- Home Appliances

- U.S. & Canada Residential Ceiling Fan Market

U.S. & Canada Residential Ceiling Fan Market Size, Trends, Share, and Growth Forecast 2025 - 2032

U.S. & Canada Residential Ceiling Fan Market by Product Type (Smart Ceiling Fans, Dual Mount Ceiling Fans, Standard Ceiling Fans, and Others), Usage (Indoor Ceiling Fans and Outdoor Ceiling Fans), Sales Channel (Wholesalers/Distributors, Direct Sales, and Others), and Country Analysis for 2025 - 2033

U.S. & Canada Residential Ceiling Fan Market Size and Share Analysis

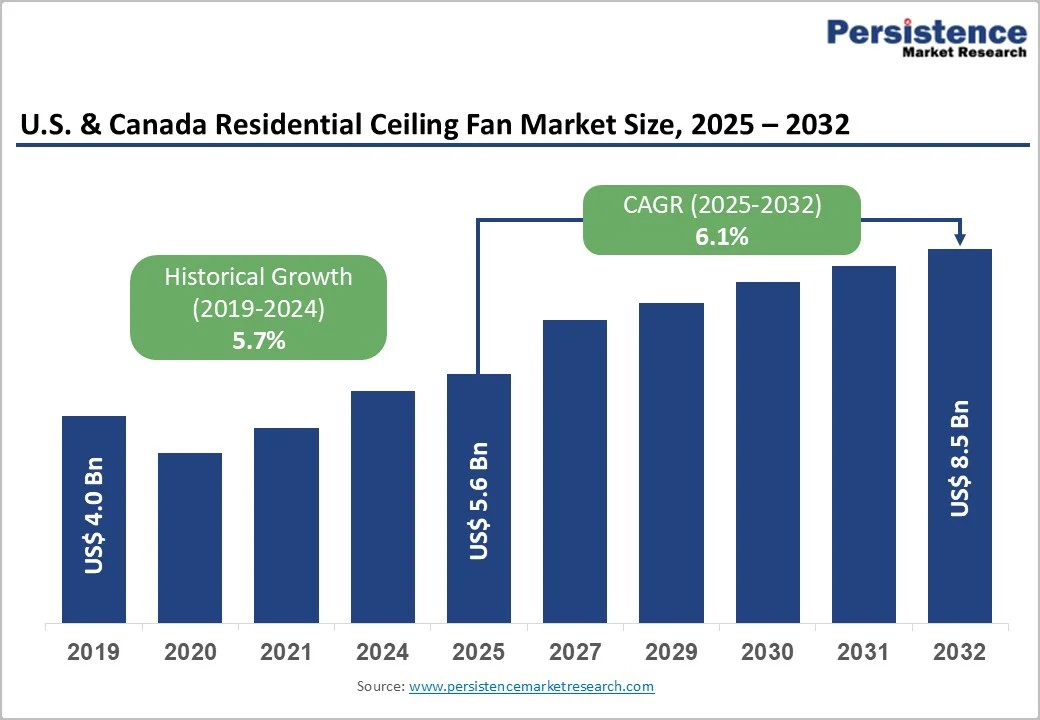

The U.S. & Canada residential ceiling fan market size is valued at US$5.6 billion in 2025 and is projected to reach US$8.5 billion by 2032, growing at a CAGR of 6.1% between 2025 and 2032.

The market is primarily driven by rising consumer demand for energy-efficient cooling and ventilation solutions that support year-round home comfort, increasing smart home technology integration, enabling remote control and voice activation compatibility, and rising consumer awareness of environmental sustainability and cost reduction.

Expanding residential construction activity and home renovation projects, erratic weather patterns requiring enhanced indoor air circulation, and manufacturers' focus on innovative product design with advanced motor technologies will further accelerate market growth.

Key Market Highlights

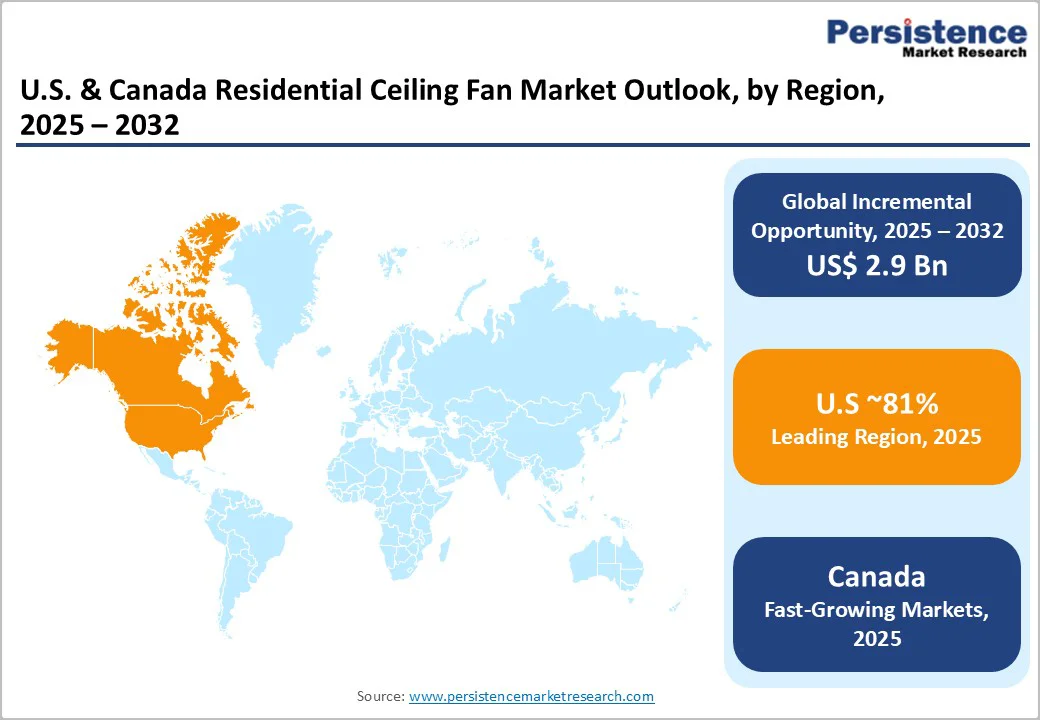

- Leading Region: The United States maintains market dominance with the largest market share and consumption volumes, driven by energy efficiency adoption, smart home technology integration, residential construction activity, and consumer preference for premium products.

- Fastest-Growing Region: Canada demonstrates the highest growth trajectory, with a 7.2% CAGR, driven by year-round climate requirements, energy efficiency

- mandates, government incentives, and rising disposable income.

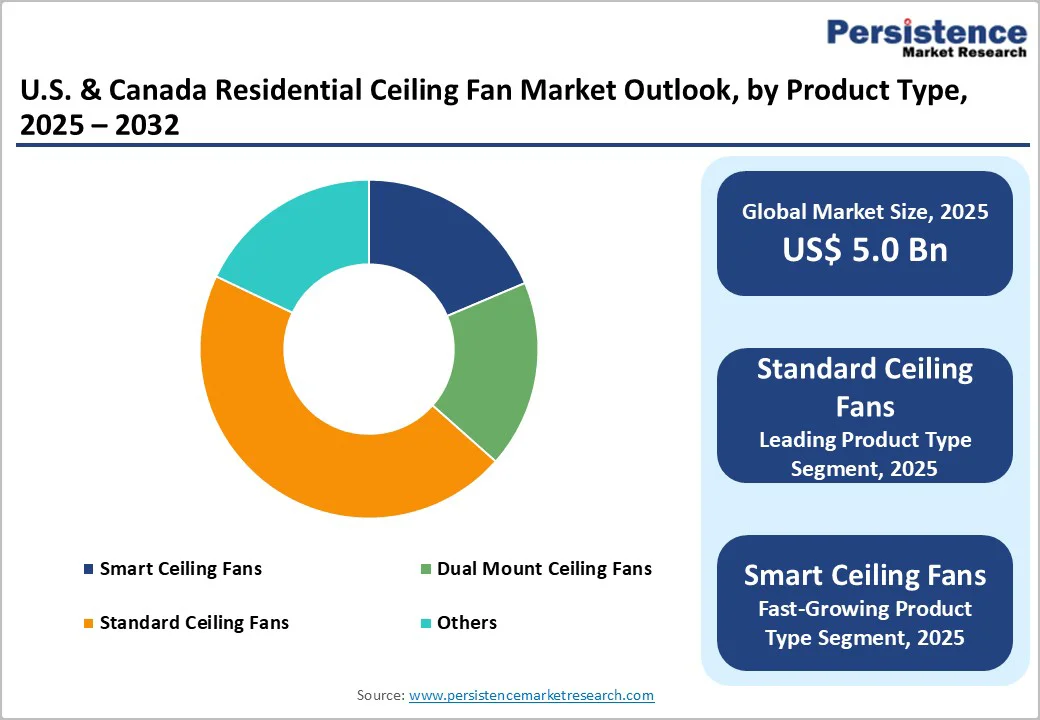

- Dominant Product Type: Standard Ceiling Fans command the largest product category at 56% market share, driven by affordability, consumer familiarity, proven reliability, and widespread retail availability supporting mainstream adoption.

- Fastest Growing Segment: Smart Ceiling Fans represent the fastest-growing product category at 5.4% CAGR, driven by IoT integration, voice control features, premium pricing support, and technology-oriented consumer preferences.

- Key Market Opportunity: Online retail channels growing at 7.5% CAGR, representing the highest-value growth opportunity through e-commerce expansion, direct consumer engagement, price transparency, and convenience-driven purchasing behavior supporting channel transformation.

| Key Insights | Details |

|---|---|

| U.S. & Canada Residential Ceiling Fan Market Size (2025E) | US$5.6 Bn |

| Market Value Forecast (2032F) | US$8.5 Bn |

| Projected Growth CAGR (2025 - 2032) | 6.1% |

| Historical Market Growth (2019 - 2024) | 5.7% |

Market Dynamics

Drivers - Rising Energy Efficiency Awareness and Preference for Low-Cost Cooling Solutions

The U.S. and Canada are witnessing a strong shift toward energy-efficient home solutions as consumers become more conscious of rising electricity costs, sustainability goals, and the need to reduce carbon footprints.

Ceiling fans have emerged as an attractive option because they consume significantly less power than air conditioners while still enhancing indoor comfort. This makes them ideal for both warm U.S. states and seasonally hot regions in Canada. The growing adoption of ENERGY STAR-certified fans, brushless DC motors, and variable-speed settings is further increasing their appeal.

Homeowners are increasingly using ceiling fans alongside HVAC systems to circulate air more effectively, reduce reliance on cooling units, and lower monthly utility bills. Government incentives and utility rebates supporting energy-efficient appliances are also encouraging this shift.

As environmental awareness and energy-saving priorities continue to rise, ceiling fans are becoming an essential fixture in modern households seeking practical, cost-effective, and sustainable cooling solutions.

Expansion of Residential Construction, Home Renovation Activities, and Interior Design Upgrades

The growth of residential construction, home remodeling, and interior enhancement trends across the U.S. and Canada is a major driver for the ceiling fans market. New housing developments, suburban expansion, and multi-family apartment projects are creating steady demand for ventilation and cooling fixtures.

At the same time, homeowners are increasingly investing in aesthetic upgrades, integrating ceiling fans not only for functionality but also as decorative elements that complement modern interior designs.

Manufacturers are responding with stylish finishes, contemporary blades, integrated LED lighting, and smart home-enabled models that sync with voice assistants and mobile apps, making ceiling fans both practical and visually appealing.

The rise of DIY home improvement culture, supported by major retailers like Home Depot, Lowe’s, RONA, and Canadian Tire, further fuels replacement purchases. Renovation activities accelerated by remote work trends and lifestyle improvements are also contributing to higher installations. Collectively, these factors drive strong growth in residential ceiling fan demand.

Restraints - Installation Complexity and Maintenance Requirements Limiting Market Appeal

Ceiling fan installation requires electrical wiring knowledge and professional expertise, creating barriers for DIY consumers. Structural considerations and ceiling height limitations restrict installation in certain residential environments. Regular maintenance requirements, including cleaning and motor servicing, add operational complexity.

Uncertainties in product lifespan and replacement frequency affect consumer purchase decisions. Warranty and technical support limitations are reducing consumer confidence in product durability.

Another key restraint affecting the U.S. and Canada ceiling fans market is the region’s strong seasonal climate variability, which limits the period during which ceiling fans are actively used.

In many northern and central parts of Canada and the U.S., long and harsh winters reduce the need for cooling appliances for several months, resulting in lower annual utilization and slower replacement cycles. Even though ceiling fans can support warm-air circulation during winter, consumer awareness of this dual-use benefit remains limited.

Opportunities - Dual-Purpose Fans for Year-Round Utilization and Climate Adaptation

Dual-mount and reversible ceiling fan technologies represent an emerging market opportunity driven by erratic weather patterns and year-round demand for utilization. Dual-purpose fans that produce warm air suitable for winter heating, enabling year-round use and expanding the addressable market.

Shift from seasonal usage patterns toward continuous year-round deployment of ceiling fans in homes. Erratic weather conditions and unpredictable temperature patterns support demand for multifunctional ventilation solutions.

Consumers recognize the effectiveness of dual-purpose fans for energy conservation in both cooling and heating applications. Manufacturers are investing in advanced motor technologies that enable efficient warm-air circulation. The Canadian market is particularly adopting year-round ceiling fan strategies due to climate requirements.

Growing consumer recognition of heating-cooling capabilities enabling 20-30% additional energy savings versus seasonal solutions. Dual-functionality represents the fastest-growing opportunity attracting technology investment.

Home Renovation and New Construction Market Expansion

Residential construction and renovation activities represent a significant growth opportunity for ceiling fan market participants. Growing home improvement spending and renovation budgets are supporting increased ceiling fan installations. New residential construction projects incorporate modern ventilation systems as standard features.

Builder and contractor preference for high-efficiency ceiling fans supporting bulk purchasing opportunities. Rising disposable income of the middle-class urban population is enabling investment in home upgrades.

Increased home ownership rates and residential property development, particularly in warmer regions. Home renovation trends prioritize comfort and energy efficiency, supporting the adoption of ceiling fans. Consumer aspirations toward better lifestyles and enhanced home functionality are driving kitchen, bedroom, and living room installations. Construction market dynamics represent a structural opportunity supporting long-term demand growth.

Category-wise Analysis

Product Type Insights

Standard ceiling fans dominate the U.S. and Canada market, holding approximately 56% market share, largely due to their affordability, proven reliability, and widespread consumer familiarity. These fans remain the preferred choice for mainstream households seeking cost-effective cooling without advanced features.

Their strong presence in retail channels, broad product variety, and competitive pricing strategies support continued market leadership. Standard fans also benefit from easier installation, lower maintenance requirements, and strong replacement demand in both single-family homes and apartments.

Smart ceiling fans are the fastest-growing segment, driven by the growing adoption of home automation and connected living technologies. Consumers are rapidly shifting toward fans equipped with Wi-Fi connectivity, app-based controls, voice-assistant integration, and energy-efficient motors.

Usage Insights

Indoor ceiling fans dominate overall market consumption, accounting for approximately 82% of total demand, primarily due to their widespread use across residential spaces such as bedrooms, living rooms, kitchens, and dining areas. Homeowners rely on indoor fans for year-round air circulation, improved ventilation, and enhanced comfort, especially when paired with HVAC systems.

Their affordability, variety of design options, and easy installation further reinforce strong household adoption. Indoor fans also benefit from continuous replacement demand driven by renovation activities, interior upgrades, and energy-efficiency improvements. While outdoor and specialty fans are gaining attention, indoor ceiling fans remain the primary choice for most households, making them the backbone of market growth.

Regional Insights

U.S. Residential Ceiling Fan Market Trends

The United States dominates the regional market with the largest market share and consumption volumes. U.S. market leadership driven by growing demand for energy-efficient solutions and mainstream smart home technology adoption.

ENERGY STAR-certified products are commanding significant market share through consumer preference and regulatory support. Rapid urbanization in metropolitan areas supports residential market expansion. Major ceiling fan manufacturers, including Hunter Fan Company, Minka Group, Kichler Lighting, and Quorum International, maintain significant market presence.

Canada Residential Ceiling Fan Market Trends

Canada is experiencing rapid market growth driven by an energy-efficiency focus and year-round utilization patterns. Canadian consumers prefer dual-purpose fans for heating and cooling applications, driven by climate requirements.

Natural Resources Canada (NRCan) regulatory framework promoting energy-efficient appliance adoption. A growing Canadian middle class and rising disposable income are supporting residential investment. The Canadian market accounts for 15-20% of the North American residential ceiling fan market share despite a smaller population base.

Competitive Landscape

The U.S. & Canada residential ceiling fan market is moderately consolidated, with leading manufacturers such as Minka Group, Kichler Lighting LLC, Progress Lighting (Hubbell Inc.), Quorum International, and Big Ass Fans collectively accounting for approximately 40-45% of the market.

Their dominance is supported by strong brand recognition, extensive product portfolios, and robust retail and distributor networks across North America. Tier-two participants, including Craftmade International, Fanimation, and Generation Brands, capture notable regional market share through specialized designs, niche product offerings, and long-standing customer loyalty.

Emerging competitors and private-label brands are increasing competitive pressure by leveraging online retail platforms, aggressive pricing strategies, and faster product refresh cycles. Across the market, companies are placing strong emphasis on smart home integration, energy-efficient motor technologies, diverse and contemporary design aesthetics, and enhanced customer service, all of which support competitive positioning and help drive market share expansion.

Key Market Developments

- In 2025, Big Ass Fans announces commercial-to-residential product line expansion supporting large residential spaces and premium market positioning.

- In 2024, Hunter Fan Company launches Techne smart ceiling fan series with advanced IoT connectivity and voice control compatibility.

- In 2023, Minka Group expands product line with premium decorative ceiling fans incorporating BLDC motor technology for energy efficiency.

Companies Covered in U.S. & Canada Residential Ceiling Fan Market

- Minka Group

- Kichler Lighting LLC

- Progress Lighting (Hubbell Inc.)

- HINKLEY, INC

- Quorum International Inc.

- Big Ass Fans

- Craftmade International Inc.

- Fanimation

- Generation Brands

- LG Electronics, Inc.

- Honeywell International

- Hunter Fan Company

Frequently Asked Questions

The U.S. & Canada residential ceiling fan market was valued at US$ 5.6 billion in 2025 and is projected to reach US$ 8.5 billion by 2032, representing a CAGR of 6.1% during the forecast period.

The primary factors driving demand for residential ceiling fans include rising preference for energy-efficient, cost-effective cooling solutions and growing home renovation and new housing construction activities across the U.S. and Canada.

Standard Ceiling Fans command approximately 56% market share**, driven by affordability, proven reliability, consumer familiarity, established distribution networks, and widespread retail availability supporting mainstream household adoption.

United States maintains market leadership with largest market share driven by energy efficiency adoption, smart home technology integration, residential construction activity, and premium product consumer preference.

Online retail channels represent highest-value growth opportunity expanding at 7.54% CAGR** through e-commerce accessibility, price transparency, convenience-driven purchasing behavior, and direct consumer engagement supporting distribution channel transformation.

Market leaders include Minka Group (United States) with comprehensive product portfolio, Kichler Lighting LLC (United States) focusing on design aesthetics and quality, and Quorum International Inc. (United States) emphasizing affordability and variety, collectively representing approximately 40-45% market concentration**.