- Specialty & Fine Chemicals

- White Spirit Market

White Spirit Market Trends, Size, Share, Growth, Forecasts, 2025 - 2032

White Spirit Market By Grade (Low Flash, Regular Flash, High Flash) Product Type (Type 0, Type 1, Type 2, Type 3) Application (Paint Thinner, Cleaning Solvent, Degreasing Solvent, Fuel, Disinfectants, Others) and Regional Analysis for 2025 - 2032

White Spirit Market Share and Trends Analysis

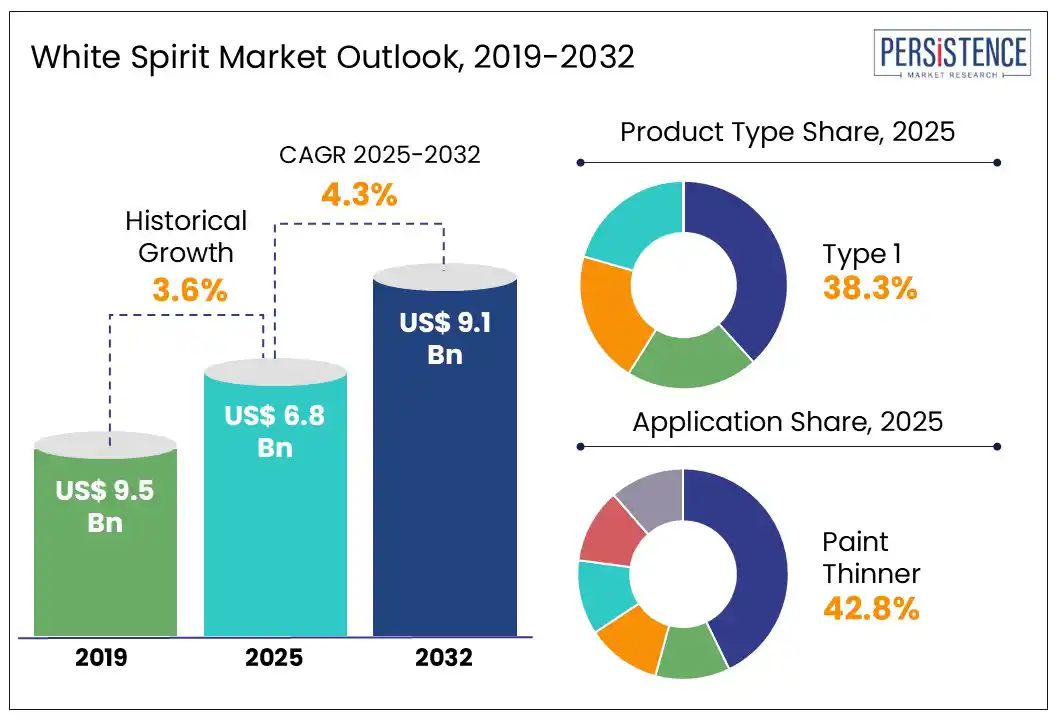

The global white spirit market is likely to be valued at USD 6.8 Bn in 2025 and is projected to reach USD 9.1 Bn by 2032, growing at a CAGR of approximately 4.3% in the forecast period from 2025 to 2032.

The white spirit market is driven by the steady rise in industrial coatings, automotive refinishing, and architectural paint applications. The paint manufacturers are investing in cost optimization and raw material efficiency to meet rising infrastructure needs, while also balancing price swings in petroleum-based inputs. As the global markets expand, white spirit holds relevance due to its strong solvency performance, ease of application, and compatibility with both consumer-grade and industrial-grade coatings, particularly in regions with high repaint cycles and weather exposure.

Key Industry Highlights:

- North America dominates with a 34.7% share in 2025, driven by strong solvent demand across coatings, degreasers, and cleaning segments.

- Europe captures 29.2% of the market in 2025, supported by surface treatment activity and industrial growth in Germany, France, and Italy.

- Paint thinners lead by application with a 42.8% share in 2025, fueled by solvent-based paint use in the automotive and construction sectors.

- Type 1 holds a 38.3% share by product in 2025, driven by its balanced evaporation rate and high utility in coatings and degreasing.

- Construction booms in India, Brazil, and Saudi Arabia are lifting demand for solvent-based thinners in large-scale infrastructure projects.

- Institutional and household cleaning demand surges across Asia and Europe, boosting solvent consumption in surface care formulations.

- Industrial degreasing applications grow rapidly in the U.S. and India, reinforcing the role of white spirit in equipment maintenance cycles.

- Eco-friendly alternatives such as d-limonene and aqueous cleaners challenge market share as users shift toward low-toxicity solvent options.

|

Global Market Attribute |

Details |

|

Market Size (2024A) |

US$ 5.4 Bn |

|

Estimated Market Size (2025E) |

US$ 6.8 Bn |

|

Projected Market Value (2032F) |

US$ 9.1 Bn |

|

Value CAGR (2025 to 2032) |

4.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.6% |

Market Dynamics:

Driver - Construction boom spurs uptick in paint thinner demand across emerging regions

A new wave of infrastructure expansion is reshaping the skyline across nations like India, China, Saudi Arabia, Brazil, and the UAE. From giga projects such as NEOM in Saudi Arabia to India’s projected warehousing demand of 159 Mn sq. ft by 2047, construction activity is scaling new heights. Government-backed capital expenditure and public-private partnerships are unlocking investments in transport, housing, logistics, and energy infrastructure, raising consistent demand for paint applications used in structural finishing and protection. This trend is catalyzing the consumption of solvent-based solutions used in surface preparation and coatings.

Paint thinners, crucial in diluting oil-based paints and maintaining consistency are directly tied to the volume of construction and maintenance work. These solvents help achieve smooth application, fast drying, and an even finish, especially on steel, concrete, and masonry surfaces common in high-rise and industrial buildings. As building and civil engineering activities expand in countries such as Mexico (+6.3% YoY growth in 2024) and Brazil (R$259.3 Bn infrastructure investment), the demand for thinners used in architectural coatings surges accordingly. These applications form a vital bridge between raw construction material and final finish.

As demand for these thinners increases, so does the appetite for white spirit, a key solvent in their formulation. With real estate on a steady climb, India is alone forecasted to touch US$5.8 Tn by 2047 and infrastructure megaprojects underway across the Middle East and Africa. The interdependence between paint, coatings, and solvent systems reflects how rising construction directly supports long-term demand for white spirit, solidifying its role in the region’s urban transformation.

Restraint - Eco alternatives challenge the market grip of white spirit

The rise of low-toxicity and biodegradable cleaning agents is steadily shrinking the footprint of white spirit in both household and industrial settings. Safer options such as d-limonene, isopropyl alcohol, and aqueous-based cleaners are gaining preference due to lower emissions and regulatory pushback on petroleum-derived products. This shift is especially evident in Europe and the U.S., where environmental norms are getting stringent every year.

Alongside safety concerns, fast-evaporating substitutes such as acetone, MEK, and butyl cellosolve are proving more effective in high-speed operations. These replacements are versatile and offer quicker turnaround in degreasing and surface prep, often with less residue. As these newer solutions carve market space, demand for white spirit continues to face pressure, particularly in industries that prioritize eco standards and air-quality compliance.

Opportunity - Cleaning solvent applications unlock growth in institutional and household markets

Across major regions such as Asia, Africa, Europe, and North America, the role of cleaning solvents is expanding with the shifting dynamics of household and institutional consumption. India’s household sector accounting for nearly 64% of gross domestic savings is witnessing a rapid adoption of surface cleaners and solvent-based solutions. The average household size is shrinking, yet urban density is bringing a higher usage of solvent cleaners in homes and public spaces.

In Africa, consumer spending is projected to hit US$2.5 trillion by 2030, much of it flowing into hygiene and maintenance products, led by a tech-savvy middle class and e-commerce growth.

Solvents form the core of many cleaning agents used across household and institutional settings. Whether in daily-use degreasers, wall cleaners, or stain removers, thinning and dissolving agents play a critical part in cleaning formulations. These agents ensure better spreadability, quicker evaporation, and high surface efficacy, particularly in multi-use spaces like schools, clinics, and offices.

With 202 million households in the EU, and over 75 million being single adults, demand is surging for ready-to-use solvent cleaners that cater to smaller yet more active living units. The U.S. also saw its median household income rise to $80,610 in 2023, boosting discretionary spending on home care and upkeep products.

White spirit remains a key ingredient in the manufacturing of paint thinners used as cleaning agents across these economies. Its use spans from solvent-rich domestic products to large-scale institutional cleaners, creating a steady pull in demand.

With rising investments across Indian households and institutions, ongoing shifts in Europe’s household structures, and consistent consumption growth in African and Middle Eastern markets, the demand pipeline for white spirit is reinforced by changing consumer behavior and evolving cleaning practices.

Market Key Trend

Degreasing solvents gain traction amid industrial maintenance surges

Industrial maintenance is scaling fast across leading economies, driven by aging equipment, regulatory pressure, and increasing automation. In the U.S., industrial upkeep now accounts for upto 20% of operating budgets in many plants. Manufacturing added US$2.3 trillion to the U.S. GDP in 2023, showed consistent output growth despite dips in overall industrial production. Vehicle, electronics, and chemical sectors rely heavily on solvent-based degreasers, creating a solid pull for high-purity cleaning agents. Similar upticks are seen in Europe, where sold production crossed €5.9 trillion in 2023, despite modest slowdowns in specific manufacturing streams.

In India, industrial capacity expansion is in full swing. Manufacturing investments surged to US$428 billion in FY23–24, and output is poised to touch US$1 trillion by FY26. Fast-growing segments such as machinery, automotive, and electronics need frequent degreasing during operations and servicing.

The demand for degreasing solvents is also expanding in sub-Saharan Africa, despite a slight decline in 2023 output to US$234 billion. Regular servicing of mining equipment and large-scale industrial assets in the region is becoming standard, reinforcing the role of solvent-based cleaning products.

This maintenance-driven demand aligns strongly with the usage of white spirit, a staple in degreasing operations. As sectors lean on mechanical consistency and operational uptime, especially in high-output markets, reliance on solvent cleaners with low residue and strong penetration power grows.

From the U.S. to India, where PMI hit a 16-year high, to the Middle East's energy-linked infrastructure growth, this shift anchors long-term opportunities in the degreasing solvent space and secures a meaningful growth path for the white spirit market.

Category-wise Analysis

Product Type Insights

Type 1 holds the highest market share of 38.3% in 2025, driven by its wide utility in cleaning, degreasing, and formulation of coatings. Its low aromatic content and stable evaporation rate make it a preferred choice across industries needing safe and efficient solvent performance. Type 1 maintains strong traction in metal processing, automotive refinishing, and household maintenance products. As end-users seek consistent drying profiles and low-toxicity options, this category continues to outperform others. Its compatibility with oil-based systems strengthens its position in both commercial and domestic spaces.

Application Insights

Paint thinners account for a market share of 42.8% in 2025, driven by their strong role in both commercial and residential sectors. In the U.S., solvent-based paints account for nearly 55% of total coatings used, especially in the automotive, aerospace, and construction industries, where performance under extreme conditions matters.

Europe’s growth is shaped by dual-use trends. DIY consumers use paint thinners for home projects, while professionals rely on them for scale and precision. Meanwhile, India’s paint industry, valued at over ?70,000 crore, continues to favor solvent-borne coatings in automotive and decorative applications despite growing environmental concerns.

Demand for traditional solvent carriers remains steady where durability and drying speed are key. Paint thinners continue to be the go-to choice for cutting viscosity, cleaning tools, and ensuring even finishes in oil-based systems. In these applications, white spirit plays a crucial role due to its high solvency power and compatibility with industrial-grade paints. As water-based alternatives expand, solvent formulations still dominate legacy and performance-driven segments, ensuring that thinners retain a critical place in the coatings supply chain.

Regional Insights

North America White Spirit Market Trends

North America holds a 22.7% share in 2025, driven by the rising use of solvents across construction, cleaning, and coating applications. A US$10 rise in Brent crude adds a 3% hike in coatings costs, pushing pricing volatility across raw materials.

Refinery utilization hit 94% in 2024, led by ExxonMobil’s $2B expansion at Beaumont, now the second-largest U.S. refinery. With 132 refineries, the U.S. continues to power chemical production, but long-term fossil-based energy is forecast to decline gradually as renewables rise 4–5% annually. Raw material costs remain unstable amid tightening supply and labor pressure.

The U.S. paint and coatings industry posted US$2.8B in exports and a US$1.6B trade surplus in 2024, with Canada and Mexico capturing US$2B, or 70% of the total. Illinois, Ohio, and Texas led state-level shipments. Despite inflation and logistics hurdles, the sector grew 5.3% in value and 2.6% in volume by mid-2024.

Demand remains strong for traditional petroleum-based materials, including white spirit, especially where waterborne or biobased options can’t match the required performance. Solvents remain vital across coatings, thinners, and degreasing lines, supporting continued growth in industrial and commercial use cases.

Europe White Spirit Market Trends

Europe holds the market share of 29.2% in 2025, driven by robust demand across industrial manufacturing, automotive refinishing, and architectural coatings. The uptick in surface treatment applications, especially in Germany, France, and Italy is consistently fueling the consumption of petroleum-derived solvents. Rising vehicle production and home improvement activity across urban hubs have added further tailwinds to the solvent supply chain.

Several EU nations continue to focus on optimizing their chemical production footprint despite recent declines in base chemical output. Refinery expansions and steady infrastructure growth in transport-heavy zones such as the Netherlands and Austria sustain momentum. Though regulatory measures are tightening, demand for versatile solutions such as white spirit remains strong across select end-use segments where durability and performance cannot be compromised.

Competitive Landscape

The global white spirit market operates in a consolidated structure, with a handful of multinational companies dominating global supply and innovation. Shell plc is advancing circular feedstock strategies and low-carbon technologies, which could enhance solvent production practices.

ExxonMobil Corporation continues to expand its petrochemical footprint with robust refinery operations supporting consistent output. Total S.A. invests in integrated production networks, ensuring reliable delivery and regional flexibility. Idemitsu Kosan Co., Ltd. strengthens its domestic and international presence through streamlined refining and specialty solvent offerings. Neste Oyj leads in sustainable hydrocarbon alternatives, positioning itself for future demand shifts. Together, these players shape the direction and dynamics of the white spirit ecosystem.

Key Developments:

- On May 09, 2025, Shell plc. entered into a strategic collaboration with Freepoint Eco-Systems to supply pyrolysis oil to its Monaca, Pennsylvania facility, aiming to boost circularity through chemical recycling of plastic waste. While the move centers on plastics, it holds indirect value for the white spirit market by showcasing how petrochemical feedstock innovation can diversify solvent production routes. As environmental regulations tighten and crude-based solvent supply chains face pressure, advancements like this could eventually support alternative sourcing paths or process optimizations in white spirit manufacturing, especially in blending or low-aromatic formulations.

- On 15 September 2022, to accelerate the transition toward low-carbon, energy-efficient solutions, including green hydrogen production and electrification Shell plc. signed a Memorandum of Understanding (MoU) with Siemens Smart Infrastructure. The collaboration supports cleaner industrial processes that influence how solvents, including white spirit, are produced and utilized. As Shell enhances its energy systems and integrates sustainable practices across operations, the solvent value chain is likely to benefit from reduced emissions, improved feedstock sourcing, and greater process efficiency.

Companies Covered in White Spirit Market

- Shell Plc.

- ExxonMobil Corporation

- Total S.A.

- Idemitsu Kosan Co., Ltd.

- Neste Oyj

- Haltermann Carless Deutschland GmbH

- DHC Solvent Chemie GmbH

- GSB Chemical Co. Pty. Ltd.

- Al Sanea Chemical products.

Frequently Asked Questions

The global market is projected to be valued at US$ 6.8 Bn in 2025.

Paint thinners are expected to hold a 42.8% share of the market in 2025, driven by strong demand across commercial and residential coating applications.

The market is poised to witness a CAGR of 4.3% from 2025 to 2032.

Rising construction and infrastructure activity across emerging regions, paired with consistent demand for solvent-based coatings, drives the growth of the white spirit market.

Expanding institutional and household use of cleaning solvents across Asia, Europe, and North America unlocks new consumption avenues for white spirit-based formulations.

Key market players include Shell Plc., ExxonMobil Corporation, Total S.A., Idemitsu Kosan Co., Ltd., Neste Oyj, and Haltermann Carless Deutschland GmbH.