- Healthcare IT

- Colon Screening Market

Colon Screening Market Size, Share, and Growth Forecast, 2026 - 2033

Colon Screening Market by Screening Test Type (Fecal Occult Blood Test (FOBT), Others), Age Group (Below 45 Years, 45-54 Years, Others), End-user (Hospitals, Diagnostic Laboratories, Specialty Clinics, Others), and Regional Analysis for 2026 - 2033

Colon Screening Market Share and Trends Analysis

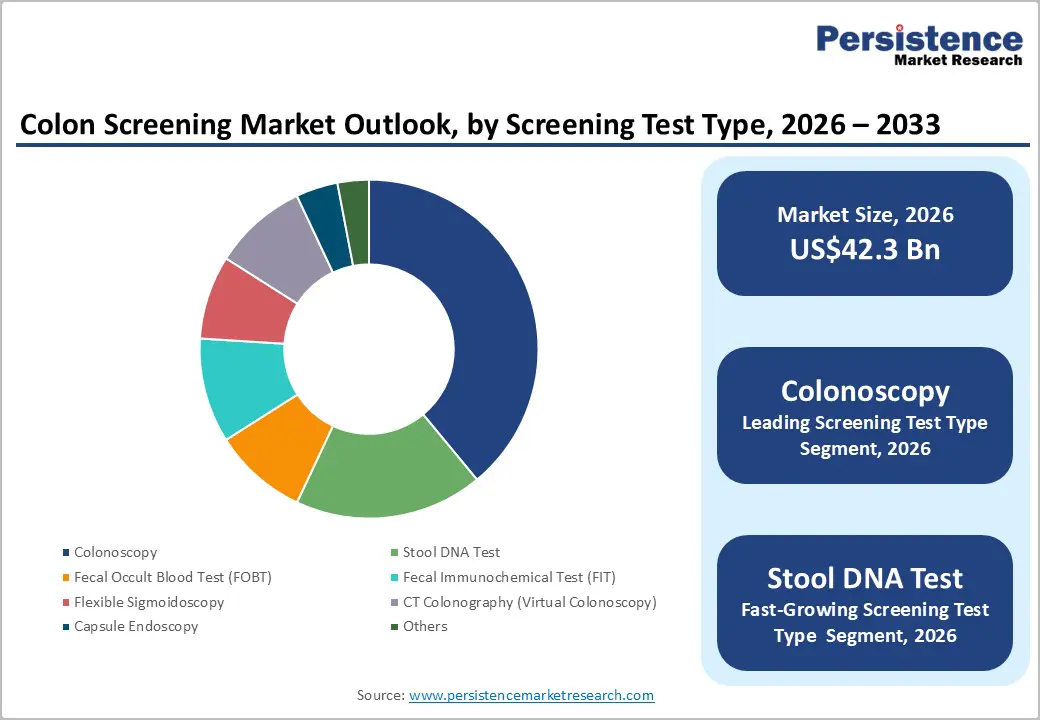

The global colon screening market size is likely to be valued at US$42.3 billion in 2026 and is estimated to reach US$58.7 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by expanding preventive healthcare programs, increasing colorectal cancer incidence, and rising adoption of non-invasive screening technologies.

Growing populations aged above 45 years continue to increase screening eligibility, creating sustained demand for diagnostic procedures and at-home testing solutions. Regulatory recommendations supporting earlier screening initiation are expanding the addressable patient pool. Technological improvements in stool DNA testing, artificial intelligence-assisted colonoscopy, and digital diagnostics are improving detection rates and patient compliance.

Key Industry Highlights:

- Leading Screening Test Type: Colonoscopy is set to hold around 39% revenue share in 2026, driven by high diagnostic accuracy.

- Fastest-Growing Screening Test Type: Stool DNA test is projected as the fastest-growing segment, driven by rising preference for non-invasive screening.

- Leading End-user: Hospitals are estimated to hold roughly a 42% revenue share in 2026, driven by integrated diagnostic infrastructure.

- Fastest-Growing End-User: Home care settings are forecast to record the fastest growth, driven by expanding adoption of at-home testing solutions.

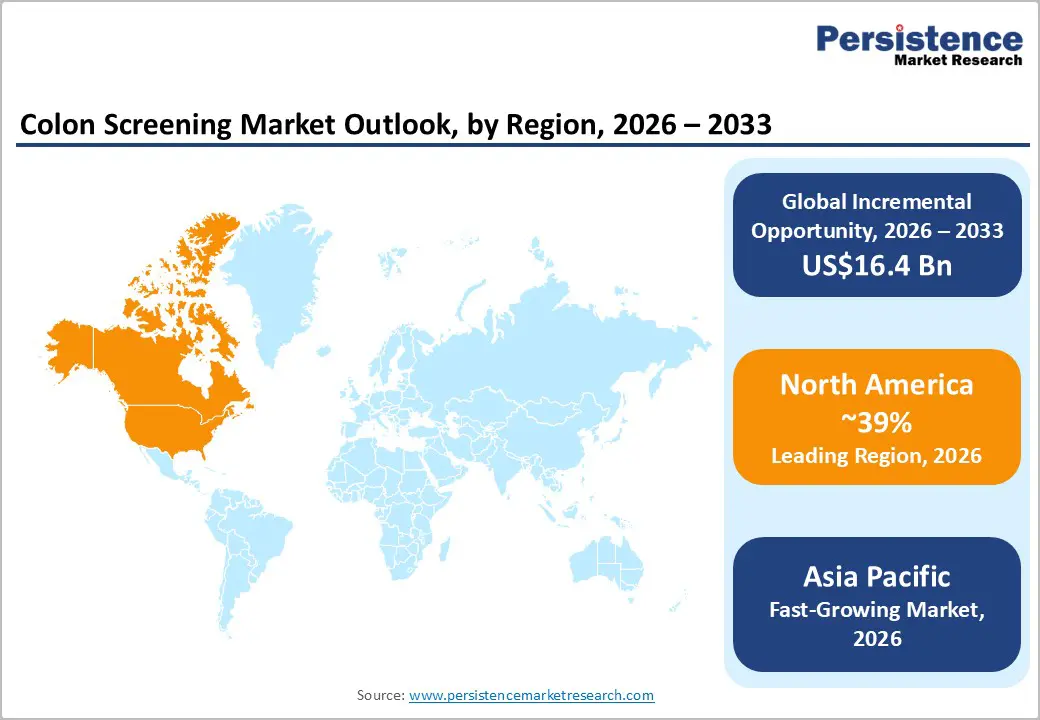

- Regional Leadership: North America is projected to capture roughly 39% of the market share by 2026, while Asia Pacific is also forecast to record the fastest growth, driven by healthcare infrastructure expansion.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as Exact Sciences Corporation and Medtronic plc leveraging technology integration and diagnostic innovation.

DRO Analysis

Driver - Expansion of Preventive Screening Guidelines and Public Health Programs

Updated clinical recommendations supporting colorectal cancer screening from age 45 are increasing eligible patient populations and strengthening long-term demand for diagnostic services. Public health agencies continue emphasizing early detection due to favorable treatment outcomes and reduced healthcare expenditure associated with advanced-stage cancer management. Screening adoption is benefiting from awareness campaigns, insurance coverage expansion, and physician-led preventive care initiatives across developed healthcare systems.

Government-supported screening policies are improving compliance among average-risk populations. The Centers for Disease Control and Prevention stated in 2025 that adults aged 45-75 should undergo routine colorectal cancer screening, expanding screening volumes across multiple testing modalities. Rising participation rates are creating sustained utilization of colonoscopy, fecal immunochemical testing, and stool DNA testing services while strengthening investments in diagnostic infrastructure.

Restraint - High Procedure Costs and Resource-Intensive Infrastructure

Colonoscopy procedures require specialized equipment, trained gastroenterologists, anesthesia support, and dedicated clinical facilities. Capital-intensive deployment increases operational expenditure for healthcare providers. Cost pressures create affordability challenges for underfunded healthcare systems and smaller medical facilities, limiting expansion potential across certain patient segments.

Lengthy procedure scheduling, bowel preparation requirements, and post-procedure recovery needs reduce throughput efficiency. Healthcare providers face rising labor costs and staffing shortages that constrain scalability. Margin pressure increases when facilities attempt to expand screening capacity without corresponding reimbursement adjustments or workforce availability.

Opportunity - Growth Potential in Home-Based Screening Programs

Home-based testing solutions present a scalable pathway for expanding population screening coverage. Fecal immunochemical tests and stool DNA tests enable sample collection outside healthcare facilities, improving accessibility among underserved populations. Healthcare providers can increase participation rates through digital patient engagement platforms, mail-based test distribution, and automated follow-up systems.

Policy support for preventive healthcare is encouraging broader reimbursement coverage for non-invasive testing methods. Increased adoption of remote diagnostics can reduce healthcare facility burden while supporting earlier disease identification. Companies investing in connected diagnostic ecosystems and laboratory integration capabilities are positioned to strengthen patient adherence and improve screening completion rates.

Category-wise Analysis

Screening Test Insights

Colonoscopy is anticipated to secure around 39% of the colon screening market share in 2026, reflecting strong clinical acceptance and high diagnostic accuracy across preventive oncology programs. Exact Sciences continues to support follow-up screening pathways through integrated diagnostic ecosystems, reinforcing procedure demand among eligible populations. Favorable reimbursement coverage and physician preference sustain utilization across hospitals, specialty clinics, and ambulatory care environments.

The stool DNA test is expected to be the fastest-growing segment, propelled by increasing preference for non-invasive diagnostics and home-based screening participation. Mainz Biomed advanced the development of next-generation stool DNA technologies during 2025, supporting broader commercialization opportunities. Improved patient convenience, molecular biomarker integration, and expanding reimbursement pathways continue to accelerate adoption across preventive healthcare networks.

Age Group Insights

The 55-64 Years segment poised to dominate with a forecast market share of over 34% in 2026, powered by elevated screening compliance and increasing preventive healthcare engagement. CDC recommendations emphasizing routine colorectal cancer screening strengthen testing volumes within this demographic. Growing awareness of early detection benefits and favorable insurance coverage continues to support diagnostic procedure utilization and follow-up assessments.

The 45-54 Years segment estimated to be the fastest-growing segment, fueled by guideline revisions lowering the recommended screening initiation age. Public health agencies intensified awareness campaigns targeting earlier screening participation, expanding eligible populations entering preventive care pathways. Rising incidence trends among younger adults and growing availability of non-invasive testing solutions continue to strengthen screening adoption rates.

End-user Insights

Hospitals are likely to be the leading segment with a projected 42% of the colon screening market share in 2026 due to extensive procedural capabilities and integrated diagnostic infrastructure. Mayo Clinic continues expanding advanced gastroenterology services supporting comprehensive colorectal screening programs. Availability of specialist expertise, imaging systems, and surgical support sustains high patient volumes across hospital networks.

Home care settings are anticipated to be the fastest-growing segment, fueled by rising utilization of at-home screening kits and digital health monitoring platforms. FDA-recognized stool-based testing approaches continue to support decentralized diagnostic pathways for average-risk populations. Greater convenience, reduced facility dependence, and expanding preventive healthcare participation are strengthening adoption across remote screening programs.

Regional Insights

North America Colon Screening Market Trends

North America is expected to lead with an estimated 39% of the colon screening market share in 2026, supported by established reimbursement frameworks, strong preventive screening participation, and advanced diagnostic infrastructure. Adoption of stool DNA testing, AI-assisted colonoscopy, and digital patient engagement platforms continues to expand screening coverage.

U.S. Colon Screening Market Insights

The U.S. is projected to account for approximately 82% of North America's revenue in 2026, supported by broad insurance coverage, high screening compliance, and extensive endoscopy capacity. Federal screening recommendations continue expanding eligible populations. Exact Sciences Corporation and Guardant Health are increasing the availability of non-invasive diagnostic solutions.

Canada Colon Screening Market Insights

Canada is forecast to contribute nearly 18% of North America’s revenue share in 2026, driven by organized provincial screening programs and growing public health investments. Healthcare authorities continue promoting fecal immunochemical testing for population-wide screening initiatives. Expansion of laboratory infrastructure and digital healthcare systems is improving participation rates and strengthening preventive oncology capabilities.

Europe Colon Screening Market Trends

Europe is expected to account for approximately 28% of the colon screening market share in 2026, supported by national cancer prevention strategies and increasing adoption of non-invasive diagnostics. Government-funded screening programs are expanding test utilization across public healthcare systems. Regulatory emphasis on early cancer detection is encouraging the deployment of molecular diagnostic technologies and advanced imaging platforms.

Germany Colon Screening Market Insights

Germany is expected to represent nearly 21% of Europe's revenue share in 2026, supported by structured screening initiatives, advanced healthcare infrastructure, and strong healthcare expenditure. Diagnostic laboratories continue investing in automation and molecular testing technologies. Growing participation among aging populations is increasing demand for routine colorectal cancer screening services.

U.K. Colon Screening Market Insights

The U.K. is projected to hold around 17% of Europe's revenue share in 2026, driven by national bowel cancer screening initiatives and healthcare modernization programs. Public awareness campaigns continue to improve screening uptake. Expansion of fecal immunochemical testing and digital patient management systems is strengthening efficiency across preventive healthcare pathways.

Asia Pacific Colon Screening Market Trends

Asia Pacific is forecast to be the fastest-growing market for colon screening, stimulated by healthcare infrastructure expansion, increasing cancer awareness, and rising healthcare expenditure. Governments are strengthening preventive healthcare initiatives while healthcare providers expand diagnostic and endoscopy capacity. Growing access to screening services is accelerating adoption across major economies.

China Colon Screening Market Insights

China is projected to account for nearly 38% of Asia Pacific's revenue share in 2026, supported by hospital expansion, healthcare modernization, and increasing implementation of preventive oncology programs. Public investments in diagnostic infrastructure are improving screening accessibility. Domestic diagnostic manufacturers continue advancing molecular testing capabilities to address growing healthcare demand.

India Colon Screening Market Insights

India is forecast to contribute approximately 16% of Asia Pacific's revenue share in 2026, driven by expanding private healthcare infrastructure, rising cancer awareness, and increasing adoption of preventive health checkups. Hospital networks continue investing in endoscopy facilities and laboratory services. Government-led cancer control initiatives are supporting the long-term development of screening programs across urban and secondary healthcare centers.

Competitive Landscape

The global colon screening market is moderately fragmented, characterized by participation from diagnostic technology developers, endoscopy equipment manufacturers, and laboratory service providers. Competitive positioning is influenced by clinical accuracy, reimbursement support, regulatory approvals, and healthcare provider relationships. Key participants include Exact Sciences Corporation, Medtronic plc, Olympus Corporation, Fujifilm Holdings Corporation, and Sysmex Corporation.

Companies continue investing in molecular diagnostics, artificial intelligence integration, and laboratory network expansion to strengthen commercial reach. Product differentiation increasingly depends on diagnostic sensitivity, patient convenience, and workflow efficiency. Strategic partnerships between diagnostic developers and healthcare systems are supporting broader screening adoption and commercialization opportunities.

Key Industry Developments:

- In May 2026, the American Cancer Society added Guardant Health’s Shield blood test to recommended colorectal cancer screening options, reinforcing the expansion of non-invasive colon screening pathways for underserved and screening-resistant populations.

Companies Covered in Colon Screening Market

- Exact Sciences Corporation

- Medtronic plc

- Olympus Corporation

- Fujifilm Holdings Corporation

- Sysmex Corporation

- Eiken Chemical Co., Ltd.

- Mainz Biomed N.V.

- Danaher Corporation

- Abbott Laboratories

- Becton, Dickinson and Company

- Quest Diagnostics Incorporated

- Laboratory Corporation of America Holdings

- Guardant Health, Inc.

- Geneoscopy, Inc.

- Cancer Prevention Pharmaceuticals, Inc.

Frequently Asked Questions

The global colon screening market is projected to reach US$42.3 billion in 2026.

Increasing colorectal cancer prevalence, expansion of preventive screening programs, and growing adoption of non-invasive diagnostic technologies drive the colon screening market.

The colon screening market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Expansion of home-based screening programs, adoption of AI-enabled diagnostic technologies, and commercialization of blood-based and molecular screening tests create key market opportunities.

Some of the key market players include Exact Sciences Corporation, Medtronic plc, Olympus Corporation, Fujifilm Holdings Corporation, and Sysmex Corporation.