- Metalworking & Fabrication

- Welding Equipment Market

Welding Equipment Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Welding Equipment Market by Equipment Type (MIG Welders, TIG Welders, Stick Welders, Plasma Arc Welding Machines, Laser Beam Welding Machines, Oxy-Fuel Welding Machines / Equipment, Resistance Welding Machines), Technology (Arc Welding, Resistance Welding, Laser Beam Welding, Oxy-Fuel Welding), Operation Mode (Automatic, Semi-Automatic, Manual) Industry (Automotive, Aerospace, Building & Construction, Power & Energy, Oil & Gas, Marine) and Regional Analysis for 20262033

Welding Equipment Market Size and Trends Analysis

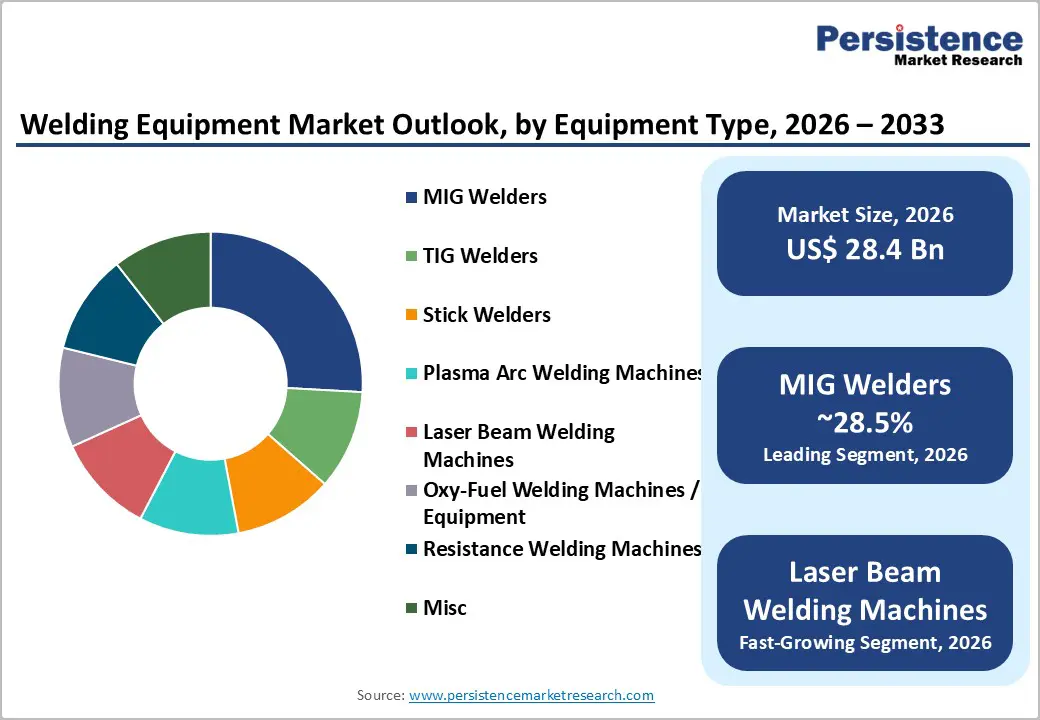

The global welding equipment market size is likely to be valued at US$ 28.4 billion in 2026 and is projected to reach US$ 44.2 billion by 2033, exhibiting a CAGR of 6.5% between 2026 and 2033.

The market's upward trajectory is underpinned by sustained automotive production, infrastructure modernisation across developed and developing economies, and the accelerated adoption of automation technologies within fabrication processes. Industrial output in key manufacturing nations continues to necessitate reliable joining solutions, while technological advancements in laser welding and digital monitoring systems are transforming traditional welding operations into precision-driven, data-enabled workflows.

Key Industry Highlights:

- Regional Leadership: East Asia leads the global Welding Equipment market with 38.4% share, supported by China’s automotive scale, dominant shipbuilding capacity, and sustained industrial automation investments.

- Europe Market Scenario: Europe captures 18% share, driven by mature automotive clusters, high-spec aerospace requirements, and energy-efficient welding power source regulations under EU ecodesign norms.

- Leading Equipment: MIG Welding Machines dominate with 28.5% share, reflecting broad adoption across automotive, fabrication, construction, and general-purpose industrial applications.

- Fastest-Growing Equipment: Laser Beam Welding Systems are the fastest-growing, propelled by precision electronics assembly, and high-speed digital manufacturing integration.

- Leading Industry: Automotive remains the largest end-use sector with 30.4% share, supported by BIW spot welding, chassis fabrication, and rising adoption of laser welding for tailored blanks.

| Key Insights | Details |

|---|---|

|

Welding Equipment Market Size (2026E) |

US$ 28.4 Bn |

|

Market Value Forecast (2033F) |

US$ 44.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

Market Dynamics

Drivers - Infrastructure Modernization and Transportation Network Development

Infrastructure investment represents a fundamental catalyst for the Welding Equipment Market, with construction projects requiring extensive metal fabrication for structural components, bridges, pipelines, and transportation systems.

According to the American Society of Civil Engineers' 2024 Bridging the Gap study, achieving infrastructure state of good repair across 11 categories requires $9.1 trillion in investment from 2024 to 2033, with public and private funding projected at $5.4 trillion if recent federal investment levels persist. The 2021 Infrastructure Investment and Jobs Act has catalysed project activity, with federal, state, and local governments spending $626 billion on transportation and water infrastructure in 2023 per Congressional Budget Office data.

In India, the PM GatiShakti initiative has expanded National Highways by 60 percent to 146,204 km, with construction pace accelerating from 11.6 km/day to 34 km/day, while landmark projects like the Delhi-Mumbai Expressway and Bogibeel Bridge demonstrate the scale of metalwork and welding operations supporting national connectivity goals.

European transport infrastructure density correlates with economic activity, with motorway expansions in Spain, Slovakia, Czechia, Romania, and Bulgaria during 2013-2023 requiring sustained welding equipment deployment for bridge construction, rail electrification projects covering 45,000 Rkm, and port capacity doubling to 2,762 MMTPA in India's Sagarmala program.

These infrastructure initiatives generate sustained demand within the Welding Equipment Market as contractors require reliable, high-capacity welding systems for joining structural steel, reinforcing components, and fabricating specialised assemblies across highway, railway, airport, and port development projects.

Technological Integration of Artificial Intelligence and IoT-Enabled Automation

Modern welding systems increasingly incorporate artificial intelligence, real-time sensor feedback, and Internet of Things connectivity, enabling autonomous parameter adjustment, predictive quality assurance, and digitalised production tracking. Smart welding machines equipped with advanced control systems automatically calibrate voltage, current, and wire feed speed based on continuous arc feedback, reducing defects and material waste while simultaneously enhancing operator safety through automated hazard detection.

Recent product launches exemplify this technological trajectory such as Miller Electric's ArcCapture™ weld camera systems, which deliver high-definition real-time visualization enabling remote observation and robotic system integration, Lincoln Electric's Flex Lase® Handheld Laser Welding System, which achieves four times the welding speed of conventional TIG processes while minimizing material distortion; and Fronius International's advanced MIG/MAG systems emphasize digitalization and precision control.

Restraint - High Initial Capital Investment and Operational Complexity

Advanced welding systems, particularly laser beam welding machines and automated robotic welding cells, require substantial upfront capital expenditure that can constrain adoption among small and medium-sized fabricators. Industrial-grade laser welding systems command prices exceeding several hundred thousand dollars, while fully configured robotic welding cells with material handling integration can surpass million-dollar investments.

Beyond equipment acquisition, facilities must invest in operator training, maintenance infrastructure, and safety systems, creating financial barriers for enterprises operating on limited capital budgets. Operational complexity further compounds adoption challenges, as laser welding and advanced automation require specialized technical personnel capable of programming weld parameters, managing CAD/CAM integration, and troubleshooting sophisticated control systems skill sets that remain scarce in many regional labor markets, particularly in developing economies where technical education infrastructure may lag industrial modernisation.

Opportunity - Advanced Materials Processing and Energy Transition Applications

The transition toward renewable energy infrastructure and lightweight materials in transportation sectors creates specialized welding requirements that drive demand for advanced equipment technologies. Vehicle battery pack assembly necessitates precise laser welding for aluminium and copper busbars connecting battery cells with thermal management requirements demanding minimal heat input to prevent cell degradation.

Wind turbine manufacturing requires high-deposition welding processes for tower fabrication, with sections reaching 100 plus meters requiring specialised submerged arc welding equipment capable of handling thick-section steel components. Solar panel frame manufacturing employs automated MIG welding for aluminium extrusion joining, while hydrogen storage vessel production demands TIG welding certification for stainless steel and composite-overwrapped pressure vessels.

Shunpu's January 2026 introduction of pulse welding technology reduces heat input, minimises deformation, and improves joint strength for precision electronic components, emphasising green and energy-efficient designs aligned with environmental sustainability. Lincoln Electric's September 2025 Flex Lase Handheld Laser Welding System offers 2kW capability for high-precision welding up to four times faster than traditional TIG processes, supporting stainless steel, carbon steel, and aluminium with minimal distortion.

These technological advancements position the Welding Equipment Market to capitalise on materials science evolution as industries adopt advanced high-strength steels, aluminium-lithium alloys, and titanium aluminides that require sophisticated welding parameters, real-time quality monitoring, and process control capabilities that next-generation equipment provides for emerging applications across energy, transportation, and advanced manufacturing sectors.

Emerging Market Industrial Development and Localisation Strategies

Rapid industrialisation in developing economies, coupled with government policies promoting domestic manufacturing capabilities, generates significant growth potential for the Welding Equipment Market.

India's defence sector transformation exemplifies this trend, with the Uttar Pradesh Defence Industrial Corridor and Tamil Nadu Defence Industrial Corridor attracting 9,145 crore in investments and unlocking 66,423 crore in potential opportunities. The government issued 788 industrial licenses to 462 companies in FY 2024-25, while the Ministry of Defence signed 193 contracts valued at 2,09,050 crore, with 177 contracts worth 1,68,922 crore awarded to the domestic industry, reinforcing indigenous production priorities.

Voestalpine Böhler Welding's February 2025 investment of over EUR 3 million in India for local welding consumables production and application technology demonstrates how global suppliers are establishing manufacturing presence to support "local for local" strategies. The company's January 2025 expansion across Bhiwadi, Thane/Mumbai, and Delhi locations added solid wire production capacity while enhancing its full-range welding solutions portfolio

Favorable FDI policies, production-linked incentive schemes, and infrastructure corridor development create conducive environments for welding equipment manufacturers to establish regional production hubs that serve both domestic demand and export markets. India's aerospace and defence sector recorded over $463 million in FDI inflows by mid-2020, while targets of achieving 70 percent self-reliance in weaponry by 2027 provides long-term growth visibility.

The Indian civil aviation sector's Vande Bharat Mission facilitated international travel recovery, while the 2020-21 defence budget of $67.4 billion, with lifted expenditure restrictions, accelerates procurement processes. MSMEs are expected to double to 16,000 by 2026, integrating into global supply chains and requiring welding equipment for precision manufacturing, further expanding the addressable market within the Welding Equipment Market as localisation policies drive domestic production capability development across multiple industrial sectors.

Category-wise Analysis

Equipment Type Insights

MIG (Metal Inert Gas) welders command the largest market share at 28.5% in 2026, reflecting their versatility across automotive, construction, and fabrication applications. Miller Electric's September 2024 launch of the XMT 400 ArcReach multiprocess welder demonstrates continued innovation in this segment, featuring ArcReach remote control technology,

Auto-Line, and Cable Length Compensation while remaining the lightest and smallest in its amperage class. The system supports TIG, flux-cored, stick, and gouging processes, enabling operators to work efficiently across diverse applications. Fronius International's April 2025 unveiling of next-level manual MIG/MAG welding systems emphasized digitalization, ease of use, and safety with fume extraction systems, ergonomic torches, and digital welding monitoring to reduce errors and save materials

Laser beam welding machines represent the fastest-growing segment, driven by automotive lightweighting initiatives, electronics miniaturisation, and precision manufacturing requirements. Lincoln Electric's September 2025 launch of the Flex Lase Handheld Laser Welding System exemplifies segment innovation, delivering 2kW capability for welding speeds up to four times faster than traditional TIG processes with autogenous and wire-fed modes for stainless steel, carbon steel, and aluminium.

The system integrates advanced safety features and versatile accessories for industrial applications while offering improved productivity and minimal distortion. Shunpu's January 2026 introduction of pulse welding technology demonstrates the segment's evolution toward reduced heat input and improved joint strength for precision electronic components.

Industry Insights

The automotive sector maintains a dominant position with 30.4% market share in 2026, reflecting the industry's intensive welding requirements across vehicle assembly operations. Global car sales of 74.6 million units in 2024, with manufacturing output reaching 75.5 million units, demonstrate the scale of production activity requiring welding equipment. U.S. market's 3.1% growth to 12.7 million units sustains North American equipment deployment. The International Organisation of Motor Vehicle Manufacturers' data showing over 77 million units produced in 2021 establishes the automotive sector's sustained volume base.

Commercial vehicle markets contribute additional demand, with North America maintaining 4 million units representing 30 percent global share and Europe posting 5.7 percent growth to 2.5 million units in 2024. The segment's welding applications span resistance spot welding for body-in-white assembly, accounting for thousands of spot welds per vehicle, MIG welding for chassis and suspension components, laser welding for roof seam joining and tailored blank fabrication, and arc welding for commercial vehicle frame construction, maintaining automotive's position as the largest end-use segment.

The aerospace sector experiences accelerating welding equipment demand driven by commercial aircraft production recovery, defense modernization investments, and structural complexity expansion in advanced aircraft programs.

Regional Insights and Trends

North America Welding Equipment Market Trends

North America commands approximately 20% substantial welding equipment market influence through advanced manufacturing infrastructure, technology leadership, and stringent quality/safety regulatory environments. The United States dominates regional positioning as the world's second-largest automotive market, with 2024 production reaching 12.7 million units, combined with significant aerospace manufacturing capacity centered in Southern California, Seattle, and Wichita.

Manufacturing sector concentration in industrial automation, precision fabrication, and contract manufacturing drives consistent premium equipment demand, particularly for advanced technologies including robotic systems and laser welding platforms. Safety regulations established by OSHA, combined with industry standards promulgated by the American Welding Society (AWS), maintain high compliance burdens that incentivise adoption of advanced safety-integrated systems, portable monitoring devices, and ergonomic equipment designs.

Investment in infrastructure modernisation under US government capital programs creates cyclical demand waves across fabrication shops, shipbuilding facilities, and industrial maintenance operations. North American manufacturers lead equipment innovation, with Lincoln Electric, Miller Electric, and ESAB headquartered in the region, establishing competitive advantages through local customer proximity, rapid product development cycles, and integration of AI/IoT technologies into welding systems.

East Asia Welding Equipment Market Trends

East Asia dominates the global welding equipment market with 38.4% share, through unparalleled manufacturing scale, infrastructure investment ambition, and industrial sector diversity. China commands singular importance as the world's largest automotive manufacturer, producing 23 million vehicles in 2024, combined with approximately 7 million electric vehicles and dominant positions in shipbuilding, capturing approximately 38 percent of global orders, steel production, and heavy equipment manufacturing. Government initiatives emphasising "Made in China 2025" manufacturing excellence, coupled with a strategic focus on advanced technology adoption and industrial automation, create structural demand for precision welding systems.

Japanese and South Korean manufacturers, including Panasonic, Daihen, and Hyundai Welding, maintain technological leadership in robotic systems and specialised welding solutions, establishing East Asia as the innovation epicentre.

Regional infrastructure intensity India's National Infrastructure Pipeline targeting US$1.4 trillion through 2025, combined with China's continued urbanisation and industrial modernization generates sustained welding system demand across construction, transportation, and heavy industrial sectors.

Europe Welding Equipment Market Trends

Europe accounts for approximately 18% of the global welding equipment market. Europe maintains strategic market positioning through mature manufacturing infrastructure, stringent regulatory environments, and specialisation in advanced technology applications. The European Union produced 10.6 million vehicle units in 2024 with modest 0.8 percent growth, reflecting market maturity and competition from Asian manufacturers.

Automotive manufacturing concentration in Germany, France, and Italy, combined with significant aerospace/defence capabilities in France, the UK, and Italy, establishes sophisticated demand for precision equipment and advanced joining technologies. European aeronautical production achieved 4.7 percent growth in 2024, supported by commercial aviation recovery and sustained defence investments following geopolitical developments.

Regulatory frameworks establishing stringent environmental compliance requirements, particularly ecodesign regulations effective January 2023, mandating minimum efficiency standards for welding equipment power sources, drive equipment technology upgrades and adoption of energy-efficient systems.

Competitive Landscape

The global welding equipment market is moderately consolidated, with a few major players holding significant share while numerous smaller and regional manufacturers operate alongside them. Leading companies such as The Lincoln Electric Company, Miller Electric Mfg. LLC, Ador Welding Limited, voestalpine Böhler Welding Group GmbH, Carl Cloos Schweisstechnik GmbH, and OTC DAIHEN Inc. dominate through advanced technologies, diverse product portfolios, and strong global distribution networks.

Competition is driven by product innovation, reliability, automation integration, and technical support rather than price alone. While North America and Europe are led by established multinationals, the Asia-Pacific features rising local and cost-competitive players. Mid-tier companies like ACRO Automation Systems and Mitco Weld Products contribute to niche applications and specialised solutions.

Key Developments:

- In September 2025 Lincoln Electric launched the Flex Lase® Handheld Laser Welding System, a 2kW solution designed for high-precision, fast welding up to four times quicker than traditional TIG processes. The system supports autogenous and wire-fed welding on stainless steel, carbon steel, and aluminium, offering improved productivity, ease of use, and minimal distortion, while integrating advanced safety features and versatile accessories for industrial applications.

- In August 2025, voestalpine Böhler Welding unveiled the CORE series for MMA welding, a new generation of portable welding machines designed for light fabrication, construction, and repair applications. The CORE series emphasizes reliability and performance in diverse environments, including shop floors, on-site locations, and extreme outdoor conditions, reflecting decades of welding expertise in a single unit.

Companies Covered in Welding Equipment Market

- The Lincoln Electric Company

- ACRO Automation Systems, Inc

- Miller Electric Mfg. LLC

- Ador Welding Limited

- Mitco Weld Products Pvt. Ltd.

- voestalpine Böhler Welding Group GmbH

- Carl Cloos Schweisstechnik GmbH

- OTC DAIHEN Inc.

- Illinois Tool Works Inc.

- Panasonic Industry Co., Ltd.

- Coherent, Inc.

- ESAB

- Polysoude S.A.S.

- Kemppi Oy.

Frequently Asked Questions

The Global Welding Equipment Market is projected to be valued at US$ 28.4 Bn in 2026.

The MIG Welders (Gas Metal Arc Welding) segment is expected to account for approximately 28.5% of the Global Welding Equipment Market by Equipment Type in 2026.

The market is expected to witness a CAGR of 6.5% from 2026 to 2033.

Infrastructure modernisation across transportation and energy networks, combined with AI- and IoT-enabled smart welding automation that boosts productivity, quality, and labour efficiency, is the primary driver of Welding Equipment Market growth.

Key market opportunities lie in advanced materials and energy-transition applications in batteries and renewables, along with rapid industrialisation and localisation strategies in emerging economies that boost domestic manufacturing and welding equipment adoption.

Key players in the Welding Equipment Market include The Lincoln Electric Company, Miller Electric Mfg. LLC, Ador Welding Limited, voestalpine Böhler Welding Group GmbH, Carl Cloos Schweisstechnik GmbH, and OTC DAIHEN Inc