- Food Ingredients & Additives

- Bakery Ingredients Market

Bakery Ingredients Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Bakery Ingredients Market by Ingredient Type (Flour & Starches, Sweeteners, Emulsifiers, Leavening Agents, and Others), by Form (Dry, Liquid, and Paste), by Application (Bread, Cakes & Pastries, Cookies & Biscuits, Rolls & Pies, and Others) by Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Convenience Stores, Online Retail, and B2B Ingredient Suppliers), and Regional Analysis from 2026 - 2033

Bakery Ingredients Market Share and Trend Analysis

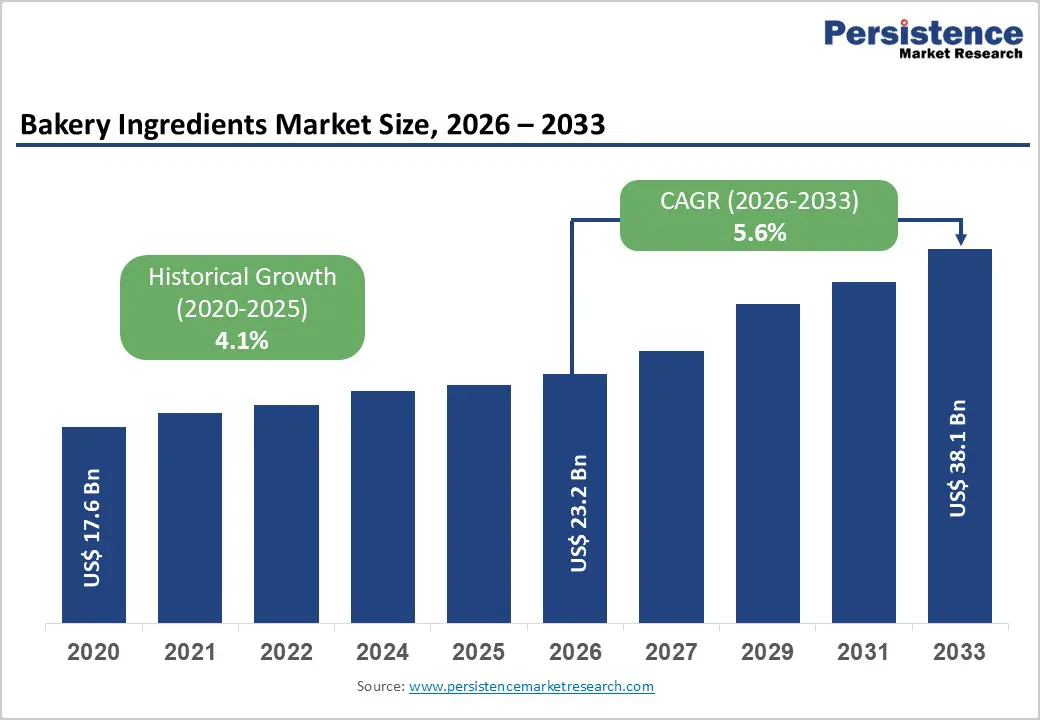

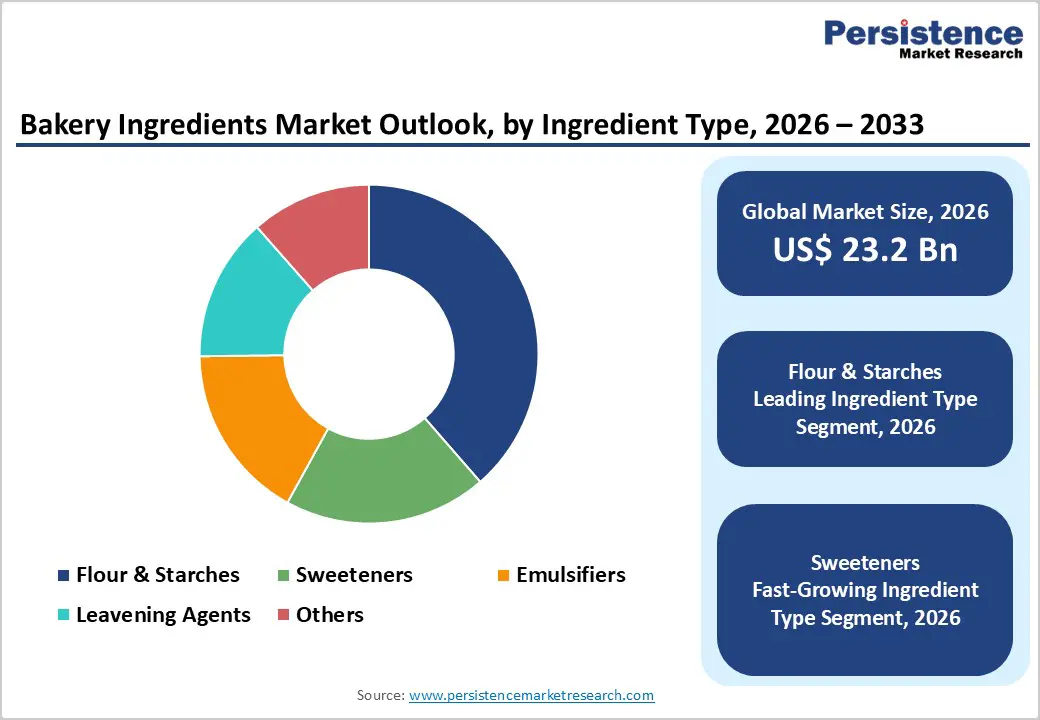

The global bakery ingredients market size is estimated to grow from US$ 23.2 Bn in 2026 to US$ 38.1 Bn by Bn 2033. The market is projected to record a CAGR of 5.6% during the forecast period from 2026 to 2033.

Global demand for bakery ingredients continues to rise as consumption of packaged baked goods increases across both developed and emerging economies. Products such as bread, cookies, cakes, and pastries require a wide range of ingredients including flour systems, sweeteners, emulsifiers, and leavening agents to maintain texture, flavor, and shelf stability during large-scale production. Rapid urbanization, changing dietary habits, and busy lifestyles have encouraged consumers to purchase ready-to-eat bakery foods, strengthening demand for specialized ingredient solutions used by industrial bakeries and foodservice providers. Additonally, manufacturers are investing in improved ingredient formulations that enhance dough performance, extend product freshness, and support consistent quality during mass production. Growing interest in premium baked goods, functional food products, and convenient snack items is also influencing ingredient innovation. Advances in food processing technologies and enzyme-based baking systems are enabling manufacturers to optimize production efficiency while maintaining desirable taste and texture characteristics. Expanding retail bakery chains, increasing demand for packaged convenience foods, and the growing presence of commercial bakery operations are expected to sustain steady expansion of the bakery ingredients sector across global markets.

Key Industry Highlights

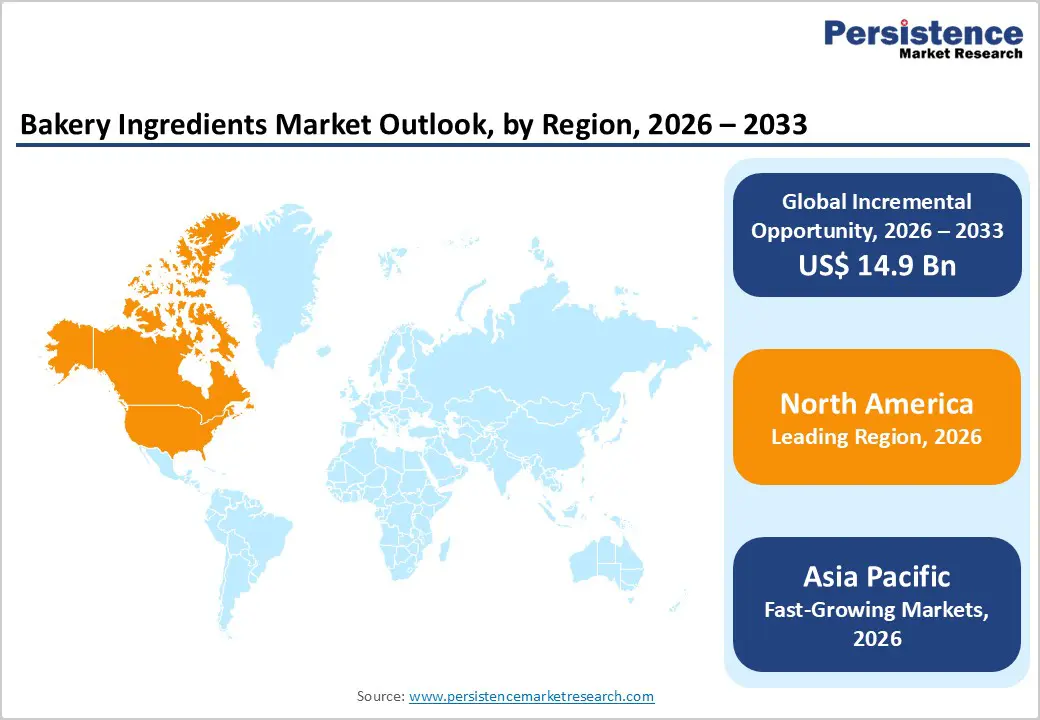

- Leading Region: North America accounts for 48.5% of global revenue, supported by a highly developed food processing industry, strong consumption of packaged bakery products, and the presence of large industrial bakeries and ingredient manufacturers.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing region, driven by rapid urbanization, rising disposable incomes, expanding retail food chains, and increasing demand for packaged bread, cakes, and bakery snacks.

- Leading Product Segment: Flour & starches remain the most widely used category, holding a 73.9% market share, largely because they serve as the structural base for most baked goods and are essential in large-scale bakery production.

- Fastest-Growing Product Segment: Sweeteners are gaining momentum as manufacturers develop alternative sweetening solutions and innovative formulations to meet evolving taste preferences and reduced-sugar product trends.

- Leading Form Segment: Dry ingredients account for the largest material share due to their longer shelf life, ease of storage, and suitability for high-volume industrial baking operations.

- Fastest-Growing Form Segment: Liquid ingredients are witnessing faster growth as modern bakeries increasingly adopt automated mixing systems that favor liquid formulations for improved consistency and processing efficiency.

| Key Insights | Details |

|---|---|

|

Bakery Ingredients Market Size (2026E) |

US$ 23.2 Bn |

|

Market Value Forecast (2033F) |

US$ 38.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

Market Dynamics

Driver - Expanding Consumption of Processed and Convenience Bakery Products Worldwide

A major factor encouraging industry growth is the steadily increasing consumption of packaged and convenience bakery products across both developed and emerging economies. Changing lifestyles, urbanization, and the growing number of working professionals have significantly increased demand for ready-to-eat foods such as bread, cookies, cakes, and snack-based baked items. These products rely on a wide range of ingredients—including emulsifiers, sweeteners, enzymes, and dough conditioners—to maintain consistent taste, texture, and shelf stability during mass production and distribution. As industrial bakeries scale their operations to meet global demand, the need for standardized ingredient formulations continues to expand. Large food manufacturers depend heavily on functional ingredient systems that improve dough strength, fermentation efficiency, and product freshness throughout the supply chain.

Additionally, rapid growth of organized retail and quick-service restaurant chains that rely on consistent bakery supplies. Sandwich breads, burger buns, pastries, and baked desserts are widely used in foodservice menus, increasing the volume of ingredients required for large-scale baking operations. At the same time, consumers are becoming more interested in premium and specialty baked products such as whole-grain breads, protein-enriched snacks, and gluten-free alternatives. This evolving demand encourages ingredient suppliers to innovate with enzyme solutions, natural emulsifiers, and specialty flour blends. Together, increasing global bakery consumption and the expansion of industrial food production continue to drive strong demand for bakery ingredient solutions.

Restraints - Volatility in Raw Material Prices and Regulatory Pressures on Food Ingredients

One of the key challenges affecting industry expansion is the volatility associated with agricultural raw materials used in bakery ingredient production. Essential inputs such as wheat, corn, sugar, and vegetable oils are subject to fluctuations caused by climate conditions, geopolitical developments, supply chain disruptions, and shifting global trade policies. Changes in crop yields or transportation costs can quickly influence ingredient pricing, creating uncertainty for manufacturers and food processors that rely on stable supply chains. These fluctuations may affect profit margins for ingredient producers as well as bakery companies that operate with tight cost structures.

Another limiting factor involves increasingly strict food safety and labeling regulations in many regions. Governments and regulatory agencies require extensive testing, documentation, and compliance for food additives, emulsifiers, preservatives, and flavoring systems used in baked goods. While these regulations protect consumer safety, they can also increase production costs and slow the introduction of new ingredients into the market. In addition, rising consumer awareness regarding artificial additives has encouraged demand for clean-label products, forcing manufacturers to reformulate recipes and replace certain synthetic ingredients with natural alternatives. This reformulation process can be complex and costly, particularly for large-scale bakeries that must maintain consistent product quality. Together, input cost instability and regulatory complexity may moderate growth for ingredient suppliers in certain markets.

Opportunity - Innovation in Functional, Clean-Label, and Health-Focused Baking Ingredients

Significant future potential is emerging from the development of healthier and functionally enhanced bakery ingredient solutions. As consumers increasingly prioritize nutrition and ingredient transparency, food manufacturers are actively reformulating baked products to include natural, plant-based, and minimally processed components. This shift has accelerated research into enzyme-based dough improvers, natural emulsifiers, plant proteins, and alternative sweeteners that improve product performance without relying on artificial additives. Clean-label bakery formulations have become particularly attractive to health-conscious consumers seeking products with recognizable ingredients and simplified labels.

Moreover, the growing demand for specialty bakery categories such as gluten-free, high-fiber, and high-protein baked foods. Ingredient suppliers are developing innovative flour alternatives derived from sources like oats, chickpeas, lentils, and ancient grains to meet these dietary trends. At the same time, advancements in food processing technologies allow manufacturers to produce ingredient systems that enhance moisture retention, extend shelf life, and maintain desirable textures in reduced-sugar or reduced-fat bakery formulations. Emerging markets also present considerable potential as rising disposable incomes and urban lifestyles increase the consumption of packaged bakery goods. The expansion of modern retail channels and foodservice chains further strengthens ingredient demand. Combined with ongoing research in food science and growing consumer interest in healthier baked products, these developments create strong long-term opportunities for ingredient manufacturers worldwide.

Category-wise Analysis

By Ingredient Type, Flour & Starches Segment Leads the Market Owing to Their Essential Role in Bakery Product Formulation

Flour & starches are projected to account for 38.6% of global market revenue in 2026, making them the most significant ingredient category within the bakery ingredients industry. Their dominance is largely attributed to their fundamental role in forming the structural base of most baked goods, including bread, cakes, and biscuits. Wheat flour remains the most widely utilized raw material due to its gluten content, which provides elasticity and gas retention necessary for dough development. Starches derived from corn, potato, and tapioca are also increasingly used to improve moisture retention, texture, and shelf stability in processed bakery products. Rising global consumption of staple baked foods, particularly bread and rolls, continues to drive demand for these ingredients. Additionally, the expansion of industrial bakeries and quick-service food chains has intensified the need for standardized flour blends that ensure consistent product quality at large production volumes. Manufacturers are also exploring fortified and specialty flours enriched with fiber, protein, or micronutrients to meet evolving consumer preferences for healthier bakery options. Continuous innovation in milling technologies and ingredient processing further supports large-scale supply, reinforcing the strong market position of flour and starch-based ingredients.

By Application, Bread Segment Dominates Applications Because It Represents the Most Widely Consumed Bakery Product Worldwide

The bread segment is anticipated to capture 41.3% of the global bakery ingredients market in 2026, reflecting its position as the most widely produced and consumed baked food globally. Bread manufacturing requires a diverse combination of ingredients such as flour, yeast, enzymes, emulsifiers, and sweeteners, making it a primary driver of ingredient demand. In many countries, bread serves as a daily staple, ensuring consistent production volumes across commercial bakeries and foodservice establishments. Industrial-scale bakeries rely heavily on specialized ingredient systems that enhance dough stability, fermentation efficiency, and shelf life. Rising urbanization and busy lifestyles have also encouraged the consumption of packaged bread, sandwiches, and convenience bakery foods. Moreover, product diversification—such as multigrain bread, gluten-free varieties, and protein-enriched formulations—has broadened ingredient utilization within this category. Food manufacturers are increasingly incorporating functional ingredients that improve softness, extend freshness, and support clean-label product development. The growing presence of large retail bakery chains and quick-service restaurants further strengthens ingredient demand for bread production, ensuring the continued leadership of this application segment across the global bakery ingredients market.

By Distribution Channel, Supermarkets & Hypermarkets Lead Distribution as They Offer Wide Product Availability and Strong Consumer Reach

Supermarkets & hypermarkets are estimated to represent 34.8% of total market revenue in 2026, highlighting their importance as major retail distribution channels for bakery ingredients and packaged baking mixes. These large retail outlets provide consumers with convenient access to a broad range of baking ingredients, including flour blends, sweeteners, premixes, and specialty additives used in home baking. Their extensive shelf space allows manufacturers to showcase multiple product variations and brands, supporting strong visibility and competitive pricing. Rising consumer interest in home baking—driven by lifestyle changes, culinary experimentation, and social media influence—has significantly boosted retail sales of baking ingredients through these outlets. Supermarkets also benefit from well-established supply chains and partnerships with food manufacturers, enabling them to maintain consistent inventory and offer promotional pricing strategies. Many retailers are expanding private-label baking ingredient portfolios, further intensifying competition within the segment. Additionally, these retail formats serve as convenient purchasing points for small bakeries, cafés, and foodservice operators seeking readily available ingredients in moderate quantities. Their accessibility, product variety, and strong consumer trust collectively reinforce the leading position of supermarkets and hypermarkets in bakery ingredient distribution.

Region-wise Insights

North America Bakery Ingredients Market Trends

North America is projected to account for 48.5% of global bakery ingredients revenue in 2026, positioning it as the largest regional market. The region’s dominance stems from a highly developed food processing sector, extensive industrial bakery operations, and strong consumer demand for packaged baked goods. The United States represents the most significant national contributor, supported by a mature bakery industry and advanced ingredient manufacturing infrastructure. Commercial bakeries across the region utilize a wide range of functional ingredients—including enzymes, emulsifiers, and dough conditioners—to maintain consistent quality and extend product shelf life.

Another factor strengthening the regional market is the high consumption of convenience foods such as sliced bread, muffins, pastries, and snack-based baked items. Large retail chains and foodservice brands rely heavily on standardized ingredient systems to support mass production. In addition, consumers in North America are increasingly seeking healthier bakery options, including whole-grain, gluten-free, and reduced-sugar products. This trend has encouraged ingredient suppliers to develop innovative formulations featuring plant-based proteins, fiber enrichment, and natural emulsifiers. Strong research capabilities among ingredient manufacturers, combined with well-established supply networks, further reinforce regional leadership. Continuous innovation in bakery formulations and growing demand for premium and artisanal baked products are expected to sustain North America’s leading share in the global bakery ingredients market.

Europe Bakery Ingredients Market Trends

Europe represents a well-established yet steadily evolving market for bakery ingredients, supported by a deep cultural tradition of bread and pastry consumption. Countries including Germany, the United Kingdom, France, Italy, and Spain contribute significantly to regional demand due to their strong bakery heritage and extensive network of artisan and industrial bakeries. European consumers display a strong preference for high-quality baked goods, ranging from specialty breads to premium pastries, which drives the need for specialized ingredients such as fermentation improvers, emulsifiers, and flavor systems.

The region’s regulatory framework also emphasizes food safety, product labeling transparency, and ingredient quality standards. As a result, manufacturers increasingly focus on developing clean-label ingredient solutions that minimize artificial additives while maintaining product performance. Demand for organic and natural baking ingredients has grown rapidly as consumers prioritize healthier food choices. Additionally, European bakeries are experimenting with alternative grains such as rye, spelt, and oats to diversify product offerings and address nutritional trends. The presence of well-known bakery ingredient suppliers and advanced food technology research institutions further strengthens innovation in the region. Although growth rates remain moderate compared with emerging markets, steady consumption patterns, evolving product innovation, and continued demand for premium baked goods ensure stable development of the bakery ingredients market across Europe.

Asia Pacific Bakery Ingredients Market Trends

Asia Pacific is expected to emerge as the fastest-growing regional market, registering a CAGR of approximately 7.9% between 2026 and 2033. Rapid urbanization, expanding middle-class populations, and changing dietary habits are key factors accelerating bakery consumption across the region. Countries such as China, India, Japan, and South Korea are witnessing a significant rise in demand for packaged breads, cakes, and snack-based baked products. Traditionally rice-based diets are gradually incorporating more wheat-based foods, creating substantial opportunities for bakery ingredient suppliers.

The growth of organized retail and quick-service restaurant chains has also contributed to increasing bakery product availability in urban areas. Industrial bakeries are expanding production capacities to meet rising demand, which in turn fuels the need for functional ingredients such as enzymes, emulsifiers, and dough conditioners that enhance texture and shelf life. Furthermore, improvements in cold-chain logistics and food distribution infrastructure are making packaged baked goods more accessible across developing economies. Local manufacturers are investing in advanced food processing technologies while international ingredient suppliers are expanding their presence through partnerships and regional manufacturing facilities. Growing consumer interest in convenience foods, combined with rising disposable incomes and increasing exposure to Western dietary patterns, continues to accelerate bakery ingredient demand across the Asia Pacific region.

Market Competitive Landscape

The global bakery ingredients market is highly competitive, with strong participation from companies such as Cargill, Incorporated, Archer-Daniels-Midland Company (ADM), Associated British Foods plc (AB Mauri), Puratos Group, International Flavors & Fragrances Inc. (IFF), and Bakels Group. These companies leverage extensive ingredient portfolios, strong R&D capabilities, global manufacturing networks, and strategic partnerships with industrial bakeries and food manufacturers.

Competitive strategies focus on developing clean-label ingredients, enzyme-based solutions, and functional bakery improvers that enhance texture, shelf life, and nutritional value. Market players are also investing in product innovation, sustainable sourcing, customized ingredient solutions, and expanding production capacities to address rising global demand for bakery products.

Key Industrial Developments

- In March 2026, Puratos Group announced that it had entered into a definitive agreement on March 10 to acquire Dawn Food Products. The strategic move is expected to significantly strengthen Puratos’ global presence and expand its capabilities as a major supplier within the baked foods industry. Company leadership described the acquisition as an important long-term step aimed at broadening product offerings and reinforcing its position in the global bakery ingredients market.

- In March 2026, CSM Ingredients introduced Tiger Granulat, a new bakery ingredient solution designed to enhance texture, appearance, and flavor in a variety of baked products. The product is developed to help bakers achieve distinctive crust patterns and improved visual appeal in artisan-style breads and specialty baked goods. With this launch, the company aims to support bakery manufacturers and professional bakers in creating innovative products while maintaining consistent quality and production efficiency.

Companies Covered in Bakery Ingredients Market

- Cargill, Incorporated

- Archer-Daniels-Midland Company (ADM)

- Associated British Foods plc (AB Mauri)

- Puratos Group

- International Flavors & Fragrances Inc. (IFF)

- Bakels Group

- Glanbia plc

- dsm-firmenich AG

- Corbion N.V.

- Kaneka Corporation

- Kerry Group plc

- Lallemand Inc.

- Novonesis Group (formerly Novozymes A/S)

- AAK AB

- Fuji Oil Co., Ltd.

- Others

Frequently Asked Questions

The global bakery ingredients market is projected to be valued at US$ 23.2 Bn in 2026.

Rising global consumption of convenient bakery products, increasing demand for clean-label and functional ingredients, and expansion of industrial bakery production are key drivers of the global bakery ingredients market.

The global bakery ingredients market is poised to witness a CAGR of 5.6 % between 2026 and 2033.

Growing demand for gluten-free, plant-based, and fortified bakery products along with innovation in enzyme-based and clean-label ingredients presents major market opportunities.

Cargill, Incorporated, Archer-Daniels-Midland Company (ADM), Associated British Foods plc (AB Mauri), Puratos Group, International Flavors & Fragrances Inc. (IFF), and Bakels Group are some of the key players in the bakery ingredients market.