- Processed Food

- Sourdough Market

Sourdough Market Size, Share, and Growth Forecast 2026 - 2033

Sourdough Market by Product Type (Type I, Type II, Type III), Ingredient (Wheat, Barley, Oats, Rye), Application (Bread, Cookies, Cakes, Waffles, Pizza, Others), and Regional Analysis, 2026 - 2033

Sourdough Market Share and Trends Analysis

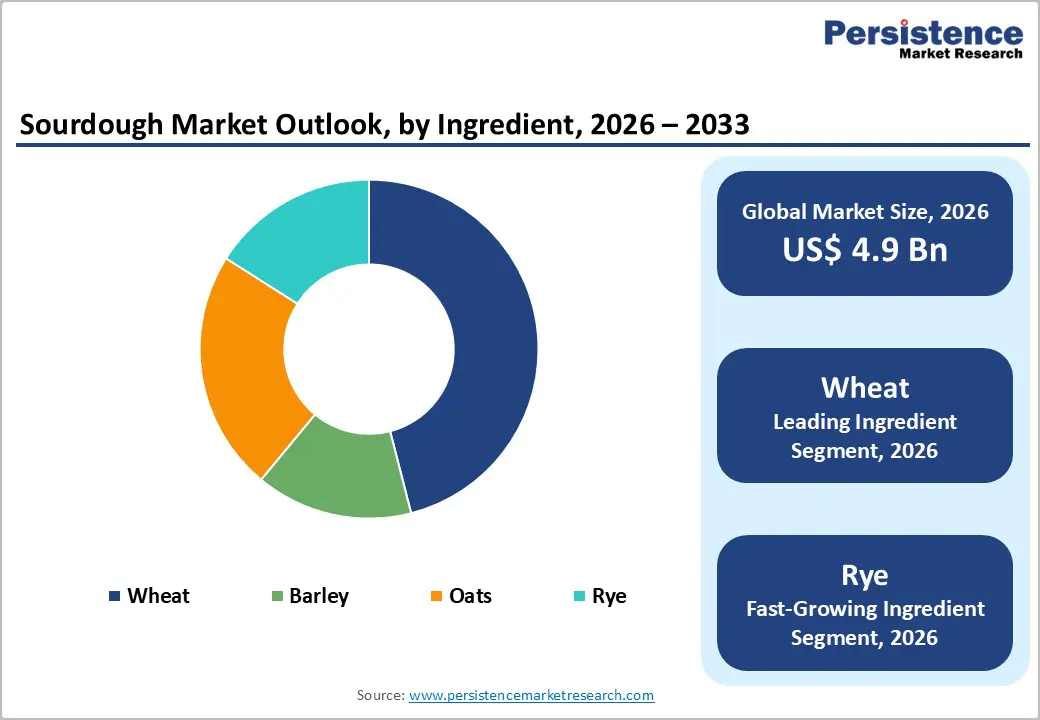

The global sourdough market size is expected to be valued at US$ 4.9 billion in 2026 and projected to reach US$ 8.2 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033.

The shift in consumer preference toward fermented, clean-label, and artisan bakery products. Health-conscious consumers are increasingly turning to sourdough owing to its lower glycemic index, enhanced digestibility, and natural preservation properties compared to conventional bread. The post-pandemic home-baking movement catalyzed mainstream familiarity with sourdough fermentation, while expanding foodservice and retail availability, particularly across Europe and North America, has solidified sourdough's transition from an artisan niche to a mainstream category.

Key Industry Highlights

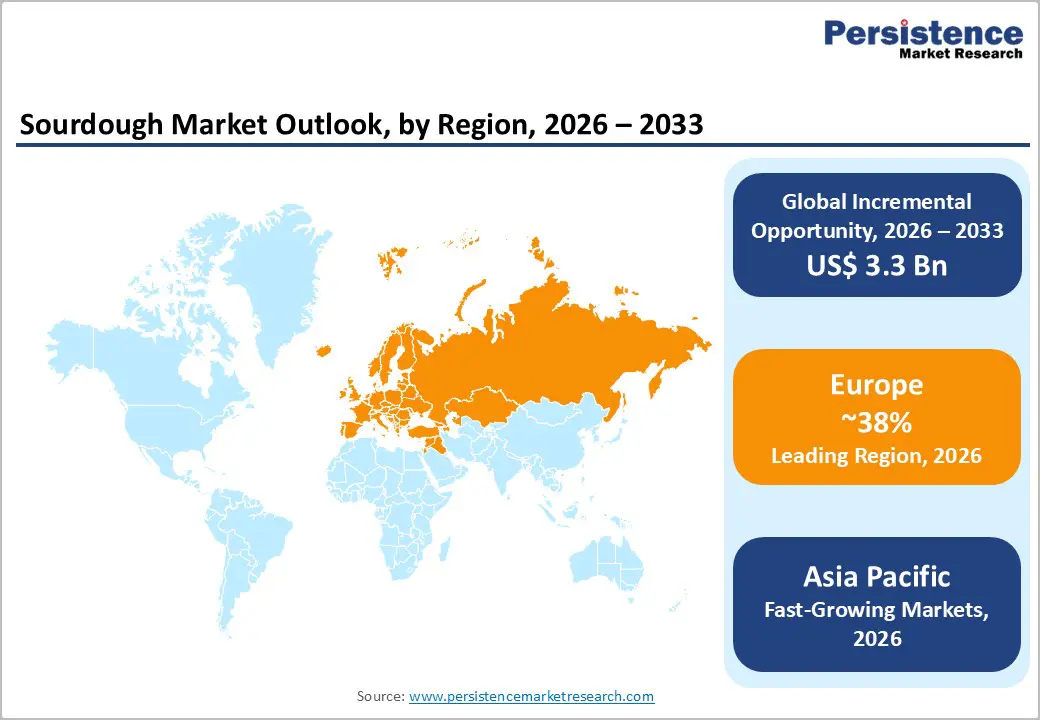

- Leading Region: Europe leads the global sourdough market with approximately 38% market share in 2025, anchored by centuries-old fermented bread traditions, mature artisan bakery networks, and strong consumer demand for authentic, clean-label sourdough products across Germany, France, and the U.K.

- Fastest-Growing Market: Asia Pacific is the fastest-growing regional market for sourdough over 2026–2033, driven by rapid urbanization, rising disposable incomes, expanding specialty bakery culture, and growing Western dietary influence in China, India, Japan, and Southeast Asia.

- Dominant Ingredient Type: Wheat is the leading ingredient with approximately 46% market share in 2025, driven by widespread agricultural availability, superior gluten properties for sourdough texture development, and deep consumer familiarity with wheat-based artisan bread globally.

- Fast-Growing Ingredient Type: Rye sourdough is the fast-growing ingredient segment over 2026–2033, propelled by its superior dietary fiber content, low glycemic index, alignment with the globally trending Nordic diet, and growing clinical evidence supporting its health benefits.

- Key Opportunity: Expanding sourdough into emerging applications, including pizza bases, crackers, and confectionery alongside growing organic and clean-label product ranges, offers manufacturers significant incremental revenue opportunities and differentiated brand positioning across premium global retail and foodservice channels.

Market Dynamics

Drivers - Growing Consumer Preference for Fermented and Gut-Health-Promoting Foods

The global gut health movement has emerged as one of the most powerful drivers of demand for the sourdough market. Sourdough fermentation produces lactic acid bacteria (LAB) that improve nutrient bioavailability, reduce antinutrients such as phytic acid, and support digestive health benefits increasingly recognized by mainstream consumers.

According to the International Scientific Association for Probiotics and Prebiotics (ISAPP), consumer awareness of gut microbiome health has grown substantially, with fermented foods commanding premium positioning in health food retail. A 2022 survey by the International Food Information Council (IFIC) found that over 40% of U.S. consumers actively sought fermented foods for digestive health benefits. This scientifically supported consumer narrative has elevated sourdough beyond a taste preference into a functional food category, fueling consistent volume and value growth across multiple geographies and retail formats.

Surging Popularity of Artisan Bakery and the Clean-Label Food Movement

The global clean-label food movement has been a transformative structural driver for sourdough adoption across the bakery. Consumers are increasingly scrutinizing ingredient lists and rejecting synthetic preservatives, emulsifiers, and additives in packaged bread, a concern documented by the European Food Safety Authority (EFSA) and reflected in the rapid growth of natural and organic bakery categories. Sourdough bread, produced through traditional fermentation with minimal ingredients: flour, water, salt, and a live starter culture, aligns perfectly with clean-label consumer values.

According to the American Bakers Association (ABA), the artisan and specialty bread segment in the United States has grown at over twice the rate of conventional packaged bread in recent years, reflecting rising premiumization and the sustained commercial momentum of artisan fermented bakery products.

Restraints - Extended Production Time and Complex Manufacturing Scalability

Authentic sourdough production relies on slow fermentation cycles of 12 to 48 hours, requiring precise temperature and humidity control, skilled artisan knowledge, and substantial fermentation infrastructure. This inherent production complexity makes industrial scalability significantly more challenging and more costly than in conventional yeast-leavened bread manufacturing.

Large bakery operators face difficulties maintaining starter culture consistency across high-volume production lines, and any starter failure can compromise entire production batches. These operational constraints increase cost-per-unit and limit the ability of mass-market manufacturers to compete on price with conventional bread without compromising the authentic characteristics that drive consumer preference.

Short Shelf Life Compared to Commercially Produced Bread

Authentic sourdough bread, produced without synthetic preservatives, has a materially shorter shelf life than commercially produced loaves, typically remaining fresh for 3 to 5 days versus 2 to 4 weeks for preservative-treated conventional bread. This characteristic limits the distribution radius and increases the risk of food waste, creating supply chain challenges for manufacturers targeting long-distance retail logistics or export markets. The Food and Agriculture Organization (FAO) estimates that approximately 14% of food is lost between harvest and retail globally, with perishable bakery products particularly vulnerable to this constraint that compounds margin pressure for premium sourdough brands seeking wider geographic distribution.

Opportunities - Expanding Rye Sourdough Demand Driven by Nordic Dietary Trends and Health Positioning

Rye sourdough represents one of the most compelling growth opportunities within the global sourdough market and is identified as the fastest-growing ingredient segment over 2026–2033. Rye-based sourdough delivers superior dietary fiber content, a markedly lower glycemic index compared to wheat sourdough, and distinctive flavor profiles that resonate with health-conscious and premium-oriented consumers.

The Nordic diet, recognized by the World Health Organization (WHO) as one of the healthiest dietary patterns globally, centers on rye bread as a staple, providing manufacturers with a credible health narrative to support global market expansion. Growing consumer awareness of fiber intake recommendations from the European Food Information Council (EUFIC) and clinical evidence supporting rye's blood sugar management properties create a strong foundation for premiumzing rye sourdough across health food, specialty retail, and professional foodservice channels internationally.

Untapped Application Potential in Sourdough-Based Snacks, Pizzas, and Confectionery

While bread remains the dominant application for sourdough, the fermented culture's flavor enhancement, textural properties, and clean-label credentials present compelling innovation opportunities across a broader spectrum of bakery and snack applications. Sourdough-leavened pizza bases, crackers, cookies, and waffle mixes are gaining notable traction on specialty retail and foodservice menus across North America and Europe. Companies investing in ready-to-bake sourdough mixes, frozen sourdough pizza bases, and sourdough-infused snack crackers can leverage consumer familiarity with the sourdough flavor profile to drive incremental category revenues and capture emerging demand at the intersection of convenience, health, and artisan food culture.

Category-wise Analysis

Product Type Insights

Type I sourdough leads the global sourdough market by product type, commanding approximately 52% of total market share in 2025. Type I sourdough, characterized by continuous or traditional fermentation at ambient temperatures using active, living starter cultures, is the authentic artisan standard that underpins the category's premium consumer positioning and health-driven demand narrative. It delivers the full spectrum of sensory and nutritional benefits associated with sourdough: complex flavor profiles, lower phytic acid content, improved mineral bioavailability, and natural preservation.

The Sourdough School (UK) and academic research published in the journal Cereal Chemistry confirm that Type I processes maximize beneficial populations of lactic acid bacteria. Specialist artisan bakeries, premium retail brands, and health-oriented foodservice operators predominantly use Type I sourdough, reinforcing its commercial dominance.

Ingredient Analysis

Wheat is the dominant ingredient in the global sourdough market, accounting for approximately 46% of total market share in 2025. Wheat's leadership stems from its widespread agricultural availability, well-understood gluten development properties that deliver the characteristic open crumb and chewy texture of sourdough, and deep-rooted consumer familiarity with wheat-based bread across global markets.

According to the International Grains Council (IGC), wheat remains the world's most widely produced and traded cereal grain, ensuring a consistent raw material supply and price competitiveness for wheat sourdough manufacturers. Major commercial bakery operators and artisan producers alike predominantly work with wheat flour, benefiting from robust ingredient supply chains. Rye is identified as the fastest-growing ingredient segment, driven by its health differentiation and alignment with Nordic dietary trends, gaining global popularity.

Application Insights

Bread is the dominant application in the global sourdough market, accounting for approximately 65% of total market share in 2025. Sourdough bread is the foundational and most historically established product in the category, with deep cultural roots in Europe, North America, and parts of Asia. The application benefits from daily consumption patterns, strong consumer repeat purchase behavior, and the premium price positioning that artisan sourdough loaves command in both retail and foodservice settings.

According to the Grain Foods Foundation, bread remains the most frequently purchased bakery item in the United States, with sourdough being the fastest-growing variety. Pizza and cookies are emerging as high-growth adjacent applications, as food manufacturers and restaurants incorporate sourdough fermentation to differentiate products through flavor complexity and clean-label narratives.

Regional Insights

North America Sourdough Market Trends and Insights

North America is a major and well-established market for sourdough, driven by the region's vibrant artisan bakery culture, health-conscious consumer base, and a deeply entrenched sourdough heritage particularly on the West Coast of the United States. The rapid expansion of specialty grocery chains and growing foodservice integration of sourdough menus are sustaining strong demand. Clean-label awareness and gut health trends continue to fuel premiumization across retail and direct-to-consumer channels in the region.

U.S. Sourdough Market Size

The United States dominates the North American sourdough market, accounting for approximately 85% of regional revenue, with an estimated market value of around US$ 900 million in 2026. San Francisco's iconic sourdough heritage, the post-pandemic home-baking boom, and thriving artisan-bakery ecosystems in major metropolitan areas collectively underpin the U.S. market's strong commercial performance.

Europe Sourdough Market Trends and Insights

Europe leads the global sourdough market with approximately 38% share in 2025, supported by centuries-old fermented bread traditions and a mature artisan bakery culture embedded in consumer dietary habits across Germany, France, the U.K., and Scandinavia. The region's robust organic and clean-label food regulatory framework, strong independent bakery networks, and growing premium retail demand for authentic sourdough products continue to reinforce its global leadership position through the forecast period.

Germany Sourdough Market Size

Germany is Europe's largest sourdough market, estimated at approximately US$ 620 million in 2026 and representing around 33% of the European market. Germany's deep-rooted rye and mixed-grain sourdough bread culture, with over 300 registered bread varieties recognized by UNESCO and thriving artisan bakery networks, underpins sustained demand and premium product positioning.

U.K. Sourdough Market Size

The United Kingdom is a rapidly expanding sourdough market within Europe, estimated at approximately US$ 340 million in 2026 and holding around 18% of the European market. The U.K. Real Bread Campaign, premium bakery chains, and the rise of sourdough subscription delivery services have collectively driven strong consumer engagement and category growth across urban and suburban markets.

Asia Pacific Sourdough Market Trends and Insights

Asia Pacific is the fastest-growing region for the global sourdough market, driven by rapid urbanization, rising disposable incomes, and growing Western bakery influence in countries such as China, India, Japan, and Australia. China is the region's largest and most dynamic market, where a growing middle class and expanding premium bakery chains in tier-1 cities are fueling sourdough demand. Increasing health awareness and the popularity of European-style artisan bakeries are key demand drivers accelerating category growth across the region.

India Sourdough Market Size

India's sourdough market is at a nascent yet high-potential stage of development, estimated at approximately US$85 million in 2026, representing around 6% of the Asia-Pacific market. Rising urban health consciousness, the expansion of specialty bakery-café culture in metros such as Mumbai, Bengaluru, and Delhi, and the growing availability of sourdough products in premium supermarkets are laying the foundation for accelerated growth.

Japan Sourdough Market Size

Japan's sourdough market is estimated at approximately US$ 175 million in 2026, accounting for around 13% of the Asia Pacific market. Japanese consumers' affinity for fermented foods, precision craftsmanship, and premium artisan bakery products has created fertile ground for sourdough adoption. High-quality artisan sourdough bakeries and imported European sourdough brands have established a discerning premium consumer segment.

Competitive Landscape

The sourdough market is highly competitive, characterized by a mix of artisanal bakeries, large-scale commercial bakers, ingredient suppliers, and frozen bakery product manufacturers. Companies compete through product innovation, clean-label formulations, organic and gluten-free offerings, and the use of heritage grains such as rye and spelt.

Strong emphasis is placed on authenticity, traditional fermentation methods, and premium taste profiles to attract health-conscious consumers. Expansion of frozen and ready-to-bake sourdough products is further intensifying competition in retail and foodservice channels. Strategic partnerships, regional expansion, and private-label offerings also play a major role in strengthening market presence.

Key Developments:

- In June 2025, U.K.-based Jason’s Sourdough introduced two new product lines, namely, Jason’s Everyday Seeded Protein Rolls and Jason’s Sourdough Creations. With the former product line, the brand aims to provide a high-protein and convenient format without compromising on taste. Jason’s Sourdough Creations line combines conventional sourdough with unique flavors.

- In May 2025, Home baker Rachel Pardoe launched her first-ever sourdough starter kit made to help other home bakers enhance their sourdough skills. This premium sourdough kit includes a high-accuracy digital scale, a customized bench scraper, an eco-friendly reusable bowl cover, a lab-dehydrated starter cultivated from Pardoe’s starter, and a few other items.

Global Sourdough Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 3.3 billion |

|

Current Market Value (2026) |

US$ 4.9 billion |

|

Projected Market Value (2033) |

US$ 8.2 billion |

|

CAGR (2026–2033) |

7.6% |

|

Leading Region |

Europe, ~38% market share (2025) |

|

Dominant Product Type |

Type I Sourdough, ~52% market share (2025) |

|

Top-Ranking Ingredient |

Wheat, ~46% market share (2025) |

|

Incremental Opportunity |

US$ 3.3 billion (Absolute Dollar Opportunity) |

Companies Covered in Sourdough Market

- Puratos

- Riverside Sourdough

- Boudin Bakery

- Gold Coast Bakeries (Queensland) Pty Ltd.

- Lallemand

- Alpha Baking Company, Inc.

- Truckee Sourdough Company

- Bread SRSLY

- The Acme Bread Company

- Josey Baker Bread

- Morabito Baking Co. Inc.

- Others

Frequently Asked Questions

The global sourdough market is expected to be valued at US$ 4.9 billion in 2026.

The primary demand drivers include the growing global gut health movement documented by the International Scientific Association for Probiotics and Prebiotics (ISAPP), the surging clean-label and artisan food consumer trend, and the post-pandemic home baking movement that introduced sourdough fermentation to mainstream consumers. Expanding retail and foodservice distribution of premium sourdough products is further accelerating market growth.

Europe leads the global sourdough market with approximately 38% of market share in 2025. Its dominance is underpinned by centuries-old sourdough fermentation traditions, a highly mature artisan bakery industry, UNESCO-recognized bread heritage in Germany, and robust consumer demand for authentic, premium, and clean-label sourdough products across key European markets.

Key opportunities include the premiumization of rye sourdough targeting health-conscious consumers aligned with the WHO-endorsed Nordic diet, expansion of sourdough into adjacent applications such as pizza bases, crackers, and functional snacks, and market entry into high-growth Asia Pacific markets where urbanization and rising disposable incomes are rapidly building sourdough consumer demand.

The leading companies in the global sourdough market include Puratos, Lallemand, Boudin Bakery, Alpha Baking Company, Inc., The Acme Bread Company, Bread SRSLY, Josey Baker Bread, Lesaffre, and Aryzta AG, among others. These players compete on fermentation technology, starter culture authenticity, clean-label formulation, and geographic expansion strategies.