury much earlier, often within hours rather than days. This allows hospitals and ICUs to stratify patient risk, proactively tailor fluid and drug management, and reduce complications, mortality, and total ICU cost burden.

Restraints - High treatment cost and limited access to renal replacement therapies

The substantial financial burden associated with acute renal replacement therapies (including CRRT, SLED, and intermittent hemodialysis), specialized ICU infrastructure, and skilled clinical staffing significantly constrains adoption in many healthcare systems. High per-patient treatment costs, frequent consumables use, and maintenance service charges increase reimbursement pressure and payer resistance, especially when bundled or capitated payment models are enforced. As hospitals face rising economic strain, procurement decisions increasingly prioritize cost efficiency and delay upgrades or adoption of advanced CRRT systems, which is restraining overall market growth.

Moreover, accessibility disparities further intensify market barriers, with large gaps between urban tertiary facilities and rural or underserved regions where dialysis units, ICU-level capacity, and trained nephrology staff are limited. Many low- and middle-income countries still rely on limited intermittent hemodialysis availability, leading to delayed treatment initiation, increased mortality, and uneven market penetration for premium renal support devices and consumables. These structural inequalities restrain overall market scalability and restrict the adoption of advanced CRRT platforms despite the rising global AKI burden.

Opportunity - Technology-Driven Care Expansion and Decentralization of Acute Kidney Management

Telemedicine, AI-enabled risk assessment platforms, and remote monitoring solutions are emerging as powerful tools in AKI management, enabling clinicians to track high-risk inpatients and recently discharged individuals who remain vulnerable to renal deterioration. Continuous monitoring of vitals, fluid balance, nephrotoxic drug exposure, and early biomarker changes allows proactive intervention, reducing emergency admissions and ICU burden. Hospitals and integrated care networks increasingly adopt subscription-based digital platforms and analytics dashboards, generating recurring service revenue while lowering overall treatment costs and improving patient outcomes. Healthcare providers are prioritizing virtual kidney care programs supported by evidence of reduced readmission rates and improved care continuity, especially for sepsis, cardiac surgery, transplant, and critically ill populations.

Furthermore, rapid technological advances in portable dialysis systems, wearable blood-purification devices, and early-stage artificial kidney technologies are shifting AKI treatment beyond traditional ICU-centric models. By enabling treatment in ambulatory settings, step-down units, and even home environments, these next-generation systems reduce reliance on high-cost critical care infrastructure and expand patient access. Companies developing miniaturized CRRT platforms and biocompatible artificial kidney implants are attracting investment and regulatory momentum, creating new product categories with premium pricing and recurring consumables demand. This decentralization of renal support unlocks significant revenue opportunities for device developers, consumable suppliers, and digital management platforms, while improving patient quality of life and addressing accessibility gaps in regions with limited dialysis capacity.

Category-wise Analysis

By Product, Continuous Renal Replacement Therapy (CRRT) Dominates Globally Due to Superior Hemodynamic Stability and Widespread Adoption in Critical Care Settings

The continuous renal replacement therapy (CRRT) segment is projected to dominate the global acute kidney injury treatment market in 2026, accounting for 28.8% of revenue. The segment’s strong performance is primarily driven by the rising burden of severe and hemodynamically unstable AKI patients requiring continuous blood purification support, the growing installation base of advanced CRRT platforms in ICUs, and increasing preference for continuous modalities over intermittent hemodialysis due to better fluid balance control and improved hemodynamic stability. Additionally, increased adoption in critical care environments, expanded reimbursement coverage across high-income healthcare systems, and technological advancements that enable precision-based dosing, automated monitoring, and reduced nursing workload further drive the segment's growth.

By Injury, Pre-renal Injury Leads the Market Globally Due to the high prevalence of Hypovolemia, Sepsis, and Cardiovascular Complications

The pre-renal injury segment is projected to dominate the global acute kidney injury treatment market in 2026, accounting for a 56.8% revenue share. This is driven by the high prevalence of dehydration, sepsis, major surgical procedures, and cardiac-related complications that significantly reduce renal perfusion, making pre-renal AKI the most frequently encountered form in hospital and ICU settings. Increased hospitalization of elderly patients with comorbidities such as heart failure, diabetes, and hypertension further elevates the risk of renal hypoperfusion, thereby expanding treatment volumes. The segment also benefits from growing adoption of early diagnostics, fluid-management strategies, and rapid renal-replacement intervention protocols, thereby supporting sustained procedural demand and resource utilization across critical-care environments.

By End-user, Hospitals Dominate Globally Due to High Patient Inflow for Emergency Care and Advanced Dialysis Infrastructure

The hospitals segment is projected to dominate the global acute kidney injury treatment market in 2026, accounting for a revenue share 67.8%. This is driven by the high concentration of critically ill patients requiring intensive monitoring, rapid diagnostics, and advanced renal replacement therapies such as CRRT and SLED, which are predominantly delivered in hospital and ICU settings. Rising admissions for sepsis, cardiac surgery, trauma, and multi-organ failure significantly increase AKI incidence within tertiary care facilities, further strengthening hospital dependency on specialized equipment, blood purification systems, and biomarker-based testing. In addition, hospitals benefit from stronger reimbursement frameworks, better clinical infrastructure, and access to trained nephrology teams, enabling higher procedural throughput and faster adoption of technologically advanced devices and digital monitoring platforms. The growing shift toward integrated critical-care management and protocol-based AKI intervention reinforces the segment’s leadership position and drives sustained purchasing of consumables, service contracts, and renal support systems.

Region-wise Insights

North America Acute Kidney Injury Treatment Market Trends

The North America market is expected to dominate globally with a value share of 47.8% in the 2026, with the U.S. leading the region due to high AKI prevalence in hospitalized and ICU patient populations, advanced critical-care infrastrudue to high AKI prevalence in hospitalized and ICU patient populations, advanced critical-care infrastructure, and rapid adoption of innovative renal replacement modalities such as CRRT and portable dialysis systems. Strong reimbursement frameworks, increased healthcare spending per capita, and widespread integration of biomarker-based early diagnostics further drive growth in the market across regions. Additionally, the concentrated presence of key device manufacturers, ongoing clinical research in nephrology, and high clinician awareness of early AKI intervention accelerate technology uptake and procurement of advanced renal support systems. Growing investment in digital health platforms, tele-nephrology, and remote patient monitoring solutions is expanding access to timely AKI management and supporting recurring service revenues across hospital networks. The region continues to experience high procedure volumes across tertiary centers, strengthening revenue contribution from consumables, disposables, and service maintenance programs.

Europe Acute Kidney Injury Treatment Market Trends

Europe is expected to achieve steady growth, driven by the rising burden of chronic comorbidities such as diabetes, hypertension, and cardiovascular diseases, which significantly increase the risk of acute kidney injury in surgical and critical-care populations. Increasing implementation of standardized AKI management protocols supported by national health authorities, along with strong emphasis on early detection, staff training, and prevention programs across hospitals and ICUs, is further accelerating adoption of advanced diagnostics and renal replacement modalities.

For instance, according to the UK Kidney Association (2023), there were 681,127 AKI episodes among 586,734 patients, with 87% experiencing a single episode, 10% experiencing two episodes, and 3% experiencing more than two episodes, underscoring the growing clinical demand across European healthcare systems.

Increasing investments in critical-care infrastructure modernization, wider availability of CRRT and SLED technologies, and expanding reimbursement coverage for high-acuity renal therapies are also boosting the region growth in the market.

Asia Pacific Acute Kidney Injury Treatment Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 7.8% between 2026 and 2033, fueled by rapidly increasing hospitalization rates for sepsis, trauma, and major surgeries, alongside a growing prevalence of chronic kidney disease, diabetes, and hypertension that significantly elevate AKI risk across emerging healthcare systems. Expanding critical-care infrastructure, rising government investments in ICU capacity, and accelerated adoption of advanced renal replacement therapies, such as CRRT and SLED, across tertiary hospitals are strengthening clinical capabilities and treatment volumes. The region is also witnessing increased penetration of portable dialysis platforms and point-of-care diagnostics, driven by the need to improve treatment access for rural and underserved populations, where dialysis infrastructure remains limited. Favorable public health initiatives, rising awareness among clinicians regarding early AKI detection, and improving reimbursement availability in countries such as China, India, South Korea, and Japan are further propelling market growth.

Competitive Landscape

The global acute kidney injury treatment market is highly competitive, with major players such as Pfizer Inc., AstraZeneca, Novartis AG, Sanofi, and Fresenius Medical Care AG dominating through broad-based product portfolios, high-volume renal replacement therapy (RRT) operations, and extensive global distribution networks.

Market participants are focused on developing and deploying next-generation continuous renal replacement therapy (CRRT) systems, point-of-care AKI biomarker diagnostics, and wearable/portable kidney support devices. Strategic initiatives include mergers and acquisitions of renal-tech start-ups, partnerships with hospital nephrology / critical-care groups, expansion of acute-care and ambulatory renal therapy networks, and investments in digital kidney-monitoring platforms and connected infrastructure, thereby reinforcing competitive positioning on a global scale.

Key Industry Developments:

- In November 2025, researchers at the University of Utah Health (U of U Health) discovered that acute kidney injury (AKI) is triggered by fatty molecules called ceramides, which cause severe cellular damage by impairing kidney mitochondrial function. The team tested a backup drug candidate designed to modify ceramide metabolism, successfully preserving mitochondrial integrity and preventing AKI progression in preclinical mouse models, marking a promising pathway for future therapeutic development.

- In July 2025, Arch Biopartners initiated patient recruitment for its Phase II PONTIAK trial, evaluating cilastatin for the prevention of nephrotoxin-induced acute kidney injury (AKI). The company has manufactured and supplied the investigational drug for the study, which has commenced enrollment at primary clinical sites in Alberta, Canada.

- In June 2025, a study published in Nature Communications by the University of Edinburgh team, funded by Kidney Research UK, identified a newly emerging group of kidney cells that appear during CKD or following AKI, contributing to progressive loss of kidney function. The research also revealed two potential therapeutic targets that could prevent AKI from progressing to CKD and help preserve kidney function in affected patients. The findings highlight how proximal tubule cells transform after injury, releasing signals that accelerate kidney damage.

Companies Covered in Acute Kidney Injury Treatment Market

- Pfizer Inc.

- AstraZeneca

- Novartis AG

- Sanofi

- Fresenius Medical Care AG

- B. Braun SE

- Baxter

- Medtronic

- GE HealthCare

- Nipro Europe Group Companies

- CSL

- Others

Frequently Asked Questions

The global acute kidney injury treatment market is projected to be valued at US$ 2.86 Bn in 2026.

The rising incidence of AKI due to an aging population, increasing prevalence of diabetes, hypertension, sepsis, and surgical complications is driving the global acute kidney injury treatment market.

The global acute kidney injury treatment market is poised to witness a CAGR of 6.8% between 2026 and 2033.

Expansion of CRRT and automated dialysis technologies in emerging markets, along with rising investments in advanced biomarker-based AKI diagnostics are creating strong growth opportunities in the market.

Pfizer Inc., AstraZeneca, Novartis AG, Sanofi, and Fresenius Medical Care AG are some of the key players in the acute kidney injury treatment market.