- Executive Summary

- Global Rheumatoid Arthritis Market Snapshot, 2025 and 2032

- Market Opportunity Assessment, 2025 - 2032, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Service Adoption Analysis

- Value Chain Analysis

- Reimbursement Scenario

- Disease Epidemiology

- Regulatory Landscape

- PESTLE Analysis

- Global Rheumatoid Arthritis Market Outlook

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, 2025-2032

- Global Rheumatoid Arthritis Market Outlook: Test Type

- Historical Market Size (US$ Bn) Analysis, By Test Type, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, By Test Type, 2025-2032

- Serology Tests

- Erythrocyte Sedimentation rheumatoid arthritis (ESR)

- Rheumatoid Factor (RF)

- Anti-cyclic Citrullinated Peptide (anti-CCP)

- Antinuclear Antibody (ANA)

- Uric Acid

- Other Test

- Monitoring rheumatoid arthritis Treatment Efficiency Tests

- Salicylate Level Count

- Muscle Enzyme Test

- Creatinine Test

- Serology Tests

- Market Attractiveness Analysis: Test Type

- Global Rheumatoid Arthritis Market Outlook: End User

- Historical Market Size (US$ Bn) Analysis, By End User, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2025-2032

- Hospitals

- Diagnostic Laboratories

- Private Laboratories

- Public Laboratories

- Ambulatory Surgical Centers

- Market Attractiveness Analysis: End User

- Key Highlights

- Global Rheumatoid Arthritis Market Outlook: Region

- Historical Market Size (US$ Bn) Analysis, By Region, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2025-2032

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Rheumatoid Arthritis Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Test Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Test Type, 2025-2032

- Serology Tests

- Erythrocyte Sedimentation rheumatoid arthritis (ESR)

- Rheumatoid Factor (RF)

- Anti-cyclic Citrullinated Peptide (anti-CCP)

- Antinuclear Antibody (ANA)

- Uric Acid

- Other Test

- Monitoring rheumatoid arthritis Treatment Efficiency Tests

- Salicylate Level Count

- Muscle Enzyme Test

- Creatinine Test

- Serology Tests

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2025-2032

- Hospitals

- Diagnostic Laboratories

- Private Laboratories

- Public Laboratories

- Ambulatory Surgical Centers

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- Europe Rheumatoid Arthritis Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Test Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Test Type, 2025-2032

- Serology Tests

- Erythrocyte Sedimentation rheumatoid arthritis (ESR)

- Rheumatoid Factor (RF)

- Anti-cyclic Citrullinated Peptide (anti-CCP)

- Antinuclear Antibody (ANA)

- Uric Acid

- Other Test

- Monitoring rheumatoid arthritis Treatment Efficiency Tests

- Salicylate Level Count

- Muscle Enzyme Test

- Creatinine Test

- Serology Tests

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2025-2032

- Hospitals

- Diagnostic Laboratories

- Private Laboratories

- Public Laboratories

- Ambulatory Surgical Centers

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- East Asia Rheumatoid Arthritis Market Outlook:

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Test Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Test Type, 2025-2032

- Serology Tests

- Erythrocyte Sedimentation rheumatoid arthritis (ESR)

- Rheumatoid Factor (RF)

- Anti-cyclic Citrullinated Peptide (anti-CCP)

- Antinuclear Antibody (ANA)

- Uric Acid

- Other Test

- Monitoring rheumatoid arthritis Treatment Efficiency Tests

- Salicylate Level Count

- Muscle Enzyme Test

- Creatinine Test

- Serology Tests

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2025-2032

- Hospitals

- Diagnostic Laboratories

- Private Laboratories

- Public Laboratories

- Ambulatory Surgical Centers

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- South Asia & Oceania Rheumatoid Arthritis Market Outlook:

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Test Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Test Type, 2025-2032

- Serology Tests

- Erythrocyte Sedimentation rheumatoid arthritis (ESR)

- Rheumatoid Factor (RF)

- Anti-cyclic Citrullinated Peptide (anti-CCP)

- Antinuclear Antibody (ANA)

- Uric Acid

- Other Test

- Monitoring rheumatoid arthritis Treatment Efficiency Tests

- Salicylate Level Count

- Muscle Enzyme Test

- Creatinine Test

- Serology Tests

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2025-2032

- Hospitals

- Diagnostic Laboratories

- Private Laboratories

- Public Laboratories

- Ambulatory Surgical Centers

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- Latin America Rheumatoid Arthritis Market Outlook:

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Test Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Test Type, 2025-2032

- Serology Tests

- Erythrocyte Sedimentation rheumatoid arthritis (ESR)

- Rheumatoid Factor (RF)

- Anti-cyclic Citrullinated Peptide (anti-CCP)

- Antinuclear Antibody (ANA)

- Uric Acid

- Other Test

- Monitoring rheumatoid arthritis Treatment Efficiency Tests

- Salicylate Level Count

- Muscle Enzyme Test

- Creatinine Test

- Serology Tests

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2025-2032

- Hospitals

- Diagnostic Laboratories

- Private Laboratories

- Public Laboratories

- Ambulatory Surgical Centers

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- Middle East & Africa Rheumatoid Arthritis Market Outlook:

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Test Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Test Type, 2025-2032

- Serology Tests

- Erythrocyte Sedimentation rheumatoid arthritis (ESR)

- Rheumatoid Factor (RF)

- Anti-cyclic Citrullinated Peptide (anti-CCP)

- Antinuclear Antibody (ANA)

- Uric Acid

- Other Test

- Monitoring rheumatoid arthritis Treatment Efficiency Tests

- Salicylate Level Count

- Muscle Enzyme Test

- Creatinine Test

- Serology Tests

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2025-2032

- Hospitals

- Diagnostic Laboratories

- Private Laboratories

- Public Laboratories

- Ambulatory Surgical Centers

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Pharmaceuticals

- Rheumatoid Arthritis Market

Rheumatoid Arthritis Market Size, Share, Trends, Growth, and Regional Forecasts 2025 - 2032

Rheumatoid Arthritis Market by Test Type (Serology Tests and Monitoring rheumatoid arthritis Treatment Efficiency Tests), End-user (Hospitals, Diagnostic Laboratories, and Ambulatory Surgical Centers), and Regional Analysis for 2025 - 2032

Rheumatoid Arthritis Market Share, and Trend Analysis

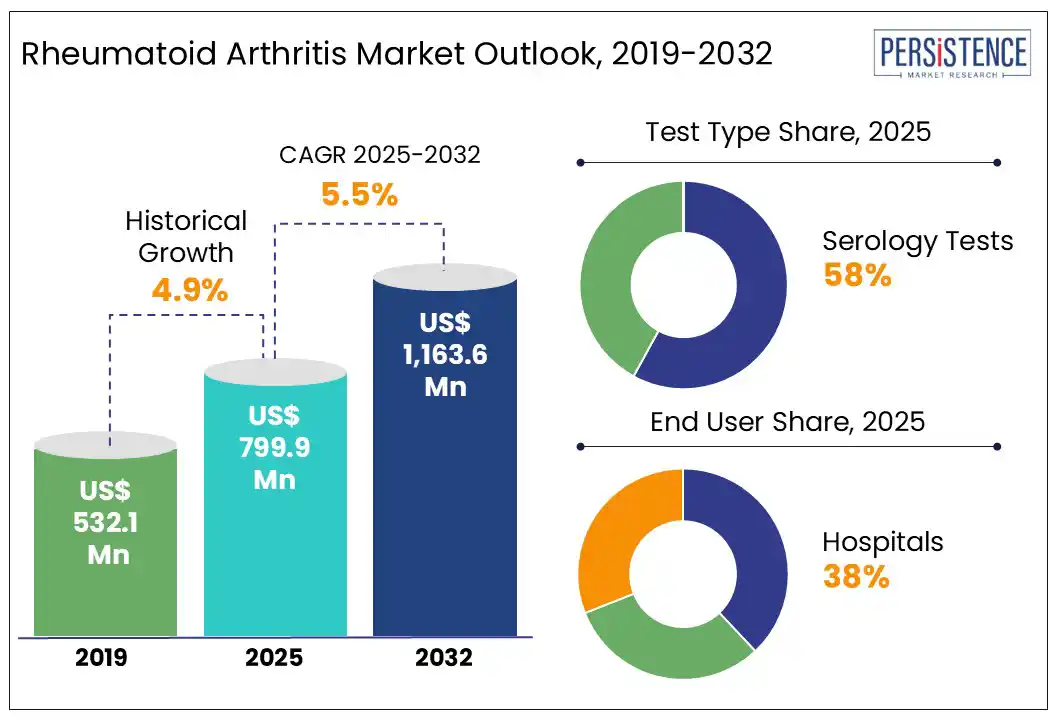

The global rheumatoid arthritis market size is likely to be valued at US$ 799.9 Mn in 2025 and is expected to reach at US$ 1,163.6 Mn by 2032, growing at a CAGR of 5.5% from 2025 to 2032.

According to Persistence Market Research report, the rheumatoid arthritis service market is evolving rapidly, driven by the need for comprehensive disease management beyond drug therapy. With rising RA prevalence and the chronic nature of the disease, demand for diagnostic services, infusion therapy, physiotherapy, telehealth, and long-term patient monitoring is surging. Service providers are focusing on integrated care models that combine in-person consultations, virtual care, and home-based services. North America leads the market due to advanced rheumatology clinics and digital health adoption, while Asia-Pacific is emerging with growing investments in outpatient and rehabilitation services. The shift toward value-based care, personalized support programs, and remote disease tracking is transforming RA services into a holistic ecosystem supporting patient outcomes, adherence, and quality of life.

Key Industry Highlights:

- High demand for biomarker-based RA testing (e.g., RF, anti-CCP antibodies) is improving diagnostic accuracy and patient stratification.

- Use of tele-rheumatology and AI-based platforms is enhancing remote diagnosis and disease monitoring.

- Growing adoption of point-of-care testing solutions for RA in outpatient and primary care settings for faster results.

- Increased use of advanced imaging technologies such as MRI and ultrasound for early joint damage detection.

- Integration of RA diagnostics into chronic care management programs is expanding diagnostic service usage.

|

Global Market Attribute |

Key Insights |

|

Rheumatoid Arthritis Market Size (2025E) |

US$ 799.9 Mn |

|

Market Value Forecast (2032F) |

US$ 1,163.6 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

4.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Dynamics

Driver - Anti-CCP antibody testing becoming gold standard

Anti-CCP antibody testing continues to solidify its role as the gold standard in rheumatoid arthritis (RA) diagnostics due to its unmatched specificity and predictive value. As of 2024, clinical guidelines globally are recommending anti-CCP testing alongside rheumatoid factor (RF) for early and accurate RA detection, particularly in patients with undifferentiated arthritis. Recent studies highlight its ability to detect RA up to a decade before symptoms appear, making it crucial for preclinical diagnosis. Moreover, growing adoption of multiplex autoantibody panels and next-generation immunoassay platforms has enhanced test efficiency, reducing turnaround time and improving accessibility. Diagnostic labs and hospitals are increasingly utilizing automated CCP testing kits approved by regulatory bodies such as the FDA and CE. In addition, ongoing research is uncovering the role of anti-CCP in treatment response prediction, further integrating it into precision medicine frameworks. With the increasing demand for early, accurate, and personalized RA care, anti-CCP testing is expected to see robust growth globally.

Restraint - Diagnostic overlap with other disorders

Diagnostic Overlap with other disorders poses a significant challenge in the rheumatoid arthritis (RA) diagnostic market. RA shares overlapping clinical manifestations, such as joint pain, stiffness, and inflammation, with other autoimmune diseases such as systemic lupus erythematosus (SLE) and psoriatic arthritis (PsA). Moreover, common biomarkers such as rheumatoid factor (RF) and antinuclear antibodies (ANA) may test positive in multiple conditions, leading to diagnostic ambiguity. This overlap often results in misclassification, delayed diagnosis, or inappropriate treatment initiation. The heterogeneity in patient presentations further complicates differential diagnosis, especially in early-stage RA. Consequently, physicians require a combination of serological tests, imaging, and clinical judgment, which increases diagnostic complexity and costs. This restraint underscores the urgent need for more disease-specific biomarkers and integrated diagnostic algorithms.

Opportunity - Clinical decision support systems (CDSS) for RA diagnosis

Clinical Decision Support Systems (CDSS) for rheumatoid arthritis (RA) diagnosis present a transformative opportunity in early disease detection and referral optimization. These intelligent platforms integrate patient-reported symptoms, lab markers such as rheumatoid factor (RF) and anti-CCP antibodies, and imaging data (e.g., X-ray or ultrasound findings) into a unified decision-making algorithm. Designed for primary care settings, CDSS tools alert general practitioners to early RA indicators and suggest timely specialist referrals before irreversible joint damage occurs. By leveraging real-time analytics, machine learning, and historical patient data, these systems minimize diagnostic delays and improve patient outcomes. The integration of CDSS into electronic health records further enhances diagnostic accuracy, reduces misclassification, and supports evidence-based care pathways for managing complex autoimmune conditions such as RA.

Category-wise Analysis

Test Type Insights

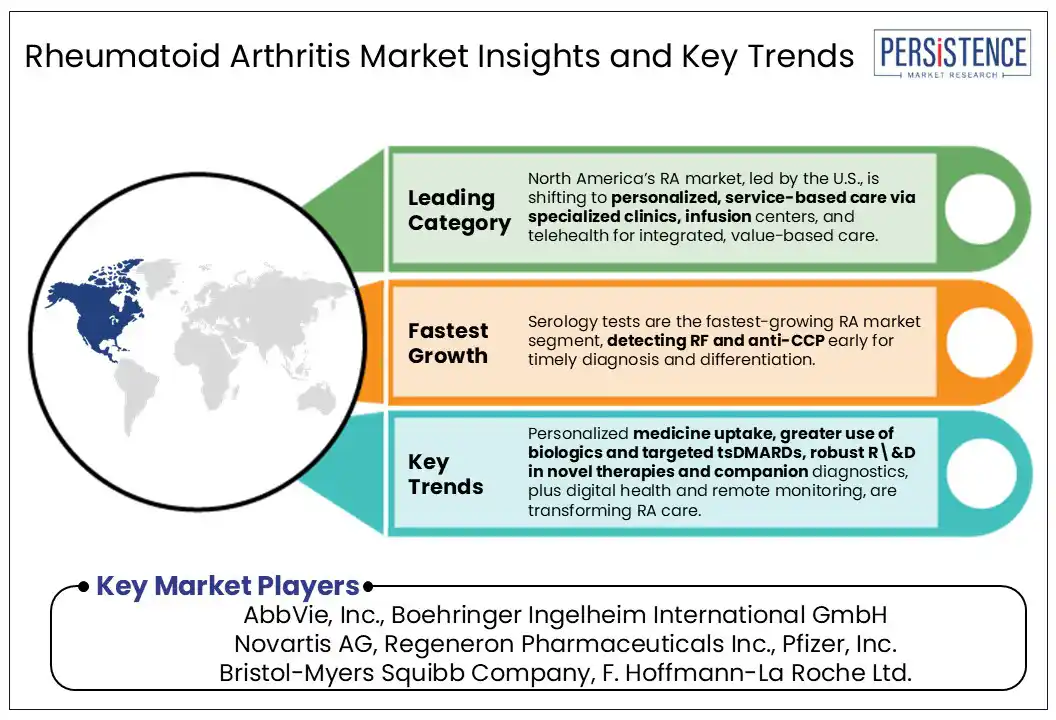

Serology account for the highest share in the test type segment of the rheumatoid arthritis (RA) market due to their critical role in early and accurate diagnosis. These tests, including rheumatoid factor (RF) and anti-cyclic citrullinated peptide (anti-CCP) antibody detection, are widely used as primary diagnostic tools to confirm autoimmune activity. Their high specificity, rapid turnaround, cost-effectiveness, and compatibility with routine laboratory workflows make them indispensable in both primary and specialist care. Additionally, serology tests are often the first line of investigation when patients present with joint pain, enabling early intervention and improved disease management. Their widespread availability and established clinical value have led to consistent adoption, securing their dominance in the RA diagnostic landscape.

End-user Insights

Hospitals dominate the end-use segment due to their integrated infrastructure, multidisciplinary care, and access to advanced biologics and infusion therapies. RA management often requires continuous monitoring, imaging, lab diagnostics, and specialist consultations all centralized in hospital settings. Moreover, biologic therapies such as TNF inhibitors and JAK inhibitors are frequently administered in infusion centers located within hospitals, reinforcing patient dependence on these facilities. In severe RA cases, hospitalization for joint surgeries or complications becomes essential, further increasing service utilization. Additionally, reimbursement policies in many countries favor hospital-based care for chronic conditions, making hospitals, a primary hub for both acute and long-term RA treatment. This convergence of advanced care and institutional support drives their leading market share.

Regional Insights and Trends

North America’s Rheumatoid Arthritis Market Trends

In North America, particularly the U.S., the rheumatoid arthritis (RA) market is witnessing a shift toward personalized, service-based care models. The rise of specialized rheumatology clinics, infusion centers, and telehealth platforms has expanded access to continuous disease management services. U.S. healthcare systems emphasize value-based care, driving integrated service delivery that combines diagnostics, biologic therapy administration, and patient education under one roof.

Approximately 18 million people globally are affected by rheumatoid arthritis, including around 1.5 million in the United States. The condition is nearly three times more prevalent in women than in men. Moreover, increasing adoption of biosimilars and home-based infusion services reflects a cost-sensitive yet patient-centric trend. The demand for remote monitoring and digital tools, supported by favorable reimbursement and private insurance policies is reshaping how RA services are delivered. These evolving service ecosystems position the U.S. as a frontrunner in transforming RA care into a holistic, service-driven market model.

Europe Rheumatoid Arthritis Market Trends

In Europe, the rheumatoid arthritis (RA) market is witnessing a significant shift toward outpatient specialty clinics and home-based infusion services, reducing dependency on traditional hospital settings. Countries such as Germany, the UK, and France are actively integrating tele-rheumatology services, enabling remote monitoring and virtual consultations. The adoption of biosimilars has surged across Europe due to stringent cost-containment policies and centralized procurement by public health systems. Furthermore, the region emphasizes early diagnosis through national screening programs, especially in Scandinavian countries. Patient registries, such as Sweden’s SRQ, enhance treatment personalization and real-world data collection. Combined with value-based care initiatives and EU-wide reimbursement reforms, Europe’s RA service model is evolving toward decentralized, cost-efficient, and technology-driven management frameworks that improve patient accessibility and outcomes.

Asia Pacific Rheumatoid Arthritis Market Trends

In Asia Pacific, the rheumatoid arthritis (RA) market is rapidly evolving, driven by expanding healthcare infrastructure, rising disease awareness, and increasing access to specialty care services in urban centers. As an emerging market, countries such as India, China, and Southeast Asia are experiencing a surge in early diagnosis and treatment, supported by government health programs and digital health platforms that extend rheumatology services to remote areas. Unlike Western regions, a significant portion of care is still delivered through public hospitals and tertiary care centers due to affordability concerns. Additionally, the growing adoption of biosimilars is reshaping treatment paradigms, making advanced therapies more accessible. Medical tourism in countries like Thailand also contributes to RA service market growth in the region.

Competitive Landscape

The rheumatoid arthritis (RA) service-based market is becoming increasingly competitive, with hospitals, specialty clinics, and telehealth providers vying for patient engagement and retention. Major healthcare networks are enhancing service delivery through integrated care pathways, digital platforms, and personalized treatment protocols. Private rheumatology centers are emerging rapidly, offering faster access to biologics and infusion therapies. Meanwhile, tele-rheumatology services are expanding, especially for follow-ups and rural outreach.

Key Industry Developments

- In September 2024, Thermo Fisher’s Phadia Laboratory Systems enhanced the precision and speed of diagnosing autoimmune diseases like rheumatoid arthritis, which had historically been difficult to diagnose accurately.

Frequently Asked Questions

The global rheumatoid arthritis market is estimated to increase from US$ 799.9 Mn in 2025 to US$ 1,163.6 Mn in 2032.

The global rheumatoid arthritis market is primarily propelled by the rapidly rising prevalence of the disease, now affecting millions worldwide, as populations age and lifestyle risk factors increase.

The market is projected to record a CAGR of 5.5% during the forecast period from 2025 to 2032.

The rheumatoid arthritis drug market is experiencing growth, with increasing prevalence of arthritis, obesity, and unhealthy lifestyles driving demand.

Serology accounts for the highest share in the test type segment of the rheumatoid arthritis market due to its critical role in early and accurate diagnosis.