- Hardware & Software IT Services

- Data Center RFID Market

Data Center RFID Market Size, Share, and Growth Forecast, 2025 - 2032

Data Center RFID Market by Component Type (Hardware (Tags, Readers, Antennas), Software & Middleware, Services (Integration, Support), Other), Tag Type (Passive, Active, Others), by Application Type (Asset Tracking & Inventory, Environmental & Thermal Monitoring, Security & Access Control, Workflow Automation, others), and Regional Analysis for 2025 - 2032

Data Center RFID Market Size and Trend Analysis

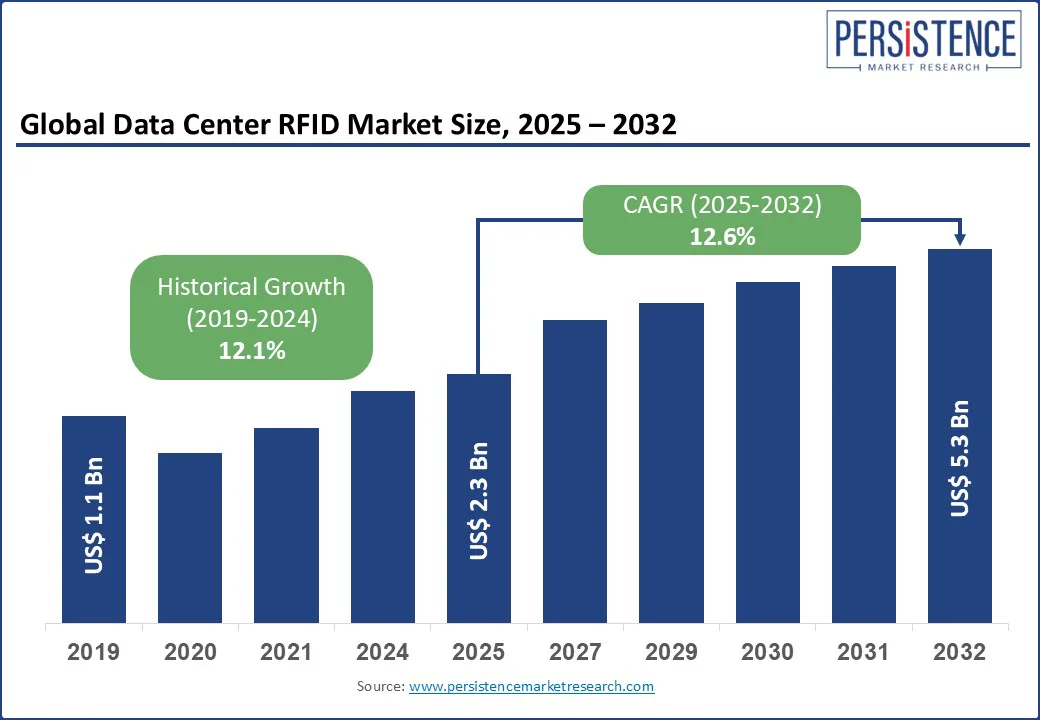

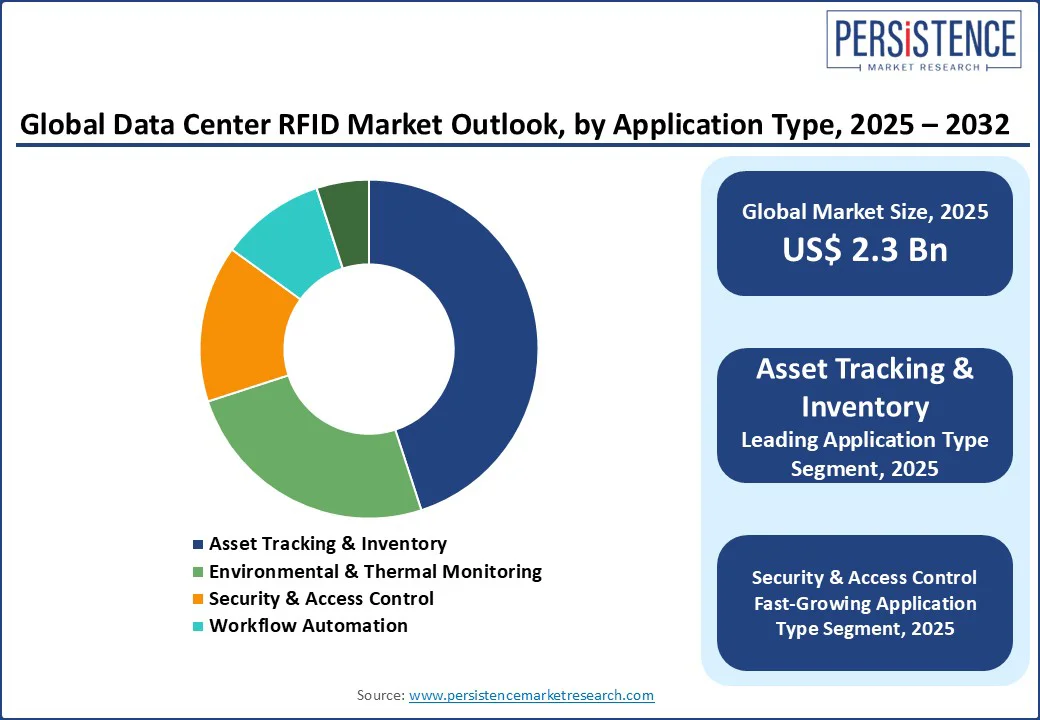

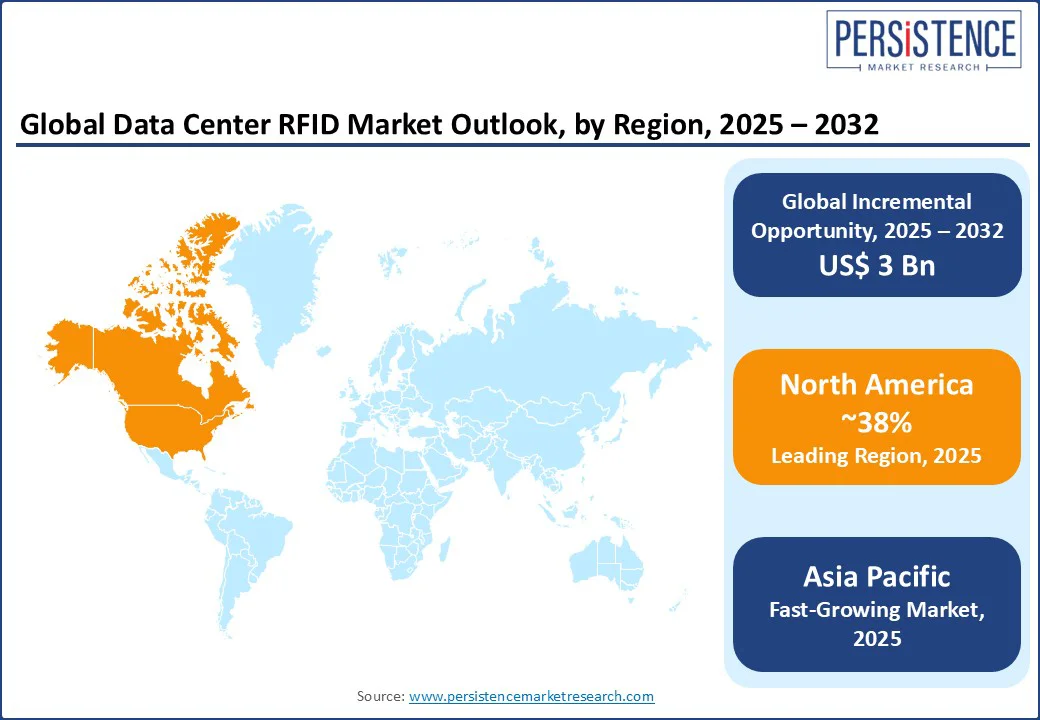

The Data Center RFID Market size is likely to be valued at US$ 2.3 Bn in 2025 and is estimated to reach US$ 5.3 Bn by 2032, growing at a CAGR of 12.6% during the forecast period from 2025 to 2032.

This growth is driven by the increasing demand for efficient asset management, enhanced security, and operational optimization in data centers worldwide. RFID technology enhances operational efficiency by minimizing human error and improving patient care across hospitals, labs, and pharmacies. Ongoing innovations such as miniaturized tags integrated with IoT and real-time location systems are further boosting adoption. Regulatory support, coupled with integration into electronic health records and cloud-based platforms, strengthens market growth while addressing patient safety and compliance. This makes RFID a critical tool for modernizing healthcare infrastructure and elevating service quality worldwide.

Key Industry Highlights

- Leading Region: North America holds a 38% share of the global data center RFID market in 2025, driven by its advanced technological infrastructure, strong venture capital investments, and leadership in AI research and innovation.

- Fastest-growing Region: Asia Pacific is the fastest-growing region in the data center RFID market, fueled by rapid digital adoption, strong AI initiatives, and growing cloud infrastructure investments.

- Major Developments: Impinj Inc. launched advanced RFID readers to enhance asset tracking in hyperscale data centers, while in October 2024, Honeywell introduced RFID-based monitoring systems to optimize energy efficiency and reduce operational costs in data centers.

- Dominant Application Type: Asset tracking and inventory management represent the leading application types in the RFID market, with hardware accounting for nearly 45% of the data center RFID market share.

|

Global Market Attribute |

Key Insights |

|

Data Center RFID Market Size (2025E) |

US$ 2.3 Bn |

|

Market Value Forecast (2032F) |

US$ 5.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

12.1% |

Market Dynamics

Driver: Growing Demand for Automated Asset Tracking and Operational Efficiency

The Data Center RFID market is growing rapidly as operators replace manual inventory methods with automated, real-time asset tracking. In high-density facilities, RFID delivers location accuracy above 99%, slashing audit times by up to 90% and improving hardware utilization rates by 15-20%. This shift is crucial for meeting operational efficiency targets and compliance with security frameworks. By integrating RFID with Data Center Infrastructure Management (DCIM) platforms, operators can reduce mean time to repair (MTTR) and ensure uninterrupted service delivery.

The U.S. Department of Energy reports that automated monitoring and asset management technologies in data centers can lower operational energy costs and reduce downtime risk through faster fault detection and resolution (energy.gov). This government-backed insight underscores RFID’s role in enabling cost savings, boosting productivity, and maintaining uptime for mission-critical workloads such as AI, IoT, and cloud services.

Restraint: High Initial Implementation Costs Challenges Growth

A major barrier to growth in the Data Center RFID market is the high initial implementation cost associated with deploying RFID systems. Large-scale data centers require thousands of tags, multiple high-frequency readers, antennas, middleware, and integration services. This results in significant capital expenditure before operational benefits are realized. Active RFID tags, while offering superior range and environmental monitoring, are substantially more expensive than passive tags and require periodic battery replacements, further increasing the total cost of ownership.

In addition to hardware, expenses for software licensing, custom integration with Data Center Infrastructure Management (DCIM) platforms, and staff training add to project budgets. According to industry estimates, initial deployment costs for RFID systems in large facilities can exceed US$1 Mn, depending on scale and complexity. For small and medium-sized operators, this investment often results in extended ROI timelines of three to five years, slowing widespread adoption despite RFID’s long-term efficiency gains.

Opportunity: IoT and AI Integration Creates Novel Opportunities

The integration of Internet of Things (IoT) and Artificial Intelligence (AI) technologies with Data Center RFID systems presents a significant growth opportunity. RFID tags embedded with environmental and asset sensors can continuously capture real-time data on temperature, humidity, power usage, and equipment location. When this data is fed into AI-driven analytics platforms, operators can enable predictive maintenance, automatically identify anomalies, and optimize cooling and energy consumption.

This convergence supports green data center initiatives by improving energy efficiency and reducing carbon footprints. The International Energy Agency (IEA) estimates that optimized environmental monitoring can cut data center energy use by up to 15%. Additionally, IoT-connected RFID devices enhance security by enabling automated alerts for unauthorized asset movement. As operators adopt AI-enabled DCIM platforms, RFID’s role as a data source for automation, sustainability, and operational intelligence will become central to next-generation data center strategies.

Category-wise Analysis

Component Type Insights

In 2025, hardware is expected to dominate the Data Center RFID market, holding over 55% market share. This category includes RFID tags, readers, and antennas, which are the foundation of any RFID deployment in data centers. The expansion of hyperscale facilities and the rising complexity of IT infrastructure are driving demand for high-volume tag deployment and advanced reader installations. Recent innovations, such as compact, high-frequency tags and rugged antennas designed for dense rack environments, are further boosting adoption in mission-critical facilities.

Services, including integration and support, are emerging as a leading segment due to the technical expertise required to deploy and maintain RFID systems. As data center operators seek seamless integration with Data Center Infrastructure Management (DCIM) platforms, demand for professional services is accelerating. This includes system design, installation, testing, staff training, and ongoing maintenance. Outsourcing these functions ensures faster deployment, minimized downtime, and maximum return on investment, especially in large, complex data center environments.

Tag Type Insights

In the data center RFID market, passive tags dominate with approximately 70% market share, serving as the backbone of asset tracking and inventory management solutions. Passive RFID tags are preferred due to their cost-effectiveness, long lifespan, and no battery requirement, making them ideal for large-scale deployments across complex data center environments. These tags enable efficient monitoring of servers, cables, and other IT assets without the need for frequent maintenance. Their widespread adoption drives improved accuracy and real-time visibility, helping data centers optimize operations, reduce downtime, and enhance security.

While passive tags lead the data center RFID market, active tags and other types continue to gain traction for specialized applications requiring longer read ranges and real-time data transmission. Active RFID tags, equipped with batteries, are used in environments demanding constant monitoring and immediate alerts. Additionally, other tag types include semi-passive or sensor-integrated tags that provide environmental data critical for data center management. Together, these tag types enable a comprehensive RFID ecosystem, but the dominance of passive tags underscores their central role in the growth and efficiency of the data center RFID market.

Application Type Insights

In the data center RFID market, asset tracking & inventory applications dominate the data center RFID market with a 45% share, serving as the backbone for efficient management of IT equipment and infrastructure. RFID technology enables precise tracking of servers, cables, and other critical assets, minimizing manual errors and improving operational visibility. This application is essential for reducing downtime, optimizing resource utilization, and streamlining inventory management across increasingly complex data center environments. The steady demand for real-time asset visibility continues to drive the widespread adoption of RFID-based tracking solutions.

Meanwhile, security & access control is the fastest-growing application segment within the data center RFID market. With increasing concerns over data breaches and unauthorized access, RFID-enabled security systems are rapidly being adopted to monitor and restrict personnel movement in sensitive areas. These systems enhance physical security by providing real-time access logs and automated entry control, meeting the rising compliance and safety requirements of modern data centers. Alongside asset tracking, security applications are critical drivers of innovation and growth in the RFID market.

Regional Insights

North America Data Center RFID Market Trends

In 2025, North America commands a dominant 38% share of the global data center RFID market, led primarily by the U.S. and Canada. The U.S., home to over 2,700 data centers, is witnessing a rapid 20% annual growth in RFID deployments driven by hyperscale operators such as Google and AWS, who are heavily investing in automation technologies and asset tracking solutions.

Canada’s market growth is propelled by its commitment to green data centers, where RFID technology helps reduce energy costs by approximately 15%, advancing sustainability initiatives. The region’s advanced technological infrastructure, combined with stringent security regulations, further accelerates RFID adoption in data centers. These factors position North America as a leading market for RFID-based security, asset management, and workflow automation within data centers. As data centers grow in complexity, RFID systems are increasingly critical for real-time monitoring, improving operational efficiency, and ensuring regulatory compliance, cementing North America’s leadership in the evolving data center RFID market.

Europe Data Center RFID Market Trends

Europe holds a significant share of the global data center market, with Germany, the UK, and the Netherlands leading the growth. This dominance is fueled by the EU’s 2024 AI Act and the ambitious €200 Bn InvestAI plan, which promotes ethical AI adoption and efficient data center operations across the region. In Germany, more than 600 data centers have adopted RFID technology to ensure strict GDPR compliance, witnessing a 25% increase in RFID adoption since 2023. The UK’s strong focus on sustainable data centers has accelerated RFID usage for energy monitoring, resulting in a 10-15% reduction in operational costs. Key drivers of growth in the European data center RFID market include stringent regulatory frameworks, proactive sustainability initiatives, and growing investments in AI-driven data center automation

Asia Pacific Data Center RFID Market Trends

Asia Pacific is the fastest-growing segment in the data center RFID market, driven by key countries such as China, India, and Singapore. India’s data center industry, expected to double by 2030, is seeing a 30% rise in RFID adoption for effective inventory management and asset tracking. China’s national AI strategy is accelerating RFID deployment across its 400+ data centers, boosting operational efficiency by 20%. Singapore, a major digital hub in the region, is driving RFID use for enhanced data center security, experiencing a 15% annual growth rate. This rapid expansion is fueled by widespread digital transformation, strong government investments in cloud infrastructure, and the continuous growth of data center networks. Asia Pacific is cementing its leadership as the fastest-growing region in the data center RFID market globally.

Competitive Landscape

The Global Data Center RFID Market is highly competitive, with key players such as Alien Technology LLC, Avery Dennison Corp., Impinj Inc., NXP Semiconductors N.V., and Honeywell International Inc. leading innovation. These companies focus on advanced RFID tags and integrated software solutions to enhance scalability and analytics. Strategic partnerships with data center operators and investments in sustainable RFID solutions strengthen their market presence.

Key Industry Developments:

- In March 2025: Impinj Inc. enhanced its RFID portfolio by launching advanced reader solutions designed to improve asset tracking accuracy and support large-scale deployments in hyperscale data centers.

- In October 2024: Honeywell International expanded its energy management offerings by integrating RFID-based monitoring systems aimed at optimizing environmental conditions and reducing operational costs in data centers through advanced automation technologies.

Companies Covered in Data Center RFID Market

- Alien Technology LLC

- Avery Dennison Corp.

- Omni-ID Ltd. (HID Global)

- Impinj Inc.

- NXP Semiconductors N.V.

- Honeywell International Inc.

- HID Global Corp.

- Vizinex RFID LLC

- InLogic Inc.

- Quanray Electronics Co. Ltd.

- SmartX Hub Inc.

- Invengo Information Tech. Co. Ltd.

- SATO Holdings Corp.

- Cisco Systems Inc.

- Johnson Controls (Cloudvue RFID)

- Others

Frequently Asked Questions

The Data Center RFID Market is valued at US$ 2.3 Bn in 2025.

Key drivers include demand for real-time asset tracking, enhanced security, and operational efficiency in data centers.

The Data Center RFID Market is projected to grow at a CAGR of 12.6% from 2025 to 2032.

Integration with IoT and AI technologies and expansion in emerging markets such as India and China present significant opportunities.

Top players include Alien Technology LLC, Impinj Inc., Honeywell International Inc., and NXP Semiconductors N.V.