- Industrial Machinery

- Physical Testing Equipment Market

Physical Testing Equipment Market Size, Share, Trends, and Growth Forecast for 2025 - 2032

Physical Testing Equipment Market By Testing Type (Noise Vibration and Harshness, Rotating Machinery, Durability and Fatigue, Hardware in the Loop, Industrial Quality), Product, Industry, and Regional Analysis from 2025 to 2032

Physical Testing Equipment Market Share and Trends Analysis

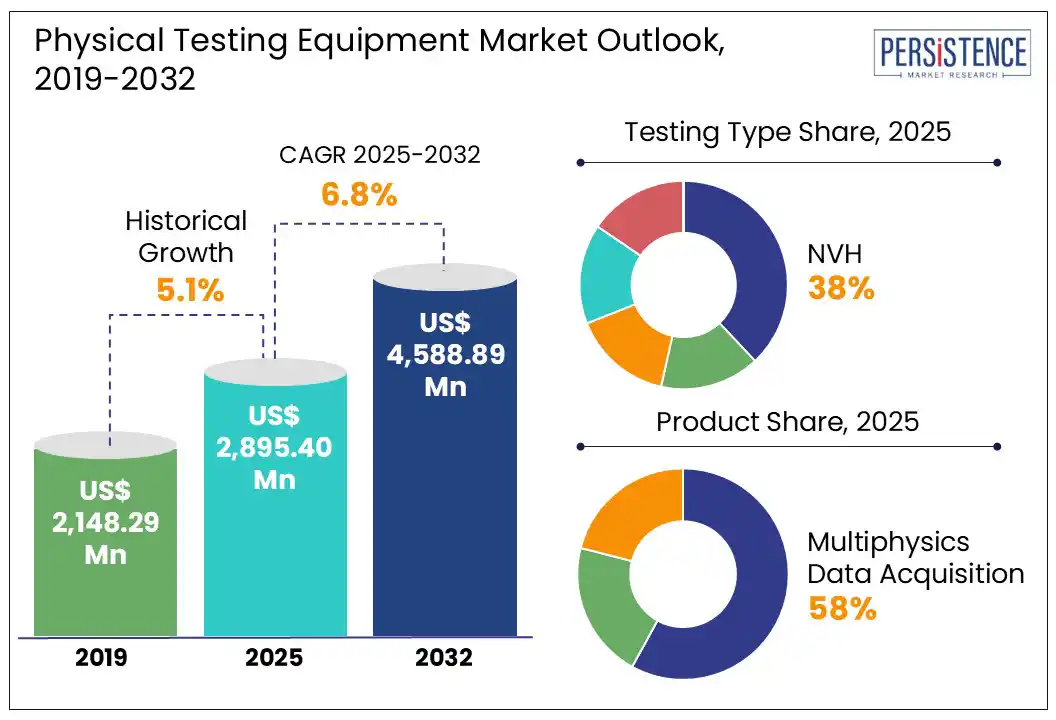

The global physical testing equipment market size is likely to be valued at US$ 2,895.4 Mn in 2025 and is estimated to reach US$ 4,588.9 Mn in 2032, at a CAGR of 6.8% during the forecast period 2025 - 2032.

Physical testing equipment used for evaluating strength, durability, and performance of materials and products, is driving advancements across industries such as manufacturing, automotive, and aerospace. The market is growing due to the adoption of smart sensors, AI analytics, and cloud connectivity. These technologies enable predictive diagnostics and remote monitoring, streamlining product development and reducing downtime. Key growth factors include rising demand for real-time data analysis, a focus on predictive maintenance to cut costs, improved product quality through advanced testing, and increased IoT integration for seamless equipment connectivity.

Key Industry Highlights:

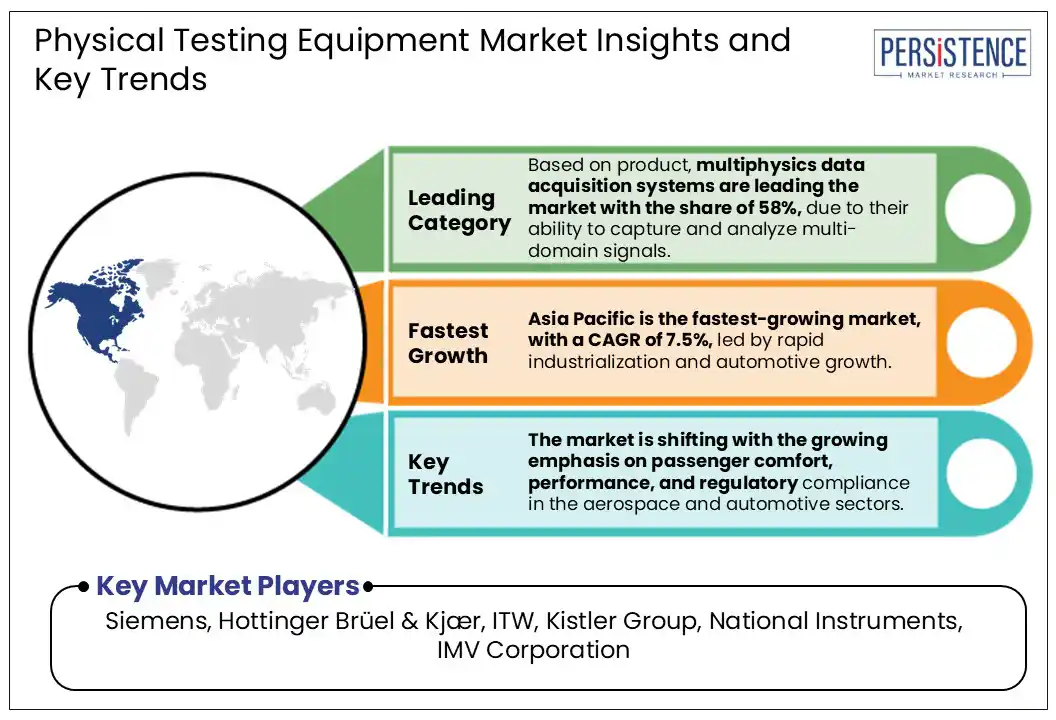

- The multiphysics data acquisition systems segment is projected to lead the market with a share of 58%, due to their ability to capture and analyze multi-domain signals.

- By industry, the automotive sector is likely to dominate with approximately 40% of the market share, due to its physical testing for ADAS and EV development.

- The NVH testing segment is expected to dominate the market with a share of 38%, due to its widespread use in aerospace and automotive industries for performance optimization and regulatory compliance.

- The growing emphasis on passenger comfort, performance, and regulatory compliance in the aerospace and automotive sectors is a major driver.

- With increasing regulatory pressure and safety standards, durability and fatigue testing is seeing rising demand in chemical and plastic industries, especially for validating product performance under long-term stress and harsh environments.

- North America dominates the market due to the prominence of aerospace and automotive industries in the region and R&D efforts undertaken.

- Asia Pacific is anticipated to be the fastest-growing market with a share of 26%, due to rapid industrialization and automotive growth.

|

Market Attribute |

Key Insights |

|

Physical Testing Equipment Market Size (2025E) |

US$ 2,895.4 Mn |

|

Projected Market Value (2032F) |

US$ 4,588.9 Mn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

6.8% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

5.1% |

Market Dynamics

Driver - Rising Demand for NVH Testing Driven by Comfort, Compliance, and Innovation

Emphasis on safety, performance, and regulatory compliance drives the demand for Noise, Vibration, and Harshness (NVH) testing in the aerospace and automotive industries. These sectors rely heavily on advanced testing solutions to reduce unwanted noise and vibrations, enhance passenger experience, and meet stringent global regulations.

Increasing regulatory mandates on safety and comfort, such as UN Regulation No. 51 for vehicle noise emissions and FAA standards for aircraft acoustic certification are prompting OEMs to adopt advanced NVH testing tools. Government programs such as the U.S. Department of Energy’s Vehicle Technologies Office (VTO) initiatives are further supporting the development in sustainable mobility and lightweight aircraft technologies, driving the need for robust testing frameworks.

Manufacturers are expanding their market reach through investments. For instance, in October 2022, Hottinger Brüel & Kjær, launched the LDS V8800 + XPA?K medium-force shaker, designed to deliver high shock and vibration performance for R&D and product validation. This innovation caters to evolving aerospace and automotive requirements for component durability, acoustic refinement, and regulatory compliance.

Restraint - High Equipment and Maintenance Costs

The high cost of advanced testing systems and their maintenance, that limits adoption among small and medium-sized enterprises, hinders the market growth. Refined equipment such as multiphysics data acquisition systems, hardware-in-the-loop (HIL) setup, and high-force shakers require significant initial investment, skilled labor, and developed infrastructure.

In emerging economies, such challenges are more pronounced, where many manufacturers prioritize production efficiency over high-end validation systems due to tight budgets. The operational costs, such as equipment downtime, spare parts, and skilled workforce training, create further barriers to widespread implementation.

Opportunity - Rising Demand in Plastics and Chemical Sector

The expanding applications of durability, fatigue, and quality testing in industries such as plastics, chemicals, and advanced manufacturing present numerous opportunities . The manufacturers are increasingly adopting the physical testing systems due to strict regulations that focus on product reliability, safety, and sustainability.

Government initiatives and policies are promoting manufacturers to expand their product portfolio. For instance, India’s Production Linked Incentive scheme for specialty chemicals and the U.S. Infrastructure Investment and Jobs Act, which promotes the use of innovative materials and technologies, are bolstering the industrial expansion and quality control investments.

The market players are also investing in product innovations to cater to the end-users with multipurpose products. For instance, in April 2025, Kistler updated its MaDaM measurement data management software to optimally help its customers to accelerate development, save time, and cut costs, including the field of measurement data management. The update features improved organization, search capability, and harmonization of data to simplify the comparison of relevant measurements. Reporting, data mining, and metadata handling functionalities have also been optimized to support efficient analysis and decision-making.

Category Wise Analysis

Testing Type Insights

The Noise, Vibration, and Harshness (NVH) testing is expected to dominate the market with a share of approximately 38%, due to its critical role in enhancing performance and comfort. NVH testing is mostly used in the automotive and aerospace sectors. With the rise of EVs, reducing vibrations and tonal noise has grown more complex, demanding greater precision. In aerospace, it ensures acoustic comfort and structural integrity while meeting strict noise regulations.

Government programs such as the European Union’s vehicle noise limits, and FAA noise standards for aircraft certification push manufacturers toward advanced NVH testing systems. The sustainability goals are driving OEMs to design quieter, lighter vehicles and aircraft, further increasing testing complexity and volume.

The manufacturers are investing in product expansion to meet the growing demand from industries. For instance, in September 2022, HBK (formerly Brüel & Kjær) introduced comprehensive vibration testing systems tailored for vehicle battery validation. These turnkey solutions integrated electrodynamic shakers, climatic chambers, and advanced DAQ to test compliance with UN?38.3/ECE?R100 standards under mechanical, thermal, and electrical stresses.

Product Insights

The Multiphysics Data Acquisition (DAQ) systems is projected to dominate, holding a market share of approximately 58%, driven by their ability to capture complex, multi-domain data across mechanical, thermal, and electrical parameters. These systems are essential in environments where linked subsystems and smart components require real-time analysis.

Sectors such as aerospace, automotive, and manufacturing rely heavily on high-performance data acquisition (DAQ) platforms for tasks ranging from prototype validation to end-of-line testing. The shift toward electrification, lightweight materials, and intelligent control systems in next-generation vehicles and aircraft is accelerating the demand for advanced DAQ tools.

Manufacturers are developing their portfolios to address these needs. For instance, in February 2025, National Instruments expanded its CompactDAQ (cDAQ) portfolio with the introduction of the cDAQ?9187 and cDAQ?9183 Ethernet chassis, along with the NI?9204 analog input module. Designed for robust benchtop and field applications, these systems feature enhanced environmental resilience, streamlined USB-C and snap-in connectivity, and seamless integration with NI’s FlexLogger software.

End-use Industry Insights

The automotive industry is leading the physical testing equipment market with a share of around 40%, driven by rapid advancements in EVs and autonomous driving technologies. The automakers are increasingly relying on physical testing systems to validate components such as batteries, motors, drivetrains, and ADAS sensors under mechanical, thermal, and vibration stress.

Governments across the globe are actively supporting the industrial transformation. The government initiatives such as the European Green Deal, India’s FAME II scheme, and the U.S. Inflation Reduction Act, provide incentives for EV manufacturing and quality assurance infrastructure, boosting investments in physical testing technologies.

Regional Insights

North America Physical Testing Equipment Market Trends

North America is projected to dominate, accounting for approximately 33% of the share, driven by a strong presence of aerospace and defense industries, along with established testing infrastructure. The North America physical testing equipment market is primarily focused on technological innovation and regulatory compliance, which led to the widespread adoption of physical testing systems.

Government support through programs such as the U.S. DoE’s Advanced Materials and Manufacturing Technologies Office and the Department of Defense Testing and Evaluation program is driving the development of advanced testing capabilities. Leading companies in the U.S. and Canada are investing in high-performance testing to meet FAA, EPA, and NHTSA regulations, particularly for aircraft, EVs, and military-grade equipment.

Europe Physical Testing Equipment Market Trends

Europe remains a key region in the physical testing equipment market, driven by strict regulatory standards and advanced industrial infrastructure. The push for sustainability, lightweight materials, and low-emission transportation further boost the need for high-precision testing solutions.

Government initiatives such as Horizon Europe and Germany’s Industrie 4.0 are accelerating digital transformation and the integration of smart testing systems in manufacturing. The region’s automotive, aerospace, and chemical sectors heavily rely on durability, fatigue, and NVH testing to ensure compliance with safety, environmental, and performance regulations such as EURO 7, REACH, and EASA certifications.

Asia Pacific Physical Testing Equipment Market Trends

Asia Pacific is fast-growing in the physical testing equipment market, fueled by rapid industrialization and expanding automotive production in countries including China, India, Japan, and South Korea. Manufacturing, rail, and plastic industries in these regions are increasingly adopting advanced testing systems to meet both domestic and international quality standards.

Government initiatives such as China’s Made in China 2025, India’s Make in India, and Japan’s Society 5.0 are promoting local innovation, technology adoption, and export-oriented manufacturing. These programs are driving the need for a robust physical testing infrastructure.

The market players are strengthening their regional capabilities by partnering with the supply chain players. For instance, in May 2025, the Kistler Group, the global market leader in dynamic measurement technology, stepped up its long-standing collaboration with KELLER Pressure, the leading manufacturer of piezoresistive pressure sensors. The companies signed a renewed agreement to further expand their strategic partnership, leverage synergies, and pursue a focused strategy.

Competitive Landscape

The global physical testing equipment market is moderately consolidated by competition among leading players. Each player is offering a broad portfolio of testing solutions tailored to various industries. The market is innovation-driven, with companies focusing on enhancing precision, speed, and integration capabilities to address evolving demands.

The companies are expanding their geographic footprint and service capabilities to address growing demand in emerging markets. As industries transition toward smart manufacturing and electrification, the market remains dynamic, with a strong emphasis on R&D, digitalization, and customer-centric innovation.

Recent Developments:

- In September 2024, Emerson broadened its NI™ USB data acquisition (DAQ) range with the launch of the NI?mioDAQ, a high-performance, bus-powered USB DAQ device to help engineers enhance the product quality and reduce time-to-market for advanced electronics. NI?mioDAQ delivered superior measurement capabilities, robust software support, and a streamlined setup experience.

- In May 2023, NI, formerly known as National Instruments, introduced the widespread availability of SystemLink™ Enterprise. Revolutionizing how companies use test insights and data to drive product and business performance, SystemLink Enterprise companies to manage test systems, data collection, and reporting from a central location and to use product-centric analytics for actionable insights.

Companies Covered in Physical Testing Equipment Market

- Siemens

- Hottinger Brüel & Kjær

- ITW – Illinois Tool Works

- National Instruments

- IMV Corporation

- Kistler Group

- DEWESoft

- ZwickRoell

- Axiometrix Solutions

- Tinius Olsen

- ABB

Frequently Asked Questions

The physical testing equipment market is projected to reach US$ 2,895.4 Mn in 2025.

The growing emphasis on passenger comfort, performance, and regulatory compliance in aerospace and automotive sectors is a major driver.

The market is projected to witness a CAGR of 6.8% from 2025 to 2032.

With increasing regulatory pressure and safety standards, durability and fatigue testing is witnessing a rising demand in chemical and plastic industries, especially for validating product performance under long-term stress and harsh environments.

Major players in the global physical testing equipment market include Siemens, Hottinger Brüel & Kjær, ITW – Illinois Tool Works, National Instruments, and IMV Corporation.