- Advanced Materials

- Silicone Solutions for Leather and Textile Market

Silicone Solutions for Leather and Textile Market Size, Share, and Growth Forecast 2026 - 2033

Silicone Solutions for Leather and Textile Market by Product Type (Silicone Resin, Silicone Fluid, Silane Coupling Agent), Application (Textile, Leather), and Regional Analysis, 2026 - 2033

Silicone Solutions for Leather and Textile Market Size and Trend Analysis

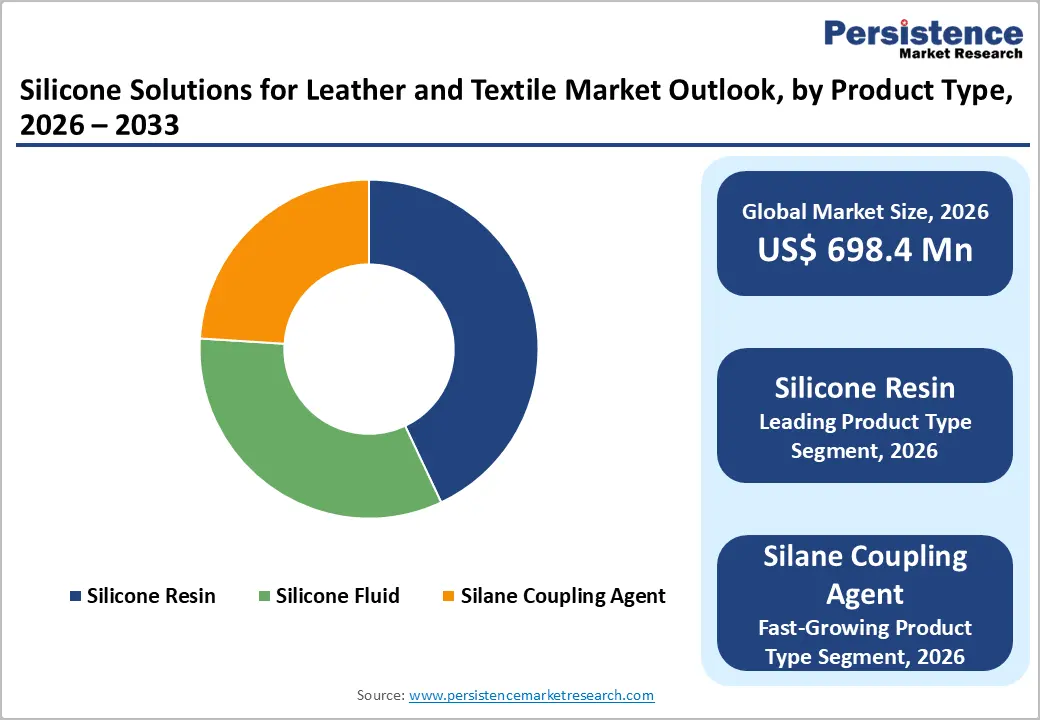

The global silicone solutions for leather and textile market size is expected to be valued at US$ 698.4 million in 2026 and projected to reach US$ 1,071.1 million by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The silicone solutions for the leather and textile markets are advancing amid the convergence of growing global apparel and footwear production, rising consumer demand for functional performance finishes, including water repellency, softness, and durability, and regulatory pressure on legacy fluorochemical (PFAS) textile finishes, driving formulator substitution toward silicone-based alternatives.

Expanding Asia Pacific textile and leather manufacturing in China, India, Bangladesh, and Vietnam is simultaneously creating the largest demand base for silicone softeners, water repellents, and bonding agents, while growing global sustainability standards are incentivizing adoption of eco-compliant silicone chemistry across premium apparel and footwear supply chains.

Key Industry Highlights:

- Leading Region: Asia Pacific holds approximately 43% of global silicone solutions for the leather and textile market share in 2026, anchored by China's 35%+ share of global textile exports and India's position as the second-largest global leather exporter.

- Fastest Growing Region: Middle East & Africa is the fastest-growing region through 2033, driven by government-backed textile and leather manufacturing investment in Ethiopia, Egypt, and South Africa, with IFC-supported sustainable tannery development creating silicone finishing solution demand.

- Dominant Segment: Silicone Resin commands approximately 43% of global product type share in 2026, driven by its essential film-forming, water repellent, and performance finishing functions across apparel, technical textiles, and premium leather goods supply chains globally.

- Fastest Growing Segment: Silane Coupling Agents are the fastest-growing product type at 8% CAGR (2026 - 2033), driven by technical textile expansion in automotive, protective, and medical fabric applications where bifunctional silane chemistry enables superior inorganic-organic substrate adhesion performance.

- Key Market Opportunity: Companies investing in PFAS-free silicone DWR finishing solutions stand to capture accelerating reformulation demand as California AB 1817, ECHA PFAS restrictions, and U.S. EPA mandates compel global apparel and outdoor brands to replace fluorochemical DWR finishes through 2026 - 2033.

DRO Analysis

Drivers - Regulatory Phase-Out of PFAS Fluorochemicals Accelerating Silicone Substitution in Textile Finishing

The accelerating global regulatory phase-out of per- and polyfluoroalkyl substances (PFAS), the workhorse chemistry of durable water repellent (DWR) finishes in the textile and outdoor apparel industry, is creating a structural, compliance-driven demand tailwind for silicone-based water repellent and functional finishing solutions. The European Chemicals Agency (ECHA) has advanced a universal PFAS restriction proposal that could affect thousands of applications across textiles and leather.

The U.S. EPA's PFAS Strategic Roadmap and state-level restrictions, including California AB 1817 prohibiting PFAS in apparel from 2025, are compelling brands including Patagonia, Gore-Tex, and major fast-fashion manufacturers to reformulate DWR finishes with silicone chemistry, directly expanding the addressable market for providers like Dow Inc. and Wacker Chemie AG.

Growing Global Apparel and Footwear Industry Driving Silicone Finishing Chemical Demand

The sustained expansion of the global apparel and footwear industry, the primary end-use sector for silicone finishing solutions, is creating a structurally growing demand base for silicone softeners, water repellents, and leather treatment products. According to the World Trade Organization (WTO), global textile and clothing exports consistently exceed US$ 900 billion annually, reflecting the scale of production requiring functional chemical finishing.

The International Leather Working Group (ILWG) reports growing brand member commitments to sustainable leather finishing chemistries, a trajectory that increases silicone solution adoption in premium leather goods manufacturing. Shin-Etsu Chemical Co., Ltd. and Momentive Performance Materials are expanding their textile and leather silicone product portfolios to capture this industry-level demand growth.

Restraints - High Raw Material Costs of Silicone Chemistry Relative to Conventional Textile Chemicals

Silicone-based finishing solutions command significant price premiums over conventional organic textile chemicals, typically 2-4x the cost of comparable wax-based or conventional softener chemistries, creating adoption friction in price-sensitive mass-market apparel and textile manufacturing segments, particularly across South and Southeast Asia where cost compression is a primary manufacturing imperative.

Silicon metal, the primary feedstock for silicone production, is subject to commodity price volatility, and supply disruptions in key production regions including China create input cost instability for silicone specialty chemical producers that limits margin visibility and constrains price competitiveness against alternative finishing chemistries.

Technical Formulation Complexity and Application Process Integration Challenges

Effective application of silicone finishing solutions to textile and leather substrates requires precise formulation chemistry, process control, and application equipment calibration, technical requirements that create meaningful adoption barriers for smaller textile mills and tanneries that lack in-house chemical finishing expertise. The Society of Dyers and Colourists (SDC) documents that silicone emulsion stability, substrate compatibility, and curing process optimization are non-trivial technical challenges that demand supplier technical service support.

This complexity limits the pace of technology adoption among the fragmented small and medium-scale manufacturing base that constitutes a significant share of global textile and leather production volume, particularly in developing market geographies.

Market Opportunities

Silane Coupling Agents: Fastest-Growing Product Type Driven by Technical Textile and Composite Applications

Silane Coupling Agents represent the fastest-growing product type within the silicone solutions for leather and textile market at a CAGR of 8% (2026 - 2033), driven by expanding adoption in technical textile applications including coated fabrics, composite reinforcement textiles, and functional surface modification for specialty synthetic fibers.

Silane coupling agents provide unique bifunctional chemistry that bridges inorganic substrate surfaces and organic polymer matrices, enabling superior adhesion, durability, and moisture resistance in demanding end-use applications including automotive interior textiles, protective workwear, and medical textiles.

The European Technical Textiles Association (EURATEX) reports that technical textile production is growing at above-average rates relative to conventional textiles, providing Evonik Industries AG, Dow Inc., and Wacker Chemie AG with a premium-margin growth vector in the silicon solutions market.

Middle East & Africa: Fastest-Growing Regional Market Driven by Textile and Leather Industry Development

The Middle East & Africa (MEA) region is the fastest-growing market for silicone solutions in leather and textile, driven by strategic government investment in domestic textile and leather manufacturing capacity across Ethiopia, Egypt, South Africa, Saudi Arabia, and UAE. Ethiopia's textile export industry, supported by government industrial park investments, has attracted major global apparel brands seeking cost-competitive manufacturing with sustainability compliance credentials, creating demand for advanced silicone finishing chemistries.

Africa's leather industry, backed by significant raw hide availability, is a target for value-added processing investment, with International Finance Corporation (IFC) initiatives supporting sustainable tannery development that requires compliant silicone-based leather treatment solutions. Specialty chemical distributors are actively expanding MEA distribution networks to capture this emerging regional demand.

Category-wise Analysis

Product Type Insights

Silicone resin leads the silicone solutions for leather and textile market by product type with approximately 43% of global market share in 2026, anchored by its critical functional roles in textile coating, leather finishing, and durable water repellent treatment applications where film-forming, cross-linking, and heat-resistant properties provide superior end-performance versus competing chemistries.

Silicone resins enable key performance attributes including dry-hand feel, anti-static properties, abrasion resistance, and high-temperature press stability in fabric finishing, applications where Dow Inc.'s DOWSIL range and Wacker Chemie AG's WACKER FINISH maintain strong market positions. Silane Coupling Agents are the fastest-growing segment at 8% CAGR (2026 - 2033), driven by technical textile innovation and PFAS-free surface treatment demand in specialty applications.

Application Insights

The textile application segment leads the silicone solutions market with approximately 62% of global market share in 2026, reflecting the far greater production volume and product diversity of the global textile industry relative to leather, the WTO reports global textile and clothing trade exceeding US$ 900 billion annually, dwarfing leather goods trade. Silicone softeners, water repellents, anti-crease agents, and functional coatings are applied across virtually all textile categories, from apparel and home textiles to technical and industrial fabrics, creating a vast, volume-driven demand base.

The Leather application segment is the fastest-growing application, driven by rising global leather goods consumption, premiumization of footwear and accessories, and the International Leather Working Group (ILWG)'s sustainability compliance requirements pushing tanneries toward higher-performance silicone-based finishing chemistry.

Regional Insights

North America Silicone Solutions for Leather and Textile Market Trends and Insights

North America accounts for approximately 18% of global silicone solutions for leather and textile market share in 2026, driven by stringent PFAS regulatory frameworks at both federal (U.S. EPA) and state levels compelling DWR finish reformulation, strong demand from technical textile manufacturers, and robust R&D investment by leading silicone specialty chemical producers including Dow Inc. and Momentive Performance Materials headquartered in the region.

U.S. Silicone Solutions for Leather and Textile Market Size

The United States represents approximately 80% of North American market revenue, backed by dominant silicone chemistry R&D leadership and California AB 1817's PFAS apparel prohibition from 2025, the most consequential state-level regulatory driver for silicone DWR adoption globally. Outdoor performance apparel brands including Patagonia and The North Face are key silicone finishing solution adopters, sustaining U.S. premium segment demand.

Europe Silicone Solutions for Leather and Textile Market Trends and Insights

Europe accounts for approximately 22% of global market share in 2026, shaped by the European Chemicals Agency (ECHA)'s universal PFAS restriction proposal and the EU REACH regulation's stringent chemical substance management framework. Archroma, The CHT Group, and Lanxess AG are key European specialty chemical players with silicone-based textile and leather finishing solutions serving Germany, Italy, and other major European textile production centers.

Germany Silicone Solutions for Leather and Textile Market Size

Germany is Europe's largest silicone solutions for leather and textile market, contributing approximately 20-22% of regional revenue. Germany's world-class technical textile industry, documented by VDMA (Mechanical Engineering Industry Association), and premium leather goods sector create high-specification silicone solution demand. Wacker Chemie AG's Munich headquarters and Evonik Industries AG's specialty silane portfolio provide strong domestic supply-side infrastructure.

U.K. Silicone Solutions for Leather and Textile Market Size

The United Kingdom represents approximately 14-16% of European silicone solutions market value for leather and textile, with demand driven by the U.K.'s established technical textile sector and premium apparel and footwear brands adopting PFAS-free silicone DWR finishes under growing regulatory and consumer sustainability pressure. The CHT Group and Archroma maintain active U.K. distribution and technical service operations supporting the transition.

France Silicone Solutions for Leather and Textile Market Size

France contributes approximately 11-13% of the European silicone solutions for leather and textile market, with premium demand from France's world-leading luxury leather goods industry, encompassing brands within LVMH and Kering supply chains, that require high-performance, sustainable silicone-based leather finishing treatments. France's REACH-aligned regulatory environment and luxury brand sustainability commitments are strong demand catalysts for compliant silicone leather chemistry through 2033.

Asia Pacific Silicone Solutions for Leather and Textile Market Trends and Insights

Asia Pacific leads the global silicone solutions for leather and textile market with approximately 43% of global share in 2026, driven by the world's largest concentration of textile and leather manufacturing capacity. China alone accounts for over 35% of global textile exports per WTO data, creating massive domestic demand for silicone softeners, water repellents, and leather finishing agents. Rising sustainability brand compliance requirements across Asia Pacific manufacturing supply chains are driving quality upgrading in silicone finishing chemistry adoption.

India Silicone Solutions for Leather and Textile Market Size

India represents approximately 14-16% of Asia Pacific market revenue, supported by its position as one of the world's largest textile exporters and the second-largest leather exporter globally per Council for Leather Exports (CLE) data. Supreme Silicones India Pvt. Ltd. and Elkay Chemicals Pvt. Ltd. provide domestic silicone chemistry supply, while global players including Dow Inc. and Wacker Chemie AG compete through established local distribution networks.

Japan Silicone Solutions for Leather and Textile Market Size

Japan accounts for approximately 10-12% of Asia Pacific market value, characterized by high-specification demand from Japan's advanced technical textile manufacturers and premium apparel sector. Shin-Etsu Chemical Co., Ltd., one of Japan's largest silicone producers, maintains strong domestic market presence with a comprehensive textile and leather silicone portfolio. Japan's aging but precision-manufacturing oriented textile industry sustains consistent demand for high-performance silicone functional finishes.

Southeast Asia Silicone Solutions for Leather and Textile Market Size

Southeast Asia contributes approximately 14-16% of Asia Pacific market revenue and is a rapidly growing sub-region, driven by textile manufacturing expansion in Vietnam, Bangladesh (South Asia), Indonesia, and Cambodia. Global apparel brands relocating manufacturing from China to diversified Southeast Asian supply chains are creating growing demand for silicone finishing chemicals that meet international brand sustainability and performance specifications.

Competitive Landscape

The global silicone solutions for leather and textile market is moderately consolidated, with global silicone majors, Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Elkem ASA, and Momentive Performance Materials, competing on integrated silicone chemistry, formulation breadth, and global technical service capabilities.

Specialty chemical players including Archroma, The CHT Group, and Evonik Industries AG differentiate through application-specific formulation expertise and sustainability-certified product portfolios. Key emerging trends include PFAS-free DWR silicone innovation, bio-based silane coupling agent development, and digital technical service platforms enabling remote application support for Asian textile manufacturers.

Key Developments

- In February 2025: Wacker Chemie AG launched an expanded range of WACKER FINISH silicone softeners and water repellents specifically formulated as PFAS-free DWR alternatives for outdoor performance apparel, targeting European and North American brand compliance with REACH and EPA regulations.

- In October 2024: Dow Inc. expanded its Asia Pacific textile and leather silicone solutions distribution network through new partnerships in India and Vietnam, targeting the rapidly growing South and Southeast Asian textile manufacturing base with its DOWSIL textile finishing portfolio and technical service capabilities.

- In April 2024: Evonik Industries AG introduced a new generation of silane coupling agents for technical textile and composite fabric applications, targeting automotive interior textiles and specialty protective fabric markets where superior fiber-matrix adhesion and moisture resistance are critical performance requirements.

Silicone Solutions for Leather and Textile Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 495.1 million |

| Current Market Value (2026) | US$ 698.4 million |

| Projected Market Value (2033) | US$ 1,071.1 million |

| CAGR (2026 - 2033) | 6.3% |

| Leading Region | Asia Pacific, 43% market share (2026) |

| Dominant Product Type | Silicone Resin, 33% market share (2026) |

| Top-Ranking Application | Textile, 62% market share (2026) |

| Incremental Opportunity | US$ 372.7 million (Absolute Dollar Opportunity, 2026 - 2033) |

Companies Covered in Silicone Solutions for Leather and Textile Market

- Dow Inc.

- Wacker Chemie AG

- Elkem ASA

- KCC Corporation

- BASF

- Archroma

- Shin-Etsu Chemical Co. Ltd

- Evonik Industries AG

- Siltech Corporation

- Avantor Inc

- Momentive Performance Materials

- The CHT Group

- Lanxess AG

- Supreme Silicones India Pvt. Ltd.

- Elkay Chemicals Pvt. Ltd.

Frequently Asked Questions

The global Silicone Solutions for Leather and Textile market is valued at US$ 698.4 million in 2026. Growing at a CAGR of 6.3%, the market is projected to reach US$ 1,071.1 million by 2033, representing an absolute dollar opportunity of US$ 372.7 million driven by PFAS regulatory substitution, global apparel industry growth, and Asia Pacific manufacturing expansion.

The primary demand drivers are the accelerating global phase-out of PFAS fluorochemical DWR finishes, with California AB 1817 prohibiting PFAS in apparel from 2025 and ECHA's universal PFAS restriction advancing in the EU, compelling reformulation to silicone chemistry, and the sustained growth of global textile and leather manufacturing tracked by the WTO at over US$ 900 billion in annual exports.

Asia Pacific leads the global market with approximately 43% of global share in 2026, driven by China's dominance in global textile exports (35%+ of global volume per WTO data), India's position as the second-largest leather exporter, and the vast concentration of textile and leather manufacturing capacity across China, India, Vietnam, and Bangladesh requiring silicone finishing chemical inputs.

The most significant near-term growth opportunities are in PFAS-free silicone DWR finishing solutions, where regulatory mandates across the U.S., EU, and California are driving mandatory reformulation by global apparel brands, and in Silane Coupling Agents for technical textile applications growing at 8% CAGR, and in the Middle East & Africa region's fastest-growing manufacturing investment trajectory.

The leading companies include Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Elkem ASA, Evonik Industries AG, Momentive Performance Materials, Archroma, The CHT Group, BASF SE, and Lanxess AG, among others profiled comprehensively in this report.