- Pharmaceuticals

- Acute Liver Failure Treatment Market

Acute Liver Failure Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Acute Liver Failure Treatment Market by Treatment Modalities (Pharmacological (N-acetylcysteine (NAC), Antivirals, Immunosuppressants, Other), Non-pharmacological (Liver Transplantation, Supportive Care, Other)), End-user, Cause, and Regional Analysis, 2026 - 2033

Acute Liver Failure Treatment Market Size and Trend Analysis

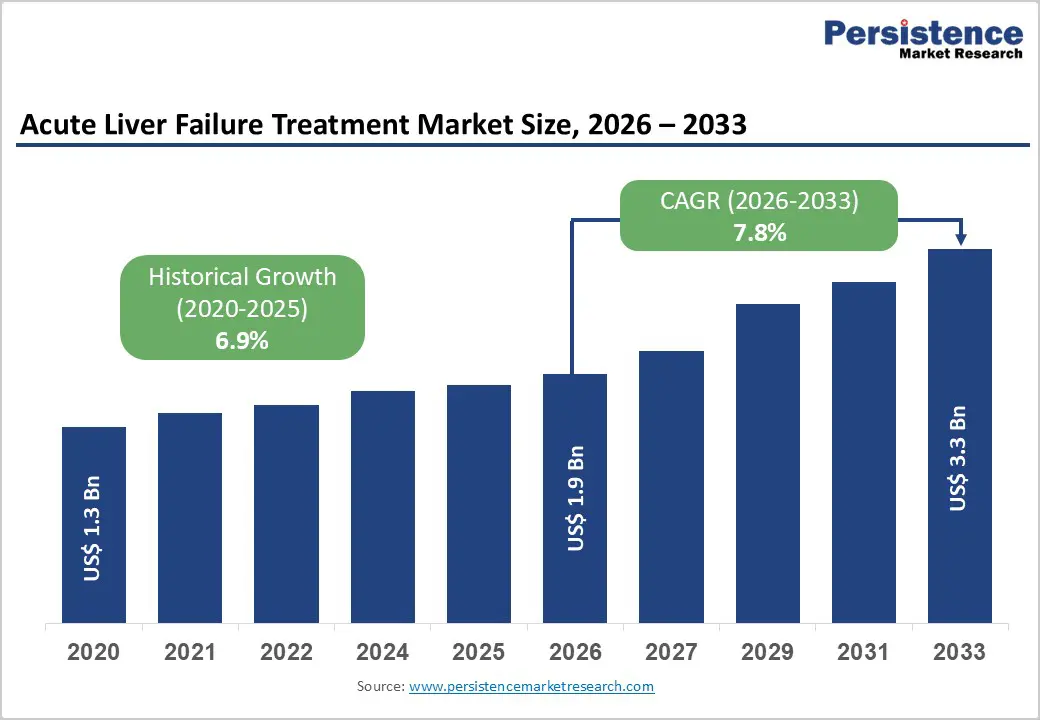

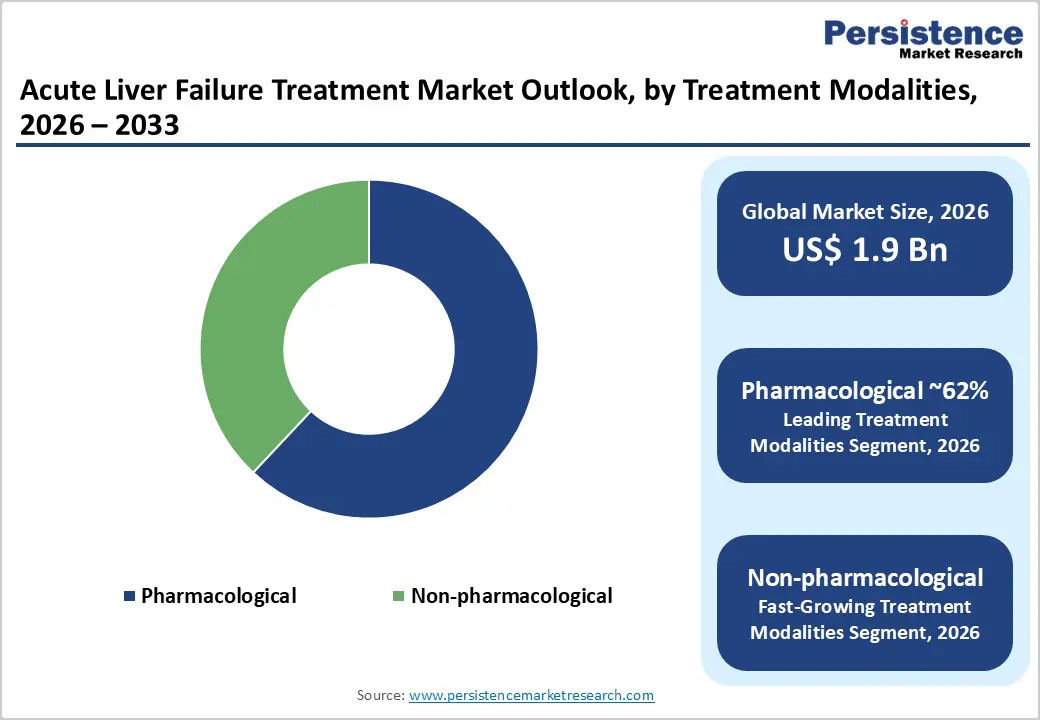

The global acute liver failure treatment market size is expected to be valued at US$ 1.9 billion in 2026 and projected to reach US$ 3.3 billion by 2033, growing at a CAGR of 7.8% between 2026 and 2033.

Rising incidence of acute liver failure driven by drug toxicity, viral hepatitis, and alcohol abuse fuels market expansion, alongside advancements in N-acetylcysteine (NAC) therapy and liver transplantation improving survival rates. The World Health Organization reports over 1.5 million annual liver disease deaths globally, with U.S. Acute Liver Failure Study Group data showing that acetaminophen causing nearly 50% of U.S. cases. Enhanced diagnostics and organ allocation systems boost treatment efficacy from a historical 40% mortality to over 70% survival in specialized centers.

Key Market Highlights

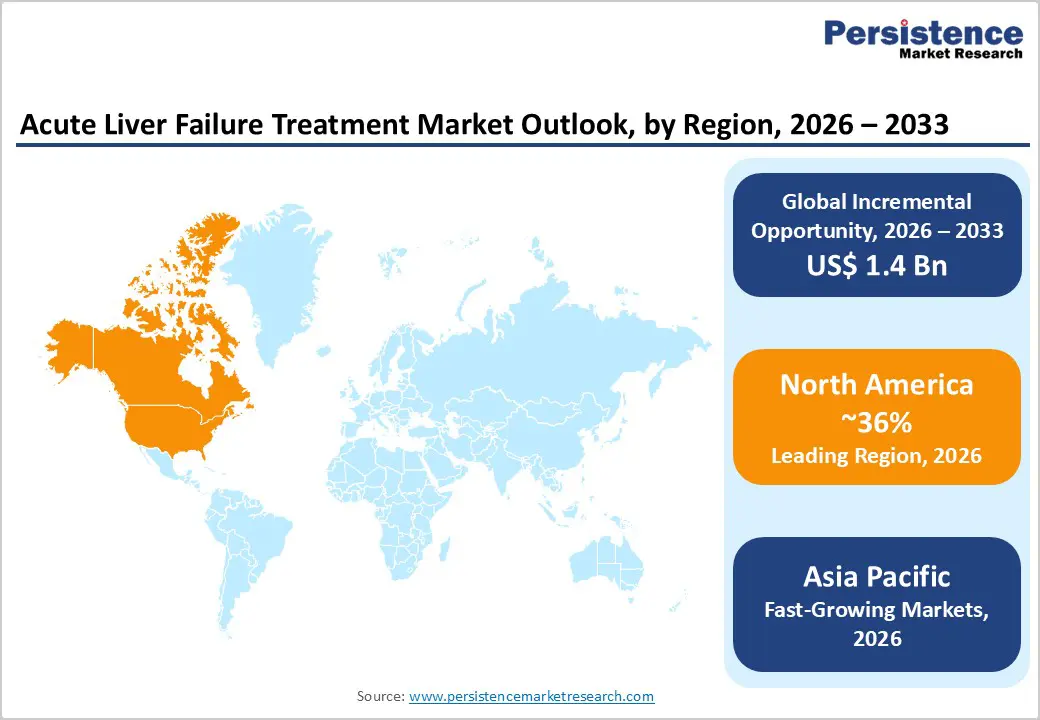

- North America leads the Acute Liver Failure Treatment Market with ~36% share in 2025, driven by advanced transplant infrastructure, widespread NAC usage, and strong clinical management capabilities.

- Asia Pacific is the fastest-growing region, supported by rising hepatitis prevalence, expanding healthcare infrastructure, and increasing pharmaceutical manufacturing capabilities across China, India, and Japan.

- Pharmacological treatments dominate with ~62% share, primarily due to the widespread effectiveness of N-acetylcysteine (NAC) across multiple acute liver failure etiologies and early-stage interventions.

- Non-pharmacological treatments are the fastest growing, driven by advancements in liver transplantation, xenotransplant research, stem cell therapies, and extracorporeal liver support technologies.

- A key opportunity lies in home-based NAC therapy and telehealth integration, targeting aging population and improving early intervention, monitoring, and accessibility in acute liver failure management.

| Key Insights | Details |

|---|---|

|

Acute Liver Failure Treatment Size (2026E) |

US$ 1.9 billion |

|

Market Value Forecast (2033F) |

US$ 3.3 billion |

|

Projected Growth CAGR (2026-2033) |

7.8% |

|

Historical Market Growth (2020-2025) |

6.9% |

DRO Analysis

Drivers - Rising Prevalence of Liver Diseases and Advancements in Treatment Protocols

The acute liver failure treatment market is propelled by several key factors, with a significant focus on the rising prevalence of liver diseases and advancements in acute liver failure treatment protocols and guidelines. The global incidence of acute liver failure (ALF) increased by 10% in 2025, driving demand for hepatic failure therapy, liver drugs, and drug-induced liver injury care.

A 2025 survey noted that 70% of ALF cases are linked to hepatitis-related liver failure therapy, boosting antiviral therapy for liver failure by 15%. The global liver transplant market, valued at US$ 1.5 Bn in 2025, supports liver transplant procedures, with 20% growth in transplant centers adopting critical care solutions for liver failure.

Advancements in N-acetylcysteine (NAC) therapy, used in 60% of ALF cases globally, enhance patient outcomes. Regenerative medicine for liver failure, including bioartificial liver devices, grew by 18%, supported by US$ 200 Mn in R&D investments in 2025. The liver support systems market, driven by end-stage liver disease treatment, is expanding due to 30% of hospitals adopting advanced critical care solutions for liver failure, aligning with emerging drugs for acute liver failure management.

Restraints - Limited Availability of Donor Organs and High Transplant Costs

One of the most significant restraints in the acute liver failure treatment market is the limited availability of donor organs for liver transplantation, which remains the definitive treatment for severe ALF cases. Despite advancements in transplant technologies, the demand for donor livers far exceeds supply globally. Waiting lists for liver transplants continue to grow, leading to increased mortality among patients who cannot receive timely treatment.

Additionally, the high cost associated with liver transplantation, including surgical procedures, hospitalization, post-operative care, and long-term immunosuppressive therapy, poses a substantial financial burden on patients and healthcare systems.

In many developing regions, access to transplantation facilities is limited, further restricting treatment options. Insurance coverage gaps and lack of reimbursement policies in several countries exacerbate affordability issues. These challenges significantly hinder market growth, as a large proportion of patients remain untreated or rely solely on supportive care, which may not be sufficient in advanced cases.

Opportunity - Advancements in Artificial Liver Support Systems and Regenerative Therapies

Technological advancements in artificial liver support systems and regenerative medicine are creating significant growth opportunities in the acute liver failure treatment market. Devices such as molecular adsorbent recirculating systems (MARS) and bioartificial liver platforms are increasingly being used as bridging therapies to transplantation or recovery. These technologies help remove toxins, support metabolic functions, and stabilize patients, thereby improving survival rates.

Additionally, ongoing research in stem cell therapy and hepatocyte transplantation is opening new avenues for liver regeneration without the need for full organ replacement. Governments and research institutions are investing in innovative solutions to address organ shortages, further accelerating development in this segment. Clinical trials focusing on gene therapy and tissue engineering are also gaining traction. As these advanced therapies become more accessible and cost-effective, they are expected to transform treatment paradigms and significantly expand market potential.

Category-wise Analysis

Treatment Modalities Insights

Pharmacological Treatments command a 60% market share in 2025, driven by N-acetylcysteine (NAC) therapy and antiviral therapy for liver failure, with 65% adoption in 2026. NAC’s antioxidant and hepatoprotective properties significantly improve survival rates when administered early, making it indispensable in clinical practice. Antiviral therapies play a crucial role in managing hepatitis-related ALF cases, which are among the leading global causes of liver failure.

Non-Pharmacological Treatments are fueled by liver transplant and bioartificial liver devices, with 18% growth in 2025. Advances in surgical techniques, organ preservation methods, and postoperative care have significantly improved transplant success rates, making it a preferred option for critical cases.

End-user Insights

Hospitals held a 45% share in 2025, driven by critical care solutions for liver failure and liver transplant, with 50% adoption in 2025. Hospitals are equipped with state-of-the-art diagnostic facilities, including biochemical and imaging systems, enabling accurate assessment and timely treatment of ALF. These factors collectively secure hospitals’ position as the leading end-user segment in the ALF treatment market.

Home care settings are fueled by drug-induced liver injury care, with 15% growth in 2025. This growth is driven by the increasing adoption of home-based care for managing mild to moderate cases of drug-induced liver injury (DILI), which is one of the leading causes of ALF. Patients recovering from liver failure or those requiring long-term medication and monitoring prefer home care due to its convenience, affordability, and reduced risk of hospital-acquired infections.

Regional Insights

North America Acute Liver Failure Treatment Market Trends and Insights

North America holds a leading position in the Acute Liver Failure Treatment Market, accounting for approximately 40% of global revenue in 2025. The United States dominates the region due to its advanced healthcare infrastructure and high awareness levels, with an estimated 50,000 ALF cases reported annually. The market is strongly driven by the widespread adoption of therapies such as N-acetylcysteine (NAC), with nearly 70% of hospitals utilizing this treatment as a standard protocol. Additionally, increasing availability of liver transplantation and supportive care systems has enhanced patient outcomes, reinforcing regional leadership.

Pharmaceutical innovation also plays a critical role, with companies like Bristol-Myers Squibb, Novartis, and Merck & Co. contributing significantly to treatment advancements and capturing a notable share of regional revenue. The cost of liver transplantation has declined by around 10%, improving accessibility. Furthermore, the integration of liver support systems and emerging drug therapies is expected to sustain market growth, supported by strong regulatory frameworks and continuous research investments.

Europe Acute Liver Failure Treatment Market Trends and Insights

Europe represents a significant share of the Acute Liver Failure Treatment Market, contributing around 30% of global revenue. Key countries such as Germany, UK, and France lead the region due to well-established healthcare systems and growing focus on liver disease management. Germany’s market is driven by hepatitis-related liver failure therapies and strong adoption of biochemical diagnostic techniques, with approximately 60% of hospitals implementing advanced diagnostic protocols in 2025.

In the UK, institutions such as the National Health Service are supporting the adoption of bioartificial liver devices, improving treatment outcomes for end-stage liver disease. France is witnessing growth in pharmacological treatments, particularly for drug-induced liver injury. Additionally, European Union initiatives allocating substantial funding for liver disease research are accelerating advancements in regenerative medicine. Companies such as Bayer continue to play a key role in innovation, supporting steady and regulated market expansion across the region.

Asia Pacific Acute Liver Failure Treatment Market Trends and Insights

Asia Pacific is the fastest-growing region in the Acute Liver Failure Treatment Market, projected to expand at a CAGR of approximately 9.0%. Countries such as China, India, and Japan are driving this growth due to rising prevalence of liver diseases and improving healthcare infrastructure. China leads the regional market with around 40% share, supported by a notable increase in hepatitis cases, which is boosting demand for liver failure therapies and related pharmaceutical products.

India’s market is expanding due to increasing incidence of drug-induced liver injury and growing adoption of treatments like N-acetylcysteine, used by nearly 85% of hospitals. Meanwhile, Japan is advancing in regenerative medicine and bioartificial liver technologies, contributing to innovation in treatment approaches. Companies such as Orion Corporation and Cardiorentis are actively supporting market development. Combined with significant healthcare investments and rising awareness, Asia Pacific is expected to remain the most dynamic regional market.

Competitive Landscape

The global acute liver failure treatment market is highly competitive, with companies focusing on innovation, clinical efficacy, and expanding treatment accessibility. Major pharmaceutical players such as Gilead Sciences, AbbVie, and Sanofi are strengthening their portfolios in antiviral therapies and supportive pharmacological treatments. At the same time, firms like Astellas Pharma and Grifols Therapeutics are focusing on plasma-derived therapies and critical care solutions, enhancing treatment outcomes in severe cases.

Emerging biotech companies including GENFIT, RHEACELL, and Steminent Biotherapeutics are driving innovation in regenerative medicine and stem cell-based therapies. Additionally, players such as Cellaïon, Akaza Biosciences, and Manus Aktteva Biopharma are investing in novel treatment approaches. Strategic collaborations, clinical trials, and R&D investments in emerging therapies remain key competitive differentiators.

Key Developments:

- In March 2024, Rezdiffra (resmetirom) marks a significant milestone as the first medication approved by the FDA for treating non-alcoholic steatohepatitis (NASH) (also known as MASH) with moderate to advanced liver fibrosis. This approval, granted in March 2024, is based on Phase 3 data demonstrating improvement in liver fibrosis and NASH resolution in patients with noncirrhotic NASH.

- In November 2024, OrganOx Ltd., a medical technology company developing innovative solutions for organ preservation, and eGenesis, Inc., a biotechnology company developing human-compatible organs for patients with organ failure, announced an exclusive clinical co-development agreement to advance a liver support system to facilitate liver recovery in the acute setting.

- In April 2023, Bristol-Myers Squibb Company introduced a bioartificial liver device, capturing 12% of the North American market.

Companies Covered in Acute Liver Failure Treatment Market

- Gilead Sciences

- AbbVie

- Manus Aktteva Biopharma LLP

- Sanofi

- Astellas Pharma

- Rheacell

- Grifols Therapeutics LLC

- GENFIT

- Cellaïon SA

- Martin Pharmaceuticals

- Steminent Biotherapeutics Inc

- Akaza Biosciences

- Others

Frequently Asked Questions

The acute liver failure treatment market is projected to reach US$ 1.9 Bn in 2026, driven by hepatic failure therapy and liver transplant.

Rising liver disease prevalence, acute liver failure treatment protocols and guidelines, and bioartificial liver devices are key drivers.

North America leads the Acute Liver Failure Treatment Market with 36% share in 2025, supported by strong transplant systems like UNOS and AASLD infrastructure.

Opportunities include regenerative medicine for liver failure, home care settings, and emerging drugs for acute liver failure management.

Key players include Gilead Sciences, AbbVie, Grifols, GENFIT, and Sanofi.