ID: PMRREP4371| 191 Pages | 17 Nov 2025 | Format: PDF, Excel, PPT* | Chemicals and Materials

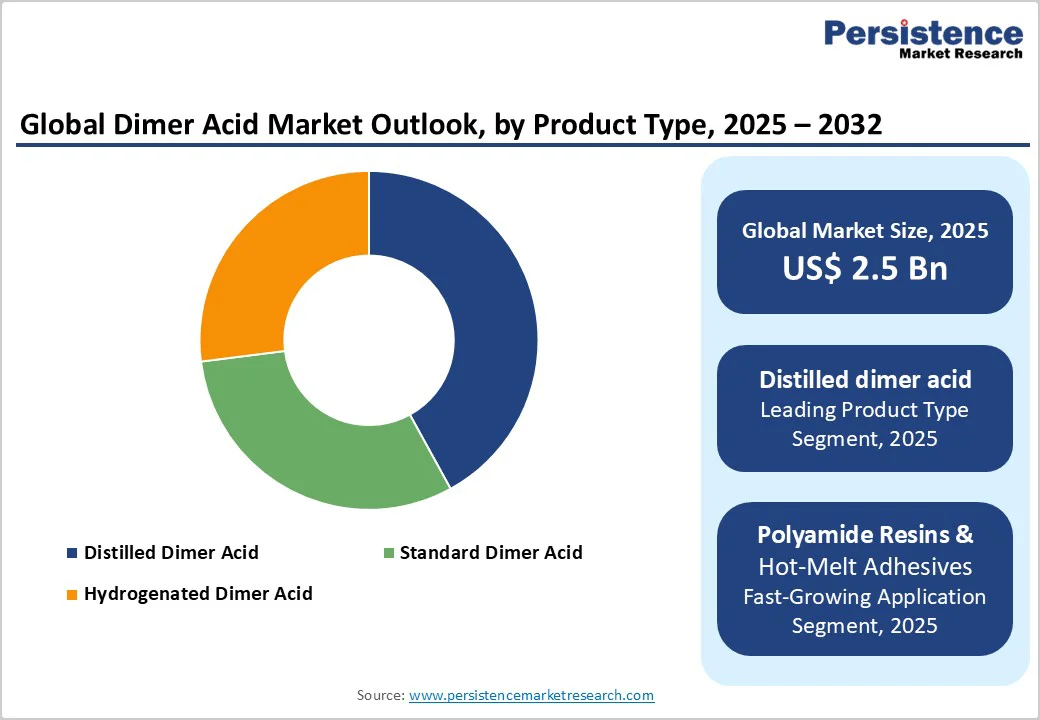

The global dimer acid market size is likely to be valued at US$2.5 billion in 2025 and is projected to reach US$4.1 billion, growing at a CAGR of 7.2% between 2025 and 2032. This robust expansion is primarily driven by the rise in demand from the construction and automotive industries, coupled with the growing preference for bio-based and sustainable chemical alternatives. The shift toward environmentally-friendly materials has further accelerated adoption across adhesives, coatings, and specialty chemical applications.

| Key Insights | Details |

|---|---|

|

Dimer Acid Market Size (2025E) |

US$2.5 Bn |

|

Market Value Forecast (2032F) |

US$4.1 Bn |

|

Projected Growth CAGR (2025-2032) |

7.2 % |

|

Historical Market Growth (2019-2024) |

6.4 % |

The construction and automotive industries serve as major growth engines for dimer acid consumption, primarily in high-performance adhesives, coatings, and sealants. In the automotive sector, dimer acids are widely applied for structural bonding, body panels, and under-the-hood components owing to their superior heat resistance, corrosion protection, and durability. Leading manufacturers such as BASF and Croda International have introduced specialized dimer acid products that not only enhance vehicle structural integrity but also support weight reduction, thereby improving fuel efficiency.

Rapid expansion of automotive production in China has further escalated demand, with dimer acid-based coatings delivering long-lasting performance while adhering to environmental sustainability standards. Concurrently, the construction sector extensively utilizes dimer acids in resins, paints and coatings for both interior and exterior applications, providing resilience against temperature fluctuations, acid rain, and harsh weather conditions. Growing infrastructure development worldwide continues to reinforce strong demand for dimer acid-based materials, highlighting their indispensable role in modern construction and automotive applications.

Sustainability trends and stringent environmental regulations are driving the adoption of bio-based dimer acids derived from renewable sources, such as tall oil fatty acids (TOFA) and vegetable oil fatty acids (VOFA) from soybean, rapeseed, cottonseed, and sunflower oils. These materials are inherently biodegradable, aligning with regulatory frameworks in Europe and North America that aim to reduce volatile organic compound (VOC) emissions.

Croda International expanded its bio-based dimer acid range to meet coating and adhesive demands in eco-conscious markets. This shift toward renewable, environmentally friendly materials benefits the dimer acid market as industries increasingly prioritize sustainable solutions, encouraging manufacturers to innovate and cater to green chemistry demands while supporting circular economy principles.

Dimer acid production depends heavily on vegetable oils and tall-oil fatty acids, making the market sensitive to raw-material price fluctuations. Prices vary due to agricultural yield changes, climate conditions, and global commodity trends, directly affecting production costs and profit margins. For instance, China consumed 2.6 million metric tons of sunflower seed oil in 2021, reflecting the scale of regional dependency.

Price volatility complicates manufacturers’ pricing strategies and may discourage price-sensitive customers, especially when alternative synthetic resins offer competitive stability. This challenge is particularly pronounced for small and medium-sized enterprises that lack hedging capacity or long-term supply contracts. Managing costs amid fluctuating feedstock prices remains a critical challenge for market participants seeking to maintain profitability and a consistent product supply.

Despite being bio-based, dimer acids face complex regulatory requirements, including the U.S. Toxic Substances Control Act, Canada’s Domestic Substances List, and China’s chemical inventories. Compliance entails extensive testing, documentation, and certification, increasing operational costs and market entry barriers, particularly for smaller firms. Regulatory requirements for VOC emissions and sustainability standards continue evolving, compelling manufacturers to invest in R&D to maintain compliance without compromising performance.

The polyamide resin sector, a key application area for dimer acids, is particularly affected, as adhesives, coatings, and oilfield chemicals must meet these stringent environmental criteria. Consequently, navigating regulatory complexity remains a critical restraint, influencing product formulation decisions, market accessibility, and global competitiveness.

The oil and gas sector offers substantial opportunities, driven by exploration, production, and refining activities. Dimer acids are used as corrosion inhibitors, scale inhibitors, wetting agents, surfactants, and demulsifiers, and are essential for drilling operations and oil recovery. The extreme operational environments in oilfield applications require chemicals with thermal stability, corrosion resistance, and lubricity, which dimer acids provide. Rising energy consumption and exploration in emerging markets such as India and China are expected to stimulate drilling activity, boosting dimer acid use. Consequently, oilfield chemicals represent a high-potential market for manufacturers seeking diversified revenue streams beyond traditional automotive and construction applications.

Advanced dimer acid-based polyamide resins are driving growth in hot-melt adhesives and epoxy curing applications. Their unique molecular structure, with long hydrocarbon chains and cyclic formations, imparts flexibility, adhesion, and hydrophobicity. Dimer-based polyamides outperform conventional nylons, offering reduced hydrophilicity and superior performance in marine maintenance, industrial coatings, flooring, and epoxy adhesives.

Hot-melt adhesives are increasingly used in packaging, food and beverage, and industrial sectors due to rapid setting, solvent-free bonding, and strong adhesion to metals, paper, wood, PVC, and polyolefins. Companies like Henkel and Arkema leverage dimer acids to develop adhesives with enhanced strength, durability, and environmental resistance. Continuous innovation in formulation technologies expands the application spectrum, positioning dimer acid polyamides as enablers of next-generation adhesive and coating solutions across industrial and consumer markets.

Distilled dimer acid dominates with a 42% share in 2025, offering superior purity and consistency. Molecular distillation removes trimer acids and residual monomers, resulting in higher dimer content (95–99%), improved color stability, and reduced viscosity. These qualities make distilled grades ideal for high-performance adhesives, coatings, and advanced polymer applications.

Hydrogenated dimer acid is another significant product segment, valued for its excellent color retention, oxidative stability, and low odor profile. It is increasingly preferred in applications requiring high flexibility and durability, such as polyamide resins, lubricants, and cosmetics. Standard dimer acids, while less pure, continue to find broad use in cost-sensitive sectors like paints, inks, and surface coatings due to their affordability and balanced performance. The growing demand for bio-based and specialty-grade derivatives is further shaping product innovations and expanding the market potential for high-purity dimer acids globally.

Viscous liquid dimer acids lead the market with 78% share, owing to superior processing and application versatility. Naturally occurring as yellowish liquids, viscosities range from 3,000 to 8,500 mPa · s at 25°C, facilitating mixing and reactions with amines, alcohols, and other chemical partners without additional melting. The liquid form simplifies handling, reduces energy consumption, and ensures compatibility with industrial equipment.

It also exhibits excellent solubility in hydrocarbons and organic solvents, while remaining immiscible with water, making it ideal for non-aqueous coatings, adhesives, and lubricant additives. Major suppliers such as Aturex Group, Kraton Corporation, and BASF package liquid dimer acids in drums, ISO tanks, flexi bags, or IBCs, enabling flexible delivery options to meet varying industrial requirements.

Polyamide resins and hot-melt adhesives dominate, capturing 47% market share in 2025. Dimer acids react with diamines such as ethylenediamine and hexamethylenediamine to form resins with excellent adhesion, flexibility, and resistance to water, oils, and greases. Hot-melt adhesives achieve softening points of 100–200°C and are widely used in packaging, automotive, electronics, and bookbinding.

Dimer-based polyamides are less crystalline, more hydrophobic, and provide strong hydrogen bonding, outperforming conventional nylons. Bostik emphasizes dimer-based adhesives for demanding industrial applications, valued for rapid setting, solvent-free characteristics, and strong substrate adhesion. Growing packaging demand drives hot-melt polyamide adoption, reinforcing its leadership in the dimer acid market.

The automotive industry dominates dimer acid consumption, accounting for 38% of total consumption, driven by high-performance demands. Dimer acid-based coatings, adhesives, and sealants enhance adhesion, corrosion resistance, durability, and structural integrity under extreme conditions, while lubricants and machining chemicals improve thermal stability and reduce friction. Additionally, lightweighting initiatives boost demand, as dimer acids enable significant weight reduction without compromising mechanical or thermal performance, reinforcing their critical role in automotive applications.

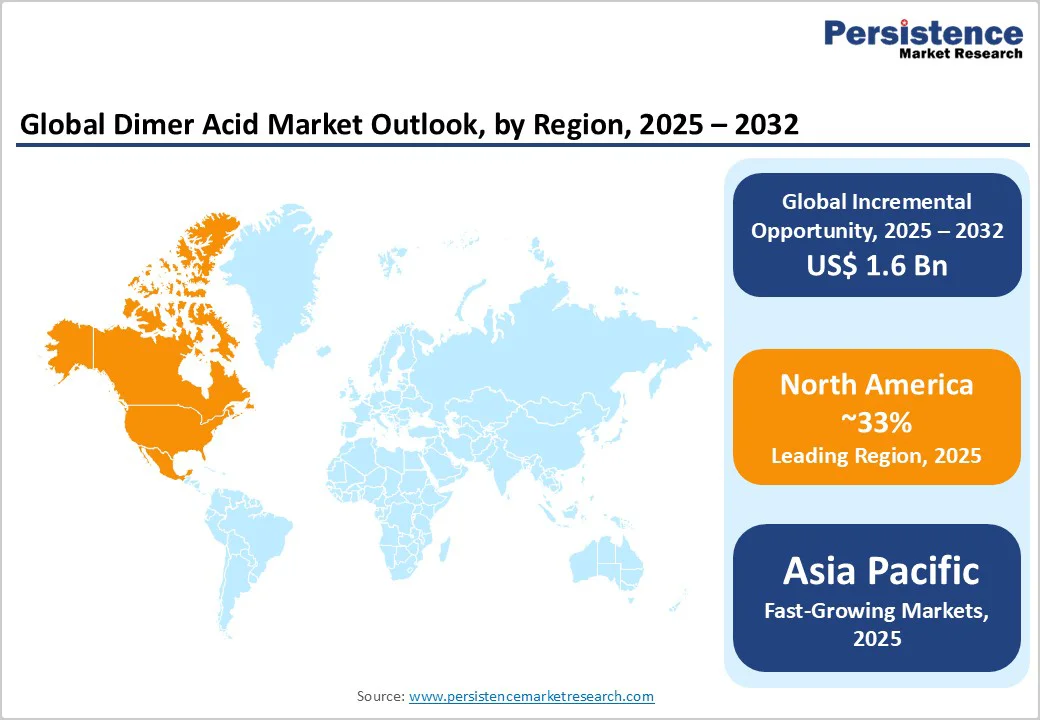

North America holds a 36% share of the global dimer acid market, led by the U.S., where regulatory support for sustainable chemistry and industrial innovation drives adoption. EPA initiatives promoting bio-based chemicals and reducing VOC emissions have accelerated the use of dimer acids from renewable feedstocks. Advanced manufacturing practices, AI-driven process optimization, and robust construction and automotive sectors further boost demand. Leading companies, such as BASF with its "BASF 4.0" program, have improved yield consistency by 15%, while Kraton Corporation leverages vertical integration in tall oil processing. Ongoing infrastructure investments and growing preference for eco-friendly adhesives and coatings support steady market expansion across the United States and Canada.

Europe is a significant market for dimer acids, characterized by stringent regulations and strong emphasis on sustainability. Compliance with REACH drives manufacturers to adopt eco-friendly formulations, conduct rigorous testing, and maintain thorough documentation. Germany leads due to its dominant automotive and chemical manufacturing sectors, often specifying dimer acid-based adhesives for lightweighting and fuel efficiency. France, the UK, and Spain are seeing growing demand across construction, renovation, and industrial projects. Key players, including Oleon N.V., have doubled production capacity, integrating circular economy principles. Low-VOC dispersions and green manufacturing, exemplified by BASF’s Dilovas? facility, align with Europe’s environmental targets while meeting the region’s demand for high-performance adhesives, coatings, and specialty chemicals.

Asia Pacific represents the fastest-growing regional market, driven by rapid industrialization, infrastructure development, and automotive expansion. China accounts for 26.8% of the global market, with strong domestic manufacturing and construction output valued at USD 4.29 trillion in 2021, fueling dimer acid demand. India’s infrastructure initiatives, contributing around USD 640 billion in 2022, and Japan’s industrial chemical consumption also support steady market growth. ASEAN nations are increasingly adopting green chemistry and sustainable formulations, promoting the uptake of bio-based dimer acids. The combination of large-scale infrastructure projects, automotive production, and environmental awareness creates ample opportunities for manufacturers to develop eco-friendly, high-performance adhesives, coatings, and specialty chemical solutions across the region.

The global dimer acid market is moderately fragmented, comprising established multinational corporations and numerous regional or specialized manufacturers. Market concentration features vertically integrated companies with captive raw material sources alongside producers focused on specific grades or applications.

Leading players such as BASF SE, Croda International Plc, Emery Oleochemicals, Kraton Corporation, and Oleon N.V. hold significant shares through broad product portfolios, global distribution, and strong customer relationships. Differentiation is driven by continuous R&D investment, with BASF’s “BASF 4.0” AI initiative reducing production downtime by 15% and improving yield by 12%, while Croda achieves an 8% energy reduction and enhanced product consistency via AI monitoring.

The global dimer acid market is valued at US$ 2.5 billion in 2025, projected to reach US$ 4.1 billion by 2032 with a CAGR of 7.2%.

Demand is driven by the construction and automotive industries, the adoption of bio-based chemicals, oilfield applications, and stringent environmental regulations.

Distilled dimer acid leads with 42% share due to high purity, color stability, reduced viscosity, and superior performance.

North America holds a 33% share, led by the U.S., with strong regulations, an innovation ecosystem, and demand from the automotive and construction sectors.

Growth exists in oilfield chemicals, polyamide resins, advanced adhesives, sustainable packaging adhesives, and emerging Asia Pacific markets.

Major players include BASF SE, Croda International, Emery Oleochemicals, Kraton Corporation, Oleon N.V., Aturex Group, Harima Chemicals, Florachem, Jarchem, Nissan Chemical, Arizona Chemical, Wilmar, Cargil, and other regional manufacturers.

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis |

Value: US$ Bn, Volume: As Applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

By Product Type

By Form

By Grade

By Application

By Industry

By Regions

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author