- Industrial Goods & Service

- Permanent Magnet Market

Permanent Magnet Market Size, Share, Trends, and Growth Forecast for 2025 - 2032

Permanent Magnet Market by Product Type (Neodymium Iron Boron, Samarium Cobalt, Aluminum Nickel Cobalt, Ferrite), End-use (Automotive, Electrical and Electronics, Energy, Aerospace and Defense, Healthcare, Other), and Regional Analysis from 2025 - 2032

Permanent Magnet Market Size and Trends

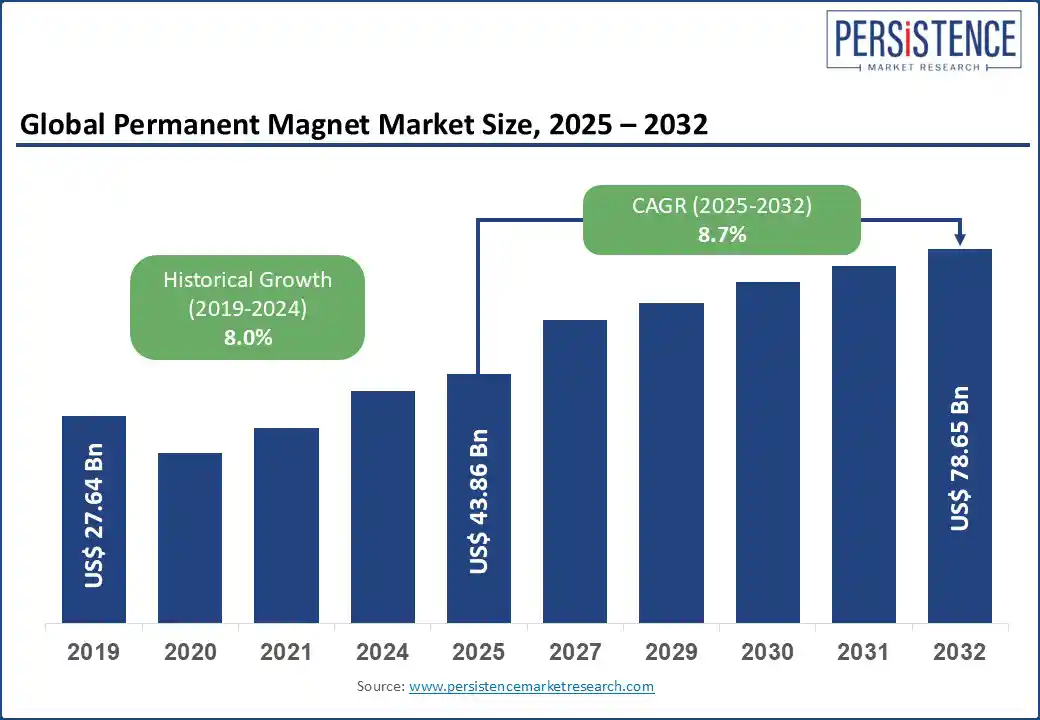

The global permanent magnet market is likely to be valued at US$ 43.86 Bn in 2025 and is expected to reach US$ 78.65 Bn, growing at a CAGR of 8.7% by 2032. The rise in popularity of electric vehicles (EVs) is driving the need for permanent magnets in the EV industry. These magnets create a magnetic field without an external power source, making them essential in various high-efficiency applications. The magnetic field caused by permanent magnets converts the electricity into torque, making it a critical component for EVs. According to IEA, EV use has continued to grow rapidly worldwide, with the global sales increasing from 716,000 vehicles in 2015 to 17 million vehicles in 2024.

Key Highlights:

- Rising use of NdFeB magnets in EVs to enhance performance, efficiency, and compactness, significantly driving demand.

- China’s dominance and export restrictions on rare earth materials disrupt global supply chains and introduce pricing volatility, restraining stable growth in the magnet market.

- The widespread adoption of compact electronic devices, such as smartphones, wearables, and laptops, creates a market opportunity.

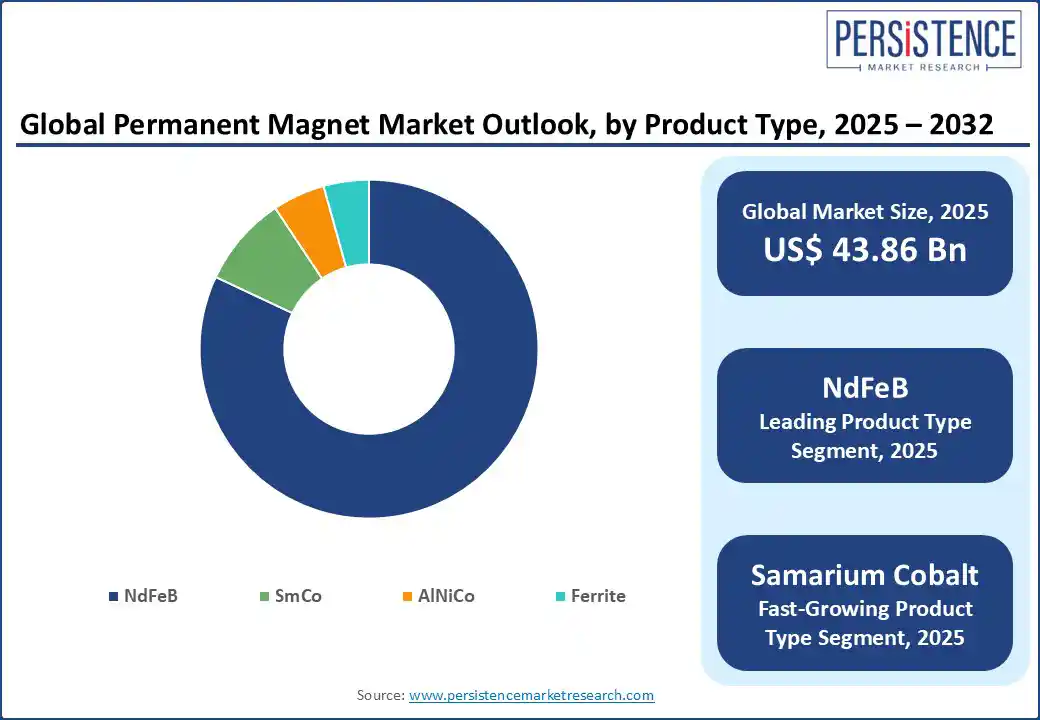

- In terms of product type, the Neodymium Iron Boron (NdFeB) magnet is dominating with a share of 82%, due to its exceptional strength, thermal stability, and compact form.

- Based on the end-use, the automotive sector is dominating the market with a share of 30%, due to heavy demand from the EV sector.

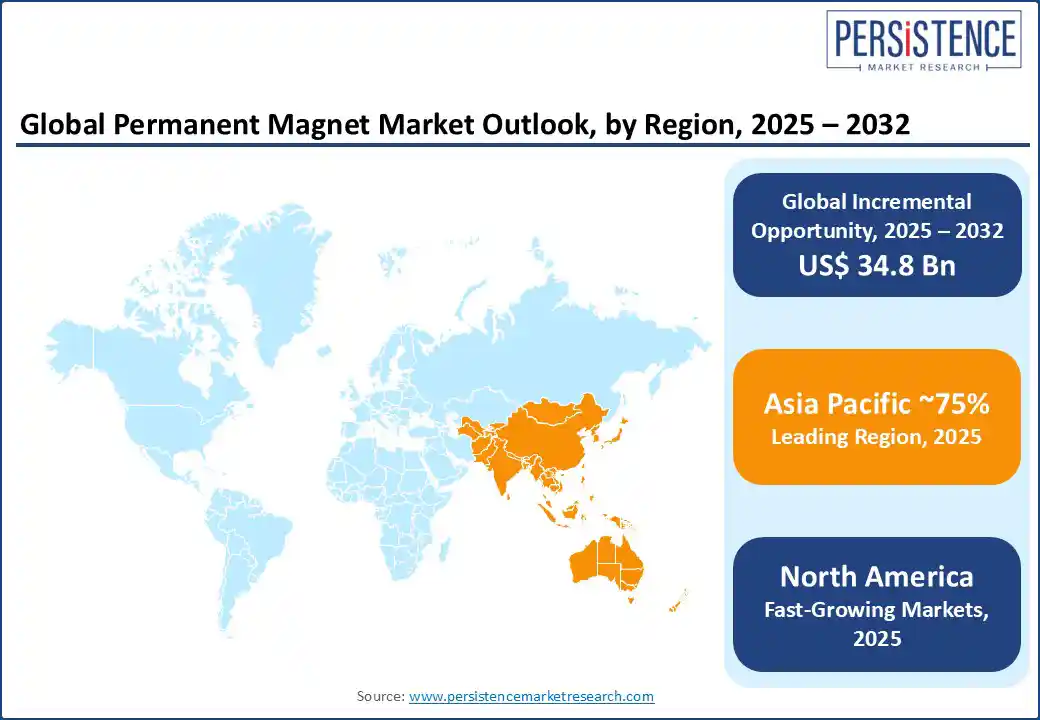

- With a share of 12% the North America is strengthening strategic expansion and refining capabilities to reduce reliance on imports.

- The European market, with a share of 10% is investing in magnet recycling and localized production to support clean mobility, energy transition, and industrial electrification goals under sustainability-focused policies.

- Asia Pacific region leads the market with 75% share of global permanent magnet, driven by China’s supply chain control and strong demand from electronics, automotive, and renewable sectors.

|

Global Market Attribute |

Key Insights |

|

Permanent magnet market Size (2025E) |

US$ 43.86 Bn |

|

Projected Market Value (2032F) |

US$ 78.65 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

8.7% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

8.0% |

Market Dynamics

Driver - The Rising Market of EVs is Driving the Demand for Permanent Magnets

The automotive industry is constantly evolving with advancements in technology. In recent years, the rising demand for EVs has shifted the focus of the automotive industry towards sustainable transportation. The permanent magnets generate their own constant magnetic field, which is used to create the motion in the vehicle. The EVs continue to make progress toward becoming a dominant automotive vehicle globally. Electric car sales in 2023 were 3.5 million higher than in 2022, a 35% year-on-year increase. This indicates robust growth even as many major markets enter a new phase, with uptake shifting from early adopters to the mass market. According to the European Institute of Innovation and Technology, in 2019, about 5,000 tons of permanent magnets were used in EVs worldwide. By 2030, the number may rise to between 40,000 and 70,000 tons on a global level, depending on the anticipated growth scenario.

Restraint - Export Controls and Trade Tensions Threaten Permanent Magnet Market Stability

Geopolitical tensions between China and Western countries are significantly restraining the global permanent magnet market. The permanent magnets are primarily produced from the rare earth elements, which are sourced from mines. China currently dominates the rare earth magnet supply chain, accounting for approximately 90% of global refining and magnet production capacity.

In April 2025, China imposed new export licensing requirements on the 7 critical rare earth elements, such as neodymium, dysprosium, and terbium, and rare-earth magnets used in electric vehicles and high-tech industries. This results in a drop of Chinese exports of rare-earth magnets, by up to 74% in April and over 58% to the U.S., triggering global supply chain disruptions and severe price volatility. The Western companies are connecting with the governments to respond to this situation. For instance, in July 2025, the U.S. Department of Defense invested US$ 400 million to acquire a 15% stake in MP Materials, supporting its expansion of domestic rare-earth mining and building a new magnet processing facility projected to begin operations in 2028.

Opportunity - Rising Adoption of Smart Electronic Devices Creates Opportunities

The rising demand for permanent magnets in the electronics sector presents a major opportunity for market growth. The rise in technology development in smartphones, laptops, wearables, and smart appliances, driving the need for compact, efficient, and high performance devices. This demand for enhanced properties encourages manufacturers to use permanent magnetic in the devices. Neodymium-based magnets are widely used in speakers, vibration motors, sensors, and miniaturized actuators, owing to their superior magnetic strength and lightweight properties. According to the article published in 2023 from the EMS Energy Institute, Pennsylvania State University, NdFeB magnet content in consumer electronic products may be small, but the global market shares for this sector accounts for almost 30% of NdFeB demand, due to a large and continually increasing consumer base. The expansion of 5G infrastructure and IoT devices is further amplifying magnet demand in advanced electronics components. This growing reliance on permanent magnets in high-volume electronic applications is creating profitable opportunities for manufacturers.

Category-Wise Analysis

Product Type Insights

NdFeB Magnets Dominate Market with Strong Demand and Strategic Expansion

Neodymium Iron Boron (NdFeB) magnets lead the permanent magnet market, primarily due to their high magnetic strength, energy efficiency, and compact design. These rare earth magnets are widely used in EVs, wind turbines, industrial automation, and consumer electronics.

Global governments are actively encouraging the expansion of NdFeB production to enhance supply chain flexibility and reduce reliance on China. China currently supplies over 85% of global output. Its NdFeB capacity rose from 30,000 tons in 2014 to approximately 260,000 tons in 2024, with further growth expected. In response, the European Union is investing in recycling-based production. For instance, In June 2025, MagREEsource, a French manufacturer of rare earth permanent magnets made from recycled scrap magnetic material, is expanding its factory in Noyarey near Grenoble. The additional 400m² will bring the total facility size to 1,500m² to support its commercial and technological development.

End-use Insights

The Booming EV Industry Drives the Demand for the Permanent magnet market

The automotive industry leads the market with a share of around 34%. The rapid increase in the adoption of EVs drives the demand for permanent magnets as a material for construction. Despite the reduction in the use of permanent magnets in engines and drivelines, EVs benefit from applying permanent magnets in BEV powertrains and battery enclosures. The environmental concerns over the use of gas and diesel as fuel drive consumers to choose EVs as an alternative. According to the International Energy Agency, almost 14 million new electric cars were registered globally in 2023, bringing their total number on the road to 40 million. Car sales have increased at a year-on-year rate of 35%. The governments across the world are promoting EV adoption through initiatives. The U.S. Inflation Reduction Act, the EU’s Green Deal, and China’s New Energy Vehicle policy promote EV production through tax incentives, emissions regulations, and the integration of high-performance magnets in EV drivetrains.

Regional Insights

North America Advances Rare Earth Independence Through Public-Private Collaboration

North America is strengthening its position through strategic investments and expansions. In response to China’s rare earth export restrictions, which caused a 75% drop in global rare earth magnet exports, the U.S. agencies and private industry are taking decisive steps to secure domestic supply chains. The activities, such as the U.S. Department of Defense's investment to acquire a 15% stake in MP Materials, highlight the government’s strategies. Furthermore, the private industries are expanding their reach by collaborating with other players. For instance, In 2025, Energy Fuels formed a strategic alliance with South Korea’s POSCO International to develop a non-China NdPr oxide supply chain, enabling the production of permanent magnets for over 30,000 EVs annually. The efforts from both the government and market players, fueled by geopolitical trade tensions coupled with the rising EV demand, drive the North America permanent magnet market significantly.

Recycling Investments Propel Europe’s Shift Toward Permanent Magnet Supply Independence

Europe permanent magnet market is shifting towards building a sustainable and resilient structure through targeted recycling initiatives, policy frameworks, and industrial investments. The region currently relies on China for about 98% of its permanent magnet supply.

Considering China’s strategic role in rare earth magnets in 2025, the European Union prioritized the development of local capabilities under the Critical Raw Materials Act. This regulation mandates that by 2030, 25% of the EU’s rare earth demand must be met through recycling, and at least 40% of processing must occur within the region. The regional market players are investing significantly in magnet recycling to meet such regulations. For instance, in March 2025, Heraeus Remloy inaugurated a neodymium magnet recycling plant in Bitterfeld, Germany, with a current capacity of 600 tons per year, expected to double to 1,200 tons.

China's Export Restrictions Drive Asia Pacific Toward Supply Diversification

Asia Pacific is dominating the global industry, with a share of more than 75%, fueled by growing EVs, renewable energy, and electronics demand. Following China’s April 2025 export restrictions, which slashed magnet exports by 75%, the end-users in the region are shifting towards non-Chinese suppliers, often paying $10–$30/kg above Chinese rates, to secure essential NdPr materials used in EV motors.

Despite China’s dominance owing to the export restrictions accelerated local investments and supply chain shifts. These developments affirm Asia Pacific’s market resilience and strategic movement toward supply diversification. For instance, in July 2025, Indian auto company Mahindra & Mahindra and parts maker Uno Minda started supply chain diversification to make rare earth magnets locally to cut reliance on China, as the Indian government draws up incentives for the production of the permanent magnets.

Competitive Landscape

The global permanent magnet market is fairly consolidated, undergoing significant transformation as countries and companies seek to diversify supply chains, reduce dependence on China, and improve material sustainability. China currently dominates the global market, accounting for over 85% of Neodymium-Iron-Boron (NdFeB) magnet production. The rising geopolitical tensions and export restrictions have pushed the highly demanding regions, such as North America and Europe to increase their dependency on recycled magnets and invest in strategic expansions to increase the fragmentation in the market. As applications diversify, market players differentiate through technological capabilities, quality, and application-specific expertise.

Recent Industry Developments:

- In June 2025, Dexter Magnetic Technologies, Electron Energy Corporation, and Magnetic Component Engineering, a unified group of leading companies for magnetic solutions, announced a joint effort to achieve DFARS 252.225-7052 compliance for Neodymium-Iron-Boron (NdFeB) and Samarium-Cobalt (SmCo) magnets by mid-2026.

- In April 2025, Cyclic Materials announced the investment of over $20 million in its first commercial facility, located in Mesa, Arizona. The new state-of-the-art facility will be the company’s first global rare earth element recycling operation focused on the separation of permanent magnets from end-of-life products.

Companies Covered in Permanent Magnet Market

- Shin-Etsu Chemical Co., Ltd.

- Proterial Ltd.

- TDK Corporation

- Yantai Dongxing Magnetic Materials Inc.

- Dexter Magnetic Technologies

- Arnold Magnetic Technologies

- Electron Energy Corporation

- Adams Magnetic Products LLC

- Ningbo Yunsheng Co., Ltd.

- Chengdu Galaxy Magnets Co., Ltd.

- Hitachi Metals, Ltd.

Frequently Asked Questions

Yes, the market is set to reach US$ 78.65 Bn by 2032.

The global growing adoption of EVs is propelling the permanent magnet market growth.

India is estimated to witness a CAGR of 9.0% in the forecast period.

The rising adoption of smart and compact electronic devices presents a significant opportunity for the permanent magnet market.

Shin-Etsu Chemical Co., Ltd. is considered the leading player of the permanent magnet market.