- Food Ingredients & Additives

- Sweetener Powder Market

Sweetener Powder Market Size, Share, and Growth Forecast, 2026 - 2033

Sweetener Powder Market by Nature (Organic, Conventional), Application (Food & Beverages, Pharmaceutical, Personal Care, Others), Distribution Channel (Online Stores, Supermarkets), and Regional Analysis for 2026-2033

Sweetener Powder Market Share and Trends Analysis

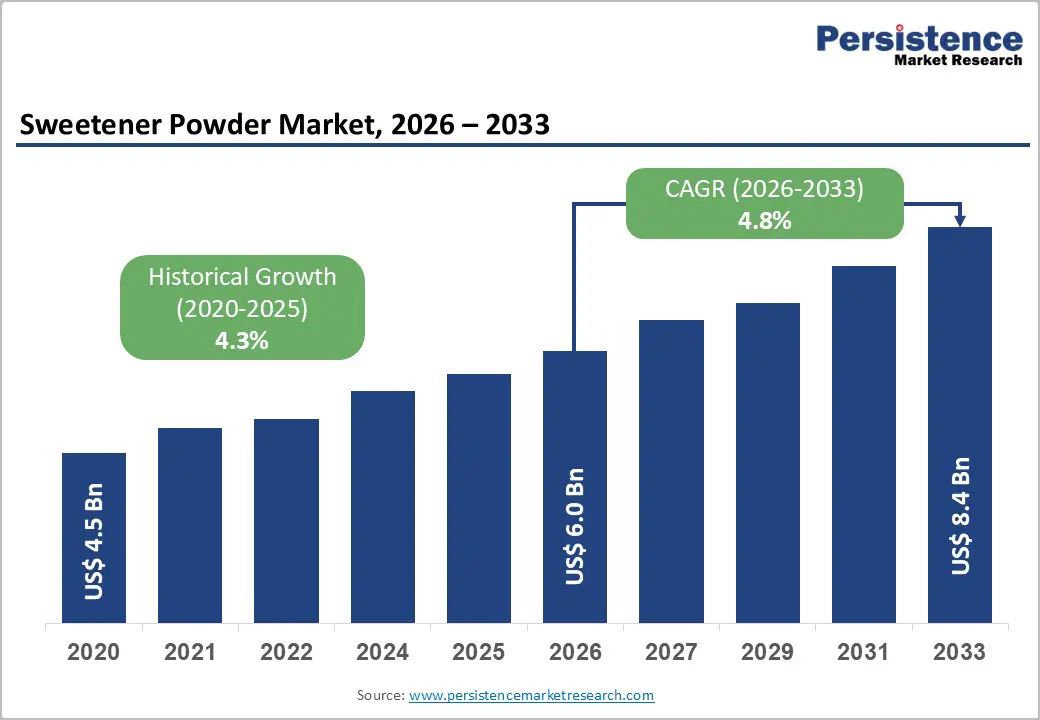

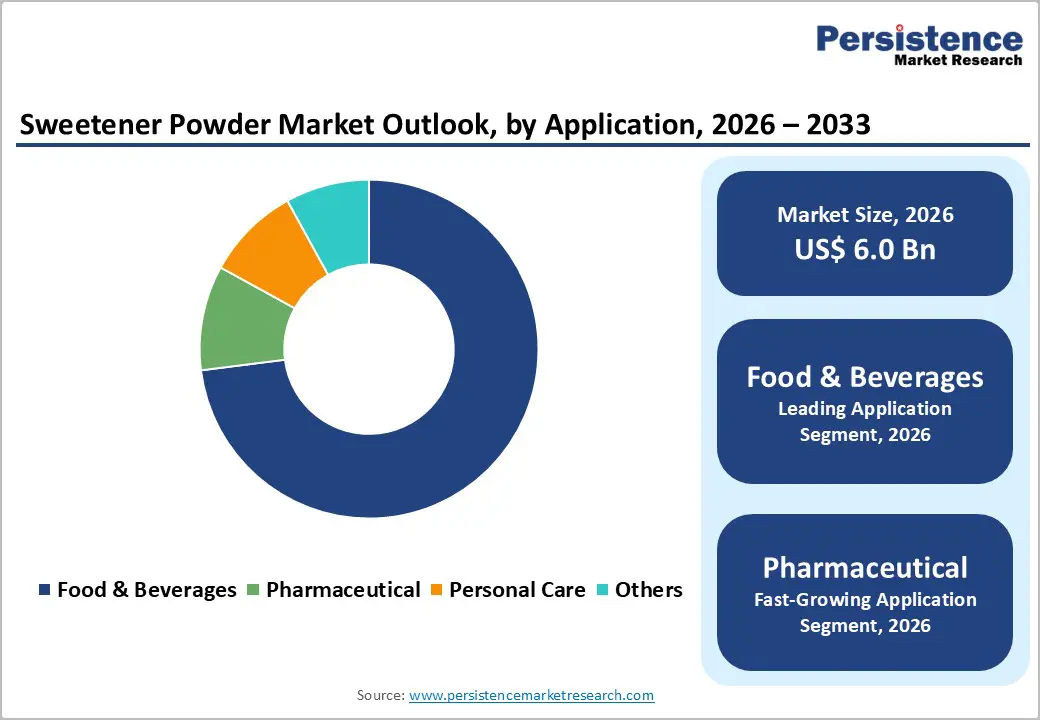

The global sweetener powder market size is likely to be valued at US$ 6.0 billion in 2026, and is projected to reach US$8.4 billion by 2033, growing at a CAGR of 4.8% during the forecast period 2026−2033. This growth trajectory reflects sustained consumer demand for sugar alternatives driven by rising health consciousness and regulatory measures targeting sugar reduction. The market benefits from expanding applications across food and beverage manufacturing,

pharmaceutical formulations, and personal nutrition products. Technological advancements in sweetener processing and formulation have enhanced product stability and taste profiles, while favorable regulatory frameworks in key markets continue to support market expansion through approved ingredient lists and health claim permissions.

Key Industry Highlights

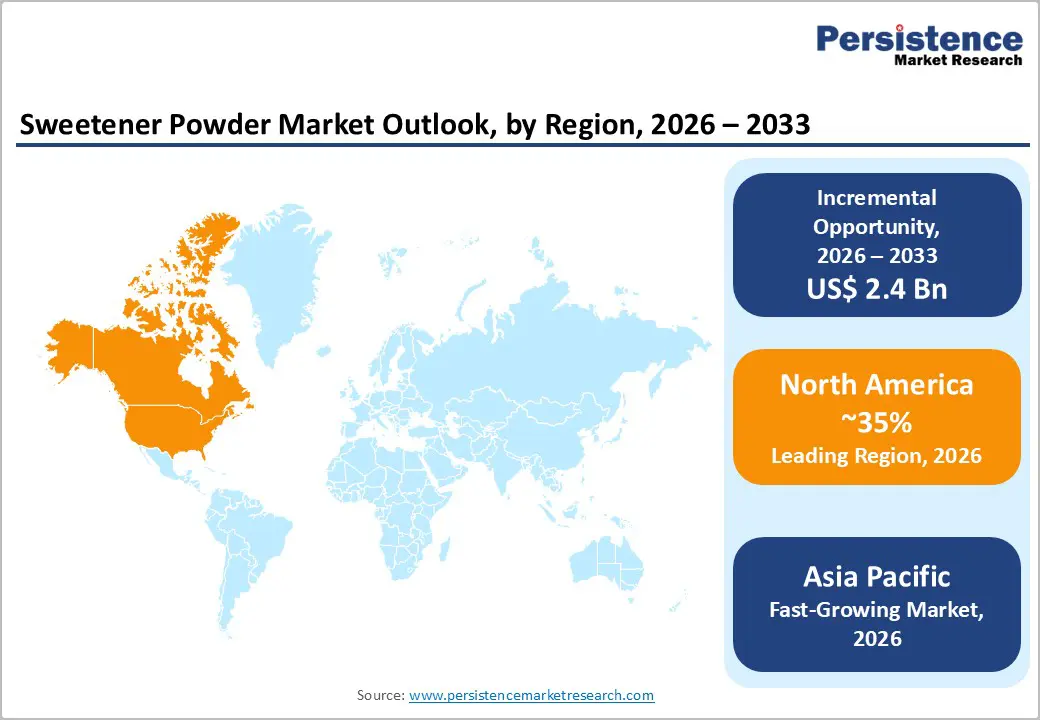

- Dominant Region: North America is expected to command a share of about 35% in 2026, boosted by established consumption habits and advanced food manufacturing bases.

- Fastest-growing Market: Asia Pacific is slated to be the fastest-growing market through 2033, fueled by rapid urbanization and expanding health awareness among consumers.

- Leading & Fastest-growing Nature: Conventional powders are likely to control around 60% of the revenue share in 2026, while organic powders are poised to grow the fastest during the 2026-2033 forecast period.

- Application Dominance: Food & beverages are set to dominate with approximately 73% revenue share in 2026, with pharmaceutical recording the highest growth between 2026 and 2033.

| Key Insights | Details |

|---|---|

| Sweetener Powder Market Size (2026E) | US$ 6.0 Bn |

| Market Value Forecast (2033F) | US$ 8.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Obesity and Diabetes Prevalence

The global rise in obesity is significantly influencing dietary behavior and is driving demand for alternatives to sugar across food and beverage markets. The World Health Organization (WHO) is reporting that approximately one in eight people worldwide were living with obesity in 2022, including about 890 million adults and 160 million children and adolescents, with prevalence rates having doubled among adults and quadrupled among younger populations since 1990. This trend is increasing the risk of metabolic disorders and related health complications, which is encouraging consumers to adopt calorie-reduction strategies. The International Diabetes Federation (IDF) estimates that diabetes affected around 589 million adults aged 20 to 79 years in 2024, with projections reaching approximately 853 million by 2050. As awareness of diet-related health risks is rising, consumers are increasingly choosing low-calorie and zero-calorie sweetener options to manage weight and blood glucose levels.

Governments across North America, Europe, and Asia Pacific are implementing sugar reduction initiatives and public health campaigns to promote healthier dietary habits, which is further strengthening the demand for sugar substitutes. Regulatory measures and fiscal policies are creating strong incentives for food manufacturers to reformulate products using alternative sweetening solutions. For instance, the U.K. has introduced taxation programs including the Soft Drinks Industry Levy (SDIL) to encourage reduced sugar consumption, while Mexico and several European nations are implementing similar policies that penalize high-sugar products. These interventions are motivating companies to incorporate sweetener powders into beverages, processed foods, and functional nutrition products to maintain consumer appeal while meeting regulatory targets.

Technological Advancements in Sweetener Processing

Major food and beverage companies are actively reformulating product portfolios to address rising consumer demand for healthier and lower-calorie options across global markets. Manufacturers are prioritizing categories such as carbonated beverages, dairy products, bakery items, and confectionery to reduce sugar content while maintaining sensory quality and consumer acceptance. Carbonated drinks are often receiving early reformulation attention because of their high sugar concentration, followed by dairy and packaged snack products where ingredient substitution strategies are improving nutritional profiles without compromising taste. Regulatory agencies are supporting these industry transitions by approving new sweetening solutions that meet safety and quality standards. The European Food Safety Authority (EFSA) is authorizing additional sweetener ingredients, while the United States Food and Drug Administration (FDA) is granting Generally Recognized as Safe (GRAS) status to several innovative compounds, which is enabling manufacturers to integrate alternative sweeteners more confidently into commercial formulations.

These regulatory approvals are expanding formulation flexibility and encouraging product innovation across multiple food segments. Consumers are increasingly preferring clean-label products that feature recognizable ingredients and transparent sourcing information, which is strengthening demand for naturally derived sweetener powders. Plant-based sweeteners such as stevia extracts are gaining significant adoption because they provide calorie reduction without compromising sweetness intensity, while monk fruit derivatives are expanding rapidly due to their natural origin and zero-calorie properties. Synthetic sweeteners continue to play an important role in large-scale manufacturing because they offer affordability and stable supply, while natural alternatives are attracting premium market segments that value wellness positioning.

Taste Performance Inconsistency across Application Matrices

Next-generation sweeteners are demonstrating inconsistent sensory performance across different food and beverage categories, which is complicating formulation strategies for manufacturers. Ingredients such as stevia are sometimes producing bitter or metallic aftertastes in applications that involve dairy matrices or acidic beverages, where flavor interactions are more complex. These sensory challenges are limiting the ability to use a single sweetener solution across diverse product portfolios that include beverages, snacks, and processed foods. In contrast, powdered sweeteners often perform more effectively in dry applications such as baked goods and nutritional mixes because heat processing and texture components help mask minor flavor deviations.

Sensory limitations are also preventing complete sugar replacement because alternative sweeteners often fail to replicate the full functional properties of sucrose, including mouthfeel, bulk contribution, and clean flavor finish. Negative consumer experiences with off-notes in one product category can reduce brand trust and discourage repeat purchases across broader product lines. Manufacturers are addressing these challenges by incorporating flavor masking technologies and bitterness modulators that reduce undesirable taste characteristics without altering intended flavor profiles. Industry focus is, therefore, shifting toward creating synergistic blends that combine multiple sweeteners to achieve balanced sweetness intensity at lower usage levels. However, these strategies are increasing formulation complexity and production costs, particularly for large-scale manufacturing operations.

Agricultural Supply Chain Concentration and Climate Vulnerability

The sweetener powder market growth is facing significant supply chain risks because natural raw material production is concentrated in limited geographic regions. Stevia cultivation is largely centered in specific agricultural zones, while monk fruit production is primarily located in southern China, which is creating exposure to climate variability, geopolitical uncertainty, and regional trade policy changes. Weather disruptions such as drought, excessive rainfall, and temperature fluctuations are affecting crop yields, while pest infestations and plant diseases are further increasing production instability. Natural sweetener supply is therefore heavily dependent on agricultural conditions that vary annually, which is complicating production forecasting and long-term procurement planning for manufacturers.

These agricultural dependencies are contributing to price volatility across global markets, as supply shortages can rapidly increase raw material costs and compress profit margins for food ingredient producers. Businesses operating with narrow margins are particularly vulnerable when input prices fluctuate unexpectedly. In contrast, synthetic sweeteners are produced through controlled industrial processes that enable consistent quality and predictable supply availability, which provides greater cost stability. Natural sweetener manufacturers must manage higher operational risk while maintaining competitive pricing across diverse geographic markets. To mitigate these challenges, companies need to diversify sourcing regions, investing in contract farming programs, and establishing partnerships with multiple agricultural suppliers to improve supply resilience.

Innovation in Natural Sweetener Derivation and Hybrid Formulations

Advancements in biotechnology are enabling cost-efficient production of rare natural sweeteners that previously faced supply limitations due to dependence on agricultural cultivation. Precision fermentation techniques are allowing manufacturers to produce target molecules through controlled microbial processes, which is eliminating seasonal variability and ensuring consistent year-round output. Enzymatic conversion technologies are transforming simple substrates into high-value sweetening compounds with improved purity and yield efficiency, which is supporting scalable manufacturing for global markets. Companies are increasingly adopting synthetic biology platforms to expand production capacity and reduce reliance on geographically concentrated crops. These innovations are facilitating commercial development of specialty sweeteners such as thaumatin and brazzein, which are recognized for their high sweetness intensity and clean sensory profiles. Reliable production through biotechnology is strengthening supply stability while enabling manufacturers to meet growing demand across multiple food and beverage applications.

Hybrid formulation strategies are further enhancing product performance by combining multiple sweetening compounds to achieve balanced taste and improved functionality. Synergistic interactions between different ingredients are increasing sweetness perception while reducing undesirable aftertastes, which is allowing manufacturers to optimize formulations for premium product categories. These advanced blends are gaining early adoption in artisanal foods where distinctive flavor quality is essential for differentiation, followed by craft beverages that emphasize layered sensory experiences. Functional nutrition products are also benefiting from these innovations since they support clean-label positioning and wellness-oriented consumer preferences.

Pharmaceutical and Nutraceutical Application Expansion

The pharmaceutical sector is increasingly incorporating sweetener powders into formulations such as tablet coatings, oral suspensions, chewable medications, and pediatric drug products to improve palatability and patient adherence. These applications require stringent quality assurance, including pharmaceutical-grade purity, stability testing, and regulatory compliance to ensure product safety and efficacy. Manufacturers are using advanced purification and processing techniques to meet regulatory standards established by authorities such as the U.S.FDA and the European Medicines Agency (EMA). Because of these rigorous requirements, pharmaceutical applications typically command higher pricing compared with conventional food uses, which is creating attractive revenue opportunities for suppliers that prioritize precision manufacturing and consistent quality control.

Sports nutrition and functional wellness markets are also expanding demand for specialized sweetener blends that enhance product appeal while supporting health-focused consumer preferences. Weight management supplements are incorporating low-calorie sweeteners that align with metabolic health goals, while functional beverages are using ingredients that provide additional benefits such as prebiotic activity and improved blood glucose stability. These formulations are helping improve digestive tolerance and overall consumer experience for physically active populations. Innovation in functional attributes is supporting premium product positioning and sustained growth across specialized nutrition categories.

Category-wise Analysis

Nature Insights

The conventional segment is set to lead with approximately 60% of the sweetener powder market revenue share in 2026, on account of its reliability, scalability, and cost efficiency for large-scale manufacturing applications. Conventional sweetener powders are delivering consistent performance across product categories such as beverages, bakery products, and pharmaceutical formulations, where stable supply and predictable pricing are critical for operational planning. Major ingredient manufacturers are integrating these solutions into reformulated food products through established sourcing networks that ensure continuous availability from key agricultural regions. Broad retail distribution is also supporting segment dominance, as supermarkets and mass-market channels are stocking conventional sweeteners that appeal to price-sensitive consumers who prioritize affordability and accessibility.

The organic segment is expected to record the fastest growth between 2026 and 2033 due to increasing demand from health-conscious consumers seeking clean-label and environmentally responsible ingredients. Certified organic sweetener powders are gaining adoption in functional foods, sports nutrition products, and premium consumer goods, particularly through digital commerce channels that target wellness-focused demographics. Brands are emphasizing sustainable cultivation practices, traceable supply chains, and natural positioning to build consumer trust and brand loyalty among younger urban populations that prioritize dietary transparency. Regulatory support in Europe and North America is encouraging adoption as policies are promoting pesticide-free agricultural inputs and sustainable food production standards. Organic sweeteners are achieving strong penetration in premium product categories such as artisanal beverages, dietary supplements, and specialized nutrition products where consumers are willing to pay higher prices for perceived health and environmental benefits. Expansion of contract farming programs in emerging agricultural regions is further supporting supply availability and accelerating segment growth momentum.

Application Insights

Food and beverage applications are anticipated to hold an estimated 73% of the sweetener powder market share in 2026, driven by widespread product reformulation initiatives focused on reducing sugar content across multiple product categories. Manufacturers are incorporating sweetener powders into beverages such as carbonated drinks, ready-to-drink (RTD) teas, flavored water, and sports beverages to meet consumer demand for lower-calorie alternatives. The beverage sector is demonstrating particularly strong adoption because companies are developing sugar-free and reduced-calorie products that align with health-conscious purchasing behavior. Sweetener powders are also being used in bakery products, dairy items, and confectionery formulations because they enhance flavor perception and maintain desirable texture without increasing caloric value.

The pharmaceutical segment is expected to experience the fastest growth between 2026 and 2033 as drug manufacturers increasingly incorporate sweetener powders into medicinal formulations to improve taste and patient adherence. Sweeteners are being used to mask bitterness from active pharmaceutical ingredients and enhance palatability across dosage forms such as oral suspensions, chewable tablets, and liquid medications. These applications are particularly important in pediatric and geriatric treatments where taste acceptance significantly influences medication compliance. Pharmaceutical companies are responding to demand for innovative drug delivery systems and personalized medicine by integrating advanced sweetener blends that provide both functional performance and patient-friendly sensory profiles. The growing focus on patient-centered healthcare is accelerating adoption across the sector, as sweetener powders offer adaptable formulation solutions that align with evolving therapeutic and regulatory requirements.

Regional Insights

North America Sweetener Powder Market Trends

North America is projected to account for approximately 35% of the sweetener powder market value in 2026, supported by strong consumer demand, advanced food manufacturing infrastructure, and well-established regulatory systems. The United States is driving regional performance due to high consumption of processed foods and beverages combined with widespread reformulation initiatives aimed at reducing sugar intake. Regulatory oversight from the U.S. FDA provides a structured pathway for innovation through the GRAS framework, which is enabling manufacturers to introduce new sweetener ingredients while maintaining safety compliance. Canada is also contributing to regional growth through regulatory alignment with U.S. standards under Health Canada, which is facilitating cross-border product development and commercialization. Consumers across North America are increasingly adopting naturally derived sweeteners such as stevia-based products, reflecting strong health awareness and preference for reduced-calorie dietary options.

Regional growth is also being reinforced by public health initiatives that address obesity and metabolic health concerns, which is encouraging beverage companies and food manufacturers to reformulate products with alternative sweeteners. Dietary trends such as ketogenic and low-carbohydrate nutrition patterns are increasing demand for compatible sweetener powders in snacks, functional foods, and meal replacements. Investment activity is expanding in biotechnology companies that are developing advanced natural sweetener solutions with improved taste performance and functional characteristics. Research and development centers operated by ingredient innovators are focusing on next-generation formulations that combine sensory quality with metabolic benefits. Manufacturers are leveraging these innovations to capture opportunities in functional nutrition, dietary supplements, and performance-oriented food products that support active lifestyles.

Europe Sweetener Powder Market Trends

Europe is foreseen to maintain a strong market position due to its advanced food processing capabilities and consumer preference for natural and reduced-sugar ingredients. Germany is leading regional demand with well-developed manufacturing infrastructure and extensive retail distribution networks, including major supermarket chains such as Aldi and Lidl that are expanding private-label sugar-free product offerings. The U.K. is influencing market dynamics through fiscal policies such as the SDIL, which is encouraging beverage manufacturers to reformulate products and reduce sugar content. France and Spain are also contributing to growth through evolving dietary patterns that adapt traditional Mediterranean foods into lower-sugar variants, while demand for diabetes management and wellness-oriented products is increasing across these markets.

Regulatory oversight from the EFSA and the European Commission (EC) is ensuring rigorous safety evaluation and approval processes for new sweetener ingredients before market entry across European Union member states. Scientific assessment panels are validating safety profiles and enabling pan-European commercialization once approval is granted. Recent regulatory developments include approvals for advanced sweeteners such as advantame and ongoing evaluations of innovative compounds derived from fermentation technologies and protein-based sweeteners such as thaumatin derivatives. Consumers are also widely using tabletop sweeteners in household settings, which is supporting retail demand. Major ingredient suppliers including Südzucker, Tate & Lyle, and Tereos are maintaining strong regional influence through large-scale production facilities located in countries such as the Netherlands, Belgium, and Germany.

Asia Pacific Sweetener Powder Market Trends

Asia Pacific is poised to emerge as the fastest-growing market for sweetener powders, driven by rapid urbanization, rising disposable incomes, and increasing awareness of metabolic health concerns among consumers. China is leading regional growth through government initiatives focused on diabetes and obesity prevention, which are encouraging food manufacturers to reduce sugar content in processed products. Expansion of the urban middle class is increasing demand for packaged foods and beverages, while large-scale manufacturing facilities are supporting both domestic consumption and export opportunities. Japan is contributing through demand for premium products that emphasize subtle sweetness profiles and natural ingredients, particularly in low-calorie confectionery and functional beverages.

India is also experiencing rapid expansion due to growing diabetes prevalence, improving retail infrastructure, and public health campaigns that promote healthier dietary choices. Government programs such as the Food Safety and Standards Authority of India (FSSAI) Eat Right India initiative are encouraging sugar reduction across food categories, which is increasing adoption of alternative sweeteners. Prime ASEAN economies, mainly Indonesia, Thailand, Vietnam, and the Philippines, are benefiting from urban lifestyle shifts and multinational investment in localized food production. The region is gaining competitive advantages from proximity to agricultural raw material sources, particularly stevia cultivation in China, which supports supply availability. Pharmaceutical manufacturing growth in India and China is also contributing to demand for sweetener powders used in medicinal formulations due to cost-effective production capabilities.

Competitive Landscape

The global sweetener powder market structure is moderately consolidated. Tate & Lyle, Cargill, Ingredion, Ajinomoto, Südzucker, and Roquette collectively account for approximately 40% of total market share. These multinational ingredient manufacturers are maintaining strong competitive positions through extensive distribution networks, diversified product portfolios, and significant investment in research and development capabilities. Market competition is intensifying as demand rises for low-calorie and naturally derived sweetening solutions across food, beverage, and pharmaceutical applications. Established companies are focusing on technological innovation to improve taste performance, enhance functional properties, and ensure regulatory compliance, which is enabling them to introduce new products that address evolving consumer preferences and health-oriented market trends.

Competitive differentiation is increasingly based on ingredient functionality, clean-label positioning, and product safety assurance, particularly within health-conscious consumer segments. Leading players are expanding portfolios through the development of next-generation sweeteners and strategic acquisitions that strengthen technological capabilities and geographic reach. Emerging companies are also entering the market with specialized natural sweetener solutions that target premium applications, which is increasing competitive pressure on established firms. The ability to align product development with regulatory standards and consumer wellness expectations is becoming a critical factor for long-term competitive success in the sweetener powder industry.

Key Industry Developments

- In July 2025, Icon Foods introduced a new sweetener formulation combining stevia glycosides such as rebaudioside M (Reb M) and rebaudioside D (Reb D) to deliver a more sugar-like taste profile, addressing aftertaste challenges and enabling broader use in reduced-sugar food and beverage applications.

- In April 2025, Waterful, a plant-based hydration brand from Bengaluru, launched BerryCola on a pioneering caffeine-free, powdered cola hydration mix that blends natural berry flavors, cola essence, betanin for color, stevia, minimal unrefined sugar, electrolytes, vitamins, and minerals.

- In March 2025, India inaugurated its first-of-its-kind green stevia processing plant in Himachal Pradesh, developed with technical support from the Council of Scientific and Industrial Research–Institute of Himalayan Bioresource Technology (CSIR-IHBT), to convert stevia leaves into steviol glycoside powder.

Companies Covered in Sweetener Powder Market

- Tate & Lyle PLC

- Cargill, Incorporated

- Ingredion Incorporated

- Ajinomoto Co., Inc.

- Südzucker AG

- Roquette Frères

- Archer Daniels Midland Company

- JK Sucralose Inc.

- Celanese Corporation

- NutraSweet Company

- Sweegen, Inc.

- GLG Life Tech Corporation

- Pure Circle Limited

- Zydus Wellness Limited

Frequently Asked Questions

The global sweetener powder market is projected to reach US$ 6.0 billion in 2026.

The market is driven by growing health consciousness, surging diabetes and obesity prevalence, and sugar reduction regulations.

The market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Major opportunities lie in natural/organic expansion in emerging markets, functional food integration, and biotech for cost-effective rare sweeteners.

Tate & Lyle PLC, Cargill, Incorporated, Ingredion Incorporated, Ajinomoto Co., Inc., Südzucker AG, and Roquette Frères are some of the key players in the market.