- Processed Food

- Pasta and Noodles Market

Pasta and Noodles Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Pasta and Noodles Market by Product Type (Dried, Instant, Frozen & Canned), Ingredient (Wheat, Rice, Quinoa, Corn, Others), Distribution Channel (B2B, B2C), and Regional Analysis 2026 - 2033

Pasta and Noodles Market Share and Trends Analysis

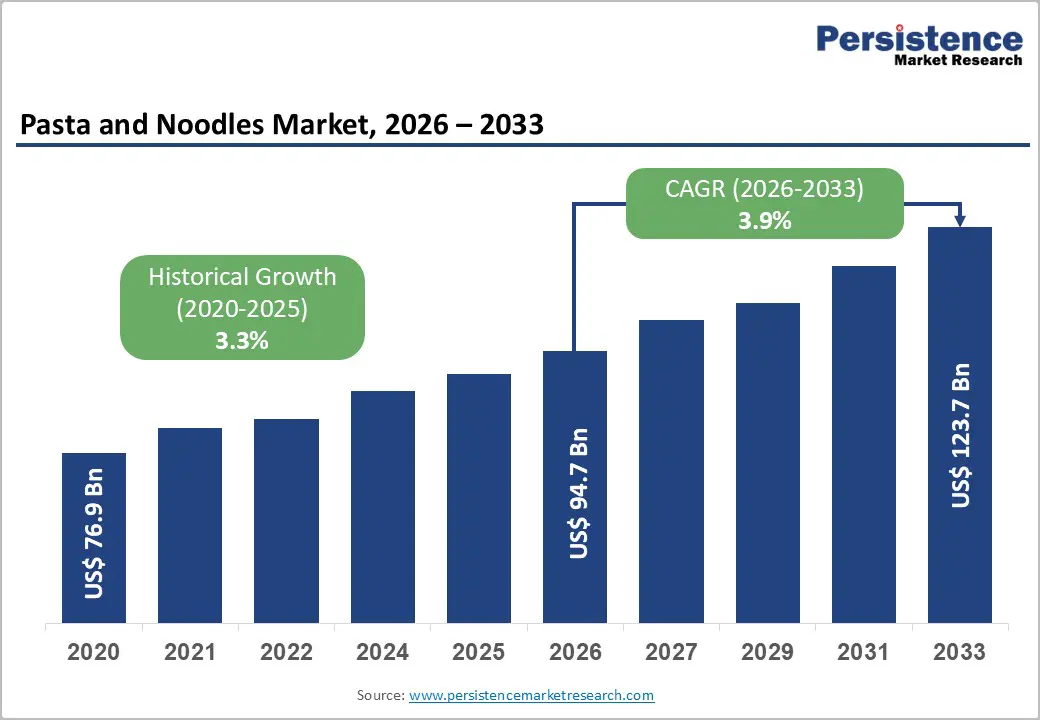

The global pasta and noodles market is projected to reach US$94.7 billion in 2026 and US$123.7 billion by 2033, growing at a CAGR of 3.9% over the forecast period.

The pasta and noodles market is growing steadily, driven by rising demand for convenience foods, urbanization, and increasing consumer preference for ready-to-cook meals. Asia-Pacific dominates the market due to high consumption of noodles and pasta, and it is also the fastest-growing region, supported by changing lifestyles, expanding retail and e-commerce channels, and rising disposable incomes that favor convenient, quick meal solutions.

Key Industry Highlights:

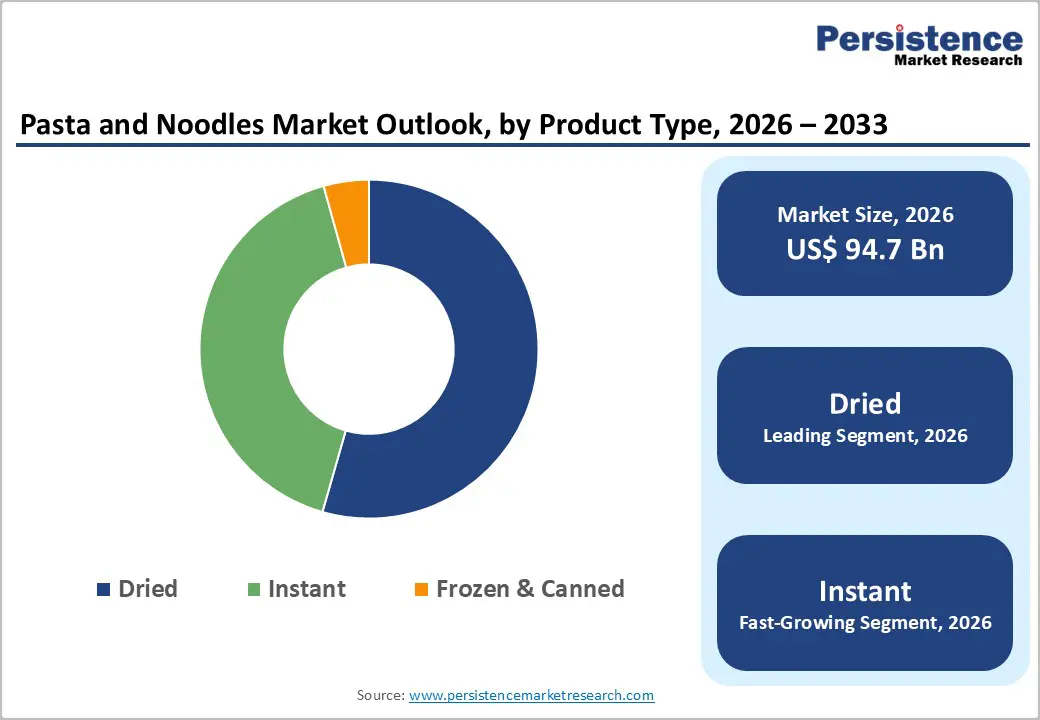

- Dominant Segment: Dried pasta dominates the market with 54.4% share in 2025, driven by long shelf life, wide consumer acceptance, and ease of preparation. Instant noodles are the fastest-growing segment, supported by convenience, on-the-go lifestyles, and continuous product innovation.

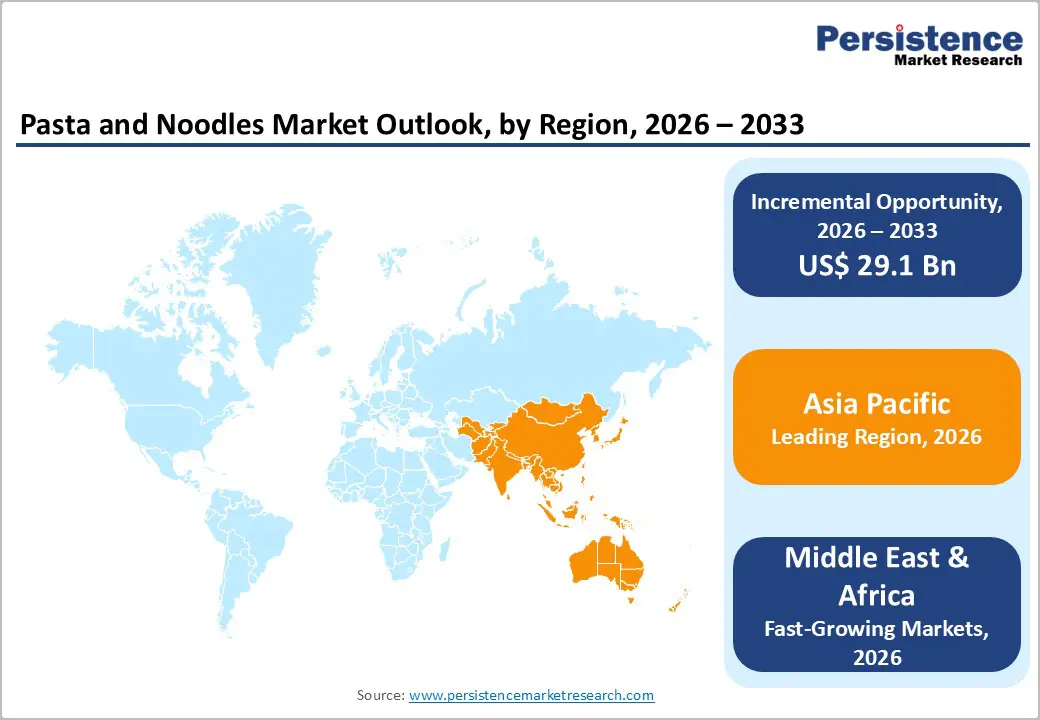

- Dominant Region: Asia Pacific holds the largest share at 50.3% in 2025, driven by high noodle and pasta consumption in China, India, Japan, and Southeast Asia. It is also the fastest-growing region, supported by urbanization, rising disposable incomes, and expanding retail and e-commerce penetration.

- Market Drivers: Growth is fueled by increasing demand for quick and convenient meals, changing lifestyles, rising health and wellness trends (e.g., gluten-free or fortified pasta), and product innovation in flavors and formats.

- Market Opportunity: Key opportunities include alternative ingredients (gluten-free, multigrain, and plant-based pasta), functional products (high-protein, fortified, or fortified noodles), premium convenience products, technological innovation in processing and packaging, and strong growth potential in emerging markets, driven by increasing adoption of Western and convenience foods.

| Key Insights | Details |

|---|---|

|

Pasta and Noodles Market Size (2026E) |

US$ 94.7 Bn |

|

Market Value Forecast (2033F) |

US$ 123.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.3% |

Market Dynamics

Driver: Rising demand for convenience foods

The global shift toward convenience foods is a significant driver of the Pasta & Noodles Market, as consumers increasingly prioritize quick and easy meal solutions amid busy lifestyles and urbanization. Around 65% of global consumers consider ease of preparation an important factor when choosing food products, reflecting heightened demand for ready-to-cook and instant pasta and noodle formats. Government and industry data indicate that changing work patterns and time constraints are reshaping food consumption behaviors, with convenience-focused products replacing traditional multi-ingredient meal preparation. Urban households are also more likely to substitute basic ingredients with prepared, convenient foods, reinforcing sustained demand growth for pasta and noodles.

Quantitative consumption patterns underscore the role of convenience in expanding demand for pasta and noodles. The World Instant Noodles Association reported over 103 billion servings of instant noodles worldwide in 2018, with steady growth in several regions, indicating entrenched consumer reliance on quick meal options. In India, convenience food categories, including instant noodles and pasta, account for an estimated 25% of the total food market, driven by urban working populations with limited meal preparation time. National surveys and food consumption data confirm that processed and ready-to-cook foods increasingly form part of habitual diets, reinforcing the role of convenience in driving global consumption of pasta and noodles.

Restraints: Health concerns over refined carbohydrates

Health concerns about refined carbohydrates constrain the Pasta & Noodles Market, as many pasta and noodle products are made from refined wheat flour, which is low in dietary fiber and nutrients. High intake of refined carbohydrates is associated with metabolic risks, including elevated blood glucose, insulin resistance, and type 2 diabetes, particularly when they constitute a large share of total carbohydrate intake. For example, a national dietary survey in India found that 62.3% of daily calories came from carbohydrates, many from refined cereals such as milled grains and added sugars, with high consumption of refined carbohydrates linked to increased risk of diabetes and obesity.

Epidemiological evidence further supports the adverse health effects of refined carbohydrate consumption, which may diminish consumer perceptions of pasta and noodle products. Studies link diets high in refined carbohydrates to greater risks of cardiovascular disease and type 2 diabetes, as these foods can elevate fasting glucose and insulin resistance measures. For example, refined grains and related foods are observed to contribute significantly to hyperglycaemia in populations with high consumption of white rice and noodles. These health concerns influence dietary guidelines and consumer choices, potentially slowing growth in markets dominated by refined pasta and encouraging demand for whole-grain or alternative options.

Opportunity: Functional and fortified products

Functional and fortified pasta and noodles represent a clear market opportunity by addressing nutritional gaps in diets that rely heavily on refined grains. Governments like India’s Food Safety and Standards Authority of India (FSSAI) have established fortification standards to allow pasta and noodles to be enriched with micronutrients such as iron, folic acid, vitamin B12, and zinc at levels that can cover 15–30% of the daily recommended intake, based on the typical processed food calorie contribution. This regulatory framework enables manufacturers to improve the nutrient profile of staple convenience foods and respond to growing public health emphasis on micronutrient adequacy.

The broader public health rationale for fortification supports consumer acceptance of fortified pasta and noodles. The World Health Organization recognizes food fortification as a cost-effective nutrition intervention that can reduce micronutrient deficiencies and improve health outcomes without adverse effects on the general population. National nutrition surveys also show that fortified foods constitute a significant portion of dietary nutrient intake; for example, U.S. nutrition data indicate that a substantial share of processed staples, including breads and pasta products, contain added micronutrients that contribute meaningfully to daily nutrient intake. These trends underpin consumer demand for nutritionally enhanced convenience foods.

Category-wise Analysis

By Product Type, Dried Dominates the Pasta and Noodles Market

Dried products accounted for 54.4% of the global market in 2025, owing to their practical production, long shelf life, and widespread consumer acceptance. Unlike fresh pasta, dried pasta can be stored for months without refrigeration, making it a reliable pantry staple for households and food service providers, which reduces spoilage and logistical costs. Italy, a leading producer, manufactured approximately 3.6-4.1 million tonnes of pasta in 2023–2024, most of which was dry pasta for domestic use and export, reflecting the strong production infrastructure supporting dried formats. Its versatility across cuisines, from Italian traditional dishes to Asian noodles, combined with ease of transport, affordability, and stability, reinforces dried pasta’s dominant position in global consumption and distribution.

By Ingredient, Wheat is gaining traction due to high global production, affordability, versatility, and ideal dough properties

Wheat dominates the pasta & noodles market because it is the most widely produced and consumed staple grain globally, making it the most accessible and cost-effective raw material for large-scale food manufacturing. Worldwide wheat production is extremely high; nearly 800 million metric tons of wheat are consumed annually as a key source of carbohydrates, including in noodles and pasta products, reflecting its central role in human diets across continents. Wheat flour milling infrastructure is well established in major producing and consuming regions, where a large proportion of flour is used in wheat-based foods such as bread, noodles, and pasta. Because wheat provides desirable dough properties such as elasticity, structure, and texture, it remains the primary ingredient for traditional pasta and many noodles worldwide, thereby underpinning its dominant market share relative to rice, corn, quinoa, and other grains.

Regional Insights

Asia Pacific Pasta and Noodles Market Trends

Asia-Pacific dominates the pasta and noodles market, with a 50.3% share in 2025, owing to the deep integration of pasta and noodles into everyday diets across the region’s large population, resulting in exceptionally high consumption volumes. Historical consumption figures show that in 2018, China alone accounted for about 40.25 billion servings of instant noodles, more than any other country, reflecting entrenched demand in Asia’s largest market and underscoring the cultural importance of noodle dishes across the region. Countries such as Indonesia, Japan, South Korea, Vietnam, and India also report significant noodle consumption, often far exceeding per-capita figures in Western regions. The sheer scale of servings in Asia, many tens of billions annually, demonstrates why the Asia Pacific region leads global demand for these products and underpins its dominant share of the global Pasta & Noodles Market.

Europe Pasta and Noodles Market Trends

Europe is an important region in the pasta & noodles market because it combines strong production capacity, deep cultural integration, and established trade networks that sustain both domestic and international demand. The European Union produced about 6.0–6.2 million tonnes of pasta in 2024 and 2025, with Italy alone accounting for nearly 68–69% of total EU output, underscoring Europe’s industrial strength in pasta manufacturing. A significant portion of this production, approximately 2.9% by tonnage, is exported, with over half traded within the EU, demonstrating the region’s integrated market and intra-regional demand. European consumers also exhibit some of the highest per-capita pasta consumption globally, particularly in Italy where the average is over 23?kg per person annually, reflecting pasta’s entrenched role in diet and tradition. These factors, production scale, export leadership, and cultural demand, make Europe a key and enduring market for pasta and noodles.

North America Pasta and Noodles Market Trends

North America is one of the fastest-growing regions in the pasta & noodles market because its consumers increasingly embrace convenient, quick?to?prepare meals while maintaining strong cultural and dietary relevance for pasta and noodle products. In the United States, for example, the average person consumes about 20 pounds of pasta annually, placing it among the top foods by per-capita consumption, reflecting persistent demand and familiarity. At the same time, Canada shows notable pasta consumption, with per-capita consumption of approximately 7.9 kg annually, indicating broad household integration of pasta into diets. These consumption patterns, together with urban lifestyles that favor quick-cooking, versatile meals and distribution systems that make pasta widely accessible through supermarkets and online channels, support growth. Additionally, North America’s diverse food culture, with Italian, Asian, and fusion dishes, continues to expand opportunities for pasta and noodles across demographics, reinforcing the region’s growing market presence.

Competitive Landscape

Leading companies in the pasta and noodles market focus on high-quality, nutritious, and innovative products. Investments target product variety, ingredient quality, and fortified or functional options. R&D emphasizes taste, texture, and health benefits, while collaborations with culinary experts and nutritionists enhance product appeal, sustainability, and consumer adoption, driving market growth, innovation, and global consumption.

Key Industry Developments:

- In November 2025, Barilla® declared pasta as the official food of the cozy season, marking the return of its Snowfall Pasta and highlighting lasagne. The announcement emphasized Barilla’s seasonal offerings designed to celebrate comfort meals, with the Snowfall Pasta returning to shelves for consumers seeking festive and warm dining experiences.

- In January 2025, NatureSweet partnered with Barilla on a flavorful meal campaign featuring fresh, high-quality tomatoes paired with Barilla pasta products. The collaboration aimed to inspire consumers to create easy, nutritious, and tasty meals at home, highlighting the synergy between NatureSweet’s produce and Barilla’s pasta.

Companies Covered in Pasta and Noodles Market

- Barilla Group S.p.A.

- Delverde Industrie Alimentari S.p.A.

- Nestlé SA

- ITC

- The Kraft Heinz Company

- Unilever PLC

- Toyo Suisan Kaisha, Ltd.

- General Mills, Inc.

- Nissin Foods Holdings Co., Ltd.

- Grupo La Moderna

- Campbell Soup Company

- Bionaturae LLC

- Others

Frequently Asked Questions

The global pasta and noodles market is projected to be valued at US$ 94.7 Bn in 2026.

Rising demand for convenience, urbanization, changing lifestyles, product innovation, and increasing global pasta consumption drive growth.

The global pasta and noodles market is poised to witness a CAGR of 3.9% between 2026 and 2033.

Alternative ingredients, fortified products, functional noodles, premium convenience formats, and growth in emerging markets present opportunities.

Barilla Group S.p.A., Delverde Industrie Alimentari S.p.A., Nestlé SA, ITC, The Kraft Heinz Company, Unilever PLC.