- Food Ingredients & Additives

- Vanilla Market

Vanilla Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Vanilla Market by Variety (Madagascar, Tahitian, Mexican, Indonesian, Others), by Nature (Organic, Conventional), by Form (Whole bean, Liquid extracts, Paste, Powder), by End-user (Food & Beverage, Cosmetics & Personal Care, Pharmaceuticals, Others) and Regional Analysis from 2026 - 2033

Vanilla Market Share and Trends Analysis

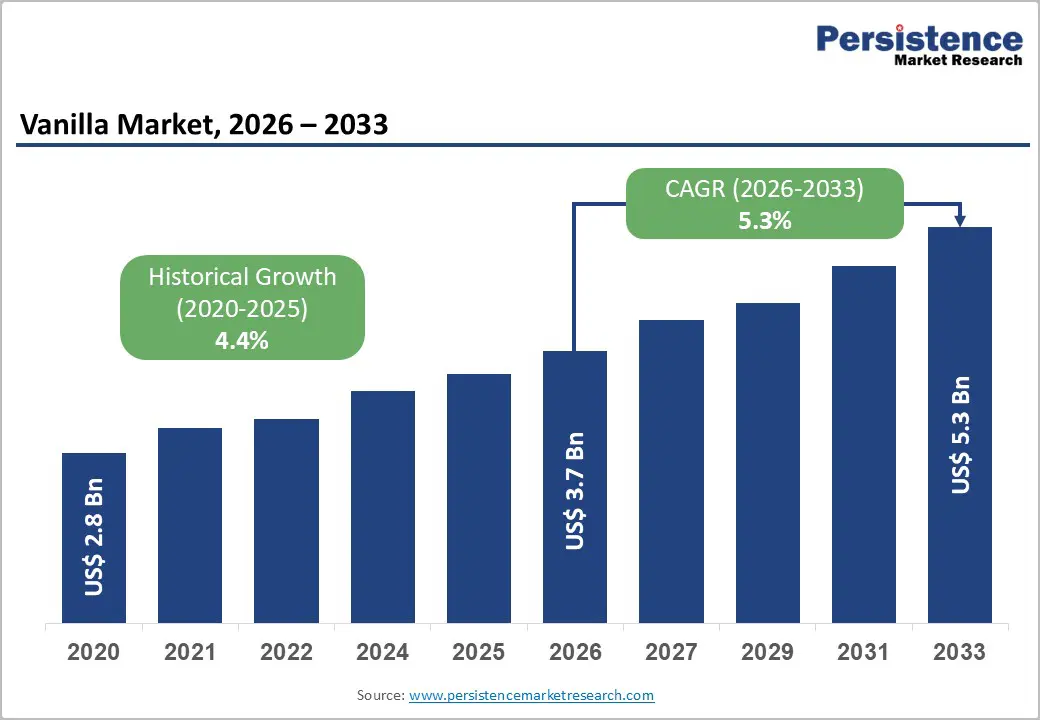

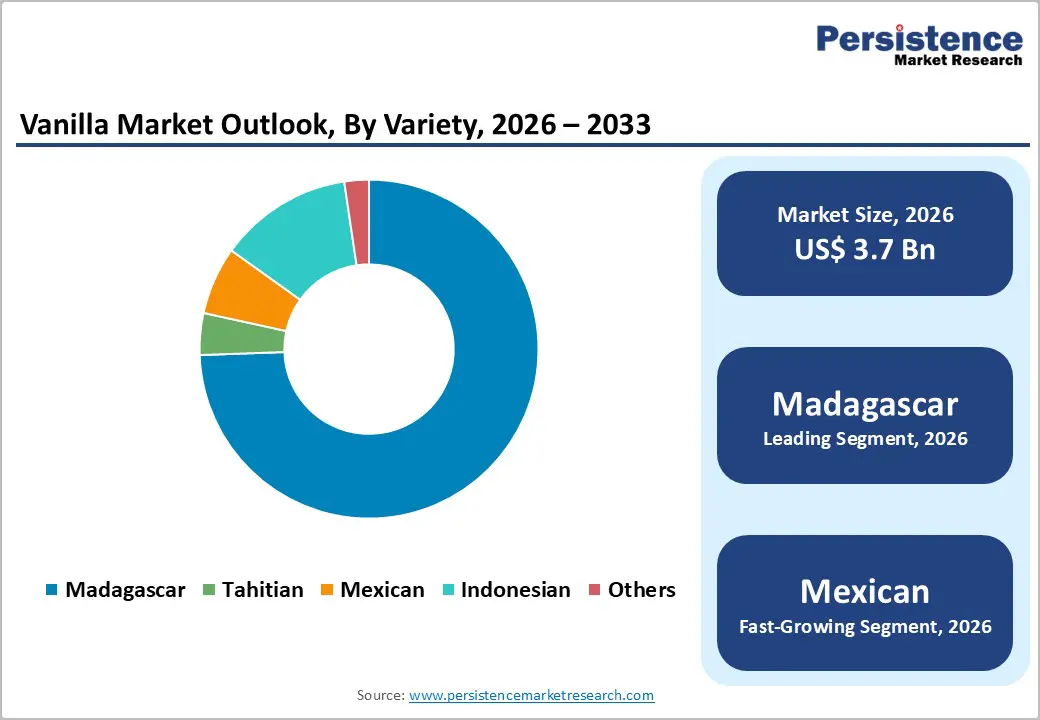

The global vanilla market size is likely to be valued at US$ 3.7 billion in 2026 and projected to reach US$ 5.3 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033.

The market is experiencing dynamic growth as premiumization, clean-label trends, and sustainable sourcing reshape consumer preferences. Increasing demand for natural flavors across bakery, dairy, confectionery, and beverages is driving higher usage intensity, while origin-linked sourcing and organic cultivation are creating opportunities for differentiation and value capture.

Key Industry Highlights:

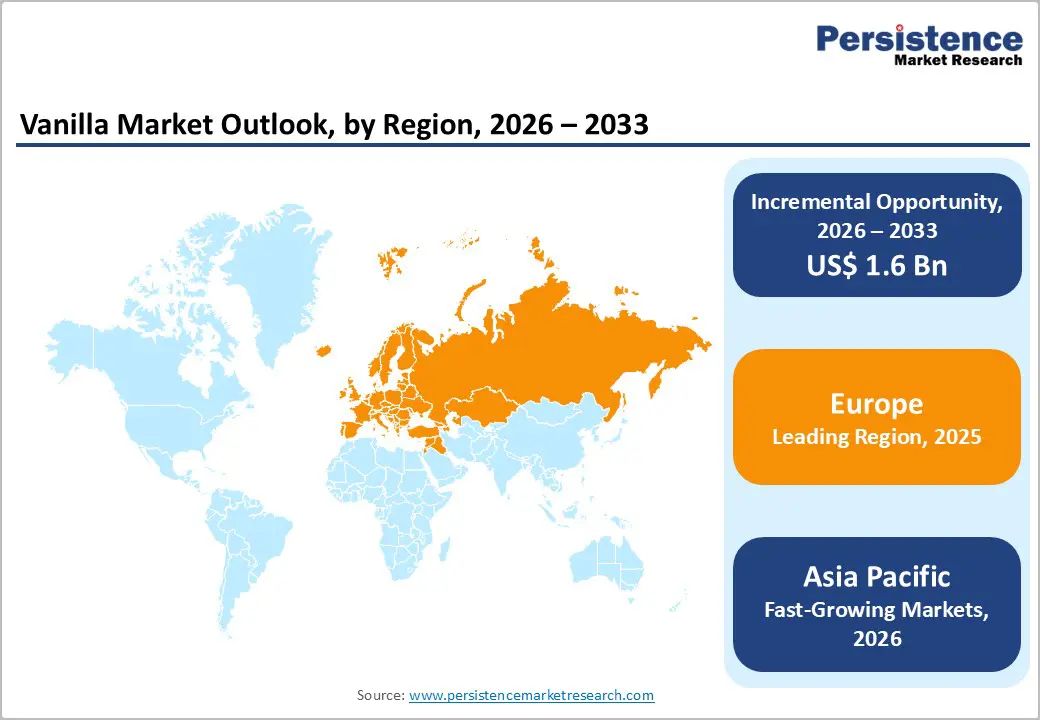

- Leading Region: Europe, holding 32% market share, driven by high consumption of bakery, confectionery, and dairy products, and strong imports by France and Germany.

- Fastest-Growing Region: Asia Pacific, fueled by rising urbanization, disposable incomes, and growing preference for natural and traceable vanilla in India, China, Japan, and South Korea.

- Fastest-Growing Segment: Organic vanilla, driven by clean-label adoption, sustainability focus, and premium positioning across multiple food and beverage categories.

- Growth Indicators: Premiumization of bakery, dairy, confectionery, and beverages increases vanilla usage intensity, while clean-label and origin-specific products enhance consumer trust.

- Opportunities: Building vertically integrated, origin-linked supply chains to secure beans, ensure traceability, and capture premium pricing.

- Key Developments: In November 2025, Coca-Cola unveiled a limited-time creamy vanilla flavor; in August 2025, Vanilla Vida established a 10-hectare facility in Uganda using proprietary indoor cultivation technology; in April 2025, Symrise celebrated World Vanilla Day for the second consecutive year.

| Key Insights | Details |

|---|---|

|

Global Vanilla Market Size (2026E) |

US$ 3.7 Bn |

|

Market Value Forecast (2033F) |

US$ 5.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.4% |

Market Dynamics

Driver - Premiumization of Bakery, Dairy, Confectionery, and Beverages Increases Vanilla Usage Intensity

Luxury cues are quietly rewriting recipes, and vanilla sits at the center of this shift. Premiumization across bakery, dairy, confectionery, and beverages is driving higher vanilla usage intensity as brands chase depth, aroma, and authenticity. Artisanal pastries, indulgent ice creams, fine chocolates, and craft beverages increasingly rely on real vanilla to signal quality and justify premium pricing. Clean-label positioning further elevates natural vanilla over synthetic substitutes, increasing per-unit inclusion rates.

France illustrates this dynamic clearly as a global benchmark for bakery and confectionery excellence. France imported around 2,034 tons of vanilla beans in 2024 to support high-end food production. Chefs and manufacturers favor origin-specific vanilla for flavor layering, reinforcing demand. This premium push strengthens vanilla’s strategic role as a value-enhancing ingredient rather than a background flavor.

Restraints - Labor-intensive cultivation and curing processes limit rapid supply scaling

Vanilla’s high value is built on a production process that is slow by design. Cultivation relies on intensive manual work, including hand pollination of individual flowers and carefully timed harvesting, leaving little room for mechanization. Output growth depends on skilled labor availability and favorable seasonal conditions, making rapid volume expansion difficult when demand rises.

The curing stage creates an additional constraint. Beans must pass through lengthy sweating, drying, and conditioning phases to develop their characteristic flavor, demanding expertise and constant oversight. Mistakes compromise quality and pricing potential, limiting aggressive scale-up. Together, these factors restrict supply flexibility, tightening availability and amplifying volatility across global vanilla markets.

Opportunity - Building vertically integrated, origin-linked supply chain to secure beans and capture premium traceability pricing

Control over origin is becoming a competitive advantage in the vanilla trade. Building vertically integrated, origin-linked supply chains allows companies to secure consistent access to high-quality beans while reducing exposure to price swings and intermediaries. Direct involvement in farming, curing, and primary processing improves quality oversight, stabilizes volumes, and strengthens long-term relationships with growers in key producing regions.

For both established players and startups, traceability unlocks premium pricing. Brands can link vanilla to specific regions, farms, or curing methods, supporting authenticity claims demanded by food, beverage, and fragrance buyers. Transparent sourcing strengthens sustainability narratives, improves forecasting, and enables differentiated storytelling, turning vanilla from a commodity input into a branded, value-generating ingredient across global markets.

Category-wise Analysis

By Variety Insights

Madagascar vanilla nearly holds 73% share as of 2025, reflecting its unmatched combination of scale, quality consistency, and global buyer trust. The island’s humid climate, fertile soils, and long-established curing expertise produce beans with high vanillin content and a rich, creamy profile favored across food, beverage, and fragrance applications. Well-developed export networks and skilled farmer communities enable Madagascar to supply large volumes while meeting stringent quality and traceability requirements.

Other origins play more specialized roles. Tahitian vanilla is prized for floral, fruity notes used in premium desserts and perfumery. Mexican vanilla carries historical significance with deeper, spicier profiles suited to traditional applications. Indonesian vanilla supports industrial demand with smokier characteristics and competitive pricing, complementing Madagascar’s dominance rather than challenging its leadership.

By Nature Insights

Organic vanilla is projected to grow at a CAGR of 7.8% during the forecast period in the global vanilla market, driven by increasing consumer preference for clean-label and naturally sourced ingredients. Shoppers are prioritizing products free from synthetic pesticides, additives, and GMOs, associating organic vanilla with superior taste, safety, and wellness benefits. This trend is reinforcing adoption across bakery, dairy, confectionery, and beverage segments.

Producers are responding with certified organic cultivation, traceable supply chains, and sustainable farming practices that appeal to environmentally and socially conscious consumers. Specialty and premium brands leverage organic vanilla to differentiate offerings, command higher price points, and build brand loyalty. As awareness and demand for natural ingredients expand globally, organic vanilla is poised for sustained market growth.

Region-wise Insights

Europe Vanilla Market Trends

Europe holds approximately 32% share in the global vanilla market, reflecting a mature region with high consumption of bakery, confectionery, and dairy products. The European food and drink market is one of the largest globally, with a turnover of nearly €1.1 trillion according to CBI Netherlands. Growth in vanilla usage is linked to rising demand for natural ingredients and the popularity of processed foods such as chocolate, ice cream, and premium baked goods. France and Germany are by far the largest vanilla importers, supporting industrial-scale production and artisanal applications alike.

In the UK, Spain, and Italy, consumers are increasingly seeking clean-label and origin-specific vanilla, driving premiumization and traceable sourcing. Artisanal chocolates, gelato, and bakery items showcase Tahitian and Madagascar vanillas for distinctive flavor profiles. E-commerce and specialty retail channels are expanding access, while sustainability and ethical sourcing narratives strengthen brand differentiation across the European vanilla market.

Asia Pacific Vanilla Market Trends

Asia Pacific vanilla market is expected to grow at a CAGR of 7.2%, driven by rising urbanization, increasing disposable incomes, and growing demand for natural flavors in confectionery, bakery, and beverages. India is emerging as both a consumer and domestic producer, cultivating small-scale plantations that contribute to local supply and premium domestic blends. China’s expanding middle class and appetite for flavored dairy, ice creams, and bakery items are further boosting vanilla consumption.

In Japan and South Korea, consumers favor clean-label, ethically sourced, and specialty-origin vanilla varieties, with retailers emphasizing traceability and quality. E-commerce and specialty gourmet channels are enabling wider access to premium vanilla products. Regional trends toward artisanal chocolates, high-end desserts, and plant-based beverages continue to strengthen adoption, making the Asia Pacific a key growth hub in the global vanilla market.

Competitive Landscape

The global vanilla market exhibits a moderately fragmented nature, with established multinational suppliers competing alongside agile startups and regional producers. Leading companies are expanding through strategic collaborations, MoUs, and production facility investments to secure high-quality beans and enhance sustainable farming practices. Startups are leveraging traceable, origin-linked supply chains and organic certifications to appeal to premium and health-conscious consumers.

Sustainable cultivation, advanced curing and processing techniques, and adherence to government regulations on pricing and trade support quality consistency and market stability. Strategic trade agreements enable smoother cross-border supply, while synthetic vanilla continues to serve cost-sensitive industrial demand. Rising consumer awareness around natural, ethically sourced vanilla drives companies to innovate and differentiate through origin storytelling, clean-label marketing, and functional product applications, reinforcing the competitive and evolving market landscape.

Key Developments:

- In November 2025, Coca-Cola unveiled a limited-time creamy vanilla flavor positioned for the festive season. The launch targets seasonal indulgence trends, blending classic cola with a smooth vanilla profile to drive short-term consumer excitement and incremental holiday sales.

- In August 2025, Vanilla Vida announced the establishment of a 10-hectare facility in Uganda. The site will deploy the company’s proprietary indoor vanilla cultivation and curing technology, aimed at improving yield consistency, reducing climate dependency, and stabilizing year-round vanilla supply for food and flavor applications.

- In April 2025, Symrise marked World Vanilla Day for the second consecutive year, commemorating the foundation of the modern flavor and fragrance industry.

Companies Covered in Vanilla Market

- Givaudan

- IFF

- Symrise

- DSM-Firmenich

- Kerry Group

- ADM

- McCormick & Company

- Olam

- Nielsen-Massey Vanillas, Inc.

- Takasago International Corporation

- Sensient Technologies

- Others

Frequently Asked Questions

The global vanilla market is projected to be valued at US$ 3.7 Bn in 2026.

Premiumization of bakery, dairy, confectionery, and beverages increases vanilla usage intensity driving the expansion of the global Vanilla market.

The global Vanilla market is poised to witness a CAGR of 5.3% between 2026 and 2033.

The primary market opportunity lies in developing vertically integrated, origin-specific supply chains that ensure consistent access to high-quality beans while enabling companies to command premium pricing through traceable and authentic sourcing.

Major players in the global Vanilla market include Givaudan, IFF, Symrise, DSM-Firmenich, Kerry Group, ADM, Nielsen-Massey Vanillas, Inc., and others.