- Sensors & Controls

- Welding Robotics Market

Welding Robotics Market Trends, Size, Share, and Growth Forecast, 2025 - 2032

Welding Robotics Market by Function Type (Arc, Spot, MIG/TIG, Laser, Others), Payload Capacity (Low (6-22 kg), Medium (30-60 kg), High (80-300kg)), End-user (Automotive, Aerospace & Defense, Construction, Mining, Oil & Gas, Electrical & Electronics, Others), and Regional Analysis for 2025 - 2032

Welding Robotics Market Size and Trends Analysis

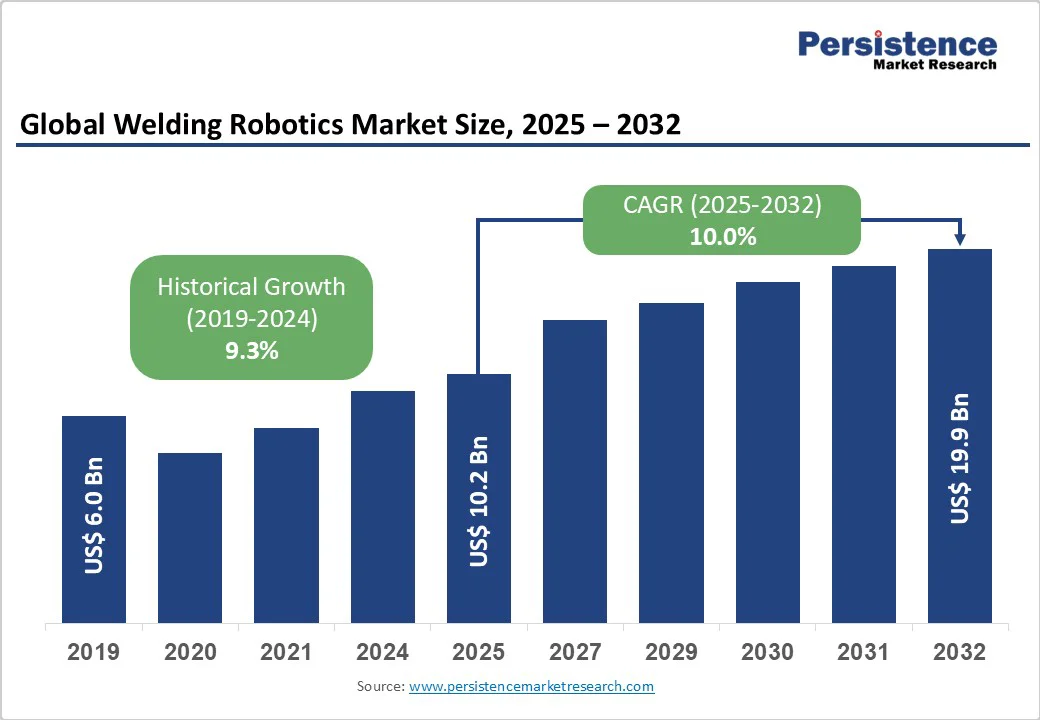

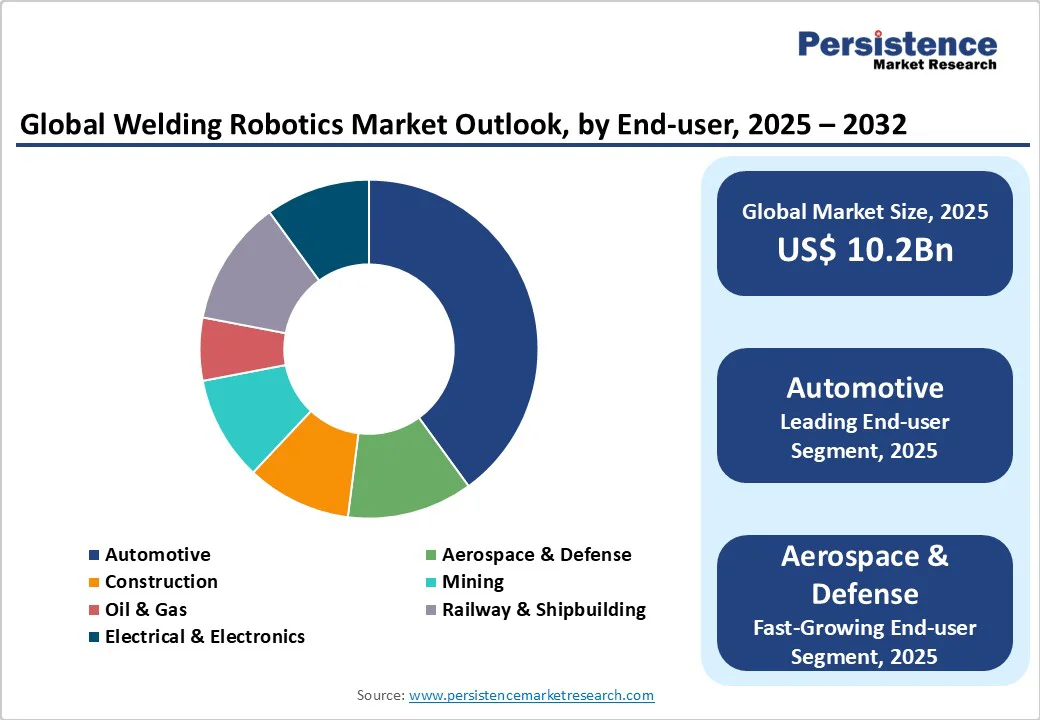

The global welding robotics market size is likely to be valued at US$10.2 Bn in 2025 and expected to reach US$19.9 Bn by 2032, registering a robust CAGR of 10.0% during the forecast period from 2025 to 2032, fueled by the increasing demand for automation in manufacturing, advancements in robotic technologies, and a global push toward enhancing production efficiency and quality.

Key Industry Highlights:

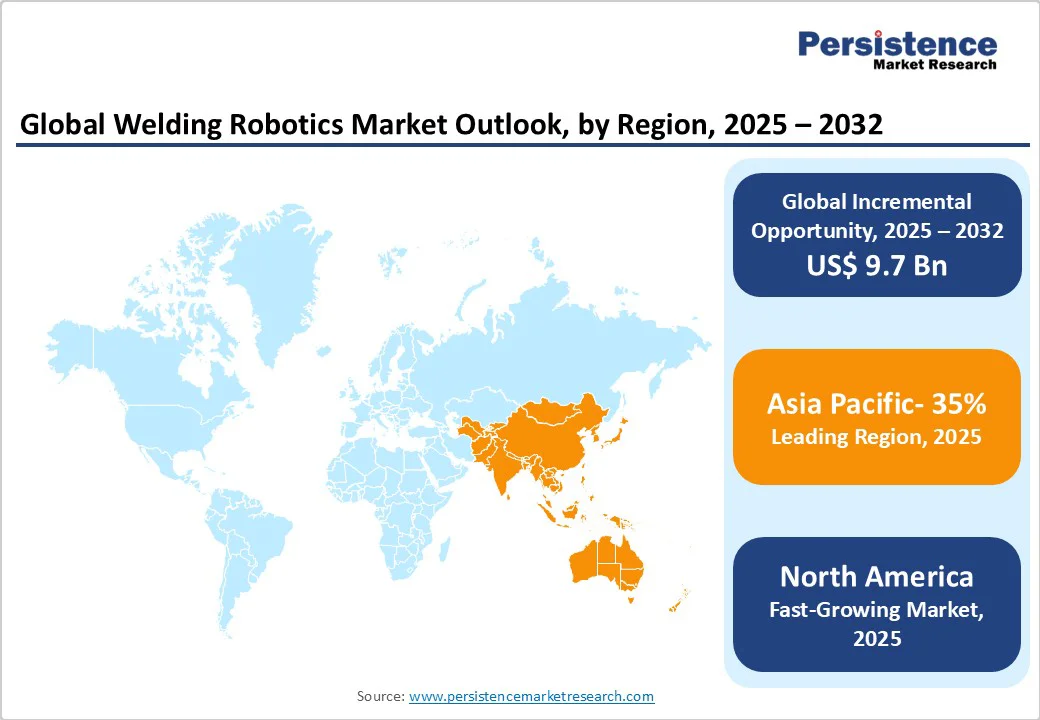

- Leading Region: Asia Pacific is likely to account for a 35% share in 2025, driven by advanced manufacturing infrastructure, widespread adoption of innovative robotics, and significant investments in automation research.

- Fastest-growing Region: North America, propelled by increasing prevalence of industrial automation, technological advancements, and expanding manufacturing access in countries such as the United States and Canada.

- Dominant Function Type: Spot accounts for approximately 26.4% of the welding robotics share in 2025, owing to its critical role in high-volume assembly and advancements in precision designs.

- Leading End-user: Automotive with a 40% share, reflecting its critical role in vehicle production and assembly procedures.

| Key Insights | Details |

|---|---|

| Welding Robotics Market Size (2025E) | US$10.2 Bn |

| Market Value Forecast (2032F) | US$19.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 9.3% |

Market Dynamics

Driver - Rising Demand for Automation in Manufacturing Amid Increasing Industry 4.0 Adoption

The global demand for automation in manufacturing is a major driver of the welding robotics market. Industrial robot installations are steadily increasing worldwide, driven by the adoption of advanced technologies that enable precise welding, crucial for productivity and consistent quality in a wide range of industries. This momentum is reinforced by Industry 4.0 initiatives, where manufacturers are increasingly integrating smart systems to enhance efficiency and streamline production processes.

Rise in labor-related challenges and the need for reliable, scalable solutions are further boosting the role of welding robotics as a key pillar of modern manufacturing. Governments and private players are investing significantly in robotic infrastructure, with China emerging as a leader in advanced welding applications for automotive and electronics manufacturing. In North America, initiatives such as the Advanced Manufacturing Partnership are expanding the use of digital and automated solutions to strengthen competitiveness.

The manufacturing sector, accounting for a large share of industrial expenditure, is turning to welding robotics to address workforce shortages and quality constraints. In the Asia Pacific, young demographics and rapid industrialization are fueling demand for spot and arc welding robots, while research in AI-enabled robotics is creating more advanced, adaptive systems.

Industries such as automotive and aerospace are deploying welding robots to achieve higher consistency, shorter cycle times, and compliance with stringent quality standards. These advances not only address immediate labor gaps but also enable scalable, flexible production, fostering long-term resilience against supply chain disruptions and positioning welding robotics as a cornerstone of next-generation manufacturing.

Restraint - High Costs of Installation and Stringent Regulatory Compliance

High costs associated with welding robotics installations present a significant barrier to market growth. The overall expense typically covers the purchase of the robot, system integration, programming, and ongoing maintenance, which collectively make adoption challenging for small and medium-sized enterprises. Unlike large corporations, SMEs often operate with tighter budgets, limiting their ability to invest in advanced automation despite its long-term benefits in productivity and quality.

Beyond financial constraints, the industry also faces hurdles due to stringent regulatory requirements. Standards set by organizations such as OSHA in the United States and ISO in Europe demand rigorous compliance, which adds to both the time and expense of deploying new robotic systems.

Ensuring workplace safety, obtaining certifications, and adhering to regional guidelines often delay the introduction of innovative solutions, restricting scalability and slowing adoption. These challenges are even more pronounced in developing regions where regulatory frameworks are still evolving, further hindering widespread adoption of welding robotics across industries.

Opportunity - Innovation in Laser and Plasma Technologies and Government Initiatives for Automation

Innovations in laser and plasma welding robots, especially advanced hybrid systems that integrate artificial intelligence with sensor fusion, are creating strong growth opportunities in the welding robotics market. These next-generation solutions deliver superior precision, faster processing, and reduced heat distortion, making them highly attractive to industries such as automotive, aerospace, and electronics where accuracy and efficiency are critical. By enabling consistent quality with minimal rework, these technologies significantly enhance production scalability and cost-effectiveness.

At the same time, government-led automation initiatives are fueling adoption across major regions. In Asia Pacific, programs such as “Made in China 2025” are prioritizing robotics and smart manufacturing, providing subsidies and favorable policies that encourage industries to transition toward advanced welding solutions.

Similarly, in North America, the Manufacturing USA initiative promotes robotics adoption through funding, incentives, and workforce training, helping manufacturers overcome cost and skill barriers. These initiatives not only accelerate the adoption of robotic welding systems but also strengthen competitiveness, foster innovation, and support long-term industrial modernization. Collectively, technological breakthroughs and supportive policies are set to reshape the welding robotics landscape, opening new opportunities for both established manufacturers and emerging players.

Segmental Insights

Function Type Insights

The welding robotics market is segmented into arc, spot, MIG/TIG, laser, and others. Spot dominates, holding approximately 26.4% of market share in 2025, due to its proven efficacy in high-volume joining, high precision, and integration into standard assembly protocols.

Spot is widely used in automotive production, offering strong bonds that reduce defects. For example, automotive manufacturers such as Toyota and Volkswagen rely on spot welding robots for chassis assembly, achieving cycle times under 10 seconds per weld.

Laser is the fastest-growing segment, driven by increasing demand for high-precision solutions in aerospace environments. Laser provides versatile deployment as advanced options, with advancements in fiber laser technology and durability making them suitable for long-term use in complex populations. For instance, aerospace firms in the U.S. and Europe opt for laser robots due to their ability to weld thin materials with minimal distortion.

Payload Capacity Insights

The welding robotics market is segmented into low (6-22 kg), medium (30-60 kg), and high (80-300kg). High (80-300kg) dominates, holding approximately 28% of market share in 2025, due to its balance of strength and capacity, robust handling capabilities, and integration into heavy-duty regimens. High payload is widely used in large-scale manufacturing, offering reliability that reduces downtime. For example, heavy machinery producers such as Caterpillar use high-payload robots for welding large steel frames.

Medium (30-60 kg) is the fastest-growing segment, driven by increasing demand for versatile applications in electronics. Medium provides optimal mobility as efficient solutions, with advancements in compact designs and control systems making them suitable for long-term use in mid-scale populations. For instance, electronics manufacturers in Asia adopt medium-payload robots for precise circuit board welding.

End-user Insights

The welding robotics market is segmented into automotive, aerospace & defense, construction, mining, oil & gas, railway & shipbuilding, electrical & electronics, and others. Automotive dominates, holding approximately 40% of market share in 2025, due to its proven efficacy in assembly lines, capacity support, and integration into production protocols. Automotive is widely used in vehicle manufacturing, offering efficiency boosts that reduce costs.

Aerospace & Defense is the fastest-growing segment, driven by increasing demand for secure and precise joining in military operations. These applications provide reliable systems as adjunct solutions, with advancements in rugged designs and automation making them suitable for long-term use in strategic populations. For instance, defense contractors such as Lockheed Martin use robotic welding for aircraft fuselages.

Regional Insights

North America Welding Robotics Market Trends

North America is emerging as the fastest-growing region in the global welding robotics market, fueled by a strong manufacturing ecosystem, substantial infrastructure investments, and a culture centered on innovation and efficiency.

The United States dominates this regional growth, with industries rapidly embracing collaborative robots and AI-driven systems that enable predictive maintenance and improved process reliability. Rising labor costs and the growing need for consistent, high-quality output are pushing manufacturers to adopt welding robotics as a cost-effective solution that ensures efficiency while reducing operational risks.

The accelerating electric vehicle industry is another major driver, supported by favorable policies and government incentives that encourage automation across automotive and related sectors. Furthermore, the integration of 5G-enabled robots into modern factories is transforming production capabilities by enabling real-time monitoring, predictive analytics, and faster decision-making.

These advances are particularly evident in automotive hubs such as Detroit and technology-driven regions such as Silicon Valley. With its focus on digital transformation and supply chain resilience, North America is positioned to secure a significant global market share.

Europe Welding Robotics Market Trends

Europe holds a substantial share of the global welding robotics market, led by countries such as the United Kingdom, Germany, and France. In the UK, industrial revival and government-backed automation initiatives are fueling adoption, with rising installations supported by a growing export market.

Germany, known for its engineering expertise and advanced manufacturing base, continues to drive innovation in welding robotics, supported by EU regulations that emphasize technological advancement and safety standards. Cities such as Stuttgart and Munich have become hubs for integrating cutting-edge solutions, with laser welding technologies gaining strong traction across industries.

France also plays a key role, with its focus on boosting manufacturing competitiveness and promoting sustainable practices. Subsidies for green technologies are encouraging adoption, particularly in arc welding applications, while Paris-based companies are developing eco-friendly robotic systems tailored for industries such as shipbuilding. Together, these countries illustrate how Europe’s advanced infrastructure, regulatory support, and industrial heritage solidify its strong position in the welding robotics market.

Asia Pacific Welding Robotics Market Trends

Asia Pacific dominates the global welding robotics market, expected to account for 38% of market share in 2025, led by China, India, and Japan. China remains at the forefront through its “Made in China 2025” initiative, which emphasizes smart manufacturing and technology exports.

Cities such as Shanghai are key hubs, where factories employ large-scale robotic welding systems to support the automotive sector and other high-volume industries. India is also emerging as a strong growth engine, fueled by its automation boom and increasing investments in cost-effective robotic solutions.

With a skilled workforce and rising industrial demand, technology hubs such as Pune and Bangalore are fostering adoption across automotive, electronics, and heavy industries. Japan, recognized globally for its expertise in precision engineering and robotics, continues to expand its role in advanced manufacturing. Supported by state-backed initiatives, Japanese firms in cities such as Tokyo and Osaka are pioneering welding robotics applications in electronics and aerospace, reinforcing Asia Pacific’s leadership in the global market.

Competitive Landscape

The global welding robotics market is highly competitive, with leading international and regional players focusing on innovation, precision, and operational efficiency to expand their presence. Rising demand for automated welding solutions in automotive, aerospace, and electronics sectors has intensified competition.

Companies are leveraging strategic partnerships, mergers, acquisitions, and advanced technologies such as AI and collaborative robots. Compliance with safety standards and quality certifications remains a key differentiator driving market leadership.

Key Developments

- June 2025: ABB expanded its large industrial robot portfolio by launching the IRB 6730S, IRB 6750S and IRB 6760 models, powered by its OmniCore™ controller platform. These robots deliver class-leading performance and sustainability, offering precise path accuracy (around 0.9 mm) and modular designs that help reduce the total cost of ownership.

- April 2025: KUKA introduced new variants in its KR FORTEC ultra robot family tailored to friction stir welding applications. These models feature enhanced rigidity, greater process force, and extended reach (up to ~3,400 mm), improving working range and accuracy in demanding e-mobility, battery, and aerospace sectors.

Companies Covered in Welding Robotics Market

- FANUC Corporation

- Kuka AG

- Kemppi Oy

- Yaskawa America

- ABB

- Panasonic Corporation

- OTC DAIHEN Inc.

- DENSO CORPORATION

- Kawasaki Heavy Industries, Ltd.

- The Lincoln Electric Company

- Miller Electric Mfg. LLC

- IGM ROBOTERSYSTEME AG

- Abhisha Technocrats Pvt. Ltd.

- Acieta LLC

Frequently Asked Questions

The welding robotics market is projected to reach US$10.2 Bn in 2025.

Rising demand for automation, technological advancements in robotics, and Industry 4.0 adoption are key drivers.

The industry is poised to witness a CAGR of 10.0% from 2025 to 2032.

Innovations in laser technologies and government automation initiatives, such as hybrid systems, present significant growth opportunities.

FANUC Corporation, Kuka AG, Kemppi Oy, Yaskawa America, ABB, Panasonic Corporation, OTC DAIHEN Inc., DENSO CORPORATION, Kawasaki Heavy Industries, Ltd., Abhisha Technocrats Pvt. Ltd., and Acieta LLC are among the leading players, known for their innovative welding solutions.