- Food Ingredients & Additives

- Hydrolyzed Plant Protein Market

Hydrolyzed Plant Protein Market Size, Share, and Growth Forecast, 2025 - 2032

Hydrolyzed Plant Protein Market By Source (Soy, Wheat, Pea, Rice, Corn, Others), Form (Powder, Liquid, Paste), Application (Food & Beverages, Cosmetics & Personal Care, Infant Formula, Functional Nutraceuticals, Others), and Regional Analysis for 2025 - 2032

Hydrolyzed Plant Protein Market Share and Trends Analysis

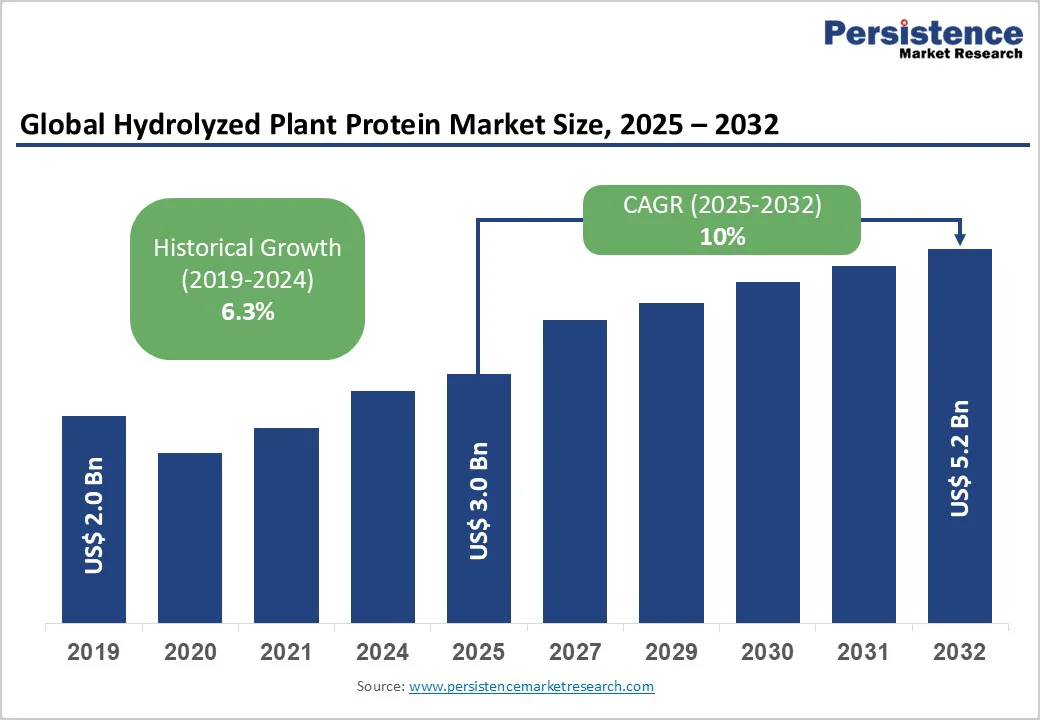

The global hydrolyzed plant protein market size is likely to be valued at US$3.0 Billion in 2025, and is estimated to reach US$5.2 Billion by 2032, growing at a CAGR of 10% during the forecast period 2025 - 2032, driven by rising consumer awareness around plant-based and allergen-free protein alternatives, increased demand for functional food ingredients, and technological advancements in enzymatic hydrolysis enhancing product taste and nutrition.

Rapid urbanization, government nutrition programs, and rising millennial and Gen Z demand for sustainable, health-focused diets are driving steady market growth, aligning with global sustainability and plant-based nutrition trends.

Key Industry Highlights

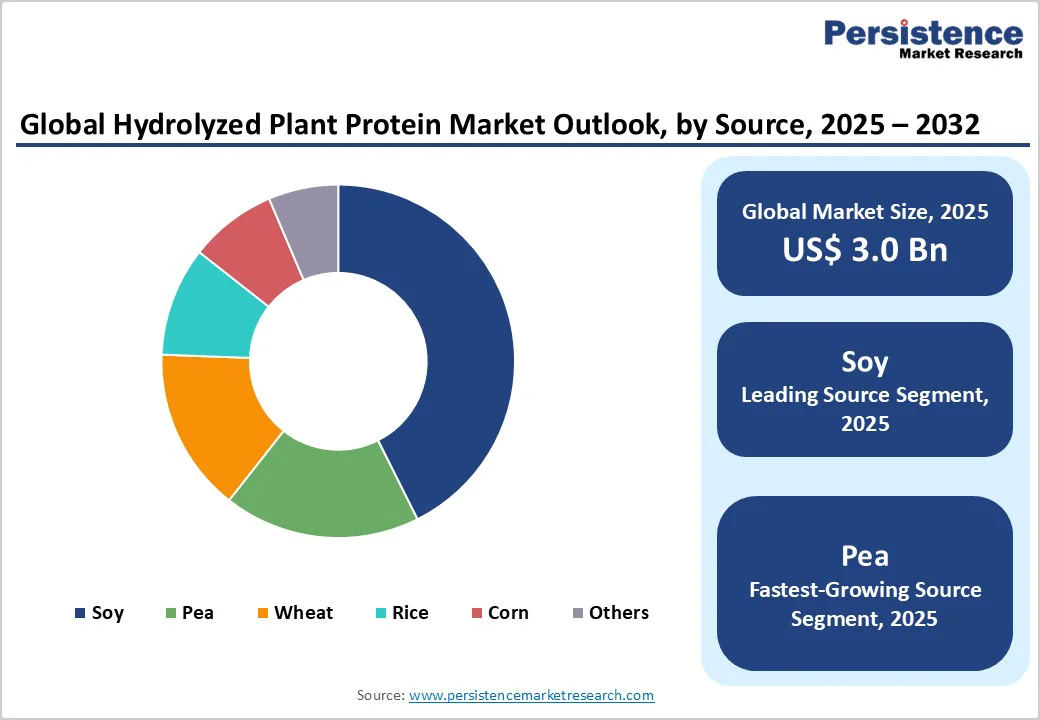

- Dominant Sources: Soy dominates with a 42.6% market share in 2025, while pea protein is the fastest-growing segment from 2025 to 2032, due to its suitability for vegan and gluten-free formulations.

- Leading Form: Powdered form holds 57.8% market revenue share in 2025, driven by its functional versatility, with liquid forms growing rapidly through 2032.

- Commanding Applications: The food & beverages segment commands 46.3% of the market revenue in 2025, with functional nutraceuticals experiencing the highest 2025 - 2032 CAGR, fueled by growing interest in performance enhancement among consumers.

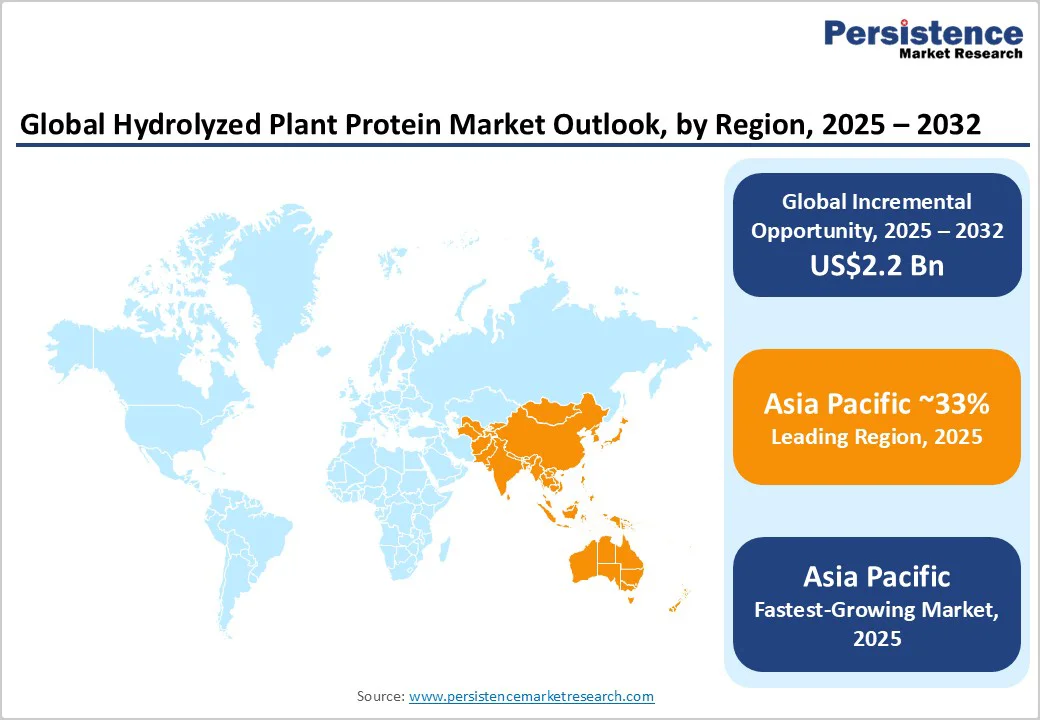

- Regional Dominance: Asia Pacific is the leading and fastest-growing regional market with 33% market share in 2025, owing to the widening implementation of government nutrition programs and massive urbanization.

- Second-largest Regional Market: North America, supported by regulatory frameworks and consumer demand.

- Industry Dynamics: Key industry developments feature major product launches, acquisitions in emerging markets, and strategic technology partnerships enhancing enzymatic hydrolysis methods.

- June 2025: Roquette expanded its Nutralys protein portfolio to include textured wheat and pea protein solutions, targeting plant-based formulations needing fibrous, meat-like textures and heartier applications such as ready meals and sauces.

| Key Insights | Details |

|---|---|

| Hydrolyzed Plant Protein Market Size (2025E) | US$3.0 Bn |

| Market Value Forecast (2032F) | US$5.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Consumer Preference for Clean-Label and Plant-Based Functional Foods

Consumer preference is steadily shifting toward clean-label and plant-based functional foods, a major driver shaping this market.

According to the Food and Agriculture Organization (FAO) and the International Food Information Council (IFIC), plant-based diets reduce exposure to allergens and support sustainable food systems, appealing strongly to health-conscious and environmentally aware demographics.

Increasing prevalence of lactose intolerance, gluten allergies, and sensitization to animal proteins is quantitatively shifting demand toward hydrolyzed plant proteins, valued for their hypoallergenic properties and superior digestibility.

Hydrolyzed plant proteins are increasingly positioned as key functional ingredients due to their enhanced solubility, flavor-masking, and nutritional benefits achieved through enzymatic hydrolysis. This refinement allows enriched inclusion in ready-to-eat meals, beverages, sports nutrition, and infant formulas, sectors witnessing compound revenue growth exceeding 8% annually.

Regulatory bodies, including the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA), are encouraging clear, transparent labeling, fostering consumer trust for clean-label products. Investment in R&D for novel enzymatic technologies continues to reduce bitterness and improve sensory profiles, accelerating product adoption and market penetration globally.

Supply Chain Vulnerabilities and Raw Material Price Volatility

One notable restraint for market expansion is supply chain fragility, particularly the volatility of raw material prices connected to crop yields and climate change-induced agricultural unpredictability.

This is compounded by rising costs for sustainable farming practices and transportation, directly impacting production expenses. Supply disruptions risk intermittent product availability, challenging manufacturers’ ability to maintain consistent quality and volume, which is critical for brand trust and regulatory compliance.

According to the United Nations Conference on Trade and Development (UNCTAD), fluctuating weather patterns and geopolitical tensions have led to frequent disturbances in supply chains and have contributed to food insecurity globally. The growing emphasis on non-GMO and organic sourcing adds further complexity and expense, as these standards limit supplier options.

Businesses in the sector must therefore adopt resilient procurement strategies, diversify sourcing bases, and invest in vertical integration to mitigate these structural challenges.

Expansion into Asia and Latin America with Nutritional Programs

A lucrative opportunity lies in tapping into emerging markets across Asia and Latin America, where government-backed nutritional enhancement programs and rising disposable incomes are driving demand for plant-based dietary supplements and fortified foods.

For example, India’s National Nutrition Mission promotes plant protein inclusion in subsidized food rations, representing a multi-billion-dollar potential segment. Market growth projections indicate Asia Pacific will register the highest CAGR through 2032, propelled by China, India, and ASEAN states that are investing heavily in food security and functional food development.

Expansion strategies that involve local partnership networks, compliance with region-specific food safety regulations, and tailored product formulations addressing regional taste and dietary needs can unlock substantial revenue growth. This opportunity brings to light the strategic importance of geographic diversification and innovation aligned with public health initiatives.

Category-wise Analysis

Source Insights

The soy segment is the clear leader for 2025, commanding an estimated 42.6% of the hydrolyzed plant protein market revenue share. This dominance is supported by the well-established supply chains, cost-effectiveness, and recognized high protein quality of soy.

Soy hydrolysates exhibit superior functional properties such as solubility, emulsification, and gelation, making them indispensable ingredients across a wide variety of food and beverage applications, including bakery, meat analogs, and protein-enriched beverages. Soy’s widespread cultivation, especially in major agricultural regions such as North America, South America, and Asia ensures a consistent supply, minimizing disruptions and keeping prices competitive.

The fastest-growing source segment throughout 2025-2032 is pea protein hydrolysate, primarily driven by the increased consumer demand for allergen-free, non-GMO protein options suitable for vegan and gluten-free diets.

Innovations in enzymatic hydrolysis are enhancing pea protein’s sensory profiles, reducing traditional bitterness, and improving digestibility, expanding its applications in infant nutrition, sports supplements, and ready-to-eat meals. The ongoing trend of diversification in protein sourcing for plant-based formulations is propelling pea protein’s rapid market penetration, with investments focused on increasing extraction efficiencies and sustainable sourcing.

Form Insights

Powdered hydrolyzed plant proteins dominate the market in 2025, with an approximate revenue share of 57.8%. Their market leadership is attributed to operational advantages such as longer shelf life, easier transportation, and broader applicability across diverse food formats.

Powders are preferred in the formulation of bakery goods, snack bars, and protein-fortified beverages due to their stability, precise dosing capabilities, and seamless integration with dry mixes. Powdered hydrolysates also align with consumer demand for clean-label formulations, allowing straightforward ingredient declarations.

The liquid form represents the fastest-growing segment during 2025 - 2032. This surge is attributable to the expanding demand for ready-to-drink (RTD) functional beverages, nutritional shakes, and liquid dietary supplements, where solubility and mouthfeel enhancements provided by hydrolyzed proteins are crucial.

Technological advancements in microencapsulation and stabilizer systems have significantly reduced common issues such as sedimentation and off-flavors in liquid formulations, enabling manufacturers to develop novel products targeting hydration, recovery, and wellness segments. The convenience of liquid protein delivery matches consumers’ fast-paced lifestyles, amplifying growth potential.

Application Insights

The food & beverages segment holds the largest share of the hydrolyzed plant protein market, accounting for approximately 46.3% in 2025. This segment is propelled by heightened consumer health awareness and the desire for natural protein enrichment in daily diets.

Hydrolyzed proteins are increasingly used as flavor enhancers, protein fortifiers, and texture improvers in bakery, meat analogs, soups, and snacks. The rising prevalence of plant-based diets and flexitarian lifestyles has expanded protein-fortified meal and beverage options, generating strong demand.

Sports nutrition and nutraceutical applications are the fastest-growing segments within the application category, with their outlook getting increasingly broadened by escalating consumer interest in performance enhancement, muscle recovery, and digestive health through clean-label plant protein supplements.

Hydrolysates provide peptides and amino acids in an easily absorbable form, making them ideal for sports drinks, protein bars, and dietary supplements aimed at athletes and active individuals. Moreover, aging populations in developed economies are driving the demand for nutraceuticals with functional benefits that support muscle maintenance and metabolic wellness, fueling the expansion of these segments.

Regional Insights

North America Hydrolyzed Plant Protein Market Trends

North America is poised to hold a substantial portion of the hydrolyzed plant protein market share in 2025. The region’s strong position is underpinned by deep-rooted consumer inclination towards plant-based diets, extensive adoption of clean-label products, and a robust innovation ecosystem.

The U.S. dominates this landscape, benefiting from favorable regulatory frameworks such as the FDA’s guidance on label transparency and GRAS status approvals, which catalyze product development and market launch momentum.

The North America market is also characterized by active collaboration between food manufacturers, ingredient suppliers, and research institutions, intensifying R&D efforts to improve protein hydrolysate taste profiles and functional performance.

Technological advancements in enzymatic hydrolysis and protein extraction methods developed here often set global benchmarks. The region’s sophisticated retail infrastructure and strong e-commerce channels facilitate efficient consumer reach. Investment opportunities abound in premium protein ingredients catering to sports nutrition, infant formula, and meal replacement sectors.

Europe Hydrolyzed Plant Protein Market Trends

In Europe, the market is buoyed by regulatory harmonization across the European Union (EU) that promotes sustainability and food safety. Germany, the U.K., France, and Spain lead market growth, with increasing plant-based diet adoption and expanding clean-label consumer segments.

European governments are actively incentivizing sustainable sourcing practices, with initiatives such as the EU Green Deal influencing ingredient supplier compliance and innovation pipelines.

A mature vegan and plant-based product consumer base supports consistent demand for high-quality hydrolyzed proteins, while stringent EU regulations on nutrition claims and allergen management create high entry barriers, favoring established players.

The European competitive landscape is marked by investments in natural ingredient development and extensive product lines addressing infant nutrition, sports supplements, and meat alternatives. The regional market is also witnessing heightened M&A activity driven by market consolidation and geographic expansion strategies.

Asia Pacific Hydrolyzed Plant Protein Market Trends

Asia Pacific emerges as the largest as well as the fastest-growing regional market for hydrolyzed plant proteins, with an estimated 33% share in 2025. Rapid urbanization, a burgeoning middle class, and government-led nutritional initiatives are primary drivers.

China, India, and ASEAN nations stand out due to ongoing investments in food processing infrastructure and growing awareness of plant protein benefits against chronic health conditions. The regional market benefits from a comparative manufacturing cost advantage and an extensive agricultural base supplying soy, pea, and wheat proteins.

National governments are actively promoting plant-protein integration within nutritional support programs targeting malnutrition and food security, synergizing with rising consumer preferences for plant-based functional foods.

Regulatory developments focusing on food safety and quality standards are progressing, facilitating harmonized market growth. Strategic partnerships between multinationals and local players to customize formulations for regional tastes are unlocking substantial growth opportunities.

Competitive Landscape

The global hydrolyzed plant protein market structure exhibits moderate concentration, with top-tier players holding approximately 45-55% of the revenue share collectively.

Leading firms such as Ajinomoto Co., Cargill Incorporated, Archer Daniels Midland Company, and DuPont Nutrition & Health dominate market dynamics through diverse product portfolios and established global distribution networks. The market is characterized by moderate consolidation, with a combination of multinational corporations and specialized regional producers competing on technological innovation, quality differentiation, and cost competitiveness.

The competitive environment rewards companies investing heavily in enzymatic hydrolysis technology advancements, sustainable sourcing, and clean-label ingredient certifications. Furthermore, agility in regional market penetration through local partnerships and acquisitions strengthens competitive positioning.

Smaller niche players focus on specialty proteins, organic certification, and novel hydrolysates, contributing to innovation diversity. Competitive strategies emphasize portfolio expansion into rapidly growing applications such as sports nutrition, infant formula, and plant-based meat substitutes.

Key Industry Developments

- In October 2025, Alpine Bio introduced a highly soluble, non-GMO soy protein isolate with whey-like functionality and developed soybean-derived lactoferrin with superior iron saturation. Targeting functional foods and beverages, the company is advancing GRAS approval and partnering to scale production and commercialization.

- In July 2025, Protein Industries Canada invested C$48.7 million (US$34.7 Million) in a pilot project with Louis Dreyfus Company and Seven Oaks Hospital’s Chronic Disease Innovation Centre to develop clean-tasting, nutritious pea protein ingredients and foods in Saskatchewan. Targeting seniors facing muscle loss and sarcopenia, the initiative supports domestic supply-chain growth, rural job creation, and expanded market opportunities. With LDC’s pea protein isolate facility opening in late 2025, efforts emphasize taste, nutrition, and digestibility for aging populations.

- In May 2025, Austrade Inc. launched non-GMO hydrolyzed sunflower lecithin powder for functional beverages. Its enzymatic process delivers HLB 9-10, enabling low-dose, neutral-flavor emulsions for plant-based creamers, nutritional drinks, protein formulas, frozen desserts, and supplements, supporting sustainable trends.

Companies Covered in Hydrolyzed Plant Protein Market

- Ajinomoto Co.

- Cargill Incorporated

- Archer Daniels Midland Company

- DuPont Nutrition & Health

- Ingredion Incorporated

- Kerry Group plc

- Tate & Lyle PLC

- Roquette Frères

- Titan Biotech Limited

- Axiom Foods Inc.

- Shandong Jianyuan Foods Co., Ltd.

- AIDP Inc.

- The Scoular Company

- Puris Proteins LLC

- Meihua Holdings Group Co., Ltd.

Frequently Asked Questions

The global hydrolyzed plant protein market is projected to reach US$3.0 Billion in 2025.

Rapid urbanization, government nutrition programs, and shifting dietary preferences among millennials and Gen Z toward sustainable and health-conscious choices are driving the market.

The hydrolyzed plant protein market is poised to witness a CAGR of 10% from 2025 to 2032.

Improving consumer awareness around plant-based and allergen-free protein alternatives, increased demand for functional food ingredients, and technological advancements in enzymatic hydrolysis, enhancing product taste and nutrition, are key market opportunities.

Ajinomoto Co., Cargill Incorporated, and Archer Daniels Midland Company are some of the top players in the hydrolyzed plant protein market.