ID: PMRREP2815| 202 Pages | 25 Nov 2022 | Format: PDF, Excel, PPT* | Healthcare

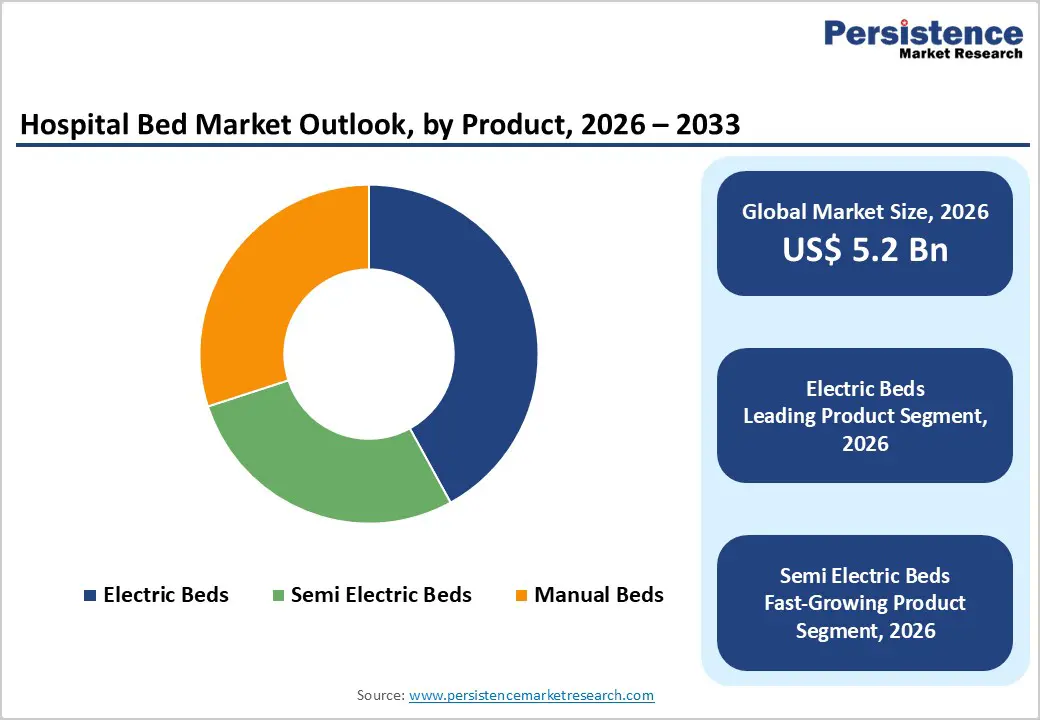

The global hospital bed market size is estimated to grow from US$ 5.2 Bn in 2026 to US$ 8.5 Bn by 2033. The market is projected to record a CAGR of 7.2% during the forecast period from 2026 to 2033.

Global demand for hospital beds is rising steadily, driven by increasing hospitalization rates, aging populations, and expanding healthcare infrastructure worldwide. The growing burden of chronic diseases, mobility impairments, and age-related conditions has significantly increased demand for acute care, long-term care, and specialized hospital beds. Rising surgical volumes, trauma cases, and critical care admissions are further accelerating bed utilization across hospitals and healthcare facilities. Expansion of public and private hospitals, specialty clinics, and long-term care centers, combined with higher healthcare spending and infrastructure modernization initiatives, is supporting market growth. Continuous innovation in electric and semi-electric beds, including automated positioning, pressure-injury prevention, and patient-safety features, is enhancing clinical efficiency and caregiver productivity. Additionally, increasing adoption of hospital-at-home models, post-acute care services, and home healthcare is expanding demand beyond traditional hospital settings. Growing emphasis on patient comfort, safety, and workflow optimization, along with the replacement of outdated bed infrastructure, continues to propel market expansion globally.

| Global Market Attributes | Key Insights |

|---|---|

| Hospital Bed Market Size (2026E) | US$ 5.2 Bn |

| Market Value Forecast (2033F) | US$ 8.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Driver – Expanding Healthcare Infrastructure, Rising Hospitalization Rates, and Technological Advancements Driving Hospital Bed Market Growth

The hospital bed market is witnessing sustained growth driven by the expansion of healthcare infrastructure, rising hospitalization rates, and increasing demand for advanced patient care solutions. Aging populations across developed and emerging economies are significantly increasing the prevalence of chronic diseases, mobility disorders, and age-related conditions that require prolonged hospitalization and long-term care. This demographic shift is directly translating into higher demand for acute, intensive, and long-term care beds. In parallel, growing surgical volumes, trauma cases, and emergency admissions are further strengthening bed utilization across hospitals.

Technological advancements are also playing a critical role in market expansion. Healthcare providers are increasingly adopting electric and smart hospital beds equipped with automated positioning, pressure injury prevention, fall detection, and patient monitoring capabilities to improve clinical outcomes and caregiver efficiency. Governments and private players are investing heavily in hospital construction, capacity expansion, and modernization initiatives, particularly in emerging markets. Additionally, the shift toward patient-centric care models is encouraging hospitals to replace conventional beds with ergonomically advanced designs that enhance comfort and safety. Together, rising healthcare demand, infrastructure investments, and technological upgrades are driving growth in the global hospital bed market.

Restraints – High Capital Costs, Budget Constraints, and Operational Challenges Limiting Market Expansion

The hospital bed market faces several restraints, including high cost structures and budget constraints within healthcare systems. Advanced electric and smart hospital beds require significant upfront capital investment, including costs for automation, electronic components, sensors, and integrated monitoring systems. These high procurement costs can be prohibitive for small hospitals, rural healthcare facilities, and public institutions operating under constrained budgets, particularly in developing regions. In addition to acquisition costs, the ongoing maintenance, repair, and replacement of technologically advanced beds increase the total cost of ownership. Hospitals must also invest in staff training to ensure proper usage and maintenance, further increasing operational expenses. Supply chain disruptions, raw material price volatility, and dependence on specialized components can impact manufacturing costs and delivery timelines.

Regulatory compliance and certification requirements for medical devices add another layer of complexity, often increasing time-to-market and development costs for manufacturers. Furthermore, limited reimbursement coverage for advanced hospital beds in certain regions restricts adoption, especially in non-critical care settings. These financial, operational, and regulatory challenges collectively slow market expansion despite growing clinical demand.

Opportunity – Growth in Home Healthcare, Long-term Care Expansion, and Smart Bed Integration, Creating New Market Opportunities

The hospital bed market presents substantial growth opportunities driven by the rapid expansion of home healthcare services and long-term care facilities worldwide. The shift toward decentralized care models, including hospital-at-home programs and post-acute home recovery, is increasing demand for electric and semi-electric beds designed for residential settings. Rising preference for home-based care among elderly patients and individuals with chronic conditions is creating new revenue streams beyond traditional hospital procurement. Long-term care facilities, nursing homes, and rehabilitation centers are also expanding rapidly due to aging populations and increasing life expectancy, particularly in North America, Europe, and Asia Pacific. These facilities require specialized beds with enhanced safety features, mobility support, and pressure management systems, driving demand for premium products.

Additionally, integration of digital health technologies into hospital beds represents a major opportunity. Smart beds with connectivity to hospital information systems, remote monitoring capabilities, and predictive analytics can significantly improve workflow efficiency and patient outcomes. Emerging markets offer further growth potential as governments increase healthcare spending and invest in hospital infrastructure upgrades. Together, expansion of alternative care settings, digital innovation, and geographic market penetration are expected to unlock significant long-term growth opportunities for hospital bed manufacturers globally.

By Product, Electric Beds Lead the Global Hospital Bed Market Due to Advanced Care Requirements

The electric beds segment is projected to dominate the global hospital bed market in 2026, accounting for 42.0% of revenue. Segment leadership is driven by the widespread adoption of electric beds across acute care hospitals, long-term care facilities, and home care settings, where patient comfort, caregiver efficiency, and clinical outcomes are critical. Electric beds offer features such as height adjustability, automated positioning, pressure redistribution, and integration with monitoring systems, which support infection control, fall prevention, and reduced caregiver strain. Their suitability for intensive care units, post-surgical recovery, and chronic disease management further strengthens demand. Continuous advancements in bed automation, smart sensors, and ergonomic design are improving safety, durability, and ease of use. Growing investments in modern healthcare infrastructure, particularly in developed markets, and rising preference for technologically advanced beds over manual alternatives continue to reinforce the dominance of electric beds globally.

By Application, Acute Care Leads the Market Driven by Advanced Drug Development and Therapeutic Innovation

The acute care segment is projected to dominate the global hospital bed market in 2026, accounting for a revenue share of 33.1%. This leadership is primarily driven by high patient admissions related to surgeries, trauma, emergency care, and critical illnesses that require short-term but intensive medical intervention. Acute care settings demand advanced hospital beds capable of supporting rapid patient repositioning, continuous monitoring, infection prevention, and compatibility with life-support equipment. The increasing prevalence of cardiovascular diseases, respiratory disorders, and complex surgical procedures is expanding acute care bed utilization across hospitals worldwide. Aging populations in developed economies and rising accident rates in developing regions are further increasing demand. Hospitals are increasingly upgrading legacy infrastructure with modern acute care beds to improve patient outcomes and operational efficiency. Additionally, rising healthcare expenditure and government initiatives to expand emergency and trauma care capacity continue to drive sustained growth in this segment.

By End User, Hospitals Lead Due to High R&D Intensity and Commercial Scale

The hospitals segment is projected to dominate the global hospital bed market in 2026, accounting for 53.6% of revenue. This dominance reflects the high concentration of inpatient admissions, intensive care units, surgical wards, and emergency departments within hospital settings. Hospitals require large volumes of beds across multiple departments, driving consistent demand for both new installations and replacement of aging equipment. Increasing focus on patient safety, infection control, and compliance with clinical standards is accelerating the adoption of advanced electric and specialty beds. Public and private hospital expansions, particularly in emerging economies, are also contributing to rising procurement volumes. Additionally, hospitals are early adopters of smart beds integrated with digital health systems to improve workflow efficiency and patient monitoring. Growing government funding, infrastructure modernization programs, and rising healthcare utilization rates continue to reinforce hospitals’ leadership in the global hospital bed market.

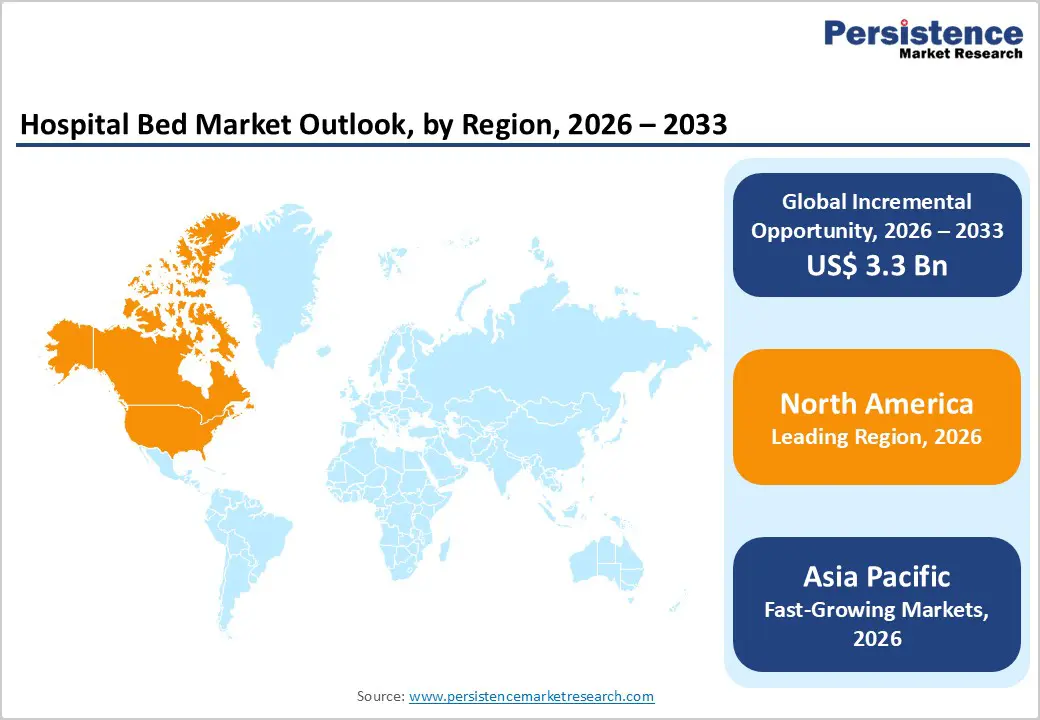

North America Hospital Bed Market Trends

The North American hospital bed market is expected to dominate globally with a value share of 47.8% in 2026, led primarily by the United States. Market leadership is supported by a well-established healthcare infrastructure, high hospital bed density, and strong capital spending by healthcare providers. Hospitals in the region consistently invest in technologically advanced electric and smart beds to improve patient safety, reduce caregiver workload, and comply with strict regulatory standards. High prevalence of chronic diseases, rising surgical volumes, and an aging population are driving sustained demand across acute and long-term care settings.

The region also benefits from frequent replacement cycles, as hospitals upgrade legacy beds with modern designs featuring automation, pressure injury prevention, and digital connectivity. Favorable reimbursement frameworks and the strong presence of leading medical equipment manufacturers further support market strength. Additionally, growth in home healthcare and post-acute care services is expanding demand beyond traditional hospital settings, reinforcing North America’s dominant position.

Europe Hospital Bed Market Trends

The European hospital bed market is expected to grow steadily, supported by aging demographics, expanding long-term care infrastructure, and continuous modernization of healthcare facilities. Countries such as Germany, the U.K., France, Italy, and the Nordic nations are key contributors due to well-developed hospital networks and strong public healthcare systems. The rising incidence of chronic diseases and mobility-related conditions is increasing demand for electric and specialized hospital beds across acute and long-term care environments.

European healthcare providers are placing greater emphasis on patient comfort, safety, and infection control, driving adoption of advanced bed technologies. Regulatory standards related to medical device safety and ergonomics are also encouraging the replacement of outdated beds. Government funding programs to upgrade hospital infrastructure, along with growing demand from nursing homes and rehabilitation centers, are driving market expansion. Additionally, the growing focus on home-based care models is creating new opportunities for hospital bed manufacturers across the region.

Asia Pacific Hospital Bed Market Trends

The Asia Pacific hospital bed market is expected to register a relatively higher CAGR of around 9.7% between 2026 and 2033, driven by rapid healthcare infrastructure development and rising healthcare expenditure. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are experiencing strong growth driven by expanding hospital networks and greater access to healthcare services. Growing populations, rising burden of chronic diseases, and higher surgical volumes are fueling demand for hospital beds across acute and long-term care settings.

Governments across the region are investing heavily in hospital construction, capacity expansion, and the modernization of public healthcare facilities. The increasing adoption of electric and semi-electric beds is being supported by improved affordability and local manufacturing capabilities. Additionally, the expansion of private hospitals and growing medical tourism in select countries are strengthening demand. The shift toward home healthcare and elder care services is further positioning the Asia Pacific as the fastest-growing regional market.

The global hospital bed market is highly competitive, with strong participation from Medline Industries Inc., Antano Group S.R.L., Invacare Corporation, Savaria Corporation, and Linet SPOL S.R.O. These companies leverage broad global distribution networks, diversified hospital and home-care bed portfolios, and continuous innovation in electric, semi-electric, and specialty bed designs to strengthen their market positions.

Key players are increasingly focused on ergonomics, patient safety features, digital bed integration, and cost-efficient manufacturing to address evolving clinical and care-setting requirements. Strategic priorities include product portfolio expansion, technology upgrades, pricing optimization, and partnerships with healthcare providers and distributors to accelerate adoption across acute care, long-term care, and home care settings.

Key Industry Developments:

The global hospital bed market is projected to be valued at US$ 5.2 Bn in 2026.

Rising hospitalization rates driven by aging populations, increasing prevalence of chronic diseases, higher surgical volumes, and sustained investments in healthcare infrastructure are the primary drivers of global hospital bed demand.

The global hospital bed market is poised to witness a CAGR of 7.2% between 2026 and 2033.

Rapid expansion of home healthcare and long-term care facilities, coupled with growing adoption of smart, electric, and connected hospital beds in emerging markets, presents significant growth opportunities.

Medline Industries Inc., Antano Group S.R.L., Invacare Corporation, Savaria Corporation, and Linet SPOL S.R.O. are some of the key players in the hospital bed market.

| Report Attributes | Details |

|---|---|

| Historical Data/Actuals | 2020 – 2025 |

| Forecast Period | 2026 – 2033 |

| Market Analysis | Value: US$ Bn Volume (Units) If Applicable |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

By Product

By Application

By End User

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author