- Metalworking & Fabrication

- Arc Welding Equipment Market

Arc Welding Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Arc Welding Equipment Market by Product Type (Shielded Metal Arc Welding (SMAW) Machines, Gas Metal Arc Welding (GMAW / MIG) Machines, Gas Tungsten Arc Welding (GTAW / TIG) Machines, Flux-Cored Arc Welding (FCAW) Machines, Submerged Arc Welding (SAW) Machines, Plasma Arc Welding (PAW) Machines, Others), Automation Level (Manual, Automatic, Semi-automatic), Welding Current Type, Gas Type, Industry and Regional Analysis, 2026 - 2033

Arc Welding Equipment Market Size and Trend Analysis

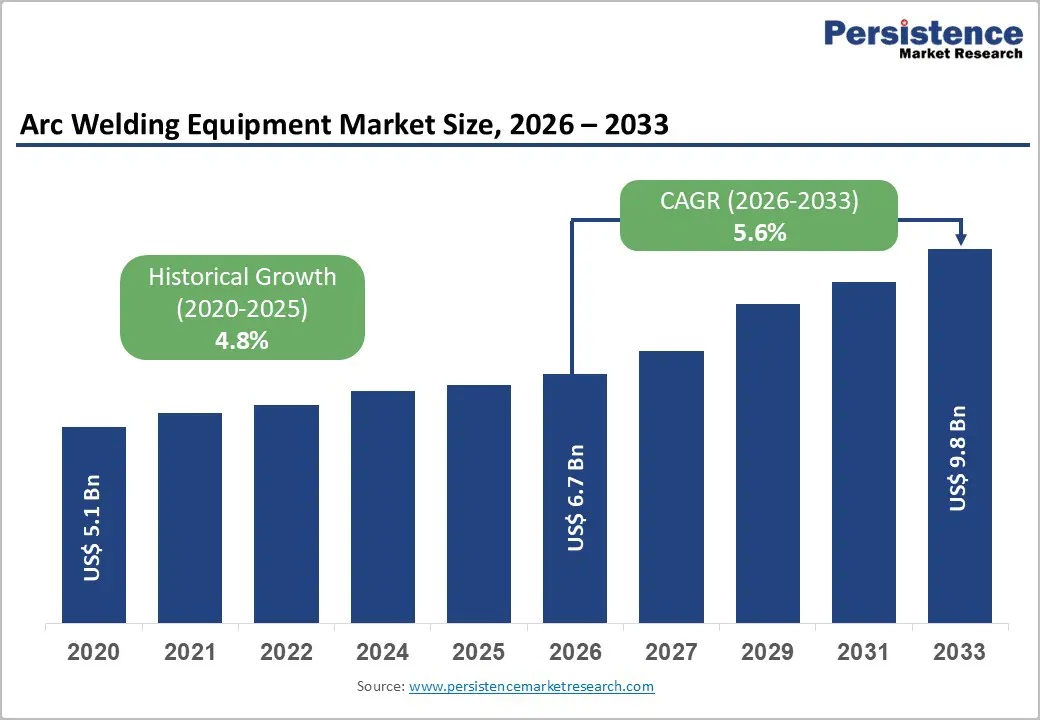

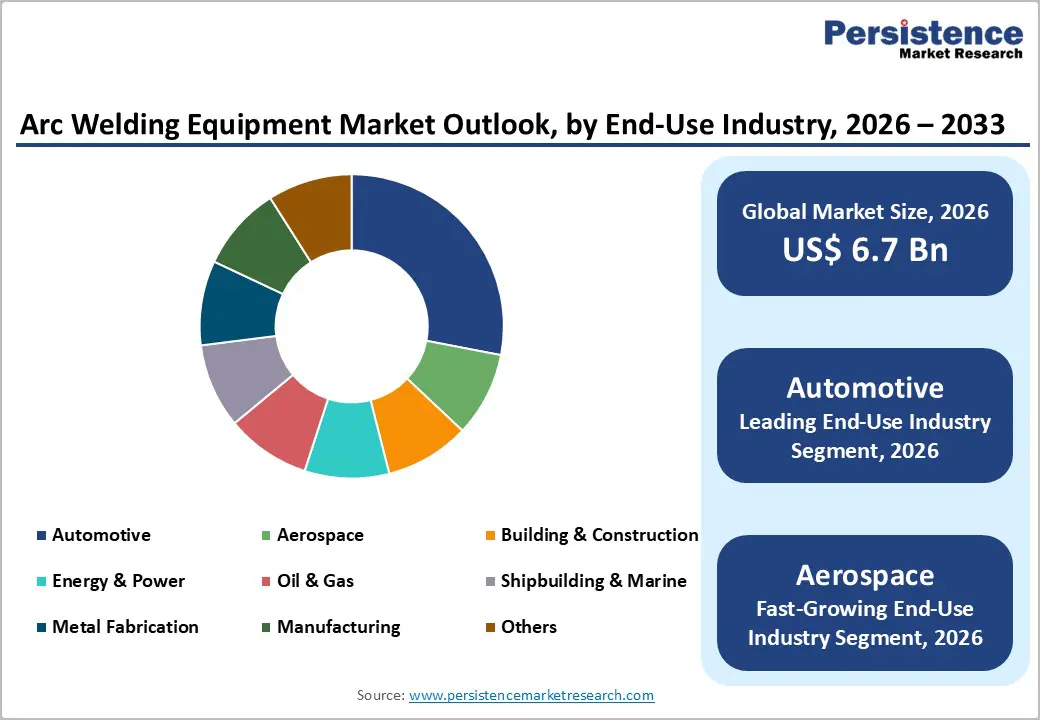

The global arc welding equipment market size is expected to be valued at US$ 6.7 billion in 2026 and projected to reach US$ 9.8 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

Accelerating infrastructure modernization initiatives, particularly in emerging economies, and the automotive industry’s rapid transition to electric-vehicle production, which requires specialized welding for battery assemblies and lightweight aluminum components, are propelling sustained demand for advanced arc-welding solutions.

Additionally, the persistent shortage of skilled welders, projected to reach 330,000 to 400,000 vacancies by 2028 according to the American Welding Society, is compelling manufacturers across sectors to adopt automated and robotic welding systems that deliver consistent quality while mitigating labor constraints.

Key Industry Highlights

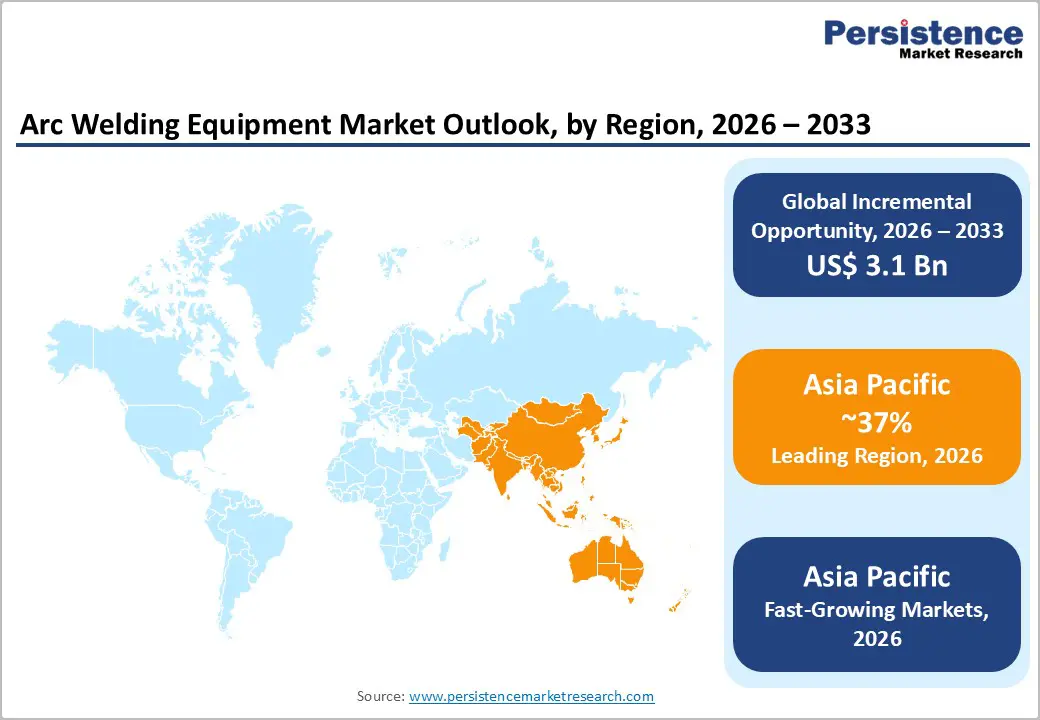

- Leading Region: Asia Pacific dominates with 37% share in 2025, driven by China’s 38.3% regional demand and India’s infrastructure expansion under the US$1.4 trillion National Infrastructure Pipeline.

- Fastest Growing Region: Asia Pacific exhibits 6.0% CAGR through 2033, propelled by China and India industrialization, electric vehicle manufacturing expansion, and shipbuilding dominance with over 60% of global orders.

- Dominant Segment: GMAW/MIG machines account for 37% of product share in 2025, with over 60% of automotive production lines using robotic MIG systems and 95% filler metal utilization.

- Fastest Growing Segment: Automatic welding equipment expands at 5.6% CAGR through 2033, driven by labor shortages of 330,000-400,000 welders by 2028 and robotic systems delivering ±0.05 mm repeatability.

- Key Opportunity: Renewable energy infrastructure expansion through 2030, requiring specialized SAW and FCAW equipment for wind turbine towers exceeding 100 meters height and offshore platform welding.

| Key Insights | Details |

|---|---|

| Arc Welding Equipment Market Size (2026E) | US$ 6.7 Billion |

| Market Value Forecast (2033F) | US$ 9.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Accelerating Infrastructure Development and Construction Activity Worldwide

Global infrastructure investment is experiencing unprecedented expansion, creating substantial demand for arc welding equipment across structural fabrication, bridge construction, and commercial building projects. The Infrastructure Investment and Jobs Act (IIJA), enacted in the United States, allocated US$1.2 trillion to roads, bridges, and utility infrastructure, thereby increasing demand for stick electrodes and flux-cored wires in structural steel applications.

According to Oxford Economics and global construction perspectives, global construction output is projected to increase by 85% to US$15.5 trillion by 2030, with China, India, and the United States accounting for more than half of this expansion. India’s National Infrastructure Pipeline aims to invest approximately US$ 1.4 trillion between 2020 and 2025 in transportation networks, energy grids, and urban development, necessitating durable welding solutions for steel structures and pipeline systems.

Automation Adoption Driven by Critical Skilled Labor Shortages

The manufacturing sector faces an acute and widening skills gap in welding, which is fundamentally reshaping equipment procurement strategies. The American Welding Society projects a deficit of approximately 330,000 welding professionals by 2028, with an average of 82,500 welding jobs requiring fulfillment annually between 2024 and 2028 across the infrastructure, energy, automotive, and construction sectors in the United States. This shortage stems from an aging workforce, with the average welder age at 55 years, coupled with insufficient development of a talent pipeline for younger workers. In response, manufacturers are accelerating investments in automatic and robotic arc welding systems that enhance productivity while reducing reliance on manual labor.

Kawasaki Motors Manufacturing Corp. (KMM) exemplifies this transition, having automated 80% of its arc-welding processes with robotic systems, relegating manual welding to 20% of operations, with the remainder focused on quality verification and hard-to-reach areas. Robotic GMAW (Gas Metal Arc Welding) and GTAW (Gas Tungsten Arc Welding) platforms deliver repeatability within ±0.05 mm, eliminate weld inconsistencies, and operate continuously without fatigue, yielding productivity gains of up to 30% according to industry automation studies.

Restraint - High Capital Investment Requirements for Advanced Welding Systems

The transition from traditional transformer-based to modern inverter-based and automated welding platforms necessitates substantial upfront capital expenditure, creating a barrier particularly for small and medium enterprises. Robotic welding cells, including GMAW and GTAW systems with integrated positioning manipulators, vision sensors, and programmable logic controllers, can range from US$ 100,000 to US$500,000 per installation, depending on complexity and payload capacity. While these systems deliver long-term returns through enhanced productivity and reduced labor costs, the initial investment burden constrains adoption rates among fabrication shops and regional contractors operating with limited capital budgets.

Additionally, specialized training programs required to operate and maintain automated welding equipment impose additional costs. Even semi-automatic systems featuring advanced digital interfaces and pulse-welding capabilities command premium prices relative to conventional manual machines, thereby slowing replacement cycles in price-sensitive market segments.

Stringent Environmental Regulations and Fume Control Compliance

Arc welding processes generate hazardous fumes, particulates, and electromagnetic emissions, and are subject to increasingly stringent occupational health and environmental regulations across major markets. The European Union’s Electromagnetic Fields (EMF) Directive mandates exposure limits that require the replacement of legacy transformer-based equipment with inverter designs incorporating field-cancellation technologies, thereby increasing compliance costs for manufacturers and end users.

Similarly, welding fume exposure standards enforced by the Occupational Safety and Health Administration (OSHA) in the United States and by analogous agencies globally require the installation of local exhaust ventilation systems, fume extractors, and personal protective equipment, thereby increasing operational expenditures. For instance, welding consumables that produce lower manganese emissions and equipment that integrates fume-mitigation technologies, such as pulsed-waveform systems, command higher prices, thereby pressuring profit margins. Moreover, evolving regulations around permissible exposure limits for hexavalent chromium and other metallic compounds generated during stainless steel welding necessitate continuous product reformulation and process modifications.

Opportunities - Renewable Energy Infrastructure Expansion Driving Specialized Welding Demand

The rapid expansion of renewable energy infrastructure is driving strong demand for advanced arc-welding equipment across wind, solar, and hydropower projects. Offshore wind developments require high-deposition welding processes for towers, monopiles, and other offshore structures that are exposed to cyclic loading and corrosive marine environments. Large-scale wind turbine towers fabricated from thick steel sections demand consistent weld quality and structural integrity.

At the same time, solar photovoltaic installations rely on welded galvanized steel mounting systems, creating demand for corrosion-resistant welding techniques. Accelerating investments in offshore wind capacity across Europe, Asia, and North America are reinforcing long-term equipment demand.

Manufacturers offering application-specific welding solutions, automation for repetitive fabrication, and materials compatible with harsh environments are well positioned to benefit from sustained renewable energy capital expenditure.

Digital Transformation and Smart Welding Technologies Integration

The integration of digital technologies into welding operations is creating new growth opportunities through enhanced productivity, quality control, and data-driven decision-making. Smart welding systems equipped with sensors, connectivity, and analytics enable real-time monitoring of weld parameters, predictive maintenance, and automated process optimization. These capabilities improve arc-on time, reduce defects, and lower engineering effort while supporting consistent weld quality across manual and automated operations.

Digital platforms also provide visibility into equipment utilization, consumable usage, and gas consumption, supporting operational efficiency. Additionally, remote monitoring, augmented guidance tools, and automated documentation help address skilled labor shortages and regulatory traceability requirements. Equipment suppliers combining hardware innovation with software-driven services can build recurring revenue models and achieve stronger customer retention.

Category-wise Analysis

Product Type Insights

Gas metal arc welding (GMAW/MIG) machines account for approximately 37% of the product type segment in 2025, driven by versatility across automotive, construction, and manufacturing applications. GMAW’s continuous wire feed and compatibility with a wide range of shielding gases enable efficient joining of ferrous and non-ferrous materials. The automotive industry represents GMAW’s dominant application, with robotic MIG systems constituting over 60% of production line welding stations. Electric vehicle manufacturing amplifies GMAW demand, as battery tray fabrication from aluminum alloys requires precise pulsed MIG welding to minimize heat input. GMAW achieves 95% filler metal utilization, compared with 65% for SMAW, resulting in superior productivity. The segment is projected to exhibit the fastest growth at a CAGR exceeding 6.0% through 2033 as automation deepens across metal fabrication and automotive industries globally.

Automation Level Insights

The automatic welding equipment segment accounts for approximately 46% of the market in 2025 and is projected to expand at a 5.6% CAGR through 2033, driven by manufacturing imperatives for consistency and labor cost mitigation. Automatic arc welding systems deliver repeatable weld quality independent of operator skill, critical for aerospace, automotive, and shipbuilding applications with zero-defect requirements.

The shipbuilding industry extensively employs automated systems for hull fabrication, where the ability to weld heavy steel plates with consistent penetration justifies capital investments. Automatic equipment adoption is particularly pronounced in the Asia Pacific, where China’s shipbuilding sector secured 38% of global orders in 2023. As manufacturers confront persistent labor shortages and tightening quality tolerances, automatic welding systems with AI-enabled adaptive control will increasingly displace manual processes.

Welding Current Type Insights

DC (Direct Current) welding equipment accounts for approximately 58% of the market in 2025, owing to superior arc stability, deeper penetration, and compatibility with inverter-based power sources. DC welding systems provide smoother, more controllable arcs than AC systems, which are particularly advantageous for GMAW and GTAW processes on ferrous metals. Inverter-based DC power sources reduce equipment weight by up to 90% relative to conventional transformers while enhancing energy efficiency. Illinois Tool Works (ITW) transitioned its welding segment to inverter architectures, achieving material conservation and operational energy savings.

The suitability of DC equipment for robotic automation further cements its dominance. The DC segment is forecast to grow at a 5.8% CAGR through 2033, as the proliferation of inverter technology reinforces the technical advantages of direct current.

Gas Type Analysis

Argon commands approximately 42% of the gas type segment in 2025, driven by its inert properties essential for GTAW (TIG) and aluminum GMAW (MIG) processes across aerospace, automotive, and precision manufacturing. Argon’s atomic structure provides effective shielding at 99.996% purity levels without reacting with base or filler metals.

Aerospace manufacturers welding titanium, aluminum, and nickel alloys rely exclusively on argon shielding to prevent oxide formation that would compromise structural integrity. Boeing and aerospace primes specify argon for automated TIG welding of critical airframe assemblies, in accordance with AWS D17.1. While carbon dioxide represents a cost-effective alternative for steel GMAW, argon’s technical performance in precision applications sustains its market leadership. The argon segment is projected to grow at a 5.4% CAGR through 2033, consistent with the expansion of aerospace production and automotive aluminum use.

Industry Insights

The automotive industry accounts for approximately 28% of the market in 2025, driven by intensive welding requirements across vehicle chassis, body assembly, and powertrain components. Global automotive production reached more than 88 million vehicles in 2023, according to OICA, each of which requires hundreds of welds. GMAW predominates in automotive applications due to its high-speed capability and compatibility with robotic automation.

Electric vehicle production increases demand, as battery pack enclosures made of aluminum alloys require specialized pulsed MIG and TIG welding. India’s FAME II scheme subsidized more than 2.5 million electric vehicles by early 2024, thereby stimulating domestic welding equipment procurement. The aerospace segment is the fastest-growing end-use, with a projected CAGR exceeding 7.0% through 2033, reflecting expanding aircraft production backlogs and stringent weld quality requirements for titanium and aluminum alloy fabrication.

Regional Insights

North America Arc Welding Equipment Market Trends and Insights

North America commands approximately 23% of the global market in 2025, underpinned by the United States’ highly diversified industrial base spanning automotive, aerospace, energy, construction, and defense sectors. Regional leadership is driven by early and widespread adoption of robotic welding systems, inverter-based power sources, and digitally enabled equipment. U.S. automotive manufacturers operate large-scale robotic GMAW lines for high-volume vehicle assembly, while accelerating electric vehicle production by major OEMs is increasing demand for aluminum welding in battery enclosures and lightweight body structures.

In aerospace, manufacturers specify high-precision GTAW systems compliant with AWS D17.1 for critical titanium and nickel-alloy components. Additionally, the Infrastructure Investment and Jobs Act’s US$ 1.2 trillion allocation is generating sustained demand for structural welding equipment across transportation, energy, and public works projects. Persistent skilled labor shortages further reinforce automation adoption.

Europe Arc Welding Equipment Market Trends and Insights

The European market is characterized by strong manufacturing ecosystems in Germany, France, and the United Kingdom, with a focus on quality and automation. Germany leads regional demand with 22.05% of European revenue, driven by automotive giants Volkswagen, BMW, and Mercedes-Benz operating advanced robotic welding facilities.

The Industrie 4.0 initiative promotes digital manufacturing, spurring adoption of IoT-enabled welding systems. France’s aerospace sector, led by Airbus, expanded 4.6% in 2023, necessitating specialized GTAW equipment for titanium airframe fabrication. Offshore wind projects in the North Sea regions drive demand for high-deposition SAW processes for tower fabrication. Regulatory compliance with the EMF Directive requires replacing legacy equipment with inverter designs, creating favorable replacement cycles.

Asia Pacific Arc Welding Equipment Market Trends and Insights

Asia-Pacific emerges as the largest and fastest-growing regional market, accounting for 37% of global revenue in 2025. China accounts for 38.3% of regional demand, reflecting its manufacturing dominance and position as the world’s largest steel producer. Chinese automotive production exceeded 23.8 million vehicles in 2023, sustaining robust demand for welding equipment, while BYD and CATL integrate robotic GMAW for battery systems.

Shipbuilding orders secured by Chinese yards drive the procurement of automatic SAW systems. India holds a 14.3% regional share, with the National Infrastructure Pipeline targeting US$1.4 trillion in investment through 2025 in highways, railways, and urban development. The “Make in India” campaign and the FAME II electric vehicle scheme are stimulating manufacturing capacity, which requires modern welding equipment. The region’s projected 6.0% CAGR through 2033 reflects continued industrialization and the adoption of automation.

Competitive Landscape

The global arc welding equipment market features a consolidated structure at the premium end, where a limited number of multinational manufacturers account for nearly half of total revenue, supported by strong brand equity, broad product portfolios, and global distribution networks. In contrast, mid-tier and regional suppliers compete aggressively in price-sensitive markets through localized manufacturing and cost-efficient offerings.

Business strategies among market leaders emphasize continuous innovation in inverter-based power sources, digital control systems, and automation-ready platforms to improve energy efficiency, portability, and weld quality.

Design differentiation, ergonomics, and multi-process capability are increasingly used to justify premium pricing. Sustainability has also emerged as a strategic focus, with manufacturers prioritizing lightweight designs, reduced material usage, and lower energy consumption. Across all tiers, companies are shifting toward integrated solution models that combine equipment, consumables, and digital connectivity, enabling stronger customer lock-in, recurring service revenues, and long-term competitive advantage.

Key Developments

- November, 2025, Novarc Technologies Inc. unveiled the SWR-TIGMIG, a dual-process spool welding robot that integrates TIG and MIG welding processes, offering enhanced efficiency, precision, and flexibility for pipe fabricators seeking to improve their welding operations.

- September, 2025, Lincoln Electric introduced the Flex Lase Handheld Laser Welding System, a 2kW solution delivering high-precision welds at faster speeds than traditional TIG methods, with user-friendly onboarding and compatibility for various materials.

Companies Covered in Arc Welding Equipment Market

- The Lincoln Electric Company

- ACRO Automation Systems, Inc.

- Illinois Tool Works Inc. (Miller Electric, Hobart Brothers)

- Ador Welding Limited

- Mitco Weld Products Pvt. Ltd.

- voestalpine Böhler Welding Group GmbH

- Carl Cloos Schweisstechnik GmbH

- OTC DAIHEN Inc.

- Panasonic Industry Co., Ltd.

- Coherent, Inc.

- ESAB (Enovis Corporation)

- Polysoude S.A.S.

- Kemppi Oy

- Cruxweld Industrial Equipment Pvt. Ltd.

- Fronius International GmbH

- Kawasaki Heavy Industries, Ltd.

- ABB Ltd.

- FANUC Corporation

- Kobe Steel, Ltd.

- Hyundai Welding Co., Ltd.

- Tianjin Golden Bridge Welding Materials Group Co., Ltd.

- Bernard (ITW Welding)

- Tregaskiss (ITW Welding)

- Air Liquide Welding

- Novarc Technologies Inc.

Frequently Asked Questions

The global arc welding equipment market is valued at US$ 6.7 billion in 2026, projected to reach US$ 9.8 billion by 2033 at a 5.6% CAGR during the forecast period.

Key drivers include global infrastructure investment such as the US$ 1.2 trillion Infrastructure Investment and Jobs Act, electric vehicle production growth, skilled welder shortages of 330,000-400,000 by 2028, and renewable energy expansion requiring specialized welding solutions.

Asia Pacific dominates with East Asia capturing 29.6% market share in 2025. China commands 38.3% of regional demand through manufacturing scale, shipbuilding leadership, and automotive production exceeding 23.8 million vehicles annually.

Renewable energy infrastructure expansion presents transformative opportunities, with offshore wind capacity additions through 2030 requiring specialized welding equipment for turbine towers exceeding 100 meters height and offshore platform fabrication across Europe, North America, and Asia.

Leading participants include The Lincoln Electric Company, ESAB (winner of three 2024 Red Dot Design Awards), Illinois Tool Works Inc. (Miller Electric), Fronius International GmbH, Panasonic Industry Co., Ltd., alongside regional players Ador Welding Limited and emerging innovator Novarc Technologies Inc. with AI-powered systems.