- Processed Food

- Dehydrated Seafood Market

Dehydrated Seafood Market Size, Share, and Growth Forecast 2026 - 2033

Dehydrated Seafood Market by Product Type (Dried Fish, Dried Shrimp/Prawns, Dried Squid & Cuttlefish, Seafood Powders, others), Drying Technology (Sun/Air Drying, Hot-Air Dehydration, Freeze-Drying, Smoke-Drying), Application (Household Consumption, Food Processing Industry, Restaurants, Pet food Manufacturers), and Regional Analysis 2026 - 2033

Dehydrated Seafood Market Share and Trends Analysis

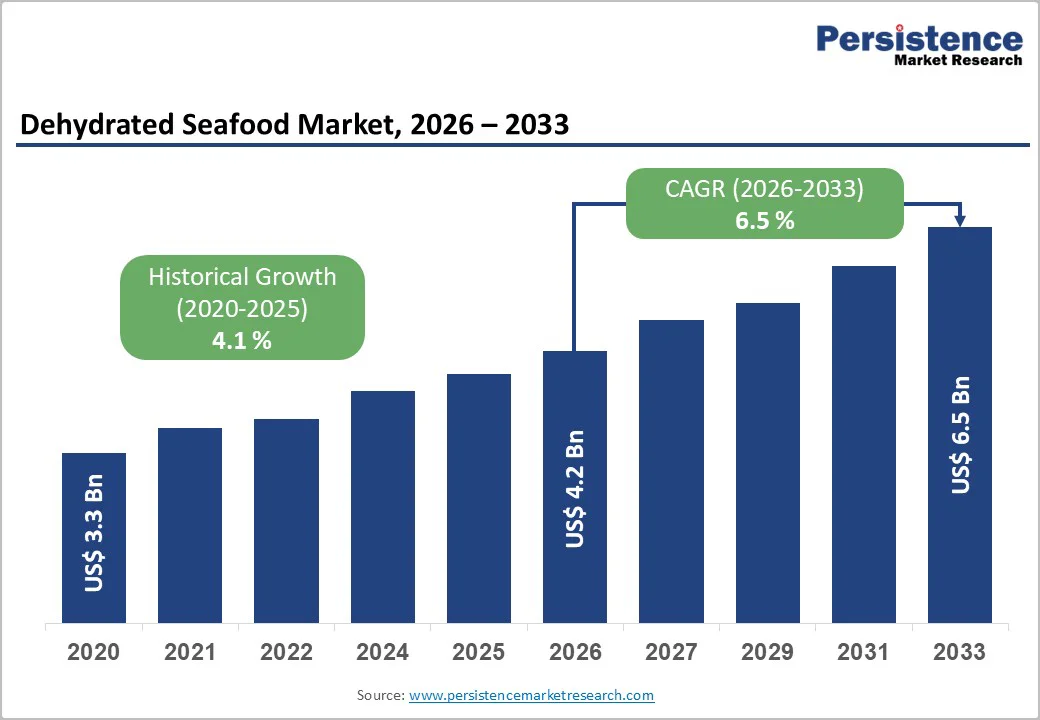

The global dehydrated seafood market size is likely to be valued at US$4.2 billion in 2026, and is projected to reach US$6.5 billion by 2033, growing at a CAGR of 6.5% during the forecast period 2026-2033. The market is growing steadily as demand increases for shelf-stable, high-protein seafood products and convenient food formats.

Advancements in dehydration technologies are strengthening product safety and export viability, while rising seafood consumption, particularly in Asia, continues to widen the consumer base. Improved cold-chain infrastructure and a shift toward healthier, low-fat dietary preferences further support scalability for manufacturers across global markets.

Key Industry Highlights

- Leading Product Type: Dried fish is expected to remain the largest segment in 2026, holding about 45% of the market revenue share, owing to its easy integration into daily cooking routines.

- Dominant Drying Technology: Sun/air drying is likely to remain the largest segment in 2026 due to its low cost and widespread traditional adoption.

- Fastest-Growing Drying Technology: Freeze-drying is projected to grow the fastest, expanding at over 8% CAGR through 2033, driven by premium product demand.

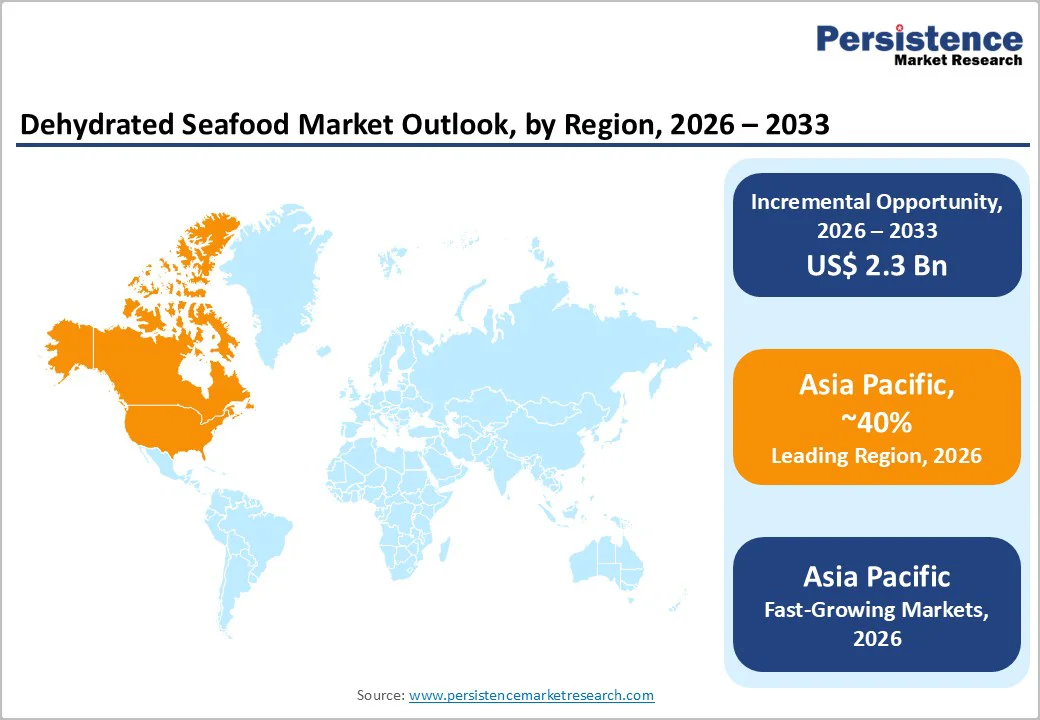

- Leading Region: Asia Pacific is expected to lead the market in 2026, accounting for over 60% of global production, powered by abundant marine resources and low processing costs.

- Key Growth Driver: Rising consumption of instant noodles, snacks, and pet food is envisaged to strengthen long-term market growth.

| Key Insights | Details |

|---|---|

|

Dehydrated Seafood Market Size (2026E) |

US$4.2 Bn |

|

Market Value Forecast (2033F) |

US$6.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.4% |

Market Factors - Growth, Barriers, and Opportunity

Rising Seafood Consumption and Expanding Demand from Food & Pet Food Industries

Global per-capita seafood consumption has more than doubled in the past sixty years, driving demand for affordable, long-lasting protein sources. Dehydrated seafood, with a shelf life extending from 12 to 24 months and minimal need for refrigeration, is now a vital solution for export markets and regions that lack reliable cold-chain infrastructure. This format is also gaining traction in instant noodles, snacks, soups, restaurant broths, and the global pet food industry, where dried fish, shrimp, and seafood powders are increasingly incorporated. These broadening consumption and application patterns have established a resilient and expanding market for dehydrated seafood products worldwide, supporting both food security and supply chain resilience in diverse geographies.

Advancements in dehydration technology, including freeze-drying, controlled hot-air drying, and hybrid systems, are enhancing product quality, nutrient retention, and microbial safety. These technologies enable processors to achieve precise moisture reduction, which is critical because acceptable moisture levels vary by product and are strictly regulated by Codex commodity standards and the U.S. Food and Drug Administration (FDA). Freeze-drying stands out for its ability to retain more than 95 percent of nutrients while extending shelf stability, making it ideal for premium human foods and high-end pet nutrition.

Supply Instability and Strict Regulatory Requirements

The dehydrated seafood market growth confronts substantial operational challenges driven by volatile raw material availability and unpredictable supply conditions. Seasonal fluctuations, climate phenomena such as El Niño, and fishing restrictions imposed by regional authorities create inconsistent catch volumes, leading to price volatility of 15-20% in major sourcing countries. These swings inflate production costs and complicate inventory planning, forcing processors to maintain higher working capital reserves or risk supply gaps. Smaller processors face disproportionate pressure because they often lack the purchasing scale or financial buffers to absorb sudden cost increases, placing them at a competitive disadvantage relative to vertically integrated players that control fishing operations or maintain diversified sourcing networks across multiple geographies.

Simultaneously, exporters must navigate stringent global quality regulations enforced by agencies such as the FDA, European Food Safety Authority (EFSA), and national marine authorities. These bodies impose rigorous standards covering moisture content, microbial safety, heavy metal contaminants, and hygiene controls throughout processing and storage. Compliance demands significant investment in laboratory testing, facility upgrades, and documentation systems, which raises barriers to entry and ongoing operational expenses, particularly for small- and medium-sized enterprises (SMEs). Non-compliance or detection of defects during import inspections can result in shipment rejections, delayed market access, and reputational damage that undermines long-term customer relationships.

Soaring Demand in Emerging Consumer Markets & Digital Distribution

High-growth markets across Asia and Africa, such as India, Indonesia, Nigeria, and Kenya, are experiencing rapid growth in packaged and convenient food consumption, creating strong headroom for dehydrated seafood formats. Expanding middle-class populations and busy urban lifestyles are driving demand for affordable, shelf-stable protein options such as seafood powders and dried shrimp snacks that fit into instant meals, home cooking, and foodservice menus. With these countries together accounting for more than 2.5 billion consumers, even modest per-capita adoption translates into substantial volume potential by 2033. In parallel, strong penetration of e-commerce and the rise of direct-to-consumer (D2C) models enable brands to reach households and small restaurants more efficiently, improve margins, test new concepts quickly, and build recurring revenue through subscription-based offerings.

Premiumization is emerging as a powerful growth vector as consumers gravitate toward natural, preservative-free, and nutrient-dense products, pushing high-quality dehydrated seafood into a faster-growth tier. Offerings such as freeze-dried shrimp, low-sodium fish powders, and curated dried seafood assortments resonate with health-conscious shoppers and speciality retail channels that are willing to pay for superior nutrition, texture, and flavor. Advanced processes such as freeze-drying support this positioning by preserving nutrients and sensory quality, thereby justifying meaningful price premiums and strengthening brand differentiation. Clean-label declarations, traceability certifications, and transparent sourcing stories further enhance trust and export appeal, especially where premium segments are projected to grow steadily.

Category-wise Analysis

Product Type Insights

Dried fish is expected to maintain its position as the leading product type, accounting for approximately 40% of the dehydrated seafood market revenue share in 2026, supported by deep-rooted household consumption across Asia Pacific and Africa. This dominance stems from its affordability relative to other protein sources, seamless integration into daily cooking routines, and widespread use in traditional recipes that span generations. Dried fish circulates through well-established local trade networks, reaching both rural villages and urban neighborhoods efficiently. Its extended shelf life, versatility in preparation methods, and strong cultural acceptance ensure that it remains a staple protein format across diverse income levels and geographies, underpinning sustained volume leadership through 2033.

Seafood powders is likely to represent the fastest-expanding segment from 2026 to 2033, driven by surging demand for dehydrated seafood from the convenience food sector, particularly instant noodles, snacks, soups, and restaurant broths. Food manufacturers favor seafood powders for their concentrated nutrient profile, extended shelf stability, and ease of incorporation into dry seasoning blends and flavoring systems. This functional advantage accelerates adoption in ready-to-cook meal kits and prepared foods targeting time-pressed consumers. Pet food producers increasingly specify seafood powders as protein-rich, palatable ingredients that align with clean-label and natural positioning. These combined drivers position seafood powders as the highest CAGR segment, with strong potential to capture share from traditional formats as convenience and premium nutrition trends intensify.

Drying Technology Insights

Sun drying and air drying are likely to remain the leading technologies in 2026 since they have low operating costs and are already deeply embedded in developing regions where traditional processing dominates. Small and medium-sized processors rely on these methods for their minimal equipment needs and straightforward scalability, enabling them to consistently supply local markets. With an estimated 35-40% share of total production, these techniques are expected to keep serving domestic demand effectively, particularly in areas where consumers prefer familiar, traditionally dried seafood products and are more price-sensitive.

Freeze-drying is projected to be the fastest-growing technology through 2033, as processors value its ability to deliver superior texture, high nutrient retention, and export-grade quality that meet premium market expectations. Adoption is increasing among manufacturers that focus on high-end packaged foods, gourmet applications, and specialised pet nutrition, where long shelf life and reliable sensory performance justify higher price points. Its strong fit with premium, clean-label positioning supports a growth of around 8% CAGR, and continued global interest in natural, high-quality products is likely to accelerate freeze-drying investments across both mature and emerging markets.

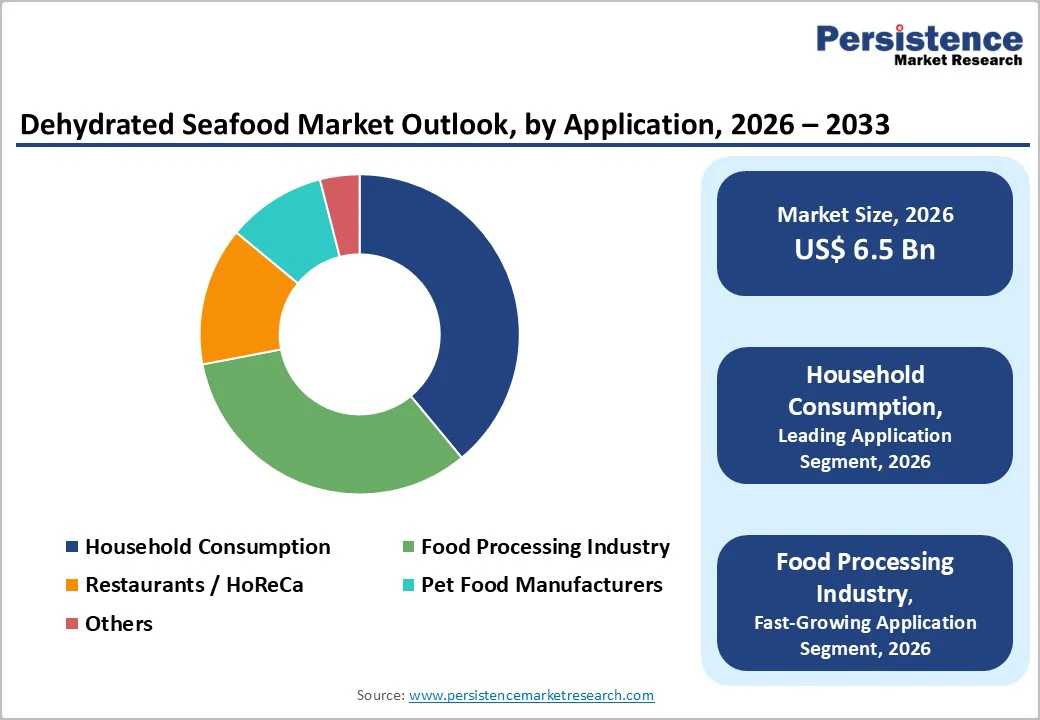

Application Insights

Household consumption is projected to remain the largest application segment, contributing over 40% of the total demand. Its dominance is rooted in long-standing cultural eating habits in Asia Pacific, Africa, and parts of Europe, where dried fish and seafood are staples. Consumers value its affordability, ease of storage, and compatibility with traditional dishes. These factors ensure stable, ongoing demand, particularly in regions where access to fresh seafood remains seasonal or limited.

The food processing industry is expected to expand the fastest during the 2026-2033 forecast period, driven by the rising usage of dehydrated seafood in instant noodles, snacks, soups, seasonings, and ready meals. The unprecedented scale of urbanization and a widespread demand for quick-to-prepare foods in China, Indonesia, India, and Japan are accelerating adoption. Manufacturers prefer dehydrated seafood for its consistent flavor, long shelf life, and ease of blending into large-scale recipes, supporting a projected CAGR of around 8% through 2033.

Regional Insights

North America Dehydrated Seafood Market Trends

North America is projected to account for roughly 24% of the dehydrated seafood market share in 2026, driven by robust demand for convenient protein sources, expanding ethnic cuisine offerings, and a thriving pet food industry. The United States dominates regional consumption, bolstered by rigorous food safety oversight from the U.S. FDA. Imports from Asia continue to rise, while adoption of advanced freeze-drying technologies supports growth across retail outlets, foodservice operations, and specialty ingredient suppliers. These factors create a stable foundation for market expansion in a region where consumers prioritize quality and convenience in their daily protein choices.

The North American market for dehydrated seafood is forecast to expand at a 6% CAGR, driven by sustained consumer interest in premium, clean-label, and sustainably sourced products. Innovation-driven companies focus on traceability features, low-sodium options, and eco-friendly packaging to align with evolving preferences. E-commerce growth and demand for gourmet dehydrated seafood variants are opening new channels, though stringent regulations and elevated production costs are shaping competitive strategies. Manufacturers that balance compliance with value-added differentiation can strengthen their positions in this high-value landscape.

Europe Dehydrated Seafood Market Trends

Europe is projected to represent close to 20% of the global dehydrated seafood demand, anchored by strong consumer preference for sustainable seafood, advanced processing infrastructure, and rigorous adherence to EFSA safety standards. Germany leads regional consumption, followed by the United Kingdom, France, and Spain, with purchasing skewed toward freeze-dried, smoked, and other premium dehydrated formats that align with quality and provenance expectations. Limited local marine resources mean that many of these products depend on imports from Asian producers, which places additional emphasis on supplier audits, documentation, and long-term sourcing relationships to ensure continuity and compliance.

Regional market growth is expected at about 4.5% CAGR between 2026 and 2033, supported by the rising popularity of Mediterranean and Asian cuisines and the expanding influence of the Hotels, Restaurants, and Cafes (HORECA) channel. Commercial buyers place high importance on certified sustainable sourcing, precise moisture management, allergen controls, and heavy metal testing, which creates room for premium-positioned suppliers that can demonstrate robust quality systems.

Collaboration with experienced Asian processors and wider adoption of vacuum-sealed, portion-controlled packaging help extend shelf life, reduce waste, and support efficient menu planning. For manufacturers and exporters, Europe serves as a high-value market for consumption, where success depends on combining technical compliance with clear sustainability and traceability credentials.

Asia Pacific Dehydrated Seafood Market Trends

Asia Pacific is projected to dominate with approximately 60% global market share in 2026, underpinned by abundant marine resources, comparatively low processing costs, and long-established seafood drying practices across coastal communities. China, Japan, Vietnam, Indonesia, India, and the Philippines are central to both production and consumption, with dried fish, shrimp, squid, and seafood powders embedded in everyday diets and regional trade flows. This combination of great domestic demand and export-oriented processing capacity positions the Asia Pacific as the operational and commercial hub of the global dehydrated seafood industry, attracting ongoing investment from regional and international players.

The regional market is also expected to record the fastest growth, with a forecast CAGR of about 8% through 2033, driven by rapid urbanization, expanding packaged food consumption, and government-sponsored fishery modernisation initiatives that upgrade fleets and processing infrastructure. Improvements in freeze-drying and controlled hot-air dehydration are improving product quality and safety, enabling Asian manufacturers to access premium segments in North America and Europe and capture higher margins. Parallel growth in instant noodle, snack, and restaurant sectors, including quick-service and casual dining formats, reinforces long-term demand for dehydrated seafood ingredients, providing manufacturers with diversified, multi-channel revenue opportunities through 2033.

Competitive Landscape

The global dehydrated seafood market structure is dominated by large integrated processors such as Thai Union Group, Maruha Nichiro, Nissui (Nippon Suisan Kaisha), Dongwon Industries, Viet I-Mei, and major exporters from India, Vietnam, Thailand, and China. These companies benefit from extensive sourcing networks, scale in harvesting and aquaculture, advanced drying technologies such as hot-air systems and freeze-drying, and established export channels into North America, Europe, and the Asia Pacific.

Players that combine third-party certifications, traceability platforms, and diversified portfolios across dried fish, shrimp, squid, and seafood powders tend to secure preferred-supplier status with multinational food, retail, and pet nutrition customers. For buyers, partnering with such suppliers reduces supply risk, simplifies compliance with import rules, and supports co-development of new value-added products.

Competitive intensity is increasing as both multinational and regional manufacturers invest in premium, clean-label, and nutrient-focused formulations to meet tightening global food safety and sustainability standards. Strategic tools such as joint ventures, contract manufacturing, and long-term sourcing alliances now link Asian processors with Western brands and retailers, helping both sides manage cost, quality, and innovation pipelines. From a strategic standpoint, investing in certifications, digital traceability, and differentiated product platforms is emerging as a critical hedge against regulatory tightening and rising customer expectations across all key regions.

Key Industry Developments

- In July 2025, Cermaq, owned by Mitsubishi, purchased Grieg Seafood’s Canada and northern Norway operations for nearly $1 billion, positioning itself among the world’s largest salmon producers.

- In May 2025, dried seafood sales in North Korea surged as families stockpiled affordable, long-lasting side dishes to feed relatives mobilized for seasonal construction and farming work. Vendors report brisk trade in small, portable items such as dried anchovies and squid, which are easy to pack into lunchboxes for men sent to remote worksites.

- In May 2025, Maruha Nichiro secured a 70% stake in Van der Lee Seafish through its Dutch subsidiary, enhancing its European footprint and processing capacity for Atlantic fish species.

Companies Covered in Dehydrated Seafood Market

- Thai Union Group

- Maruha Nichiro Corporation

- Nippon Suisan Kaisha (Nissui)

- Beijing Seatreasures Group

- PT. Bumi Menara Internusa

- Seafood Products Pvt. Ltd.

- Dongwon Industries

- Oceana Group

- Pacific Andes

- Seahawk Marine Foods

- Lian Hin Enterprise

Frequently Asked Questions

The global dehydrated seafood market is projected to reach US$ 4.2 billion in 2026.

High demand for long-shelf-life seafood, growth in processed food applications, and increasing exports from the Asia Pacific are driving the market.

The market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Key market opportunities include premium freeze-dried products, seafood powders for seasonings, expansion in pet food, and rising HoReCa consumption.

Thai Union Group, Maruha Nichiro Corporation, Nippon Suisan Kaisha (Nissui), Beijing Seatreasures Group, and PT Bumi Menara Internusa are some of the key players in the market.