- Advanced Materials

- Polypropylene Random Copolymer (PPR) Pipe Market

Polypropylene Random Copolymer (PPR) Pipe Market Size, Share, Trends, Growth, and Forecast, 2025 - 2032

Polypropylene Random Copolymer (PPR) Pipe Market by Grade (Single-layer, Multi-layer), Application (Residential Plumbing, Commercial Infrastructure, Healthcare & Institutional Buildings), Regional Analysis for 2025 - 2032

Polypropylene Random Copolymer (PPR) Pipe Market Share and Trends Analysis

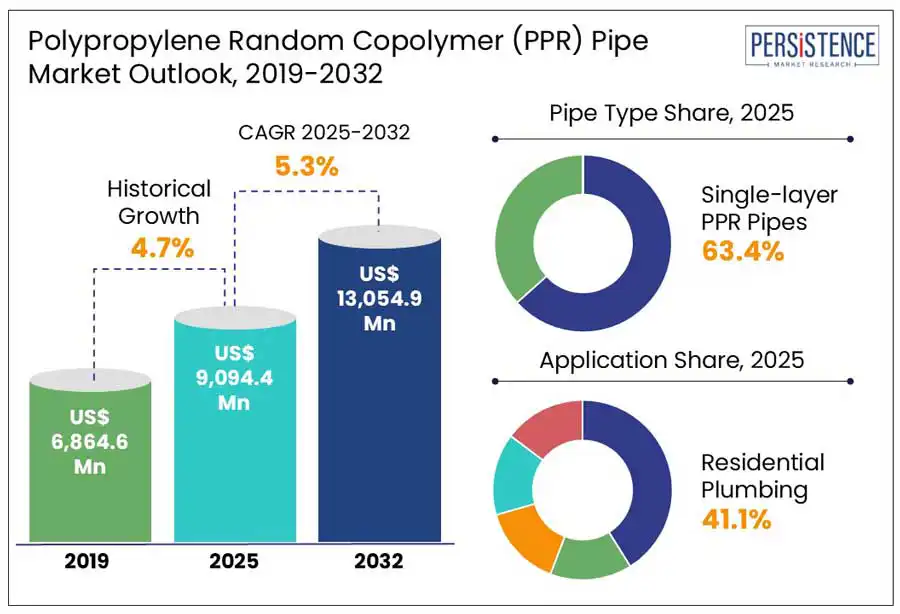

According to Persistence Market Research, the global Polypropylene Random Copolymer (PPR) Pipe market size is poised to reach US$ 9,094.4 Mn and projected to reach US$ 13,054.9 Mn to expand at a CAGR of 5.3% by 2032.

The industry’s trajectory reflects the growing use of durable and heat-resistant piping solutions across multiple infrastructure categories, aligning with the broader acceleration of global construction activity, particularly in emerging economies. Rising investments in residential plumbing systems and commercial infrastructure drive demand, supported by urbanization and increasing construction output in countries such as India and China. In India alone, over 31,000 new homes are required daily to meet population growth and urban housing demand. Piping systems essentially delivers long-term performance and reliability, especially in high-use areas like apartments, office towers, malls, and institutional buildings.

The market is also witnessing a rise in adoption across healthcare facilities, HVAC systems, agricultural water management, and industrial installations such as compressed air setups and chemical handling pipelines.

|

Global Market Attribute |

Key Insights |

|

Polypropylene Random Copolymer(PPR) Pipe Market Size (2024A) |

US$ 8,636.7 Million |

|

Estimated Market Size (2025E) |

US$ 9,094.4 Million |

|

Projected Market Value (2032F) |

US$ 13,054.9 million |

|

Value CAGR (2025 to 2032) |

5.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.7% |

Market Dynamics:

Driver - Growth in global infrastructure investment drives market expansion

The ongoing surge in infrastructure investments across multiple regions has been instrumental in fueling demand for high-performance piping systems.

In the U.S., total construction spending reached a seasonally adjusted annual rate of $2,195.8 billion in February 2025, showing a 2.9% increase over the previous year. This expansion, particularly in residential and non-residential sectors, underscores the growing requirement for efficient fluid transport systems across varied applications such as plumbing, water supply, and HVAC systems. The high adoption of modern materials in infrastructure upgrades has placed these piping solutions at the core of development efforts.

Europe's commitment to advancing public infrastructure through civil engineering and renovation projects further supports this trend. Germany witnessed a 20% rise in public construction orders in 2023, led by investments in energy-efficient buildings and transport infrastructure. Italy, too, experienced an 18% growth in civil engineering, which is projected to rise by another 20% in 2024 under the National Recovery and Resilience Plan.

These developments create a strong foundation for market expansion through robust infrastructure-led demand.

Restraint - Economic uncertainty and regional decline challenges growth

Despite strong momentum in infrastructure, regional economic headwinds have curtailed growth in certain segments, limiting full-scale market expansion.

In Germany, residential construction declined sharply in 2023, with housing permits dropping 27% and detached housing approvals plummeting over 40%. High construction costs, compounded by mortgage interest rates surging from 1.3% to over 4%, made new residential investments financially unviable for both households and commercial entities.

This downturn significantly reduced material demand across large-scale developments.

France witnessed a similar trajectory with an 8% decline in residential infrastructure in 2023 and an anticipated further contraction of 21.3% in 2024.

This trend is intensified by the phasing out of government incentives and tighter credit markets. These declines in core construction sectors have a direct impact on the demand for associated building materials, including piping systems, thus constraining consistent growth momentum across the market landscape.

Opportunity - Emerging opportunities in renovation and public infrastructure projects

While new residential developments may face slowdowns in certain geographies, renovation and public-sector investments are opening up fresh opportunities for market players. Italy's housing renovation market remained resilient in 2023, growing by 0.5%, supported by the Superbonus measure.

France's residential renovation market grew by 2.2% in the same year, driven by energy-efficiency upgrades. These trends indicate that renovation-focused policies and tax incentives play a vital role in maintaining material demand during broader economic uncertainty.

Public infrastructure continues to offer expansive opportunities, particularly with rising global emphasis on climate-resilient and energy-efficient systems. Germany's civil engineering orders rose 3% in 2023, supported by transport and rail infrastructure upgrades. Italy’s infrastructure spending under NRRP is projected to rise 20% in 2024, creating favourable conditions for suppliers aiming to serve large-scale public sector projects.

These channels present attractive opportunities for sustained growth and strategic market entry.

Market Key Trends

Surge in Civil Engineering Projects Boosts Material Demand

Major countries have reinforced their commitment to public infrastructure with growing investments in civil engineering projects. Italy’s civil engineering segment experienced an 18% increase in 2023 and is forecast to grow another 20% in 2024 under NRRP.

This growth is linked to upgrades in utilities, urban infrastructure, and transport systems, creating a sustained pipeline of demand for efficient piping solutions. Germany also recorded a 3% increase in civil engineering orders, bolstered by transport and energy renovation initiatives.

This trend is not isolated to Europe. In the U.S., public construction spending reached $509.3 billion in February 2025, up from $508.3 billion the previous month. Educational and highway projects in particular posted gains, reflecting continued federal and state-level infrastructure support.

The cumulative demand from these activities elevates the importance of durable, easy-to-install piping products in meeting project timelines and environmental compliance goals.

Shift Towards Sustainable Construction Materials Gains Momentum

The construction and infrastructure industries are increasingly aligning with global sustainability goals.

Government policies in Germany and France are encouraging energy-efficient renovations, while Italy’s infrastructure projects under the NRRP include strong provisions for green upgrades. In this context, eco-friendly and recyclable building materials are gaining priority in procurement decisions.

This sustainability push is leading to the increased adoption of thermoplastic piping systems that support reduced carbon footprints and enhanced durability.

As builders and contractors emphasize material performance, recyclability, and energy efficiency, demand is shifting in favor of advanced alternatives that meet these evolving benchmarks. These dynamics are setting a strong precedent for long-term material preference transitions within the infrastructure supply chain.

Category-wise Analysis

Grade Insights

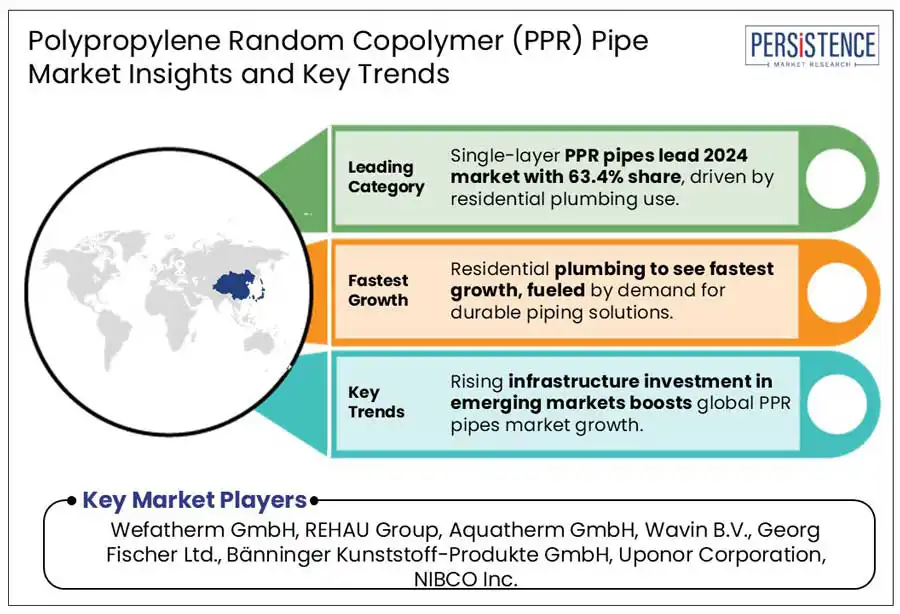

In 2024, single-layer pipes represent the largest share of the Polypropylene Random Copolymer (PPR) pipe market, accounting for 63.4%. Their popularity stems from ease of installation, thermal resistance, and suitability for a wide range of plumbing systems in both residential and commercial buildings.

The segment's momentum is supported by strong global trade activity, as demonstrated by KPT Piping System Private Limited receiving the ‘Export Leaders in PPR Pipes and Fittings’ award at the Asia Business Conclave Awards held in Singapore on February 1, 2024. The award emphasizes the company’s growing international footprint and aligns with a broader industry trend of expanding export capabilities in PPR pipe production.

Application Insights

The residential plumbing segment holds a 41.1% share of the PPR pipe market in 2024, driven by urban housing demand and infrastructure upgrades. Rising awareness of the advantages of PPR pipes, such as resistance to scaling and chemical corrosion, makes them a preferred choice for household water systems.

In March 2025, the Supreme Industries Limited entered into an MoU to acquire Wavin India’s piping business for $30 million plus net working capital. This strategic acquisition provides access to Wavin B.V.’s advanced piping technologies and expands Supreme’s manufacturing capacity, directly influencing the availability and innovation of residential piping systems.

In January 2025, GF Piping Systems partnered with Gradiant to enhance water and wastewater treatment solutions. This collaboration includes the integration of GF’s IR-63 M infrared welding machine into Gradiant’s R&D operations, supporting innovation in precise piping applications relevant to residential use.

Regional Insights

South Asia and Oceania Polypropylene Random Copolymer (PPR) Pipe Market Trends

South Asia and Oceania collectively account for 15.3% of the global PPR pipe market in 2024, with India driving most of the regional growth through massive infrastructure development. India's National Infrastructure Pipeline (NIP) and the Gati Shakti master plan are catalyzing high investments in water supply, urban infrastructure, and sanitation all major consumers of PPR pipes.

Housing-focused schemes such as the Smart Cities Mission and Housing for All continue to stimulate residential pipe demand. Sectors like power, roads, and irrigation absorbing more than 80% of infrastructure spending are scaling the need for durable and thermally resistant piping systems. Rising healthcare investments, reaching US$ 372 billion in FY23, and a booming medical tourism sector valued at US$ 7.69 billion in 2024 are also supporting demand for clean, non-corrosive PPR piping in hospitals and diagnostic facilities. These initiatives position South Asia, particularly India, as a critical engine of growth in the PPR pipe market.

Europe Polypropylene Random Copolymer (PPR) Pipe Market Trends

Europe accounts for a 21.2% market share in the global PPR pipe segment in 2024, with building construction supporting moderate growth despite challenges in civil engineering. In August 2024, construction of buildings rose by 0.9% in the Euro Area and 1.8% in the EU, while civil engineering declined by 2.1% and 3.9% respectively.

Countries such as Sweden, the Netherlands, and Romania showed notable gains in construction activity. PPR pipe demand is also growing in sectors like water infrastructure, where the EU sources 65% of its drinking water and 25% of its irrigation water from groundwater.

Competitive Landscape

The global polypropylene random copolymer (PPR) pipe market shows characteristics of moderate consolidation, driven by strategic expansions, acquisitions, and product innovation from established players. Companies like REHAU Group, Aquatherm GmbH, Georg Fischer Ltd., and Wavin B.V. continue to strengthen their foothold by aligning their solutions with large-scale infrastructure and commercial demands. These manufacturers are expanding offerings to cover wider application scopes, focusing on durability, efficiency, and system integration across segments.

KPT Pipes, Wefatherm GmbH, and Bänninger Kunststoff-Produkte GmbH are actively pushing for growth through international recognition, size enhancements, and technological upgrades. Their efforts to address evolving market needs in performance and scale reflect increasing competition. While the market leans toward consolidation due to high involvement from global leaders, the presence of regional innovators keeps it competitive, avoiding a purely oligopolistic structure.

Key Developments

- On October 5, 2023, KPT Pipes and Fittings Private Limited was recognized as “Prominent PPR Pipes and Fittings Manufacturers of the Year” at the House of Commons, UK Parliament. The company announced plans to become the first in India to launch 630mm diameter Polypropylene Random Copolymer (PPR) pipes in 2024, marking a significant product launch in the PPR pipe market.

- On June 28, 2024, REHAU launched its new PP-R fiber range, offering a complete O-ring-free plumbing solution for commercial and multi-residential buildings. This launch enables seamless integration with REHAU’s RAUTITAN PE-Xa system through a dedicated adapter, extending polymer piping solutions up to 125mm. The development addresses growing demand for larger-diameter hygienic pipework in complex projects.

Companies Covered in Polypropylene Random Copolymer (PPR) Pipe Market

- Wefatherm GmbH

- REHAU Group

- Aquatherm GmbH

- Wavin B.V.

- Georg Fischer Ltd.

- Bänninger Kunststoff-Produkte GmbH

- Uponor Corporation

- NIBCO Inc.

- Zhejiang Weixing New Building Materials Co., Ltd. (VASEN)

- Kalde

- KPT Pipes

- Euroaqua PPR Pipe

Frequently Asked Questions

The global market is projected to value at US$ 9,094.4 Million in 2025.

The market is poised to witness a CAGR of 5.3% from 2025 to 2032.

Growth in global infrastructure investment and rising demand for efficient residential plumbing solutions are driving the expansion of the PPR pipe market.

Emerging opportunities include renovation and public infrastructure projects driven by increasing government investments and the demand for durable, cost-effective piping solutions.

Wefatherm GmbH, REHAU Group, Aquatherm GmbH, Wavin B.V., Georg Fischer Ltd., Bänninger Kunststoff-Produkte GmbH, Uponor Corporation, and NIBCO Inc.