- Telecommunications

- RFID Electronic Toll Collection System Market

RFID Electronic Toll Collection System Market Size, Share, and Growth Forecast 2026 - 2033

RFID Electronic Toll Collection System Market By Component (Hardware, Toll Collection & Management Software, Services), Toll Charge Type (Perimeter-based Charges, Time-based Charges, Point-based Charges, Distance-based Charges), Application (Urban Areas and Roadways, Highways), and Region Analysis 2026 to 2033

Market Overview

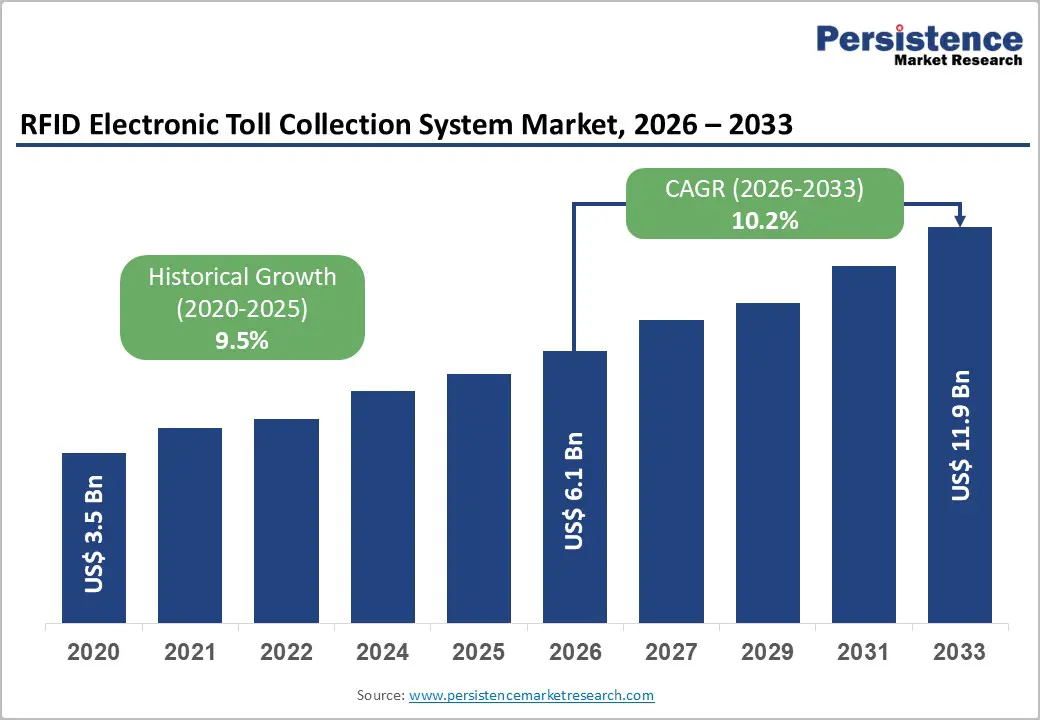

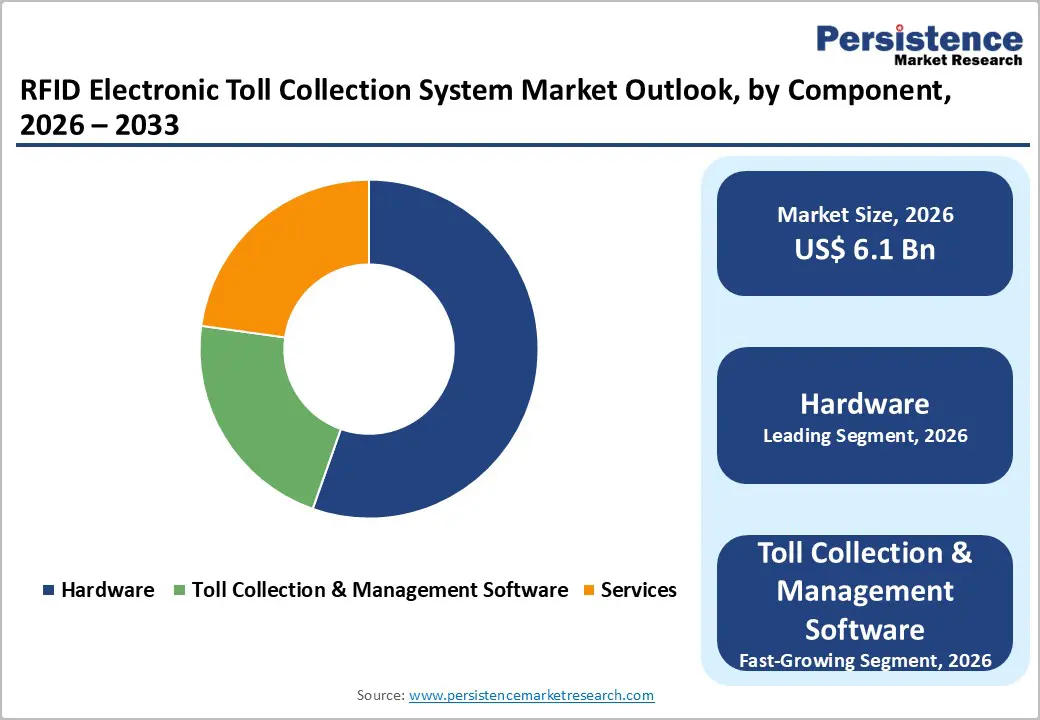

The global RFID Electronic Toll Collection System Market size is projected to be valued at US$6.1 Billion in 2026 and is anticipated to reach US$11.9 Billion by 2033, growing at a CAGR of 10.2% between 2026 and 2033. This expansion is driven by increasing traffic congestion in urban areas affecting 71% of major cities globally, government initiatives mandating cashless toll collection across 67 countries, and smart transportation infrastructure investments exceeding around US$428 billion worldwide. Vehicle population growth surpassing 1.4 billion units, declining RFID technology costs by ~48%, and environmental benefits reducing emissions by around 35% at toll plazas further accelerate adoption.

Key Market Highlights

- Hardware leads with 55% share, driven by RFID vehicle tags and fast-growing toll management software powered by cloud and AI.

- Distance-based charges dominate at 34%, while point-based tolling grows rapidly through urban congestion pricing.

- Highways lead applications at 56%, with urban areas expanding via smart city mobility and congestion management.

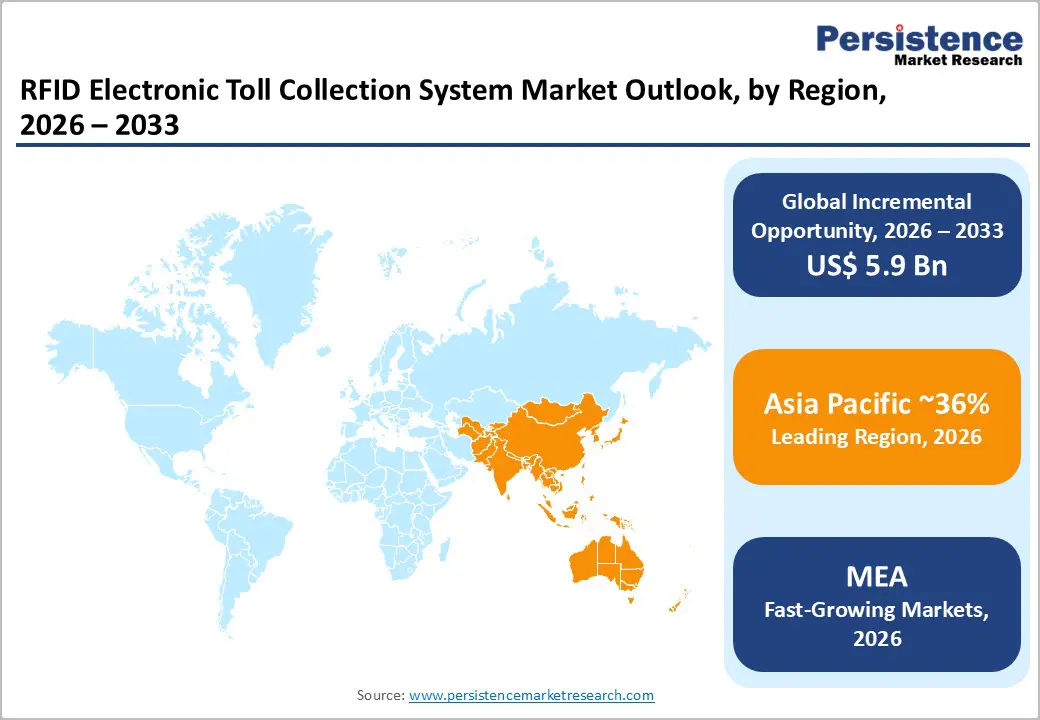

- Asia Pacific holds 36%, fueled by China’s massive expressway network and India’s FASTag program.

- North America grows strongly at 8.9%, Europe holds 24% supported by interoperability mandates.

- Strategic moves include hybrid RFID-GNSS-5G platforms, US$420M software acquisitions, and transponder partnerships for 2.4 million vehicles annually.

| Key Insights | Details |

|---|---|

| RFID Electronic Toll Collection System Market Size (2026E) | US$ 6.1 billion |

| Market Value Forecast (2033F) | US$ 11.9 billion |

| Projected Growth CAGR (2026-2033) | 10.2% |

| Historical Market Growth (2020-2025) | 9.5% |

Market Dynamics Analysis

Market Drivers

Escalating Traffic Congestion and Urban Mobility Challenges

Global urbanization has intensified traffic congestion challenges, with the Texas A&M Transportation Institute reporting that traffic delays cost the U.S. economy US$88.4 billion annually through wasted fuel and lost productivity. The World Bank documents that major metropolitan areas experience average congestion levels of 71%, with commuters spending 54 hours annually in traffic delays. Manual toll collection systems create bottlenecks reducing highway throughput by 40% and increasing vehicle emissions by 35% at toll plazas according to the U.S. Environmental Protection Agency. The International Road Federation reports global vehicle registrations reached 1.446 billion units in 2024, growing at 3.8% annually, creating unprecedented demand for efficient toll collection infrastructure. RFID-based electronic toll collection systems enable vehicles to traverse toll points at highway speeds, eliminating stop-and-go traffic patterns and improving throughput by 300%.

Government Smart City Initiatives and Intelligent Transportation Systems

Government investments in smart city infrastructure and intelligent transportation systems significantly accelerate RFID toll collection adoption. The United Nations reports 193 countries implementing smart city programs with combined investments of US$428 billion through 2030. China's smart transportation initiatives under the 14th Five-Year Plan allocate US$72 billion for intelligent highway systems including comprehensive electronic toll collection networks. The European Union's Cooperative Intelligent Transport Systems Directive mandates interoperable electronic toll collection across member states by 2027, with investments exceeding €89 billion. India's National Electronic Toll Collection program implemented FASTag systems across 950 toll plazas, achieving 97% electronic transaction penetration and processing 235 million transactions monthly. The U.S. Federal Highway Administration's Every Day Counts initiative promotes all-electronic tolling across state departments of transportation, eliminating cash collection infrastructure and reducing operational costs by 42%.

Market Restraints

High Development Costs and Design Complexity Challenges

RFID electronic toll collection deployment demands significant capital, with highway implementations costing US$2.8-7.5 million per plaza for gantries, readers, antennas, back-office systems, and violation enforcement. Budget constraints affect 58% of state transportation authorities, while replacing legacy infrastructure adds costs for decommissioning and workforce transitions. Interoperability across jurisdictions increases integration complexity by 35-50%. Small-scale deployments with limited traffic face extended payback periods of 9-14 years, discouraging adoption in rural or low-traffic routes despite long-term operational savings.

Privacy Concerns and Data Security Vulnerabilities

Electronic toll collection systems face consumer resistance over vehicle tracking and location privacy. Nearly half of drivers express discomfort with continuous RFID monitoring, while data breaches surged 52% in 2023, exposing payment and travel information. Compliance with GDPR and state privacy laws imposes average costs of US$4.2 million annually. Cybersecurity risks enabling toll evasion and unauthorized access further threaten revenue. Consumer trust deficits and legal concerns over data retention create adoption barriers, limiting voluntary RFID tag acquisition despite operational benefits.

Market Opportunities

Integration with Connected Vehicle Technologies and V2X Communication

The convergence of RFID toll collection with connected vehicle technologies and vehicle-to-everything communication creates significant value-addition opportunities. Connected vehicle deployments are projected to reach 775 million units globally by 2030, enabling integrated mobility services combining toll payment with parking, fuel, and traffic information. Vehicle-to-infrastructure communication supports dynamic toll pricing based on congestion levels, time-of-day, and vehicle classification, optimizing traffic flow and maximizing revenue collection. The U.S. Department of Transportation's connected vehicle pilot programs demonstrate 34% reduction in traffic delays through integrated tolling and traffic management. This convergence represents a US$18.6 billion opportunity by 2032, with platform-based business models generating recurring revenue through value-added mobility services beyond traditional toll collection.

Distance-Based Road User Charging and Mileage-Based Fee Systems

The transition from fuel taxes to distance-based road user charging creates expanding opportunities for RFID toll collection infrastructure. Government fuel tax revenues decline 23% annually due to improving vehicle fuel efficiency and electric vehicle adoption, necessitating alternative transportation funding mechanisms. The International Transport Forum projects distance-based charging could generate US$340 billion annually by 2035, replacing declining fuel tax receipts. Oregon's Road Usage Charge program, Singapore's Electronic Road Pricing 2.0 system, and Netherlands' planned kilometer charging demonstrate viable implementation models. GPS-integrated RFID systems enable precise distance tracking, supporting equitable user-pays principles while addressing infrastructure funding gaps. This transition represents substantial market expansion beyond traditional toll roads to comprehensive road network coverage.

Segmentation Analysis

Component Analysis

Hardware including RFID UHF antennas, toll RFID readers and scanners, RFID vehicle tags, and barcode labels commands a 55% market share. This segment delivers the physical backbone enabling contactless vehicle identification and automated toll transactions. RFID vehicle tags form the largest and fastest growing category, with deployments exceeding 420 million units globally and annual issuance of 67 million tags. Falling tag costs from US$18 to US$4.50 and durability extending seven to ten years accelerate adoption.

Toll collection and management software is the fastest growing component, expanding at 13.0% CAGR through 2033, driven by cloud platforms, advanced analytics, and mobile payments. These solutions support centralized account management, violation processing, customer portals, financial reconciliation, AI fraud detection, dynamic pricing, and predictive maintenance, improving jurisdiction toll network efficiency.

Toll Charge Type Analysis

Distance-based charges dominate the toll charge type segment with 34% market share, reflecting equitable user-pays principles charging motorists proportionally to actual road usage. This methodology addresses fairness concerns versus flat-rate tolling, deployed across corridors in Germany, Switzerland, and expanding Asian markets. Systems use entry-exit matching or GPS tracking to calculate trip distance and variable rates by vehicle class and route, optimizing revenue while redistributing traffic and easing congestion on major highways.

Point-based charges show strong growth at 10.2% CAGR, driven by urban congestion pricing and zone-based tolling. This model targets bottlenecks, bridges, and high-demand corridors for traffic control. Examples include London, Singapore, Stockholm, Milan, and New York, with adoption expanding as cities pursue precision tolling strategies for sustainable mobility management initiatives.

Application Analysis

Highways maintain application segment leadership with 56% market share, serving intercity corridors, expressways, and limited-access roadways where high-speed tolling delivers maximum benefits. Highway applications form the foundation of RFID tolling, showing clear ROI through collection cost reductions averaging 68% versus manual systems and throughput improvements generating 25-40% additional revenue capacity. Free-flow tolling removes plaza infrastructure, enabling continuous operation at design speeds while maintaining efficiency, supported by reliability and three decades of implementation experience.

Urban areas and roadways show solid growth at 9.1% CAGR, driven by congestion pricing, smart city mobility programs, and zone-based access controls. Urban RFID tolling supports traffic management beyond revenue collection, using dynamic pricing to influence travel behavior, manage peak demand, and optimize network utilization across dense metropolitan transport systems.

Regional Market Insights

North America

North America demonstrates strong growth at 8.9% CAGR, driven by all electronic tolling conversions eliminating cash infrastructure, highway privatization, and interoperability enabling seamless regional travel. The United States leads adoption with 520 toll facilities across 35 states collecting around US$15.3 billion annually, with 89% of transactions processed electronically via E-ZPass and regional systems. State transportation agencies implement cashless tolling, cutting operating costs 42% while improving throughput and safety. Projects including Texas LBJ Express, Virginia I-66 Express Lanes, and California Gateway Express deploy advanced RFID supporting dynamic pricing. Canada expands electronic tolling in Ontario and British Columbia, while Mexico broadens coverage. Interoperability frameworks like E-ZPass connect 39 agencies across 19 states serving 42 million accounts, enabling innovation in mobile payments, vehicle integration.

Europe

Europe maintains roughly 24% market share, growing at a steady 8.4% CAGR, shaped by EU interoperability directives, comprehensive truck tolling, and urban congestion charging. Germany leads deployment via nationwide truck tolling across 15,000 kilometers, generating €7.4 billion annually using satellite positioning with RFID verification. The United Kingdom applies electronic tolling on bridges, tunnels, and motorways, while France’s autoroute network achieves 99.4% electronic penetration. Spain operates advanced free-flow highways serving 52 million tourists yearly. The European Electronic Toll Service Directive mandates cross-border interoperability by 2027, harmonizing RFID standards and settlement. Sustainability priorities expand congestion charging in Stockholm and Milan, with Brussels and Edinburgh planned, while 5G and connected vehicle investments enable next-generation integrated mobility services across regional passenger freight transport networks.

Asia Pacific

Asia Pacific commands a significant 36% market share, driven by extensive highway construction, rapid motorization, and government mandates for electronic tolling across new infrastructure. China leads with the world’s largest expressway network spanning 177,000 km, processing 1.6 billion ETC transactions daily and achieving 95% cashless penetration, with 190 million active users by 2024. India’s FASTag program is the fastest growing, handling approximate 235 million monthly transactions across 950 toll plazas under mandatory RFID adoption. Japan operates advanced tolling on urban and intercity highways, while South Korea’s Hi-Pass reaches 89% penetration. ASEAN countries including Thailand, Indonesia, Malaysia, and the Philippines expand electronic tolling. Regional manufacturing delivers RFID tags and readers at 45% lower costs, supporting affordable, large-scale deployments across diverse transport corridors.

Competitive Landscape

Strategic Developments

- In January 2025, TransCore announced technology partnership with leading automotive manufacturers integrating embedded RFID transponders in vehicle production, eliminating aftermarket tag installation requirements and enabling seamless toll collection for 2.4 million vehicles annually across North American markets supporting connected vehicle ecosystem development.

Business Strategies

Market leaders pursue integrated mobility platform strategies combining tolling with parking, fuel payment, and public transit creating comprehensive transportation payment ecosystems. Technology differentiation emphasizes multi-protocol readers, cloud-based back-office systems, and AI-powered analytics reducing operational costs while enhancing revenue assurance. Strategic partnerships with automotive manufacturers enable embedded transponder integration in connected vehicles, while collaborations with payment processors expand account acquisition and reduce payment friction. Geographic expansion targets high-growth emerging markets through local manufacturing and technology transfer arrangements supporting government localization requirements.

Companies Covered in RFID Electronic Toll Collection System Market

- Kapsch TrafficCom AG

- Thales Group

- TransCore (Roper Technologies)

- Conduent Transportation

- Neology, Inc.

- Q-Free ASA

- Verra Mobility Corporation

- Siemens Mobility

- Cubic Transportation Systems

- Far Eastern Electronic Toll Collection Co.

- Xerox Corporation

- EfkON AG

- Mitsubishi Heavy Industries

- Raytheon Company

- Smartrac Technology Group

Frequently Asked Questions

The RFID Electronic Toll Collection System Market is projected at US$6.06 Billion in 2026, expanding to US$11.93 Billion by 2033.

Rising global vehicle density is intensifying congestion pressures, prompting governments to mandate electronic tolling under smart city programs, as it delivers significant emission reductions, improves traffic flow, and offers substantial operational cost efficiencies compared to manual toll collection systems.

The market is projected to grow at a CAGR of 10.2% between 2026 and 2033.

Massive infrastructure expansion in emerging markets, integration of tolling with connected vehicle ecosystems, and the shift toward distance-based charging models to replace declining fuel tax revenues present strong long-term growth opportunities for electronic toll collection systems.

Leading players include Kapsch TrafficCom, Thales Group, TransCore, Conduent Transportation, Neology Inc., Q-Free ASA, Verra Mobility, Siemens Mobility, Cubic Transportation Systems, Far Eastern Electronic Toll Collection, Xerox Corporation, EFKON AG, Mitsubishi Heavy Industries, Raytheon Company, and Smartrac Technology Group.