- Specialty & Fine Chemicals

- Leather Chemicals Market

Leather Chemicals Market Size, Share, and Growth Forecast, 2025 - 2032

Leather Chemicals Market by Product Type (Tanning and Dyeing Chemicals, Beam-house Chemicals, Finishing Chemicals), Chemical Function (Chrome-based, Chrome-free Mineral, Synthetic Organic), End-use (Footwear, Furniture, Automotive, Textile and Fashion, Others), and Regional Analysis for 2025 - 2032

Leather Chemicals Market Size and Trends Analysis

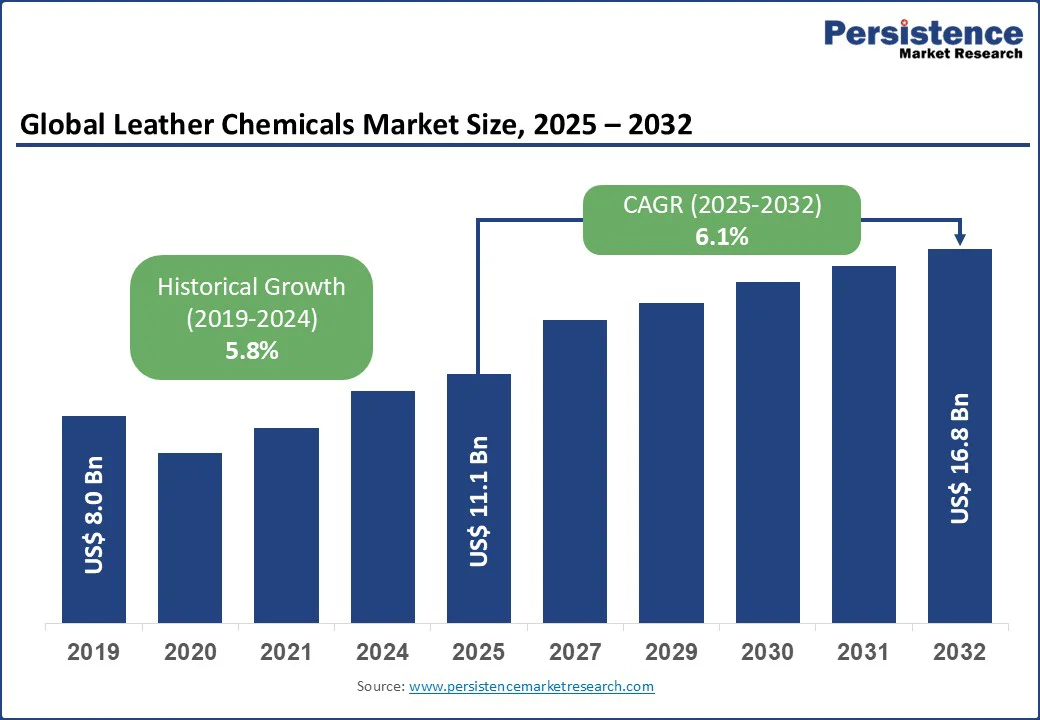

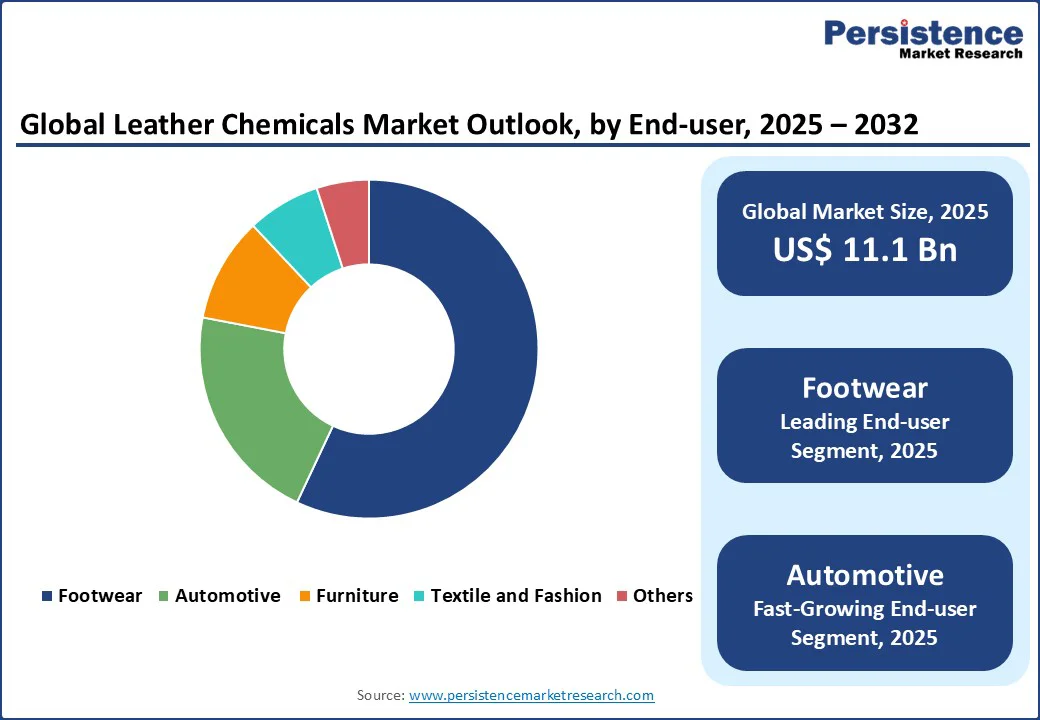

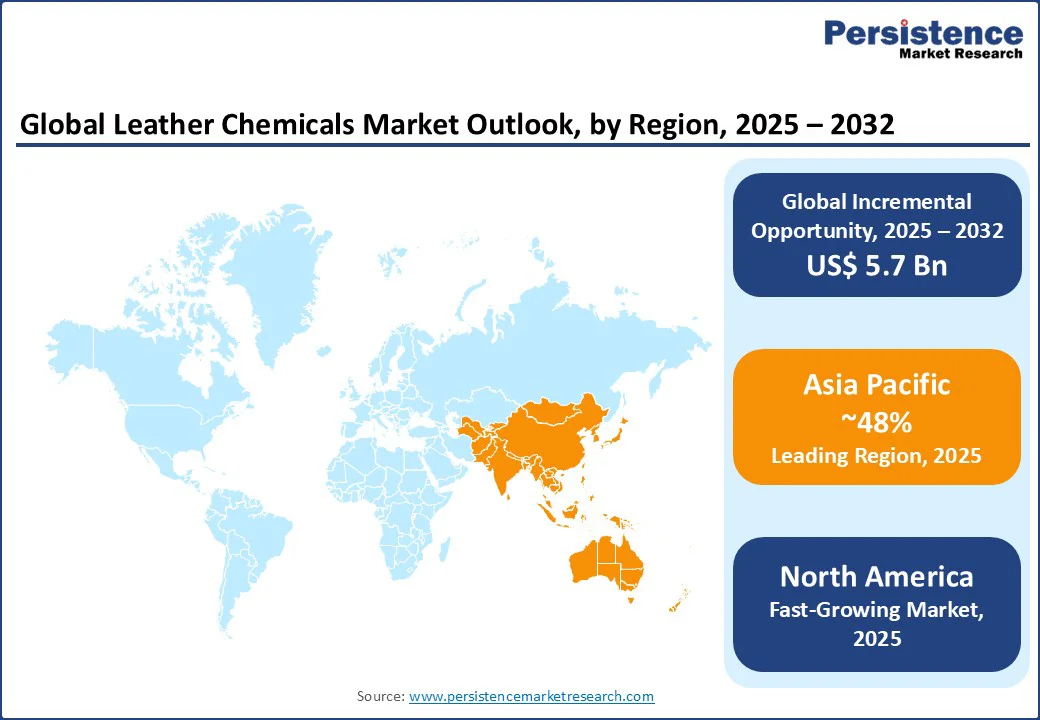

The global leather chemicals market size is likely to be valued at US$11.1 Bn in 2025 and is expected to reach US$16.8 Bn by 2032, growing at a CAGR of 6.1% during the forecast period from 2025 to 2032.

Key Industry Highlights:

- Leading Region: Asia Pacific, holding a 48% market share in 2025, driven by the dominance of leather production hubs in China and India, high demand for footwear and automotive leather, and rapid industrialization.

- Fastest-growing Region: North America is the fastest-growing market, fueled by expanding manufacturing capabilities, rising consumer demand for premium leather goods, and supportive government policies in countries such as China, India, and Vietnam.

- Dominant Product Type: Tanning and dyeing chemicals, commanding nearly 46% market share, due to their critical role in leather processing and widespread use in high-volume production for footwear and fashion.

- Leading End-Use: Footwear, accounting for over 57% of market revenue, driven by global demand for stylish, durable, and sustainable leather footwear.

| Global Market Attribute | Key Insights |

|---|---|

| Leather Chemicals Market Size (2025E) | US$11.1 Bn |

| Market Value Forecast (2032F) | US$16.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.8% |

The leather chemicals industry has witnessed robust growth, driven by increasing demand for high-quality leather products in sectors such as footwear, automotive, and fashion, coupled with advancements in eco-friendly and sustainable chemical solutions. The need for efficient processing, enhanced durability, and aesthetic appeal in leather production has significantly boosted market expansion.

Market Dynamics

Driver - Rising Demand for Sustainable and High-Quality Leather Products

The rising consumer inclination toward sustainable and premium-quality leather products is a major factor driving the leather chemicals market. Over the past decade, demand for high-end leather goods across the footwear, automotive, and fashion industries has expanded significantly, fueled by increasing disposable incomes, rapid urbanization, and evolving preferences for durable and aesthetically appealing materials.

Leather chemicals such as tanning agents, dyes, and finishing solutions are essential in improving the strength, texture, and appearance of leather, making them critical in meeting these market expectations.

Leading players such as Stahl International and BASF SE are investing in eco-friendly innovations to meet the needs of environmentally conscious consumers and adhere to stringent regulatory frameworks such as the EU’s REACH regulation.

Moreover, the rise of vegan leather alternatives, although a challenge for traditional leather, has stimulated the development of synthetic organic chemicals designed to replicate leather properties, further supporting market expansion.

For instance, Stahl introduced its Stahl Neo and Ympact portfolios, both bio-based and compliant with REACH and ZDHC MRSL requirements. At the same time, BASF launched Hapte, a sustainable synthetic leather solution that cuts greenhouse gas emissions by 52%, lowers energy consumption by 20%, and reduces water use by 30% compared to conventional methods.

Restraint - Stringent Environmental Regulations and High Compliance Costs

Stringent environmental regulations and high compliance costs pose significant challenges to the leather chemicals market. The production and chemical function of leather chemicals, particularly chrome-based tanning agents, involve processes that can generate hazardous waste and emissions, raising environmental concerns.

Regulatory bodies such as the U.S. Environmental Protection Agency (EPA), the European Chemicals Agency (ECHA), and China’s Ministry of Ecology and Environment impose strict guidelines on chemical usage, waste disposal, and emissions, requiring manufacturers to invest in costly compliance measures.

For instance, compliance with the EU’s REACH regulation, which restricts the use of hazardous substances such as chromium, demands significant financial investment in R&D for alternative chemicals and advanced waste treatment systems.

These compliance costs are particularly burdensome for small and medium enterprises (SMEs), which often lack the resources to adopt eco-friendly technologies or meet regulatory standards. Additionally, the complexity of aligning chemical formulations with diverse regional regulations increases production costs and extends project timelines.

For example, in 2023, a leading leather chemical manufacturer faced delays in product launches due to prolonged regulatory approvals in Europe, highlighting the financial and operational strain caused by compliance challenges. While large players such as Lanxess AG and Clariant can absorb these costs, smaller manufacturers face barriers to entry, limiting market innovation and growth.

Opportunity - Advancements in Eco-Friendly and Bio-Based Leather Chemicals

Advancements in eco-friendly and bio-based leather chemicals present a boost for the sector. The increasing focus on sustainability and environmental responsibility has driven research into innovative chemical solutions, such as chrome-free tanning agents, bio-based dyes, and water-based finishing chemicals.

These advancements reduce the environmental footprint of leather production while meeting consumer demand for sustainable products. For instance, companies such as Stahl International and TFL Ledertechnik GmbH have developed bio-based tanning agents derived from natural End-uses, such as vegetable extracts, which offer comparable performance to traditional chemicals with lower environmental impact.

The integration of nanotechnology in finishing chemicals has enabled the development of water-repellent, stain-resistant, and durable leather products, appealing to industries such as automotive and fashion. The rise of circular economy initiatives, particularly in Europe and North America, has further encouraged manufacturers to adopt recyclable and biodegradable chemical solutions.

For instance, BASF SE’s introduction of a biodegradable finishing agent in 2024 reduced waste in leather processing by 20%, gaining traction among eco-conscious brands. As global demand for sustainable leather products grows, particularly in premium segments such as automotive and luxury fashion, eco-friendly and bio-based leather chemicals are expected to create new avenues for innovation and long-term market expansion.

Category Analysis

Product Type Insights

Tanning and dyeing chemicals dominate the leather chemicals market, expected to account for approximately 46% share in 2025. Their dominance stems from their essential role in transforming raw hides into finished leather, ensuring durability, color consistency, and aesthetic appeal.

These chemicals are widely used in high-volume production for footwear and fashion, with companies such as Clariant and DyStar Group offering advanced tanning and dyeing solutions that enhance efficiency and quality. Their versatility and compatibility with diverse leather types make them a preferred choice for manufacturers globally.

The finishing chemicals segment is the fastest-growing, driven by increasing demand for high-performance and aesthetically appealing leather products in automotive and furniture. Finishing chemicals, such as coatings and sealants, enhance leather’s resistance to wear, water, and stains, catering to industries with stringent quality requirements.

The growing popularity of premium leather in luxury vehicles and high-end furniture, particularly in North America and Europe, is accelerating the adoption of advanced finishing solutions, with significant growth potential in high-value chemical functions.

Chemical Function Insights

Chrome-based chemicals accounted for a 57% share in 2025. Their dominance is driven by cost-effectiveness, efficiency, and the ability to produce high-quality leather with superior strength and flexibility. Chrome-based tanning agents, offered by companies such as Lanxess AG and BASF SE, are widely used in footwear and automotive leather production due to their scalability and reliability.

The chrome-free mineral segment is the fastest-growing, fueled by rising environmental concerns and regulatory restrictions on chrome-based chemicals. Chrome-free tanning agents, such as those based on vegetable or synthetic alternatives, are gaining traction in eco-conscious markets such as Europe and North America. The shift toward sustainable leather production, supported by innovations from companies such as Stahl International, is driving rapid adoption in this segment.

End-use Insights

Footwear accounts for approximately 57% of the revenue share in 2025. The segment’s dominance is driven by the global demand for stylish, durable, and sustainable leather footwear, particularly in emerging markets such as the Asia Pacific. Companies such as TFL Ledertechnik GmbH and Schill+Seilacher GmbH provide tailored chemical solutions that enhance footwear leather quality, supporting large-scale production for global brands.

The Automotive end-use is the fastest-growing, driven by the increasing adoption of premium leather in luxury and electric vehicles. Leather chemicals enable the production of high-performance leather with enhanced durability and aesthetics, meeting the automotive industry’s stringent standards. The rise in electric vehicle production, particularly in the Asia Pacific and Europe, is accelerating the adoption of specialized chemical solutions in this segment.

Regional Insights

North America Leather Chemicals Market Trends

North America is projected to account for the leather chemicals market, reflecting its strong position in premium leather production and innovation. The United States dominates the region, driven by its robust automotive and fashion industries, which demand high-quality leather chemicals for luxury vehicles and designer apparel. Leading companies such as DuPont de Nemours Inc. and Eastman Chemical Company are headquartered in the U.S., contributing to the region’s leadership in developing advanced chemical solutions.

The growing focus on sustainable leather production, supported by EPA regulations and consumer demand for eco-friendly products, has spurred investments in chrome-free and bio-based chemicals. Additionally, the rise of electric vehicle manufacturing in the U.S., with companies such as Tesla prioritizing premium leather interiors, has increased demand for specialized finishing chemicals.

North America’s strong R&D ecosystem and private investments in sustainable technologies continue to drive market growth, positioning the region as a key player in shaping global trends in the leather chemicals market.

Europe Leather Chemicals Market Trends

Europe is a significant player in the leather chemicals market, supported by its strong fashion, automotive, and furniture industries. Leading countries such as Italy, Germany, and France drive the region’s growth, with Italy emerging as a global hub for luxury leather goods.

The European Chemicals Agency (ECHA) and stringent REACH regulations have accelerated the adoption of eco-friendly chemicals, such as chrome-free tanning agents and bio-based finishes. Companies such as Stahl International and BASF SE are at the forefront of developing sustainable solutions, catering to the premium brands in the fashion and automotive sectors.

The region’s focus on circular economy initiatives and sustainable production practices has further encouraged R&D for recyclable and biodegradable chemicals. The growing demand for premium leather in luxury vehicles and high-end furniture, particularly in Germany and France, strengthens Europe’s market position, ensuring steady growth in the coming years.

Asia Pacific Leather Chemicals Market Trends

Asia Pacific is positioned as the leading market for the global leather chemicals market, holding a 48% share in 2025. Countries such as China, India, and Vietnam are driving the region’s expansion, with China as the largest producer and consumer of leather goods globally.

The region’s dominance is fueled by its massive footwear and apparel manufacturing base, supported by low-cost labor and large-scale production capabilities. India’s leather industry, driven by government initiatives such as “Make in India,” is expanding rapidly, with companies such as Pidilite Industries Limited and Haryana Leather Chemicals Ltd catering to domestic and export markets.

The growing demand for automotive leather, particularly in China’s booming electric vehicle sector, is driving the adoption of specialized chemicals. Additionally, the rise in consumer spending on premium leather goods and supportive government policies for sustainable manufacturing are creating substantial opportunities for chemical vendors. With advancements in eco-friendly chemicals and expanding industrial Chemical Functions, the Asia Pacific is expected to dominate future market growth.

Competitive Landscape

The global leather chemicals market is marked by intense competition, combining the dominance of established global leaders with the presence of numerous regional and niche players. In developed regions such as North America and Europe, major firms, including Clariant, Lanxess AG, and BASF SE, lead through economies of scale, advanced R&D capabilities, and long-standing partnerships with leather goods manufacturers.

Asia Pacific region is experiencing rapid expansion, supported by rising demand for footwear, automotive interiors, and fashion products, as well as increasing investments from both international players such as Stahl International and TFL Ledertechnik GmbH, and regional companies such as Pidilite Industries Limited and Haryana Leather Chemicals Ltd.

The market demonstrates a dual structure consolidated at the top by global multinationals, yet fragmented across mid-sized and local vendors catering to cost-sensitive markets. To remain competitive, companies are emphasizing product innovation, eco-friendly and bio-based chemical solutions, and compliance with sustainability regulations.

Strategic collaborations with leather manufacturers, increased investment in R&D for sustainable technologies, and adoption of digital marketing and supply chain optimization have emerged as key approaches, especially as demand rises from premium footwear, automotive, and luxury fashion segments.

Key Developments

- In July 2024, BASF launched Haptex 4.0, a new material for making synthetic leather that is fully recyclable. This means leather products made with it can be reused without creating waste, and it can be recycled together with PET fabric without the need to separate layers.

- In January 2024, Pidilite Industries Limited partnered with Italy’s Syn-Bios to distribute Syn-Bios products across South Asia (India, Sri Lanka, Bangladesh, Nepal, and Vietnam), along with a technical collaboration for leather chemical solutions.

Companies Covered in Leather Chemicals Market

- Clariant

- DyStar Group

- Elementis PLC

- Lanxess AG

- Stahl International B.V.

- BASF SE

- TFL Ledertechnik GmbH

- Zschimmer & Schwarz Chemie GmbH

- Schill+Seilacher GmbH

- Sisecam Chemicals

- Buckman Laboratories International

Pidilite Industries Limited - Silvateam S.p.A.

- Abhilash Chemicals and Pharmaceuticals Pvt Ltd

- Others

Frequently Asked Questions

The global Leather Chemicals Market is projected to reach US$ 11.1 Bn in 2025.

The rising demand for sustainable and high-quality leather products is a key driver.

The leather chemicals market is poised to witness a CAGR of 6.1% from 2025 to 2032.

Advancements in eco-friendly and bio-based leather chemicals are a key opportunity.

Clariant, Lanxess AG, BASF SE, Stahl International B.V., and TFL Ledertechnik GmbH are key players.