- Beauty & Personal Care

- Vegan Cosmetics Market

Vegan Cosmetics Market Size, Share, and Growth Forecast 2026 - 2033

Vegan Cosmetics Market by Product Type (Facial Products, Eye Products, Lip Products, Nail Products, Others), Packaging Type (Pumps & Dispensers, Compact Cases, Jars, Pencils and Sticks, Tubes, Others), End-user, Price Range, Sales Channel, and Regional Analysis, 2026 - 2033

Vegan Cosmetics Market Size and Trend Analysis

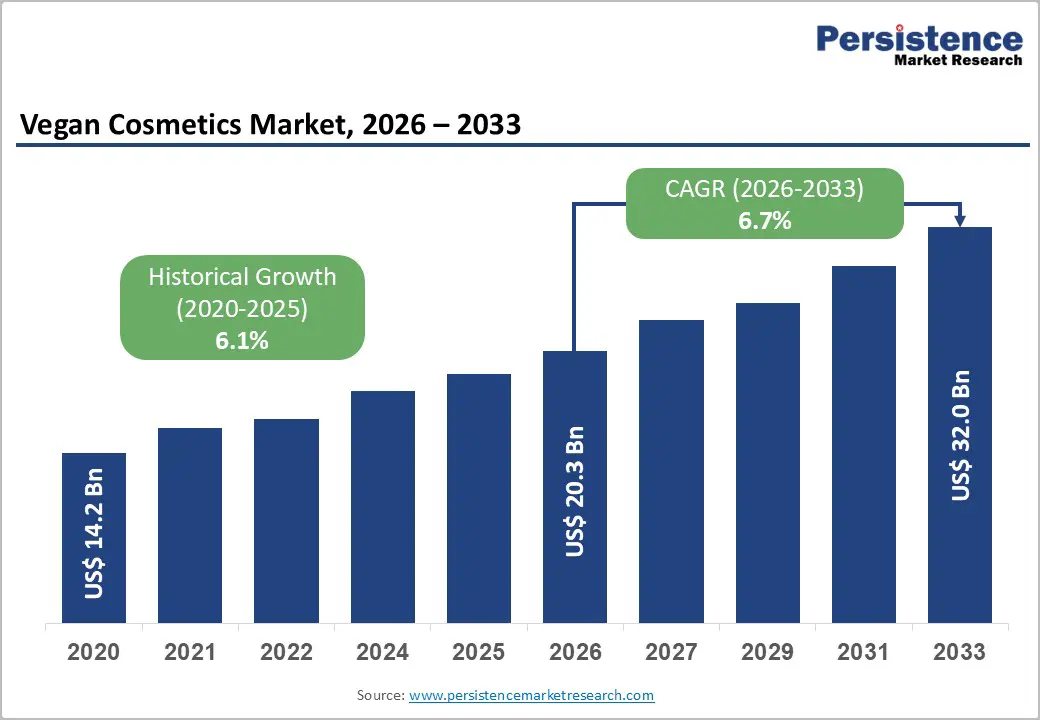

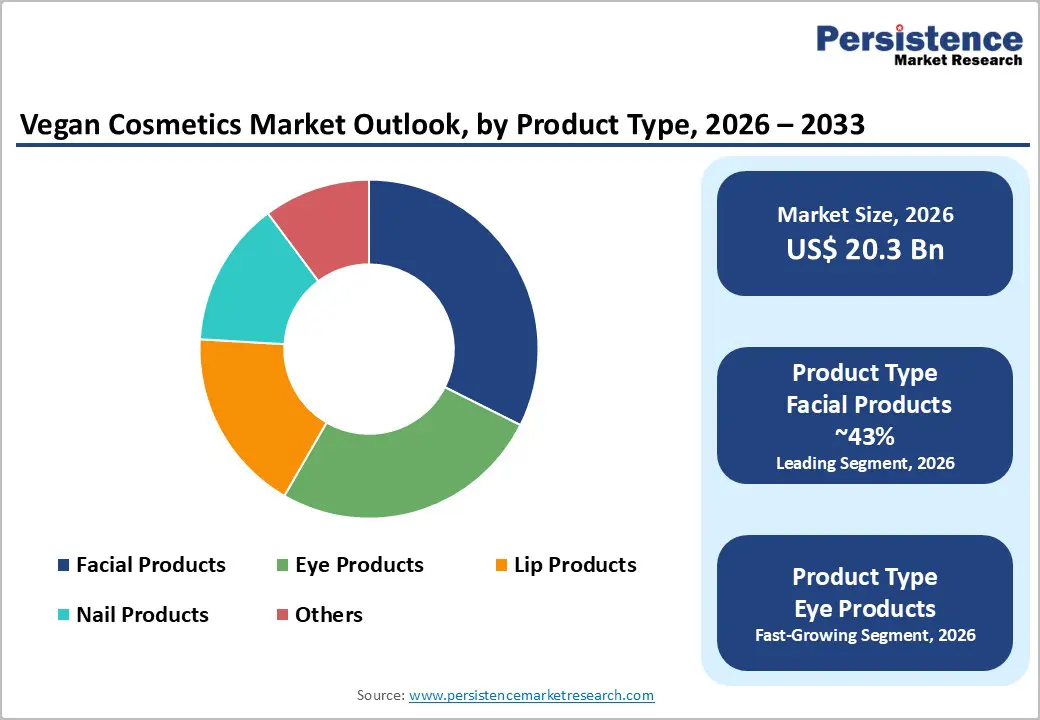

The global vegan cosmetics market size is projected to be valued at US$ 20.3 billion in 2026 and is expected to reach US$ 32.0 billion by 2033, expanding at a CAGR of 6.7% during the forecast period.

The market growth is driven by a pronounced shift toward ethical consumerism, where purchasing decisions increasingly reflect values related to animal welfare and sustainability. The rise of the clean beauty movement has pushed vegan formulations into the mainstream, encouraging brands to eliminate animal-derived ingredients. Additionally, stringent regulations and growing advocacy from organizations promoting cruelty-free practices continue to accelerate market adoption.

Key Industry Highlights:

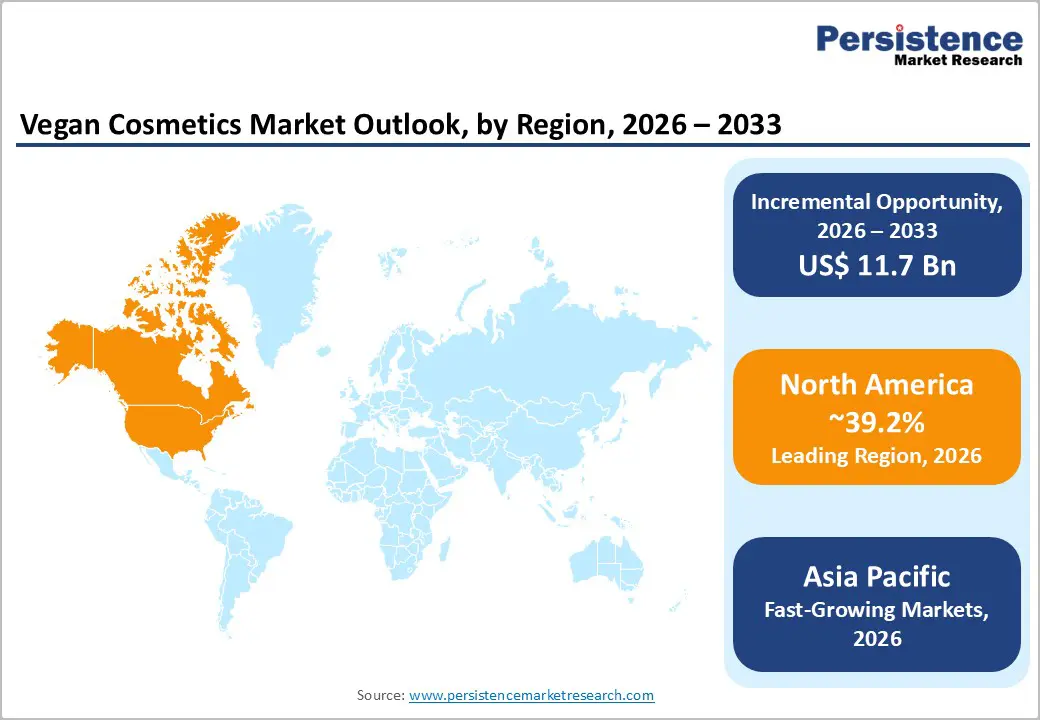

- Leading Region: North America leads the global vegan cosmetics market with approximately 39.2% market share, supported by high consumer awareness, strong purchasing power, celebrity-led brand influence, and an extensive network of specialty beauty retailers that drive product visibility and trust.

- Fastest Growing Region: Asia Pacific, currently accounting for around 32.3% of global market share, represents the fastest-growing region, driven by regulatory easing on animal testing, rising ethical awareness among young consumers, and the rapid adoption of vegan formulations within K-Beauty and J-Beauty ecosystems.

- Dominant Segment: Facial Products dominate the market with approximately 43% share, as consumers prioritize ingredient safety and ethical sourcing for products such as foundations and concealers that remain on the skin for prolonged periods.

- Fastest Growing Segment: Online sales channels are witnessing the most rapid growth, supported by expanding direct-to-consumer strategies, influencer-driven discovery, virtual try-on tools, and subscription-based purchasing models.

- Key Market Opportunity: Bio-engineered and lab-grown ingredients present a significant opportunity, enabling vegan cosmetics to deliver performance parity with animal-derived actives and unlock premium and clinical beauty segments.

| Key Insights | Details |

|---|---|

|

Vegan Cosmetics Market Size (2026E) |

US$ 20.3 Billion |

|

Market Value Forecast (2033F) |

US$ 32.0 Billion |

|

Projected Growth CAGR (2026-2033) |

6.7% |

|

Historical Market Growth (2020-2025) |

6.1% |

Market Dynamics

Drivers - Rising Influence of Ethical Consumerism and Expanding Clean Beauty Standards

The primary growth driver shaping the vegan cosmetics market is the accelerating shift in consumer values toward ethical consumption, particularly among Gen Z and Millennial demographics. These consumers actively prioritize transparency, animal welfare, and ingredient integrity when making purchasing decisions. Growing interest in certified vegan products reflects rising trust in third-party verification, pushing brands to reformulate cosmetics by eliminating animal-derived ingredients such as keratin, collagen, and carmine.

This ethical shift strongly overlaps with the clean beauty movement, where vegan labeling is increasingly associated with safety, non-toxicity, and overall skin health. As a result, major beauty retailers have introduced dedicated “conscious” and ethical beauty sections, enhancing product visibility and accessibility. This retail-level endorsement has significantly increased consumer adoption and sales momentum for compliant vegan cosmetic brands.

Strengthening Regulatory Bans and Legislative Support Against Animal Testing

Supportive regulatory frameworks banning animal testing have emerged as a structural driver accelerating the growth of vegan cosmetics globally. The European Union’s early prohibition on animal testing for cosmetics set a precedent, encouraging other regions to adopt similar cruelty-free legislation. Markets such as Canada, Brazil, and multiple U.S. states have implemented laws that favor ethical, transparent cosmetic formulations.

In the United States, regulatory developments such as enhanced ingredient safety oversight have indirectly strengthened demand for plant-based and vegan cosmetic products. These regulations reduce compliance uncertainty for vegan brands while compelling conventional cosmetic manufacturers to reformulate. As a result, regulatory pressure is expanding the overall addressable market and reinforcing vegan cosmetics as a compliant, future-ready alternative.

Restraints - High Formulation Costs and Operational Supply Chain Complexities in Vegan Cosmetics

A key restraint hindering the broader adoption of vegan cosmetics is the high formulation cost associated with replacing animal-derived ingredients. Common inputs such as lanolin, collagen, and carmine are inexpensive and highly functional, whereas plant-based or synthetic alternatives often require advanced biotechnology, specialized extraction methods, or limited agricultural sourcing. These factors significantly increase the cost of goods sold and complicate procurement strategies for manufacturers.

Achieving equivalent performance, color payoff, texture stability, and shelf life without animal ingredients presents technical challenges, especially in color cosmetics. As a result, many vegan cosmetic products are positioned within premium price segments. This pricing structure limits accessibility for cost-sensitive consumers, particularly during periods of inflation and reduced discretionary spending.

Greenwashing Practices and the Lack of Globally Standardized Vegan Labeling Frameworks

Greenwashing remains a persistent challenge in the vegan cosmetics market, undermining consumer trust and market transparency. Brands frequently use ambiguous terms such as “natural,” “clean,” or “plant-based” without adhering to strict vegan formulation standards. The absence of a universally accepted legal definition for vegan cosmetics creates inconsistencies across regions and enables misleading claims.

Furthermore, vegan certification largely depends on voluntary programs offered by organizations such as PETA or Leaping Bunny, which impose additional costs and compliance requirements. Smaller brands may struggle to obtain these accreditations, while non-compliant players dilute market credibility. This lack of standardization complicates differentiation for genuinely ethical brands and slows informed consumer decision-making.

Opportunity - Innovation in Bio-Engineered and Lab-Grown Ingredients Enhancing Vegan Cosmetic Performance

A major growth opportunity for the vegan cosmetics market lies in advancements in biotechnology that enable the development of bio-engineered and lab-grown ingredients. Through microbial fermentation and bio-identical synthesis, ingredient suppliers are producing vegan alternatives to traditionally animal-derived proteins such as collagen and elastin. These innovations allow brands to replicate the functional benefits of animal ingredients without ethical compromise.

As these bio-fermented ingredients become commercially scalable, they help close the performance gap that has historically limited vegan cosmetic adoption. This progress unlocks high-value segments such as anti-aging, clinical, and dermatologist-backed cosmetics. Demand is expected to accelerate particularly in North America and Europe, where consumers prioritize both ethical sourcing and proven product efficacy.

Expansion into Men’s Grooming and Gender-Neutral Cosmetic Product Categories

The men’s grooming and gender-neutral cosmetics segment represents a largely untapped growth opportunity for vegan cosmetic brands. Male consumers are becoming increasingly engaged with skincare and cosmetic routines, driven by rising awareness of personal appearance, sustainability, and ingredient safety. This shift is creating demand for vegan formulations across facial cosmetics, concealers, and grooming essentials.

Brands adopting inclusive, gender-neutral positioning and minimalist packaging are successfully resonating with this audience. Moving away from traditional, hyper-masculine branding toward clean and ethical formulations expands the consumer base beyond women. Markets such as the United States and South Korea are expected to lead growth as male beauty norms evolve toward comprehensive skincare practices.

Category-wise Analysis

Product Type Insights

Facial Products dominate the vegan cosmetics market, accounting for approximately 43% of the total market share. This leadership is driven by the essential role of foundations, concealers, primers, and face powders in daily beauty routines. Consumers are particularly cautious about ingredients in products that remain on the skin for extended durations, accelerating the adoption of vegan alternatives. Strong performance parity and shade inclusivity offered by leading brands have further reinforced facial cosmetics as the primary revenue-generating segment.

Eye Products represent the fastest-growing product category, supported by rising experimentation and trend-driven makeup usage. Increased demand for vegan mascaras, eyeliners, and eyeshadows is being fueled by improvements in pigmentation, longevity, and formulation performance. Social media influence and frequent product innovation continue to encourage rapid adoption among younger consumers seeking expressive yet cruelty-free makeup options.

Packaging Type Insights

Tubes lead the vegan cosmetics packaging segment, contributing around 36% of the total packaging share. Their dominance stems from versatility, cost efficiency, and compatibility with a wide range of cosmetic formulations, including foundations, primers, and liquid makeup. Tubes are widely preferred by mass and mid-range brands due to their lightweight nature, durability, and logistical advantages, making them ideal for high-volume distribution.

Refillable and sustainable packaging formats are emerging as the fastest-growing category as environmental awareness intensifies. Brands are increasingly adopting reusable jars, refill pods, and bio-based materials to align with circular economy goals. Consumer preference for reduced plastic waste and sustainable packaging innovation is driving experimentation beyond conventional formats.

End-user Insights

Women account for the largest share of the vegan cosmetics market, representing approximately 70% of overall demand. This dominance reflects the historically female-centric structure of the cosmetics industry and early marketing focus on women aged 18–34. These demographics exhibit strong engagement with ethical consumption trends, higher brand loyalty, and greater willingness to adopt certified vegan cosmetic products across facial, eye, and lip categories.

The Men segment is the fastest-growing end-user category, driven by shifting grooming norms and increased acceptance of cosmetic usage. Rising interest in facial cosmetics, concealers, and skin-enhancing products is expanding adoption. Gender-neutral branding and clean, ethical positioning are further accelerating male participation in the vegan cosmetics market.

Price Range Insights

The Mass price range segment dominates the vegan cosmetics market, accounting for approximately 57% of total unit sales. Competitive pricing has played a critical role in expanding market penetration, enabling wider consumer participation in ethical beauty consumption. Strong availability through drugstores, supermarkets, and large retail chains has reinforced high sales volumes, particularly among students and budget-conscious consumers seeking affordable vegan alternatives.

The Premium segment is emerging as the fastest-growing price category as consumer confidence in the efficacy of vegan cosmetics increases. Demand is increasing for high-performance products that offer long wear, advanced pigmentation, and skin-beneficial formulations. As ethical credentials increasingly align with performance expectations, premium vegan cosmetics are gaining traction among quality-conscious consumers.

Sales Channel Insights

Specialty beauty stores dominate the sales channel landscape, accounting for approximately 40% of total market value. Retailers such as Sephora and Ulta Beauty play a critical role in validating vegan cosmetic brands through curated assortments and in-store labeling. The ability to test shades, textures, and finishes remains essential for cosmetic purchasing decisions, reinforcing the leadership of specialty retail in value generation.

Online retail represents the fastest-growing sales channel, supported by direct-to-consumer expansion and digital engagement strategies. Influencer-led marketing, social commerce, and transparent certification communication are driving rapid online adoption. Younger consumers increasingly favor digital platforms for convenience, product discovery, and ethical brand storytelling.

Regional Insights

North America Vegan Cosmetics Market Trends

North America dominates the global vegan cosmetics market, accounting for approximately 39.2% of total market share, driven primarily by the United States’ strong consumer purchasing power and advanced beauty innovation ecosystem. The region benefits from a well-established indie and celebrity-led beauty landscape, where vegan positioning is closely associated with performance and trend leadership. Strong retail penetration through specialty beauty chains further reinforces regional dominance.

Growth momentum continues to be supported by heightened regulatory oversight and evolving consumer preferences. The enforcement of stricter cosmetic safety regulations has indirectly favored transparent, clean, and vegan formulations. Continuous brand launches, influencer-driven marketing, and high awareness of cruelty-free standards ensure sustained consumer engagement and reinforce North America’s leadership position.

Europe Vegan Cosmetics Market Trends

Europe represents a mature and highly regulated market for vegan cosmetics, underpinned by its early adoption of animal testing bans and strong ethical consumption culture. The region benefits from deep-rooted consumer trust in certified vegan and cruelty-free products, particularly across Germany, the United Kingdom, and France. European consumers place strong emphasis on ingredient transparency, environmental responsibility, and regulatory compliance.

The European vegan cosmetics market is expected to expand at a CAGR of approximately 6.3% over the forecast period, supported by sustainability-driven purchasing behavior. Demand is increasingly shaped by expectations for biodegradable packaging, carbon-neutral logistics, and circular beauty practices. Regulatory harmonization across the European Union further facilitates cross-border trade and accelerates regional market penetration.

Asia Pacific Vegan Cosmetics Market Trends

Asia Pacific is emerging as the fastest-expanding regional market, currently accounting for approximately 32.3% of global market share. Market growth is fueled by a large youth population, rising disposable incomes, and evolving ethical awareness across major economies. Regulatory reforms in key countries have lowered entry barriers for cruelty-free and vegan cosmetic brands, supporting increased regional participation.

The region’s growth trajectory is further strengthened by innovation-led beauty cultures in South Korea and Japan, where vegan formulations are being integrated into advanced cosmetic development. In emerging markets such as India, cultural alignment with non-violent principles and rising urban demand for herbal vegan cosmetics are accelerating adoption. These combined factors position the Asia Pacific as a critical growth engine.

Competitive Landscape

The vegan cosmetics market exhibits a fragmented yet increasingly consolidated competitive structure. While a large number of small and emerging brands continue to enter the space, market power is gradually concentrating among a limited group of high-visibility players. Competition is primarily driven by rapid innovation, with brands differentiating through advanced plant-based ingredient technologies, proprietary formulations, and strong ethical positioning centered on transparency and inclusivity.

Consolidation activity is intensifying as established cosmetic groups seek to strengthen their ethical and clean beauty portfolios. Strategic acquisitions of high-growth vegan brands and expanded omnichannel retail presence are reshaping competitive dynamics. At the same time, pure-play vegan brands are scaling through digital-first strategies, global retail partnerships, and focused brand storytelling to strengthen long-term market positioning.

Key Market Developments:

- In May 2025, e.l.f. Beauty announced its definitive agreement to acquire Rhode, the skincare brand founded by Hailey Bieber, for US$ 1.0 Billion. This strategic move significantly expands e.l.f.'s presence in the prestige skincare category.

- In August 2025, Rare Beauty reached a valuation of approximately US$ 2.7 Billion, driven by the immense success of its Soft Pinch Liquid Blush and expansion into international markets, solidifying its status as a top-tier player.

- In March 2024, Haus Labs by Lady Gaga launched exclusively with Sephora across 12 new European countries, including France, Italy, Germany, and Spain, marking a major international retail expansion for the science-driven vegan brand.

Companies Covered in Vegan Cosmetics Market

- e.l.f. Cosmetics

- Pacifica Beauty

- Milk Makeup

- Haus Labs

- R.E.M. Beauty

- Florence by Mills

- Rare Beauty

- Barry M Cosmetics

- Ecco Bella

- Urban Decay

- Beauty Without Cruelty

- PHB Ethical Beauty

- Bite Beauty

- 100% Pure

- Inika Organic

Frequently Asked Questions

The global vegan cosmetics market is forecast to reach US$ 32.0 billion by 2033, growing at a robust CAGR of 6.7% from 2026 to 2033.

The major drivers include the rise of ethical consumerism, strict government bans on animal testing in regions such as the EU, and the growing "clean beauty" trend, which favors plant-based, non-toxic ingredients.

Facial products segment leads the market with approximately 43% share, driven by high demand for vegan foundations, concealers, primers, and face powders used in daily beauty routines.

North America dominates with around 39.2% market share, supported by high consumer awareness, strong purchasing power, celebrity brand influence, and a dense specialty retail network.

A major opportunity lies in bio-engineered and lab-grown ingredients, such as vegan collagen and proteins, which enable high-efficacy cosmetic products without animal-derived components.