- Medical Devices

- Next Generation IV Infusion Pumps Market

Next Generation IV Infusion Pumps Market Size, Share, and Growth Forecast 2026 – 2033

Next Generation IV Infusion Pumps Market by Product Type (Volumetric Infusion Pumps, Syringe Infusion Pumps, Ambulatory Infusion Pumps, Insulin Infusion Pumps, Enteral Infusion Pumps, Others), Application (Oncology, Diabetes Management, Pain Management, Pediatrics & Neonatal Care, Others), End-user (Hospitals, Ambulatory Surgical Centers (ASCs), Home Care Settings, Specialty Clinics), and Regional Analysis, 2026–2033

Next Generation IV Infusion Pumps Market Share and Trends Analysis

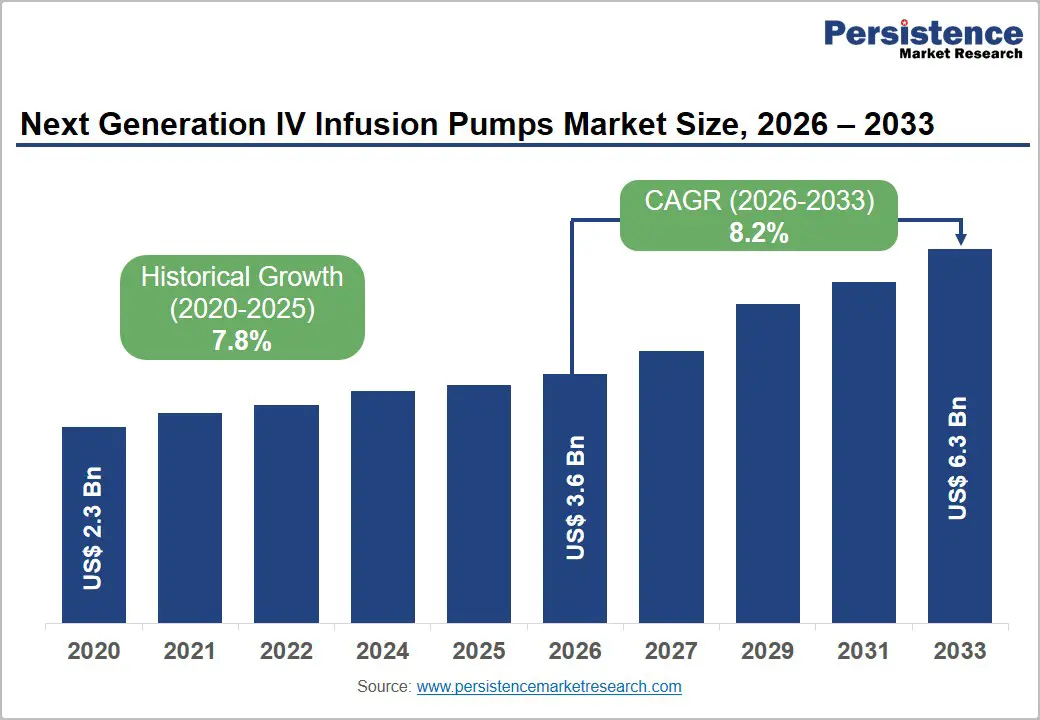

The global next generation IV infusion pumps market size is expected to be valued at US$ 3.6 billion in 2026 and projected to reach US$ 6.3 billion, growing at a CAGR of 8.2% between 2026 and 2033.

Growing demand for precise and safe drug delivery systems in critical care and chronic disease management. These advanced pumps integrate smart technologies such as dose error reduction systems, wireless connectivity, and interoperability with electronic health records, enhancing medication safety and workflow efficiency. Increasing ICU admissions, growing cancer and diabetes prevalence, and expansion of hospital digital infrastructure are further supporting adoption.

Key Industry Highlights:

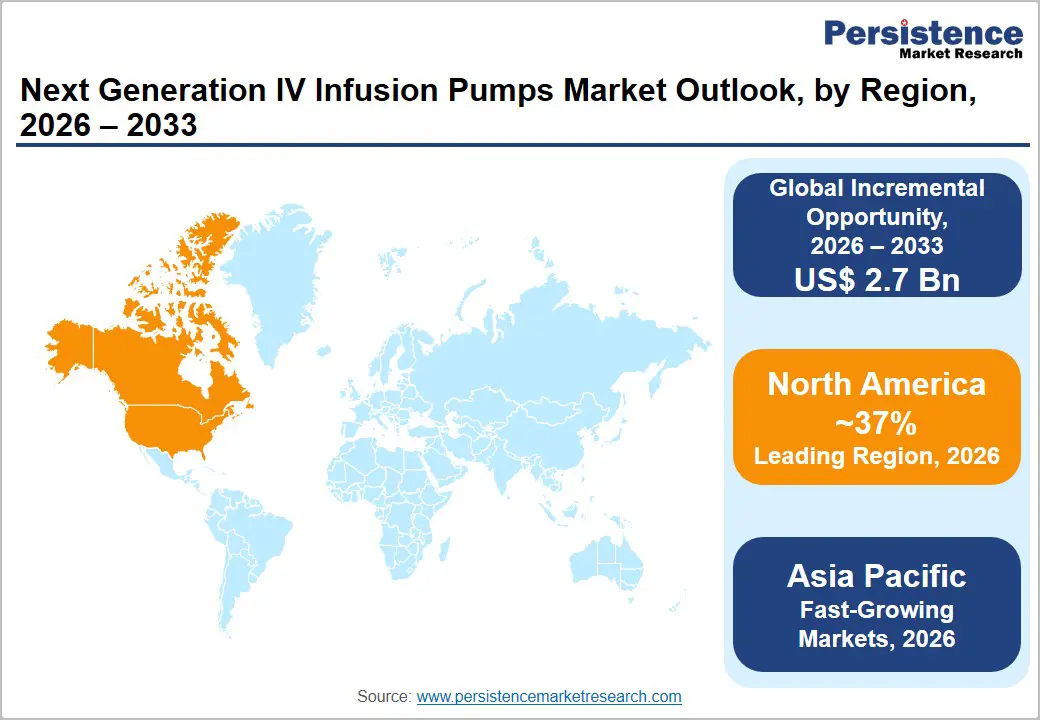

- Leading Region: North America leads the global Next Generation IV Infusion Pumps market with approximately 37% revenue share in 2026, driven by FDA smart pump safety mandates, Joint Commission mandatory DERS adoption standards across 6,000+ U.S. hospitals, and CMS Hospital at Home waiver programs expanding ambulatory pump home deployment.

- Fast-growing Market: Asia Pacific is the fast-growing regional market, propelled by China's NMPA-accelerated approval activity, India's Ayushman Bharat program expanding inpatient procedure access, rapidly expanding corporate hospital surgical and oncology capacity, and Mindray's cost-competitive smart pump platforms gaining public hospital market share.

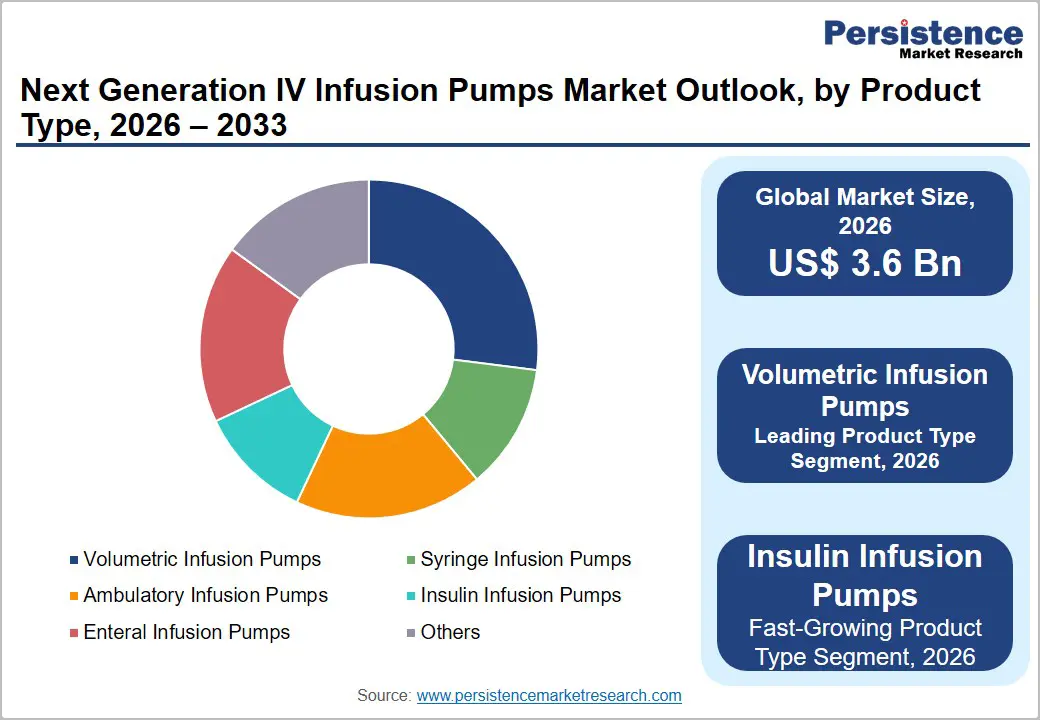

- Leading Product Type: Volumetric infusion pumps dominate the product type category with approximately 27% share in 2026, anchored by universal hospital deployment across ICU, surgical, emergency, and general inpatient settings with leading platforms from Baxter, BD (Alaris), and B. Braun integrating advanced DERS, wireless connectivity, and EHR interoperability.

- Dominant Product Type: Insulin infusion pumps are the fast-growing product segment, driven by FDA-approved closed-loop AID systems (Medtronic MiniMed 780G, Omnipod 5, Tandem Control-IQ) demonstrating superior glycemic outcomes in NEJM-published trials, and the IDF's estimated 8.4 million global Type 1 diabetes patients driving sustained AID adoption.

Market Dynamics Analysis

Drivers - FDA Safety Mandates and Adverse Event Data Driving Rapid Replacement of Legacy Infusion Pump Systems

Regulatory pressure from the U.S. FDA is one of the most powerful structural catalysts for next-generation infusion pump adoption in the world's largest medical device market. The FDA's infusion pump adverse event database has consistently documented infusion pump-related errors as among the most prevalent and clinically consequential medical device malfunctions, prompting the agency to issue guidance on infusion pump interoperability and drug library management best practices.

The Institute for Safe Medication Practices (ISMP) estimates that infusion-related errors account for a substantial proportion of all serious hospital medication errors. The Joint Commission's National Patient Safety Goals requiring smart pump technology adoption across accredited U.S. hospitals is creating a compliance-driven upgrade cycle, with hospitals actively replacing non-networked, library-deficient legacy pumps with next-generation smart platforms from Baxter International, BD (Alaris), and ICU Medical that offer mandatory DERS compliance and wireless EHR integration.

Rise in Burden of Chronic Diseases and Home Infusion Therapy Adoption Expanding Addressable Market

The global rise in chronic conditions for ongoing intravenous medication administration, including cancer, diabetes, chronic pain, heart failure, and infectious diseases need long-term antibiotic therapy. The International Diabetes Federation (IDF) estimated 537 million diabetic adults globally in 2021, with insulin pump therapy representing the gold standard for Type 1 diabetes management.

The American Cancer Society reports over 2 million new U.S. cancer diagnoses annually, the majority of whom receive intravenous chemotherapy through infusion pump systems. Simultaneously, the National Home Infusion Association (NHIA) documents that the U.S. home infusion therapy sector has grown at over 8% annually, driven by hospital reimbursement pressures shifting post-acute care to lower-cost home settings that require sophisticated ambulatory infusion pump platforms with remote monitoring capabilities.

Restraints - High Capital Cost and Lengthy Procurement Cycles Limiting Rapid Market Penetration

Next-generation infusion pump systems, particularly enterprise-wide smart pump platforms with EHR integration, Dose Error Reduction Software (DERS), and wireless clinical surveillance capabilities, represent significant capital investments for hospital systems, with full enterprise deployments across large health networks ranging from USD 5 million to over USD 50 million.

Budget constraints in public hospital systems across Europe, Latin America, and developing Asia Pacific markets, combined with lengthy government medical procurement tender processes that can extend 12–24 months, substantially delay market penetration and create extended revenue recognition cycles for manufacturers that constrain growth velocity in price-sensitive institutional markets.

Cybersecurity Vulnerabilities and IT Integration Complexity Creating Adoption Barriers

The connectivity features that define next-generation infusion pumps including Wi-Fi, Bluetooth, and EHR bidirectional data exchange, simultaneously introduce cybersecurity vulnerabilities that are emerging as significant procurement barriers. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) has issued multiple advisories identifying critical vulnerabilities in major infusion pump brands, and the FDA's 2023 Medical Device Cybersecurity guidance imposes new pre-market cybersecurity requirements that increase development costs and extend approval timelines.

Healthcare IT integration complexity, including HL7 FHIR middleware requirements for EHR connectivity, creates lengthy implementation projects that delay realized clinical utilization of advanced pump features and increase total cost of ownership calculations for risk-averse hospital procurement committees.

Opportunities - Insulin Infusion Pumps: Fastest-Growing Product Segment Driven by Closed-Loop Artificial Pancreas Systems

Insulin Infusion Pumps represent the fastest-growing product segment in the next-generation IV infusion pumps market, propelled by the accelerating clinical adoption of closed-loop automated insulin delivery (AID) systems commonly known as artificial pancreas technology that integrate continuous glucose monitors (CGMs) with insulin pumps through proprietary control algorithms.

The FDA has approved multiple hybrid closed-loop AID systems, including Medtronic's MiniMed 780G, Insulet's Omnipod 5, and Tandem Diabetes Care's Control-IQ, each demonstrating superior glycemic control outcomes versus conventional insulin pump therapy in clinical trials published in the New England Journal of Medicine and Diabetes Care. The IDF's estimate that Type 1 diabetes affects approximately 8.4 million people globally, combined with growing Type 2 diabetes insulin intensification trends and expanding insurance reimbursement for AID systems, positions insulin infusion pumps as the highest-growth product category through the 2033 forecast horizon.

Category-wise Analysis

Product Type Insights

Volumetric infusion pumps lead the next-generation IV infusion pumps market by product type, commanding approximately 27% of global revenues in 2026. Volumetric pumps, which deliver precise, programmable fluid volumes at controlled rates across general inpatient, intensive care, surgical, and emergency settings, constitute the foundational infusion device category deployed throughout hospital infrastructure.

Their versatility in administering large-volume intravenous fluids, parenteral nutrition, blood products, and a broad range of intravenous medications makes them the highest-utilization pump category across inpatient care settings globally. Leading platforms including Baxter's SIGMA Spectrum, BD's Alaris PK, and B. Braun's Infusomat Space incorporate next-generation features including drug libraries, dose error reduction software (DERS), wireless network connectivity, and EHR bidirectional integration that distinguish them from legacy volumetric systems and drive hospital upgrade investment in the segment.

Application Insights

Oncology represents the leading application segment in the next-generation IV infusion pumps market, accounting for approximately 32% of global revenues in 2026. Intravenous chemotherapy administration is among the highest-risk, highest-precision infusion therapy contexts where accurate drug delivery rates are critical to both efficacy and patient safety, making the advanced programming controls, drug library safeguards, and interoperability features of next-generation smart pump platforms particularly valued.

The American Cancer Society reports over 2 million new U.S. cancer diagnoses annually, and the National Comprehensive Cancer Network (NCCN) clinical guidelines for the majority of cancer types include intravenous chemotherapy regimens requiring precisely programmed multi-drug infusion pump protocols. The global shift toward outpatient chemotherapy delivery in ambulatory infusion centers is additionally driving adoption of ambulatory pump platforms specifically optimized for oncology drug administration.

End-user Insights

Hospitals constitute the leading end-user segment in the next-generation IV infusion pumps market, representing approximately 58% of global revenues in 2025. Hospitals deploy the broadest and most diverse infusion pump installed bases spanning intensive care units, oncology day centers, surgical suites, neonatal intensive care, and general medical-surgical floors, generating the highest aggregate device procurement volumes and the most complex enterprise-scale interoperability requirements.

The Joint Commission's smart pump adoption standards, FDA medical device adverse event reporting mandates, and hospital quality metric programs linking medication error rates to reimbursement incentives collectively create compliance-driven capital equipment upgrade cycles in the hospital channel. Enterprise-wide smart pump deployment contracts encompassing thousands of units per health system generate the highest-value individual procurement events in the infusion pump market and represent the most competitively contested commercial battleground for major pump manufacturers.

Regional Insights

North America Next Generation IV Infusion Pumps Market Trends and Insights

North America leads the global Next Generation IV infusion pumps market with approximately 37% revenue share in 2026, driven by the United States' combination of stringent FDA smart pump safety guidance, Joint Commission mandatory smart pump adoption standards, and a large established hospital infrastructure actively replacing legacy infusion systems. Growing home infusion therapy programs under CMS Hospital at Home waiver expansions and strong commercial insurance reimbursement for home infusion are additional demand catalysts across the region.

U.S. Next Generation IV Infusion Pumps Market Size

The United States accounts for approximately 88% of North American revenues, anchored by over 6,000 hospitals undertaking enterprise-wide smart pump refresh programs, FDA cybersecurity compliance mandates driving next-generation platform adoption, and the world's largest home infusion therapy sector serving over 3 million patients annually per NHIA data, generating sustained ambulatory pump procurement demand.

Europe Next Generation IV Infusion Pumps Market Trends and Insights

Europe is the second-largest next-generation infusion pumps market, supported by the EU Medical Device Regulation (MDR 2017/745) raising software and cybersecurity requirements for networked infusion devices, universal healthcare systems providing consistent capital equipment budgets, and growing adoption of smart pump technologies aligned with European Medicines Agency (EMA) medication safety recommendations. Germany, France, the U.K., and Italy lead European market revenues, supported by established hospital automation infrastructure.

Germany Next Generation IV Infusion Pumps Market Size

Germany holds approximately 23% of European revenues, driven by Germany's world-leading hospital infrastructure density, comprehensive GKV statutory health insurance covering inpatient infusion therapies, and proactive BfArM (Federal Institute for Drugs and Medical Devices) medical device quality oversight that incentivizes hospital procurement of safety-certified next-generation smart pump platforms from B. Braun Melsungen and international manufacturers.

U.K. Next Generation IV Infusion Pumps Market Size

The United Kingdom accounts for approximately 18% of European revenues, supported by NHS England's national patient safety infrastructure, MHRA medical device regulation alignment with EU MDR standards, and centralized NHS procurement frameworks that periodically deploy next-generation smart pump platforms across hospital trusts through framework agreements enabling consistent technology standardization and volume pricing.

France Next Generation IV Infusion Pumps Market Size

France represents approximately 15% of European infusion pump revenues, driven by HAS (Haute Autorité de Santé) patient safety recommendations supporting smart pump adoption in French hospitals, Assurance Maladie inpatient procedure reimbursement sustaining hospital capital equipment budgets, and growing home infusion therapy infrastructure under HAD (Hospitalisation à Domicile) programs expanding ambulatory pump demand.

Asia Pacific Next Generation IV Infusion Pumps Market Trends and Insights

Asia Pacific is the fast-growing regional market for next-generation IV infusion pumps through 2033, propelled by rapidly expanding hospital infrastructure, rising cancer and diabetes incidence rates, and growing regulatory sophistication in China, Japan, India, and ASEAN markets. China's National Medical Products Administration (NMPA) approval activity for advanced infusion pump platforms is accelerating, and domestic manufacturers including Mindray are competing with international brands on sophisticated feature sets at cost-competitive price points for public hospital procurement tenders.

India Next Generation IV Infusion Pumps Market Size

India accounts for approximately 16% of Asia Pacific revenues and is the region's fastest-growing national market, driven by rapidly expanding corporate hospital surgical and oncology capacity, CDSCO-regulated medical device quality improvements, and the government Ayushman Bharat insurance scheme expanding access to inpatient procedures that require infusion pump therapy across previously underserved patient populations.

Competitive Landscape

The global next generation IV infusion pumps market is characterized by a highly consolidated competitive landscape, dominated by a few global medical technology leaders with strong product portfolios and extensive distribution networks. Leading companies focus on smart infusion systems integrated with dose-error reduction software, connectivity with hospital IT systems, and advanced safety features to minimize medication errors. Strategic priorities include product innovation, regulatory approvals, and digital integration with electronic medical records. Mid-sized players compete through cost-effective ambulatory and specialty pump solutions, while emerging manufacturers are expanding in Asia Pacific with affordable offerings.

Key Developments:

- In October 2025, Becton Dickinson (BD) launched new AI-enabled healthcare solutions designed to strengthen connectivity across diverse healthcare settings. The initiative was aimed at improving data integration, interoperability, and real-time information sharing between clinicians, laboratories, and care teams.

- In April 2025, ICU Medical Inc. received U.S. FDA 510(k) clearance for its new Plum Solo™ single-channel infusion pump and updated Plum Duo™ dual-channel pump along with upgraded LifeShield™ infusion safety software, marking the completion of the initial rollout of its IV Performance Platform.

Global Next Generation IV Infusion Pumps Market – Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.3 Billion |

|

Current Market Value (2026) |

US$ 3.6 Billion |

|

Projected Market Value (2033) |

US$ 6.3 Billion |

|

CAGR (2026–2033) |

8.2% |

|

Leading Region |

North America, 37% market share (2026) |

|

Dominant Product Type (Category 1) |

Volumetric Infusion Pumps, ~27% market share (2026) |

|

Top-Ranking Application (Category 2) |

Oncology, ~32% market share (2026) |

|

Incremental Opportunity (2026–2033) |

US$ 2.7 Billion |

Companies Covered in Next Generation IV Infusion Pumps Market

- Baxter International

- B. Braun Melsungen AG

- Becton Dickinson (BD)

- ICU Medical

- Fresenius Kabi

- Smiths Medical

- Medtronic

- Terumo Corporation

- Mindray

- Moog Inc

- Nipro Corporation

- Zyno Medical

- Micrel Medical Devices

Frequently Asked Questions

The global Next Generation IV Infusion Pumps market is estimated to be valued at US$ 3.6 billion in 2026.

A major driver is the increasing incidence of chronic diseases and critical care admissions, such as cancer, diabetes, and cardiovascular disorders, which require precise and continuous intravenous drug delivery.

North America leads with approximately 37% of global revenues in 2026, with the United States as the dominant national market.

Hospitals are increasingly investing in closed-loop medication management systems, where next-generation infusion pumps are directly connected to electronic health records (EHRs), pharmacy systems, and clinical decision-support tools.

The leading companies in the global Next Generation IV Infusion Pumps market include Baxter International, B. Braun Melsungen AG, Becton Dickinson (BD), and ICU Medical.