- Food Ingredients & Additives

- Vegan Flavors Market

Vegan Flavors Market Size, Share, and Growth Forecast, 2025 - 2032

Vegan Flavors Market By Form (Powder, Liquid Concentrates), Source (Herbs & Spices, Vegetable/Protein-derived), Application, and Regional Analysis for 2025 - 2032

Vegan Flavors Market Size and Trends Analysis

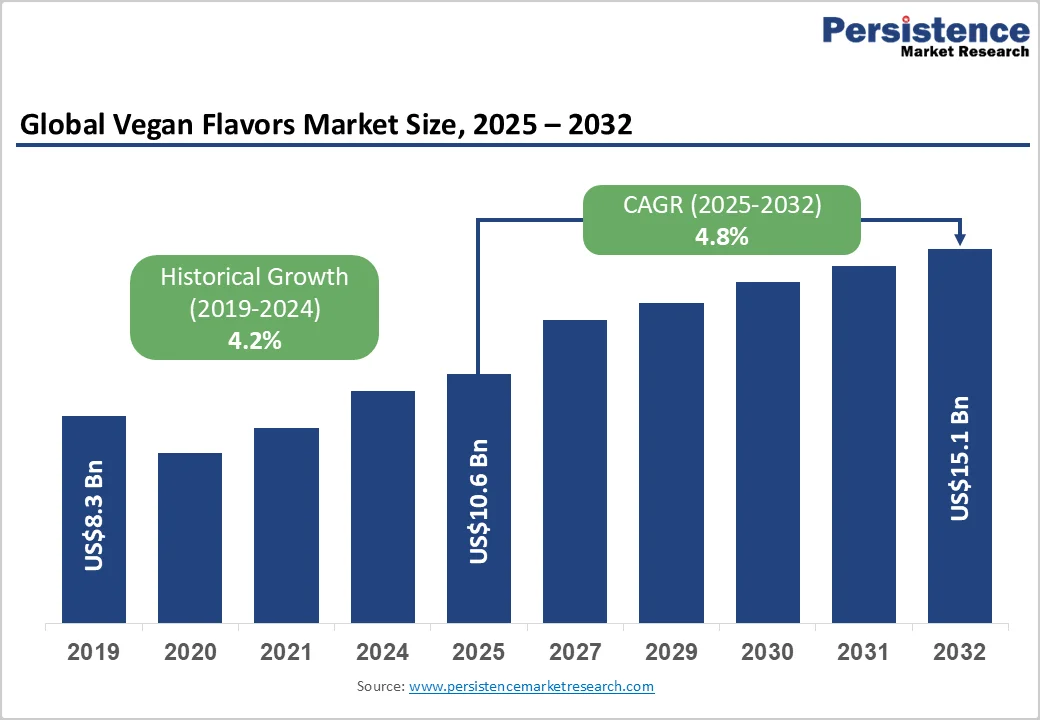

The global vegan flavors market size was valued at US$10.6 Billion in 2025 and is projected to reach US$15.1 Billion by 2032, growing at a CAGR of 4.8% between 2025 and 2032, driven by the rising adoption of plant-based diets, increasing demand for clean-label ingredients, and rapid product innovations in plant-derived savory and dairy-analog flavors.

Growing consumer demand for plant-based products with authentic animal-like flavors, combined with clear vegan labeling regulations, is driving flavor houses to invest in R&D and partner with food manufacturers to scale tailored formulations, strengthening their market leadership.

Key Industry Highlight

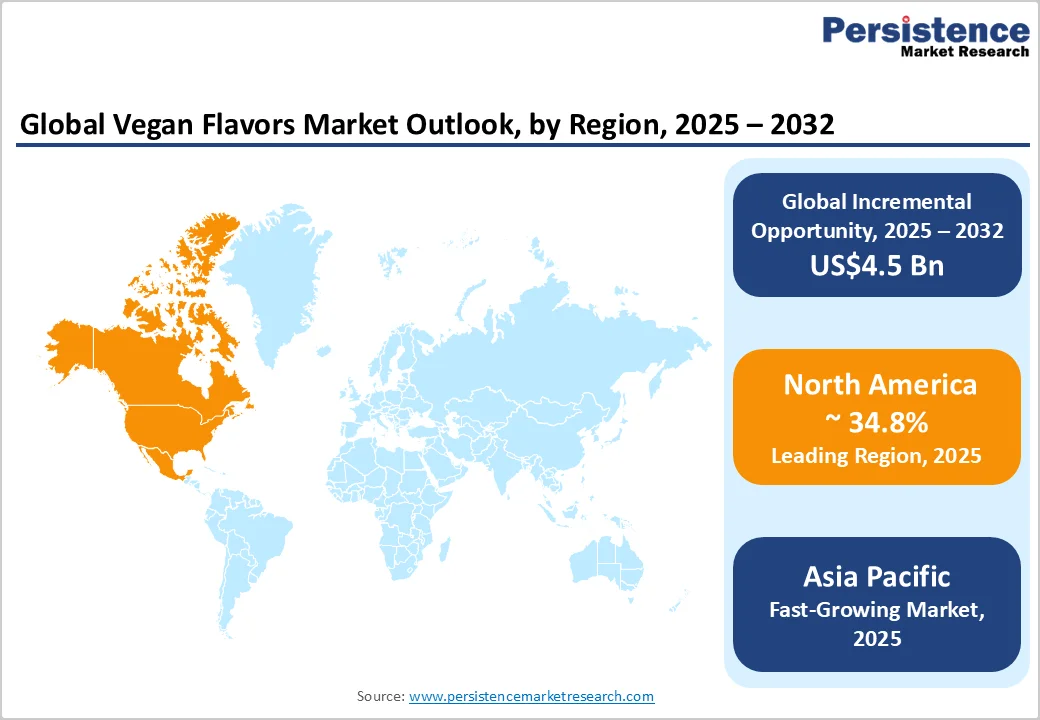

- Leading Region: North America, with over 34.8% market share in 2025, driven by high per-capita plant-based consumption, early adoption of fermentation-derived flavors, and strong R&D investments.

- Fastest-growing Region: Asia Pacific, projected CAGR of 6.2% (2025 - 2032), supported by urbanization, changing diets, and localized plant-based launches in China, Japan, India, and ASEAN countries.

- Investment Plans: Companies are expanding R&D centers and fermentation-based flavor technology; notable investments include Symrise’s Chicago innovation center (2024) and Givaudan’s Shanghai plant-based flavor hub (2023).

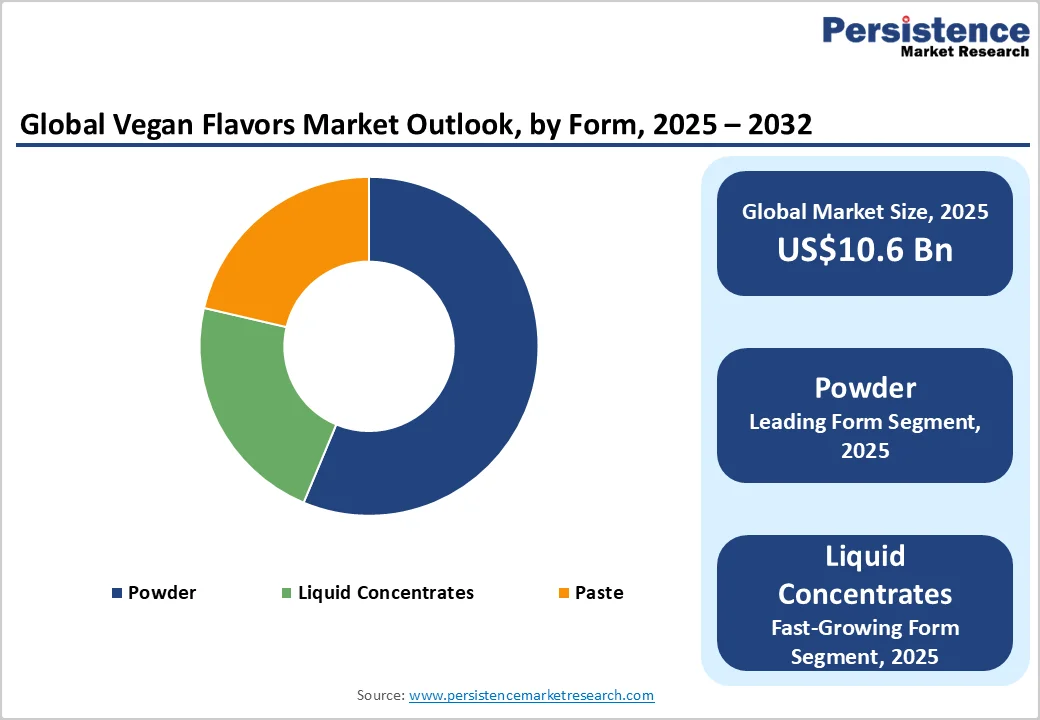

- Dominant Form: Powder flavors, holding approximately 58% of market share in 2025, favored for bakery, snacks, and powdered beverages.

- Leading Source: Herbs & spices, contributing 45% revenue share, widely used for savory and umami flavoring in meat and dairy analogs.

| Key Insights | Details |

|---|---|

| Vegan Flavors Market Size (2025E) | US$10.6 Bn |

| Market Value Forecast (2032F) | US$15.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Plant-Based Food Adoption and Scale Effects

The growing adoption of plant-based meat, dairy, and ready meals is expanding the demand for vegan flavor systems. Double-digit growth in plant-based food categories globally has prompted flavor companies to prioritize R&D for meat- and dairy-like flavor systems. Increased production volumes allow for larger R&D investments, lowering per-unit flavor development costs and improving profit margins for specialist vendors.

Clean-Label and Natural-Ingredient Preference

Consumers increasingly prefer natural, non-animal, and short-label ingredient lists. Manufacturers are replacing animal-derived or synthetic aroma compounds with botanically sourced extracts, fermented ingredients, and biotech-derived flavor molecules. This shift in procurement leads to higher-value natural and fermentation-derived inputs, giving competitive advantage to suppliers able to deliver stable, label-friendly solutions.

Sensory Technology and Ingredient Innovation

Advances in flavor encapsulation, taste modulation, and biotechnology, including fermentation-derived molecules, enhance the authenticity of plant-based products. These technologies reduce dependence on scarce botanical extracts, ensure repeatable sensory outcomes, and shorten time-to-market for new vegan products, supporting premiumization and innovation strategies.

Barrier Analysis - Ingredient Cost and Supply Volatility

High-quality plant extracts and fermentation-derived molecules carry a cost premium compared with conventional synthetic chemicals. Weather-sensitive botanicals introduce supply risks and price volatility, which can compress margins and delay product launches. Input-cost exposure can shift gross margins by several percentage points during poor harvest years.

Regulatory Complexity and Labeling Fragmentation

Regulations around terms such as “vegan,” “plant-based,” and dairy/meat analogs vary globally, creating compliance costs and potential reformulation requirements. Increased labeling complexity can add low-to-mid single-digit percentage costs to product launches and slow geographic expansion.

Opportunity Analysis - Emerging Markets and Mainstreaming Of Vegan Diets

Asia-Pacific and parts of Latin America are transitioning from niche to mainstream plant-based consumption. Rising incomes and urbanization are expanding demand for vegan flavors. Targeted product launches in these regions could capture several hundred million US$ in incremental revenue by 2032.

Ingredient Innovation through Fermentation and Biotechnology

Biotech-derived flavor molecules allow cost-effective replication of complex aromas traditionally sourced from animals or scarce botanicals. Growing investment and adoption in this sector create a significant growth avenue, with fermentation-based flavors forecasted to form a multi-hundred-million US$ opportunity by 2030.

Category-wise Analysis

Form Insights

Powdered flavors dominate the vegan flavors market, capturing around 58% of market share in 2025, due to their transportability, long shelf life, and compatibility with dry blends such as seasonings, bakery mixes, powdered beverages, and instant soups. They are especially favored in snack and bakery applications, providing consistent taste, aroma, and color without affecting texture.

For instance, powdered umami flavors from yeast extracts enhance savory notes in plant-based meat snacks, while powdered cocoa and vanilla remain staples in bakery and beverage products. Their minimal refrigeration needs and storage stability make them ideal for large-scale manufacturers, enabling wider distribution and lower operational costs.

Liquid concentrates are experiencing the fastest growth in the vegan flavors market due to their blending flexibility, rapid solubility, and lower energy needs during processing. Ideal for beverages, sauces, dairy alternatives, and ready meals, they allow quick incorporation without compromising taste.

Examples include liquid cocoa or almond flavors in plant-based milks, protein shakes, and oat-based beverages, as well as ready-to-drink coffee alternatives and flavored yogurts. Cold-chain compatibility and on-demand dosing enable manufacturers to launch new products rapidly while ensuring clean-label compliance and consistent sensory quality.

Source Insights

Herbs and spices lead in revenue share as they provide essential savory, aromatic, and umami notes in plant-based products. These sources are particularly important in meat analogs, plant-based sauces, soups, and ready meals. For example, rosemary, thyme, and smoked paprika are commonly used to mimic roasted or grilled meat flavors in vegan sausages or plant-based burgers.

Similarly, spice extracts such as turmeric and ginger enhance both taste and perceived freshness in plant-based beverages and dairy alternatives. Herbs and spices have a well-established role in flavoring, ensuring consistent demand from both global flavor houses and regional food manufacturers.

Fermentation-derived flavors and protein hydrolysates are the fastest-growing source segments, replicating complex animal-derived aromas, umami notes, and creamy textures. Companies are increasingly leveraging fermentation to produce molecules such as hefe yeast-derived savory flavors or dairy-mimicking compounds for cheese, yogurt, and butter alternatives.

For example, fermented savory flavor concentrates are used in plant-based cheeses to provide an authentic aged cheese taste, while protein-derived peptides enhance mouthfeel in plant-based beverages and meat substitutes. Investments in biotech and fermentation-based flavor solutions are driving high CAGR growth, as these solutions offer scalable, sustainable, and reproducible alternatives to traditional animal-derived or rare botanical ingredients.

Application Insights

Food and beverages account for the largest share of vegan flavor consumption, encompassing plant-based meat, dairy alternatives, snacks, bakery, soups, sauces, and beverages. For instance, plant-based yogurts, cheeses, and nut-based milks rely heavily on flavor systems to deliver creamy, authentic tastes.

Savory snacks such as vegan jerky, protein bars, or plant-based chips use spice and fermentation-derived flavor blends to enhance umami and overall taste profiles. Food manufacturers are the primary buyers and co-developers, collaborating with flavor houses to ensure that vegan products meet consumer expectations in both taste and label transparency.

Ready-to-drink beverages and dairy analogs are expanding at the fastest rate due to growing consumer interest in plant-based milks, protein shakes, oat or soy beverages, and functional drinks enriched with vitamins or probiotics. Flavors such as vanilla, chocolate, almond, and fruit extracts are widely incorporated into these products to enhance sensory appeal.

For example, oat-based lattes or protein shakes often include a combination of liquid and powder flavors to balance sweetness, creaminess, and stability. Clean-label, soluble flavor systems are crucial in these applications, as they maintain taste consistency while meeting consumer demand for transparency and natural ingredients.

Regional Insights

North America Vegan Flavors Market Trends - R&D-Driven Innovation and Strategic Expansion in Vegan Flavors

North America represents the largest market for vegan flavors, with a 34.8% market share in 2025. The region’s growth is primarily fueled by high per-capita consumption of plant-based products, driven by increasingly health-conscious and environmentally aware consumers. The U.S. market further benefits from substantial R&D investments and early adoption of fermentation-derived flavor molecules that authentically replicate dairy and meat notes in plant-based offerings.

The regulatory environment, particularly the FDA’s guidelines on clean-label and vegan claims, promotes transparency and bolsters consumer confidence, incentivizing manufacturers to innovate. The market landscape is dominated by major global flavor houses such as Givaudan, Kerry, and IFF, alongside specialized startups that cater to niche segments such as plant-based meats, dairy alternatives, and functional beverages.

Notable recent developments include Kerry Group’s 2023 launch of plant-based savory flavor concentrates targeting quick-service restaurants (QSRs) and retail brands, Givaudan’s 2024 partnership with biotech startup Perfect Day to expand fermentation-derived dairy flavors, and Symrise’s establishment of an innovation center in Chicago in 2025 focused on clean-label and plant-based flavor research. Strategic mergers and acquisitions remain a key trend, aimed at enhancing R&D capabilities, broadening product portfolios, and accelerating market penetration across the U.S. and Canada.

Europe Vegan Flavors Market Trends - Sustainability-Driven Growth with Botanical Sourcing and Regulatory Harmonization

Europe demonstrates robust demand for vegan flavors, with key markets including Germany, the U.K., France, and Spain. This growth is underpinned by sustainability-driven consumers, increased adoption of plant-based diets, and heightened awareness of environmental issues. The region benefits from sophisticated retail infrastructure, strong supply chain networks, and a mature regulatory framework characterized by EU-wide harmonization of labeling and ingredient standards.

European markets are served by a mix of global flavor houses and regional specialists, who leverage advanced R&D networks in countries such as Switzerland, France, and Germany to develop flavors tailored to local preferences. Investment activity in the region emphasizes botanical sourcing, fermentation-derived flavors, and mid-sized natural flavor firms, with private equity increasingly playing a role in funding innovation and scaling operations.

Recent milestones include Symrise’s 2023 expansion of its natural and plant-based flavor portfolio in Germany, Givaudan’s 2024 acquisition of Naturex to enhance botanical sourcing and support vegan flavor R&D, and Firmenich’s 2025 launch of a new plant-based dairy flavor range targeting retail markets in the U.K. and France.

Europe’s competitive landscape combines established multinational players with agile regional innovators, with ongoing investments focusing on sustainable ingredient sourcing, fermentation-derived aroma technologies, and partnerships with food startups to accelerate market adoption.

Asia Pacific Vegan Flavors Market Trends - Regional R&D and Cost-Effective Flavor Solutions Supporting Market Growth

The Asia Pacific region is the fastest-growing market for vegan flavors, driven by rapid urbanization, shifting dietary habits, rising disposable incomes, and growing health and sustainability awareness. Key markets such as China and Japan lead in flavor innovation, investing heavily in research to develop plant-based dairy and meat alternatives. India, characterized by a price-sensitive yet increasingly health-conscious consumer base, focuses on delivering cost-competitive flavor solutions.

The region’s advantages include large-scale manufacturing capabilities, access to diverse botanical ingredients, and lower production costs, providing competitive leverage to both global and regional flavor houses. Companies are actively establishing regional R&D centers to customize formulations that cater to local tastes and culinary preferences, such as fermented soybean flavors in China and tropical fruit blends in Southeast Asia. Regulatory environments vary widely, with countries such as Japan enforcing clear vegan labeling standards, while emerging markets continue to evolve their guidelines.

Recent developments highlight Givaudan’s 2023 opening of a plant-based flavor R&D hub in Shanghai focused on savory and dairy alternatives, Symrise’s 2024 launch of tropical fruit and plant-based dairy flavors tailored for ASEAN ready-to-drink beverages, and Takasago’s 2025 investment in fermentation-derived umami flavor technology in Japan aimed at enhancing meat alternatives.

Investment strategies in APAC prioritize scaling local production, co-developing flavors with regional food manufacturers, and leveraging native botanical and fermentation expertise to meet expanding demand in both urban centers and tier-2 cities.

Competitive Landscape

The global vegan flavors market is moderately consolidated, with major players, including Givaudan, Kerry, IFF, Symrise, and Firmenich, holding over 40% of revenue, leveraging R&D, global distribution, and co-development with food manufacturers. The remaining market is fragmented, served by smaller firms and startups targeting niche applications, regional preferences, and emerging segments such as fermentation-derived flavors.

Competitive advantage relies on innovation, regulatory compliance, and formulation expertise, with leaders focusing on co-development, biotechnology partnerships, clean-label offerings, cost-effective supply chains, and regional expansion to meet rising consumer demand for authentic plant-based flavors.

Key Industry Developments

- In September 2024, Symrise opened an innovation center in Chicago focused on clean-label, plant-based flavor research, improving regional R&D capabilities for beverages and savory applications.

- In January 2024, Givaudan acquired Naturex and strengthened botanical sourcing and plant-based flavor development in Europe, supporting clean-label product launches.

- In February 2025, Firmenich introduced a plant-based dairy flavor range in the U.K. and France, emphasizing natural, label-friendly solutions for retail and foodservice applications.

Companies Covered in Vegan Flavors Market

- Givaudan

- International Flavors & Fragrances (IFF)

- Symrise

- Firmenich

- Kerry Group

- Sensient Technologies

- Robertet

- Takasago

- T. Hasegawa

- Mane

- Döhler

- Bell Flavors & Fragrances

- Wild Flavors

- Archer Daniels Midland Company (ADM)

- Frutarom

- Naturex

- GNT Group

- Baolingbao Biology

- Huabao International

- Dohler Group

Frequently Asked Questions

The vegan flavors market size in 2025 is US$10.6 Billion.

The vegan flavors market is projected to reach US$15.1 Billion by 2032.

Key trends include rising adoption of plant-based diets, increased demand for clean-label and natural ingredients, growth of fermentation- and protein-derived flavors, and innovation in ready-to-drink and dairy analog applications.

The powder form segment is the leading category, holding approximately 60% of market share, widely used in snacks, bakery, and powdered beverage applications.

The vegan flavors market is expected to grow at a CAGR of 4.8% between 2025 and 2032.

Major players with strong portfolios include Givaudan, International Flavors & Fragrances (IFF), Symrise, and Firmenich.