- Electrical Equipment & Services

- Permanent Magnet Motor Market

Permanent Magnet Motor Market Size, Share, and Growth Forecast for 2025 - 2032

Permanent Magnet Motor Market By Design Type (Brush, Brushless), Motor Type (AC, DC), Power Rating (upto 25kW, 25k-100kW, 100-300kW) Magnet Material (Ferrite, Neodymium-Boron-Iron (NDBFe), Samarium-Cobalt (Sm-Co)), Application, and Regional Analysis for 2025 - 2032

Permanent Magnet Motor Market Size and Trends Analysis

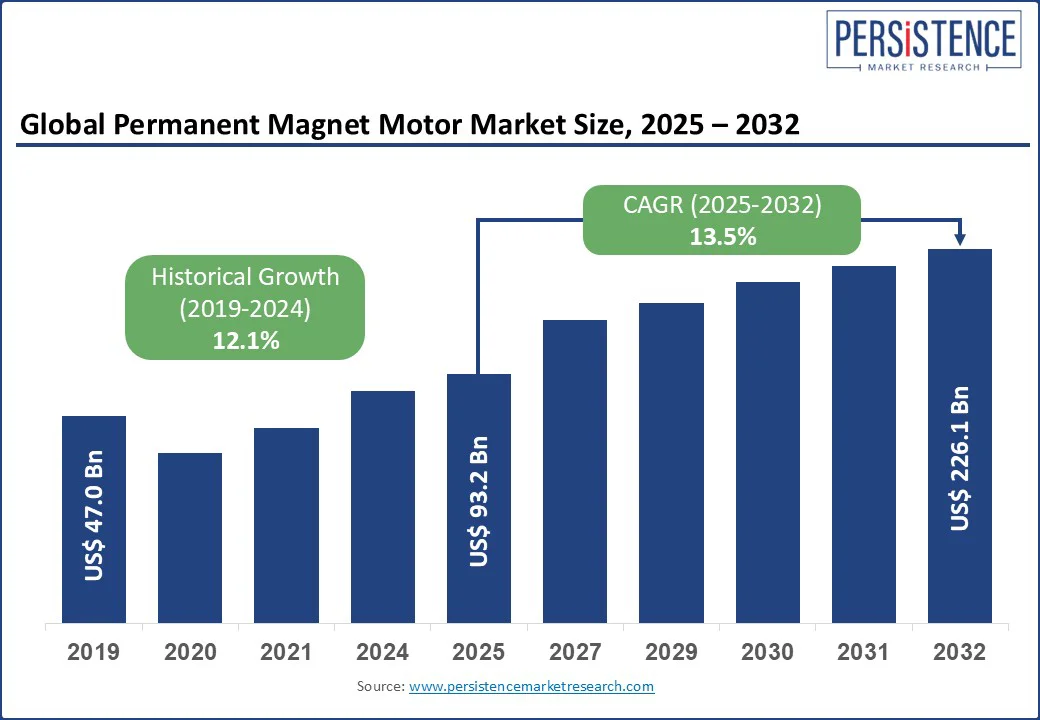

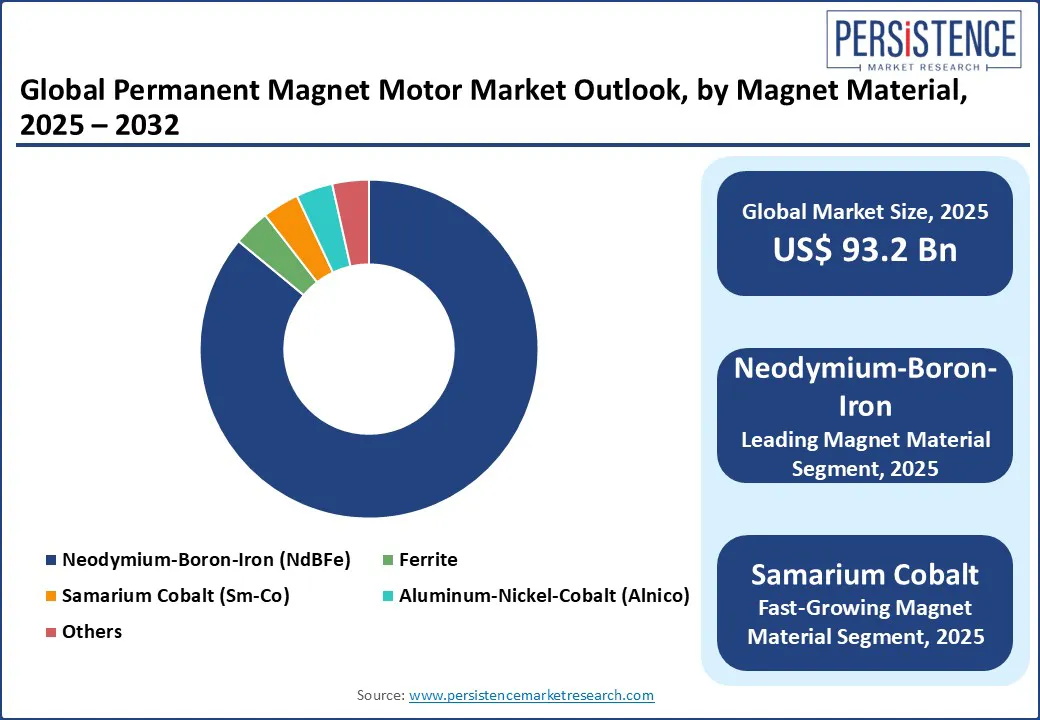

The global permanent magnet motor market size is likely to be valued at US$ 93.2 Bn in 2025 and is estimated to reach US$ 226.1 Bn in 2032, at a CAGR of 13.5% during the forecast period 2025 - 2032.

Permanent magnets, made from materials such as iron, nickel, cobalt, or rare-earth elements such as neodymium, generate a consistent magnetic field without external power, making them vital for applications such as electric motors, generators, and medical devices. From a market perspective, the global demand for permanent magnets, particularly neodymium-based ones, is surging due to their critical role in renewable energy technologies, electric vehicles, and consumer electronics.

The market is projected to grow significantly, driven by advancements in material science and increasing adoption of green energy solutions, though supply chain challenges for rare-earth elements may impact pricing and availability. In addition, the permanent magnet motor market growth is driven by the production of electric vehicles that require highly efficient permanent magnet (PM) motors. Similarly, the growing adoption of PM motors in industrial applications, consumer appliances, and power equipment is also boosting the product demand.

Key Industry Highlights:

- The automotive segment is projected to lead the market in 2025 with approximately 35% market share due to the extensive use of PM motors in electric vehicles (EVs).

- The booming market for power equipment such as generators, wind turbines and hydro power is expected to drive the demand for PM motors with about 14% CAGR during the forecast period.

- Neodymium-based synchronous motors hold the largest market share due to their efficiency and preferred choice in high-demand applications.

- The rising adoption of PM motors in medical devices and HVAC systems is expected to create lucrative opportunities in the coming years.

- PM motors in generators, wind turbines, and hydropower are expanding at around 14% CAGR, addressing the demand for clean energy infrastructure.

- Rising investments in robotics and smart manufacturing (with > 4.2 million industrial robots by end-2023) boost the demand for PM motors that offer precise control, compactness, and connectivity.

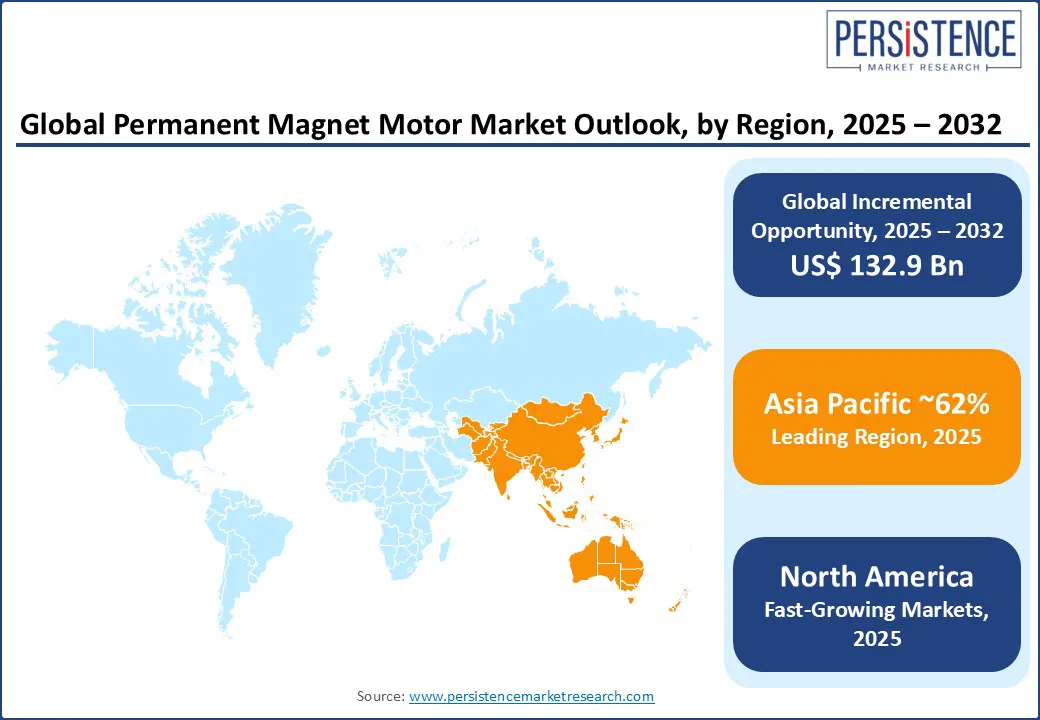

- Asia Pacific leads the market for permanent magnet motors due to rapid growth in end-use sectors, followed by North America and Europe.

|

Global Market Attribute |

Key Insights |

|

Permanent Magnet Motor Market Size (2025E) |

US$ 93.2 Bn |

|

Market Value Forecast (2032F) |

US$ 226.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

13.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

12.1% |

Market Dynamics

Driver - Increasing Adoption of Energy-efficient Brushless Motors in Automotive Electric Vehicle Powertrains is Driving the PM Motor Market Growth

The increasing use of energy-efficient brushless permanent magnet motors in EV powertrains is driven by the rapid rise in electric vehicle adoption. In 2023, global EV sales reached nearly 14 million units, reflecting an approximate 35% year-on-year increase, with battery electric vehicles (BEVs) making up 70% of those sales. EVs accounted for about one-fifth of new car sales worldwide, while in China, new energy vehicles hit 12.9 million units, representing roughly 40% market share.

This swift growth in EVs boosts the demand for compact, high-torque, and energy-efficient PM brushless motors in powertrains. Projections indicate that global EV sales will be 20 million by the end of 2025, with BEVs expected to grow around 25% annually. By 2030, EV sales could reach 39 million units, supported by increasing battery capacity and strong policy incentives, further accelerating the shift toward permanent magnet motors.

Restraint - High Cost and Supply Constraints of Rare-earth Magnet Materials Limit Market Expansion

The growth of the permanent magnet motor market is being held back by the high costs and limited availability of rare-earth materials such as neodymium and praseodymium. Since China controls over 90% of the global rare-earth magnet processing, the supply chain is vulnerable to export restrictions. Prices are highly volatile, with NdPr costing between US$75 and US$180 per kilogram outside China, compared to about US$ 62 per kilogram within the country.

The demand for NdFeB magnets is increasing at a rate of 7–8% annually, but supply is only growing by around 5%, leading to shortages. OEMs are facing rising costs and shipment delays of over 45 days. As automakers stockpile materials to avoid shortages and no reliable rare-earth-free alternatives exist yet, the dependence on expensive and geopolitically concentrated resources continues to be a major challenge for market growth.

Opportunity - Rising Industrial Automation Boosts the Demand for Permanent Magnet Motors in Industrial Applications

The rise of industrial automation offers a significant growth opportunity for the permanent magnet motor market. Global industrial automation is expanding quickly, with automation and control systems expected to grow at over 10% annually through 2032. In North America, industrial robot orders increased by 14.1% year-on-year in Q3 2024. By the end of 2023, over 4.28 million industrial robots were in operation worldwide, highlighting the global move toward smart manufacturing.

Permanent magnet motors are increasingly preferred in automation due to their reliable performance, precise motion control, and suitability for space-constrained environment, which makes them ideal for applications such as robotics, conveyors, CNC machines, and AGVs. As Industry 4.0 and IIoT adoption speed up, PM motors provide benefits in connectivity, predictive maintenance, and real-time operational adjustments, making them vital for modern and future-ready manufacturing environments.

Category Wise Analysis

Magnet Material Insights

Neodymium-Iron-Boron magnets are projected to dominate the permanent magnet motor market, capturing a share of approximately 86% in 2025, due to their outstanding magnetic properties such as high flux density, coercivity, and energy product. These qualities make them perfect for high-performance uses such as EVs and industrial motors. At present, over 80–90% of modern EVs rely on NdFeB-based motors, with about 1.5 kg of NdFeB magnets needed per vehicle, enabling efficient and compact powertrain designs.

Permanent magnet synchronous generators (PMSGs) are used globally in nearly all offshore wind turbines and about 76% of offshore units overall. With approximately 110 GW of new wind capacity being added annually, the adoption of PMSG technology continues to grow, driving NdFeB magnet demand. Hydropower systems also benefit from permanent magnet generators, which improve efficiency and allow more compact turbine designs. These renewable energy applications further reinforce the dominance of NdFeB magnets in the global permanent magnet motor market.

Power Rating Insights

Permanent magnet motors with power ratings up to 25 kW are seeing rapid growth in demand, especially in consumer appliances and light industrial uses. Worldwide, over 300 million electric motors power devices such as pumps, fans, and HVAC systems, accounting for nearly 40% of total electricity consumption, switched to highly efficient PM motors in this range, reducing energy use by 20–30%, with a typical payback period of one to three years.

Beyond household appliances, low-power PM motors are widely used in medical devices, power tools, and compact aerial drones. In healthcare, these motor-powered surgical instruments, infusion pumps, and mobility aids offer precise control and quiet operation. In cordless power tools, PM motors provide high torque and energy efficiency in compact sizes.

Similarly, their lightweight and responsive performance makes them ideal for drone propulsion systems. The global cargo drones market size is expected to reach US$ 16.5 Bn by 2032 witnessing a staggering CAGR of 34.1% between 2025 and 2032. Such expansion in end-use markets will bolster the demand for low-powered PM motors.

Regional Insights

Asia Pacific Permanent Magnet Motor Market Trends

Asia Pacific, especially China and India, is anticipated to dominate the market, accounting for a share of approximately 62% in 2025, fueled by rapid industrial growth and strong government incentives. China leads the region, accounting for over 60% of Permanent Magnet Synchronous Motor (PMSM) demand, due to its dominant role in EV manufacturing and industrial automation. India, responding to increasing demand, imported over 53,000 tonnes of rare-earth magnets in FY 2024 to support expanding EV and gear motor industries.

To reduce reliance on Chinese imports, India has launched multi-year programs and financial incentives aimed at localizing rare-earth magnet production. Companies such as Sona Comstar are gearing up to produce magnets domestically, with EVs already making up about one-third of their revenues. Government initiatives such as PLI and FAME are further boosting the adoption of PM motors across the automotive, automation, and infrastructure sectors. The combination of industrial output, electrification targets, and evolving supply chains is poised to solidify Asia Pacific’s position as a major growth engine in the global permanent magnet motor market.

North America Permanent Magnet Motor Market Trends

In North America, the aerospace and defense sectors are key drivers of demand for permanent magnet motors as they require compact, lightweight, and high-performance systems. Over 40% of PMSM demand in the U.S. comes from these industries, where motors are used in applications such as aircraft control surfaces, UAVs, missile systems, and naval equipment. The U.S. is making significant investments in domestic NdFeB magnet production to secure critical defense supply chains, aiming to fulfill up to 51% of national magnet needs by 2026.

North America also benefits from a strong industrial and innovation ecosystem. Over 35% of automated systems in the region use permanent magnet synchronous motors, showing widespread adoption in manufacturing, robotics, and energy sectors. Companies are increasing local magnet production capacity, supported by strategic contracts for defense and industrial uses. The combination of advanced manufacturing, government support, and aerospace demand positions North America as a high-potential market for permanent magnet motors.

Europe Permanent Magnet Motor Market Trends

Europe’s strict environmental regulations and the growing adoption of EVs are major factors driving the increased use of permanent magnet motors in the region’s automotive sector. In 2024, EVs made up 22.7% of all new car registrations in the EU, with BEV sales rising by 37%. Plug-in hybrids accounted for 8% of registrations, showing strong momentum toward low-emission vehicles.

In the first quarter of 2025, EV sales in Europe grew 28% to reach 573,500 units, largely fueled by tighter CO2 emission standards and government incentives. Permanent magnet motors, valued for their high efficiency, compact size, and strong torque performance, are becoming the preferred choice in EV powertrains. With the EU targeting a 55% reduction in emissions by 2030 and planning to ban new internal combustion engine vehicles by 2035, adopting permanent magnet motors in Europe is both a regulatory requirement and a technological advantage for automakers.

Competitive Landscape

The global permanent magnet motor market is highly competitive, with key players such as Nidec Corporation, Siemens AG, ABB Ltd., and Toshiba Corporation focusing on strategic developments such as mergers, acquisitions, and capacity expansions. For instance, Nidec has been aggressively investing in EV motor production facilities across Europe and Asia, aiming to secure supply chains and meet rising demand from automotive OEMs.

Companies are also investing in rare-earth material sourcing and innovation to reduce supply risk and enhance motor performance. For example, Siemens is developing advanced magnet-free motor technologies to diversify offerings, while ABB has integrated AI and IoT capabilities into its motor systems to support smart manufacturing. These strategies not only strengthen the market presence but also set benchmarks for energy efficiency, reliability, and technological advancement, shaping future industry standards.

Key Industry Developments

- In March 2025, AML developed PM-Wire™, a scalable technology for customized permanent magnets, enhancing motor efficiency, reducing assembly complexity, and lowering costs. This innovation strengthened domestic supply chains and supported the permanent magnet motor market by enabling high-performance, application-specific magnet solutions, reducing reliance on imported rare-earth materials.

- In June 2025, ABB unveiled its LV Titanium Variable Speed Motor platform in India, combining an IE5 ultra-premium efficiency permanent magnet motor and integrated variable-speed drive. This plug-and-play, compact solution (1.5–30 kW) offered quieter operations, high low-speed torque, and space-saving design.

Companies Covered in Permanent Magnet Motor Market

- Siemens AG

- Rockwell Automation

- Johnson Electric Holdings Ltd.

- ABB Ltd.

- Allied Motion Technologies Inc.

- Ametek Inc.

- Toshiba Corporation

- Franklin Electric Company Inc.

- Allied Motion Technologies Inc.

- Nidec Corporation

- Danaher Corporation

- WEG

- Yaskawa America, Inc.

- Carter Motor Company

- Dumore Motors

- FAULHABER Group

Frequently Asked Questions

The Permanent Magnet Motor market size is estimated to be valued at US$ 93.2 Bn in 2025.

Increasing adoption of energy-efficient brushless motors in automotive electric vehicle powertrains is the key demand driver for Permanent Magnet Motor market.

In 2025, Asia Pacific region is projected to dominate the market with 62% share in the global Permanent Magnet Motor market.

Permanent magnet motors with power ratings up to 25 kW are seeing rapid growth in demand, especially in consumer appliances and light industrial uses.

Siemens AG, Rockwell Automation, Johnson Electric Holdings Ltd, ABB Ltd., and Allied Motion Technologies Inc. are the leading players.