- Pharmaceuticals

- Next Generation Drug Conjugates Market

Next Generation Drug Conjugates Market Size, Share, and Growth Forecast, 2026 – 2033

Next Generation Drug Conjugates Market by Conjugate Type (RNAi Conjugates, Antisense Oligonucleotide Conjugate, Others), Targeting Ligand (Peptides, Others), Payload Type (Radionuclides, Si-RNA, Cytotoxic Drugs), and Regional Analysis 2026 – 2033

Next Generation Drug Conjugates Market Size and Trends Analysis

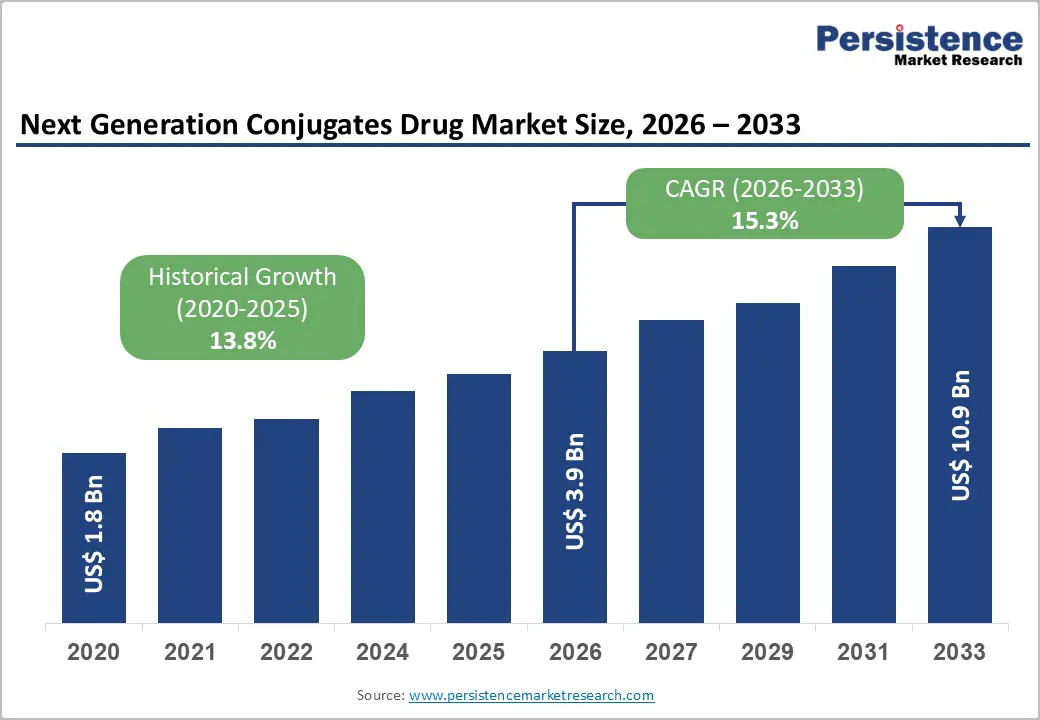

The global next generation drug conjugates market size is likely to be valued at US$3.9 billion in 2026 and is expected to reach US$10.9 billion by 2033, growing at a CAGR of 15.3% during the forecast period from 2026 to 2033, driven by the transition from traditional Antibody-Drug Conjugates (ADCs) to more versatile platforms, including RNAi conjugates and Peptide-Drug Conjugates (PDCs).

Growth is fueled by rising demand for targeted treatments in oncology and rare disorders, with approved products such as Lutathera and Givlaari demonstrating clinical success. Regulatory approvals, such as for GalNAc conjugates such as Givlaari® and Pluvicto®, have accelerated adoption, while partnerships with big pharma enhance commercialization.

Key Industry Highlights:

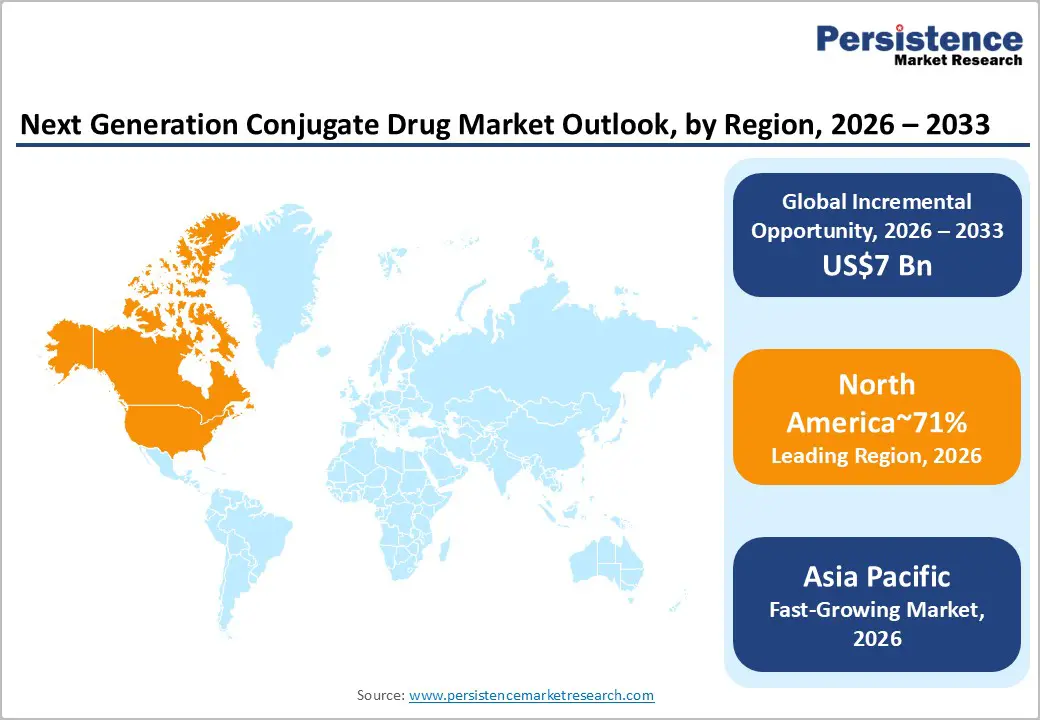

- Leading Region: North America is expected to lead with around 71% share, supported by R&D concentration and early technology adoption.

- Fastest Growing Region: Asia Pacific, to be the fastest growing, led by China and South Korea, expanding clinical and manufacturing capacity.

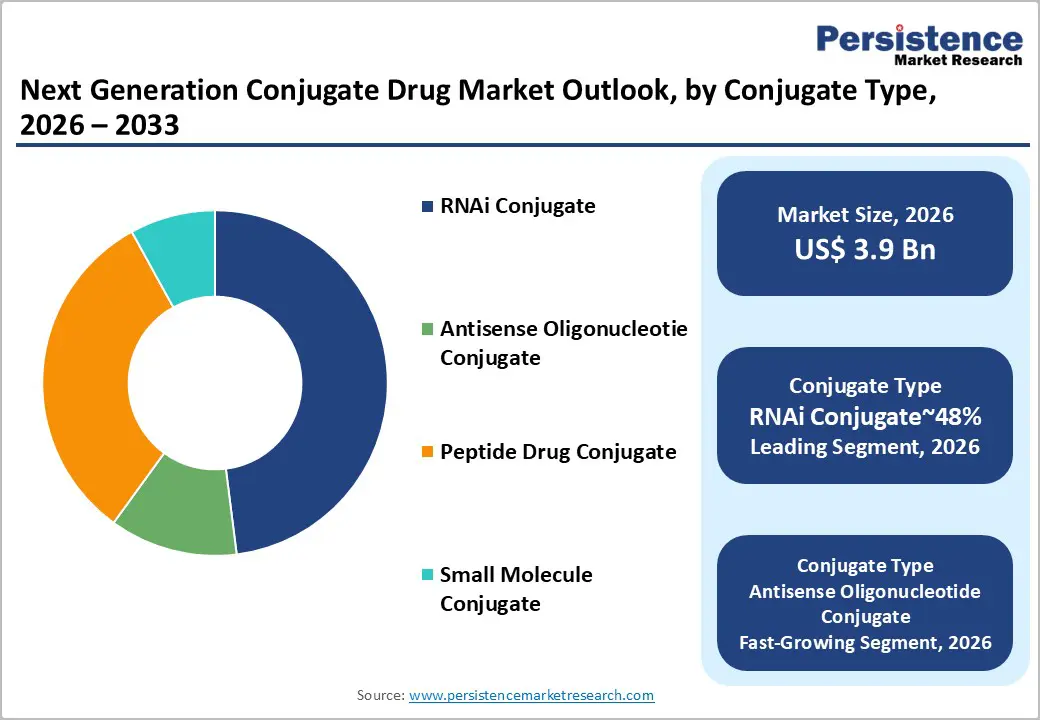

- Leading Conjugate Type: RNAi Conjugates are expected to lead with around 48% share, supported by strong clinical pipelines and validated delivery platforms.

- Leading Targeting Ligand: Peptides, to lead with approximately 58% share, reflecting broad applicability and mature targeting chemistries.

| Key Insights | Details |

|---|---|

| Next Generation Drug Conjugates Drug Market Size (2026E) | US$3.9 Bn |

| Market Value Forecast (2033F) | US$10.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Advancements in Targeted Delivery Technologies

Advances in next-generation drug conjugates are reshaping targeted therapeutics by extending precision delivery beyond antibody-centric platforms toward ligand-guided modalities such as peptides and GalNAc constructs. These architectures improve tissue penetration, intracellular uptake, and payload stability, addressing pharmacokinetic and off-target toxicity constraints that limit conventional antibody drug conjugates in certain indications. The expanding collaboration ecosystem between oligonucleotide developers and large pharmaceutical sponsors is accelerating translational pathways from platform science to clinic-ready assets, embedding targeted delivery technologies deeper into discovery pipelines and late-stage development strategies. Regulatory validation of ligand-directed conjugates in oncology and rare disease therapy reinforces platform credibility and lowers adoption friction across therapeutic areas.

At the value-chain level, maturation of targeted delivery platforms reallocates investment toward conjugation chemistries, linker technologies, and scalable bioconjugation manufacturing, increasing the strategic value of specialized CDMO capabilities. Approved therapies such as Lutathera and Amvuttra anchor clinical confidence in non-antibody targeting modalities, while heightening regulatory expectations around reproducibility, stability, and long-term safety monitoring. Payer scrutiny of high-cost specialty therapeutics further elevates the importance of delivery efficiency in demonstrating differentiated clinical value. Collectively, these dynamics integrate targeted delivery technologies into core biopharmaceutical development and manufacturing infrastructures.

Rising Prevalence of Chronic Diseases and Demand for Targeted Therapy

The expanding burden of chronic and complex diseases is structurally shifting pharmaceutical demand toward precision therapeutics that can modulate disease pathways with higher selectivity than conventional systemic treatments. Limitations of non-specific cytotoxic regimens, particularly their adverse safety profiles and narrow therapeutic windows, elevate the clinical and regulatory premium placed on targeted delivery modalities. Radionuclide drug conjugates and RNA interference-based therapies address these constraints by enabling localized payload delivery and pathway-specific gene silencing, aligning therapeutic design with the growing emphasis on biomarker-driven treatment paradigms. This transition embeds targeted platforms within oncology and immunology development pipelines as core modalities rather than adjunct options.

At the market and value-chain level, rising utilization of targeted therapies increases dependence on specialized manufacturing, radiopharmaceutical handling, and controlled distribution infrastructures capable of supporting complex biologic administration. Regulatory frameworks governing advanced therapies impose stringent requirements on conjugation reproducibility, cold-chain integrity, and clinical safety monitoring, raising compliance costs and qualification thresholds for suppliers. Health system investment in advanced infusion and nuclear medicine capabilities further concentrates adoption within regions with mature care delivery ecosystems, reinforcing geographic asymmetries in access while structurally expanding demand for precision-enabled therapeutic platforms across regulated healthcare markets.

Barrier Analysis – Bioconjugation and Manufacturing Complexity

Bioconjugation introduces substantial manufacturing complexity across linker chemistry, payload stability, and process control, creating persistent barriers to scalable production of advanced conjugates. Reproducibility constraints across batch manufacturing increase production risk and elevate unit costs relative to conventional small-molecule platforms, complicating commercial scale-up for emerging modalities such as peptide-phosphorodiamidate morpholino oligomers. The requirement for tightly controlled conjugation kinetics, sterile handling, and high-purity intermediates further constrains manufacturing throughput and operational flexibility across clinical and commercial pipelines.

Supply chain fragility remains a material restraint, as illustrated by prior availability disruptions affecting radioligand therapies such as Pluvicto, which exposed downstream vulnerabilities in isotope sourcing, fill-finish capacity, and qualified manufacturing slots. These constraints heighten the risk of delayed market access and deferred revenue realization for novel conjugates, particularly in oncology-focused pipelines. The dependence on specialized bioconjugation expertise and bespoke manufacturing infrastructure structurally disadvantages mid-sized developers, slowing platform diversification and extending timelines for broader clinical adoption of next-generation conjugate therapies.

Stringent Regulatory Requirements and Long Lead Times

Regulatory agencies such as the FDA and EMA classify next-generation conjugates as combination products, which materially elevates the evidentiary burden across development and approval pathways. Sponsors must independently characterize and validate the ligand, linker, and payload, in addition to the final conjugated entity, expanding the scope of CMC documentation, nonclinical toxicology, and clinical pharmacology requirements. The need to delineate the pharmacokinetics and pharmacodynamics of multiple interdependent components complicates trial design, increases protocol amendments, and prolongs regulatory interactions across early and mid-stage development.

Clinical attrition remains structurally elevated due to unforeseen off-target toxicities and complex bio-distribution profiles inherent to conjugated platforms. This risk profile extends development timelines, inflates capital intensity, and compresses effective patent life at commercialization. As a result, sponsors face prolonged time-to-market, higher program-level sunk costs, and constrained portfolio throughput, disproportionately affecting smaller developers with limited regulatory infrastructure and risk-bearing capacity.

Opportunity Analysis – Expansion to Non-Oncology Indications

Next-generation drug conjugates are extending beyond oncology into autoimmune and genetic disease pathways, reflecting the adaptability of ligand-directed delivery platforms across diverse biological targets. GalNAc-mediated RNA interference modalities enable hepatocyte-specific uptake through ASGPR binding, aligning therapeutic delivery with liver-centric disease mechanisms and improving on-target exposure relative to systemic approaches. This platform's versatility addresses long-standing delivery constraints in non-oncology indications where conventional small molecules and biologics face limited tissue selectivity and suboptimal intracellular access. As precision delivery becomes embedded within immunology and rare disease pipelines, NGDC architectures transition from niche oncology tools into cross-therapeutic enabling technologies.

At the value-chain level, expansion into non-oncology indications reallocates development and manufacturing capacity toward scalable conjugation chemistries, oligonucleotide production, and validated delivery ligands optimized for organ-specific targeting. Regulatory pathways for genetic and autoimmune therapies impose heightened expectations around long-term safety, off-target effects, and durability of response, increasing the compliance burden for platform developers and manufacturing partners. Combination strategies with established immunomodulatory agents introduce formulation and stability complexities that elevate integration requirements across CDMO, cold-chain logistics, and clinical supply infrastructure, structurally broadening the commercial footprint of NGDC platforms beyond oncology-centric markets.

Personalized Medicine Integration and AI-Enabled Payload Selection

The convergence of personalized medicine frameworks with next-generation conjugate platforms is reconfiguring therapeutic design toward biomarker-aligned targeting and patient-stratified delivery architectures. As molecular diagnostics refine patient segmentation, conjugate payloads and targeting ligands can be aligned with disease-specific receptor expression and intracellular processing pathways, improving therapeutic index relative to one-size-fits-all regimens. Artificial intelligence applied to payload selection and linker optimization enhances screening efficiency across large chemical and biologic libraries, accelerating identification of candidates with favorable stability, potency, and intracellular release profiles. This integration embeds data-driven design within discovery workflows, shifting conjugate development from empiric iteration toward model-informed optimization.

At the value-chain level, AI-enabled payload engineering increases reliance on high-quality training datasets, standardized bioassays, and interoperable data infrastructures across discovery, preclinical validation, and manufacturing translation. Regulatory expectations around explainability, model validation, and reproducibility introduce compliance layers that reshape development governance and quality systems. Personalized deployment models further intensify coordination between diagnostics, therapeutic manufacturing, and clinical delivery, increasing complexity across supply chains and raising barriers to entry for platforms lacking integrated data and bioconjugation capabilities. These dynamics structurally elevate the strategic importance of computationally informed conjugate design within precision therapeutics ecosystems.

Category–wise Analysis

Conjugate Type Insights

RNAi conjugates are expected to dominate the oligonucleotide conjugates market, capturing around 48% of the market share in 2026. This is driven by the clinical maturity of GalNAc ligand conjugation and the established role of siRNA-mediated gene silencing in hepatocyte-targeted therapies. RNAi conjugates offer high target specificity, durable knockdown, and favorable safety profiles compared to alternative delivery methods. Developers are focused on standardized liver-directed platforms to expedite clinical translation, while innovations in GalNAc architectures, endosomal escape chemistries, and solid-phase manufacturing continue to enhance pipeline efficiency. Companies such as Alnylam, Arrowhead, and Ionis are expanding their RNAi portfolios, locking in discovery-to-commercial workflows and long-term lifecycle management, sustaining RNAi’s dominance in structured therapeutic models.

Antisense oligonucleotide (ASO) conjugates are projected to be the fastest-growing segment, driven by unmet needs in rare and genetically heterogeneous disorders. Advances in conjugation chemistries, tissue-selective ligands, and sequence engineering are expanding ASO applications beyond liver-centric indications to areas such as neuromuscular and CNS-adjacent disorders. Adoption is boosted by improved delivery vectors, stability profiles, and translational toolchains that reduce development friction. Companies such as Ionis, Sarepta, and Roche are scaling ASO conjugate platforms to capture early demand and build personalized therapy pipelines.

Targeting Ligand Insights

Peptides are expected to dominate the targeting ligand segment of the conjugated therapeutics market, capturing approximately 58% of the share in 2026. This is driven by their pivotal role in receptor-mediated delivery in oncology workflows and radiopharmaceutical development. Peptides offer favorable pharmacokinetics, deep tissue penetration, and cost-effective solid-phase synthesis, making them ideal for scalable manufacturing and high-throughput clinical programs. Innovations in bicyclic peptide architectures, affinity-optimized scaffolds, and linker technologies that are compatible with radionuclides and cytotoxics continue to boost their adoption. Companies, including Novartis, Bicycle Therapeutics, and Telix, are expanding their peptide-based portfolios, positioning themselves within radioligand therapy ecosystems.

Amino Sugars (GalNAc) are anticipated to be the fastest-growing targeting ligands, driven by their potential in hepatocyte-specific delivery for RNAi and antisense therapies. Innovations in ligand engineering, multivalent strategies, and conjugation chemistry are accelerating their uptake, particularly for cardiometabolic and rare diseases. Alnylam, Ionis, and Arrowhead are scaling their GalNAc-conjugated pipelines to capitalize on the growing demand. As clinical validation, regulatory acceptance, and payer confidence increase, GalNAc ligands are expected to outpace overall market growth during the forecast period.

Regional Insights

North America Next Generation Drug Conjugates Market Trends

North America is expected to remain the dominant region with a market share of approximately 71% in 2026, underpinned by the depth of its biopharmaceutical innovation ecosystem and the concentration of late-stage clinical development and commercialization capabilities in the U.S. The region’s leadership is structurally linked to the presence of integrated pharma and biotech leaders such as Novartis, Pfizer, Merck, Amgen, and Alnylam, alongside a dense network of translational research centers and oncology-focused clinical trial infrastructure. Commercial momentum is reinforced by the rapid uptake of radioligand therapies and targeted conjugate platforms in U.S. oncology centers, with branded products such as Pluvicto and Lutathera establishing clinical and commercial validation for peptide- and small-molecule–based targeting approaches. Canada complements this leadership through an increasingly active clinical development environment and regulatory pathways that facilitate parallel North American trial execution and earlier market access for high-unmet-need indications.

Market expansion in North America is being shaped by sustained capital deployment into precision oncology, rare disease platforms, and multi-omic drug discovery, which collectively favor conjugate modalities that can improve therapeutic index and patient stratification. Competitive dynamics remain fragmented, with incumbent oncology leaders consolidating exposure to conjugate pipelines through targeted partnerships and bolt-on acquisitions, while platform specialists such as Bicycle Therapeutics, ImmunoGen-aligned programs, and radiopharmaceutical developers expand clinical breadth. The convergence of AI-enabled target discovery, biomarker-driven trial design, and industrial-scale conjugation manufacturing positions North America as the principal commercialization and platform-development hub for next generation conjugate therapeutics.

Asia Pacific Next Generation Drug Conjugates Market Trends

Asia Pacific is projected to be the fastest-growing regional market for next-generation drug conjugates, with significant growth in China, Japan, and India as local innovation and clinical activity scale. China is expected to drive most of the growth, fueled by an expanding domestic biotech sector and companies, including Kelun-Biotech, Sirnaomics, and Suzhou Ribo, which are advancing conjugate and oligonucleotide pipelines in collaboration with global partners. Japan contributes high-value translational science through platforms such as PeptiDream, with support from multinational companies such as Novartis. India is emerging as a cost-efficient development and manufacturing hub, with its growing CDMO footprint and biologics capabilities being leveraged by Western sponsors for resilient supply chains and faster clinical execution.

The region’s growth is driven by rising oncology incidence, expanding clinical trial infrastructure, and lower development costs, all of which support a steady inflow of licensing and co-development agreements. Partnerships are increasingly pairing Western payload technologies with Asian-scale process development and patient recruitment. Activity is expanding beyond traditional ADCs into peptide conjugates, radioconjugates, and GalNAc-based delivery systems, with regional companies investing in linker chemistry and scalable bioprocessing. As clinical and manufacturing depth grows, Asia Pacific is set to become the key driver of volume growth in the global next-gen drug conjugates market.

Europe Next Generation Drug Conjugates Market Trends

Europe is expected to remain the second-largest and stable market for conjugated therapeutics, bolstered by strong clinical research in countries, including Germany, the U.K., and France, along with a coordinated regulatory and reimbursement environment. The region benefits from academic–industry collaborations, nationally funded research, and the presence of major pharma players, including Roche, Novartis, Bayer, AstraZeneca, and Sanofi, which anchor late-stage development and commercialization. The U.K. stands out in peptide drug conjugate research through innovators such as Bicycle Therapeutics, while France’s radiopharmaceutical expertise and Novartis’ Lutathera franchise enhance the region's credibility in targeted radioligand and peptide-based conjugates.

Market growth in Europe is driven by payer-driven value assessments and health technology evaluations that prioritize conjugate platforms showing improvements in therapeutic index, response durability, and patient stratification. Leading companies are integrating conjugates with immuno-oncology regimens, expanding indications beyond monotherapy. Strategic collaborations, such as Bayer’s partnership with Bicycle Therapeutics on radio-conjugates and AstraZeneca’s work in oligonucleotide and conjugate modalities, reflect the shift toward multi-modal pipelines. Europe’s strong reimbursement structure, translational science, and platform partnerships position it as a key region for next-gen conjugate therapeutics.

Competitive Landscape

The global next generation drug conjugates market exhibits a moderately consolidated structure, with a limited group of leading pharmaceutical companies accounting for the majority of the overall value. Large, established players continue to anchor the competitive landscape through strong clinical pipelines, global commercialization capabilities, and deep regulatory experience. At the same time, the competitive balance is shifting as mid-sized biotechnology firms with proprietary linker and payload platforms attract substantial investor backing and partnership interest. This dynamic is reshaping competitive power away from pure platform ownership toward the clinical and commercial performance of individual therapeutic assets.

Competitive positioning remains strongly innovation-led. Market leaders differentiate through late-stage clinical depth, broad therapeutic portfolios, and the ability to scale manufacturing and commercialization. Mid-tier and emerging biotech players compete by targeting focused therapeutic niches such as targeted radiopharmaceutical delivery and RNA-based conjugates, using differentiated chemistry and delivery technologies to secure strategic collaborations. Overall, market leadership increasingly reflects product-level clinical outcomes and regulatory success rather than platform breadth alone.

Key Industry Developments:

- In February 2026, Arrowhead Pharmaceuticals conducted a successful independent U.S. launch of REDEMPLO® (plozasiran) for FCS. This marks Arrowhead’s transition to a commercial-stage company, validating the TRiM™ platform's market viability. REDEMPLO is the first FDA-approved drug from Arrowhead’s TRiM™ platform, which utilizes GalNAc conjugation to deliver siRNA payloads specifically to hepatocytes. This validates the commercial viability of "ligand-mediated" delivery systems over older technologies such as lipid nanoparticles.

- In December 2025, Bicycle therapeutics 15-year strategic partnership with the UK Nuclear Decommissioning Authority for 212Pb supply. A major hurdle in the radiopharmaceutical market is the limited and unstable supply of alpha-emitting isotopes such as Lead-212 (212Pb). This partnership secures access to 400 tonnes of reprocessed uranium, providing a "sustainable and continuous" source. Lead-212 supply is a critical "make-or-break" factor for the next generation conjugates drugs market because it serves as the essential fuel for Targeted Alpha Therapy (TAT), the next frontier beyond current blockbuster radiotherapies such as Pluvicto®.

- In July 2024, Ionis Pharmaceuticals launched TRYNGOLZA™ (Olezarsen) as the first-ever therapy for FCS. This solidifies Ionis as a fully integrated commercial-stage biotech. Olezarsen represents the next frontier - Oligonucleotide Conjugates. This conjugate specifically targets Asialo-glycoprotein receptors (ASGR) on the surface of liver cells (hepatocytes). This ensures the drug is delivered directly to the liver while sparing other tissues, a core tenet of "next-gen" conjugate design.

Companies Covered in Next Generation Drug Conjugates Market

- Novartis

- Alnylam Pharmaceuticals

- AstraZeneca

- Ionis Pharmaceuticals

- Arrowhead Pharmaceuticals

- Bicycle Therapeutics

- Novo Nordisk

- Eli Lilly

- Roche

- Bristol Myers Squibb

- Sanofi

- Telix Pharmaceuticals

- Lantheus

- Sutter Hill Ventures-backed Kivu Bioscience

- Araris Biotech

- Chugai Pharmaceutical

- CureVac

Frequently Asked Questions

The global next generation drug conjugates market is projected to be valued at US$3.9 billion in 2026 and is expected to reach US$10.9 billion by 2033, driven by the clinical and commercial validation of targeted platforms such as RNAi conjugates and peptide-drug conjugates.

The shift from antibody-centric platforms toward ligand-guided modalities such as peptides and GalNAc constructs improves tissue penetration, intracellular uptake, and payload stability. Regulatory validation of these platforms in approved therapies (e.g., Givlaari®, Pluvicto®) has de-risked adoption, accelerating pipeline progression and commercialization.

The next generation drug conjugates market is forecast to grow at a CAGR of 15.3% from 2026 to 2033, reflecting strong clinical momentum and expanding therapeutic applications beyond oncology into rare and cardiometabolic diseases.

North America is the dominant regional market, accounting for approximately 71% share, supported by its deep biopharmaceutical R&D ecosystem and rapid clinical adoption of radioligand and RNAi therapies.

The market is moderately consolidated, with leadership from Novartis and Alnylam Pharmaceuticals, which have established commercial franchises in radioligand and RNAi therapies. Platform-specialist biotechs such as Arrowhead Pharmaceuticals, Ionis Pharmaceuticals, and Bicycle Therapeutics compete through differentiated delivery chemistries and strategic partnerships with large pharma.