- Clothing, Footwear, & Accessories

- Leather Luggage and Goods Market

Leather Luggage and Goods Market Size, Share, and Growth Forecast 2026 - 2033

Leather Luggage and Goods Market Product Type (Travel Luggage, Handbags, Backpacks, Wallets & Small Leather Goods, Briefcases & Business Bags, Other Leather Goods), Leather Type (Genuine Leather, Full-Grain Leather, Top-Grain Leather, Suede Leather, Miscellaneous Leather Types), Sales Channel (Online Retail, Specialty & Multi-Brand Stores, Single-Brand Stores, General Retailers & Department Stores, Other Unorganized Channels) and by Regional Analysis 2026 - 2033

Leather Luggage and Goods Market Size and Trend Analysis

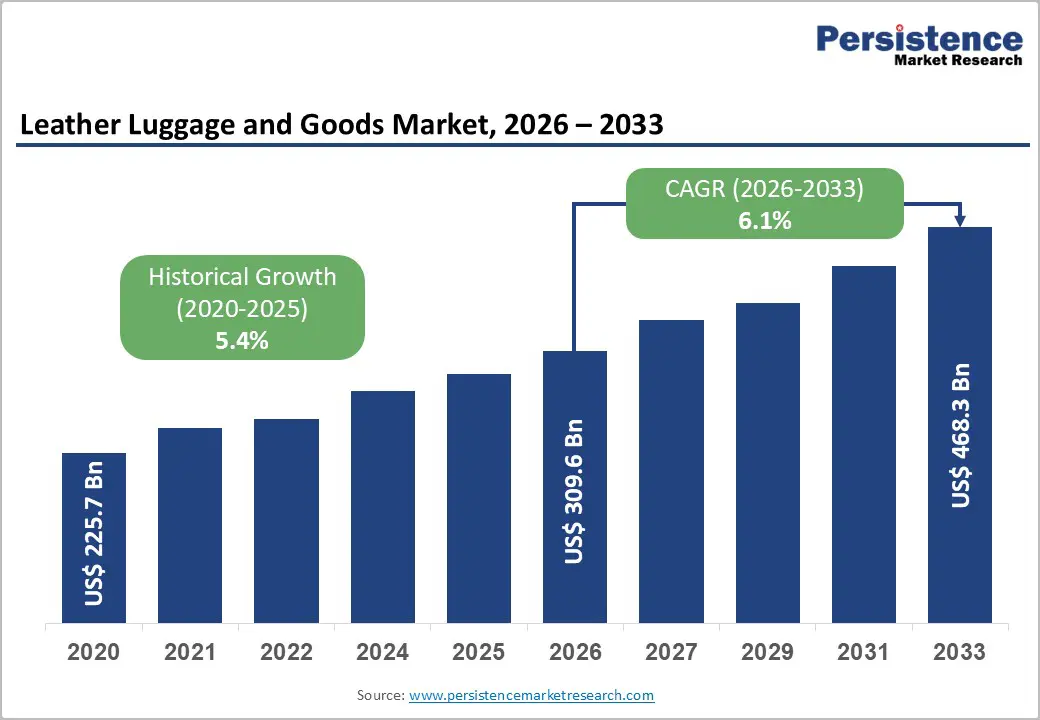

The global leather luggage and goods market size is projected at US$309.6 billion in 2026 and anticipated to reach US$468.3 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033. The market expansion is predominantly driven by accelerating disposable income levels in emerging economies, particularly across Asia Pacific, combined with surging international tourism activities and shifting consumer preferences toward premium, durable products.

Rising urbanization and middle-class expansion in developing nations, coupled with growing e-commerce penetration and digital-first retail adoption, further strengthen market fundamentals. Additionally, evolving consumer demand for customized, sustainable leather products and the integration of smart technology in luggage solutions contribute substantially to sustained market growth trajectories throughout the forecast period.

Key Highlights Summary

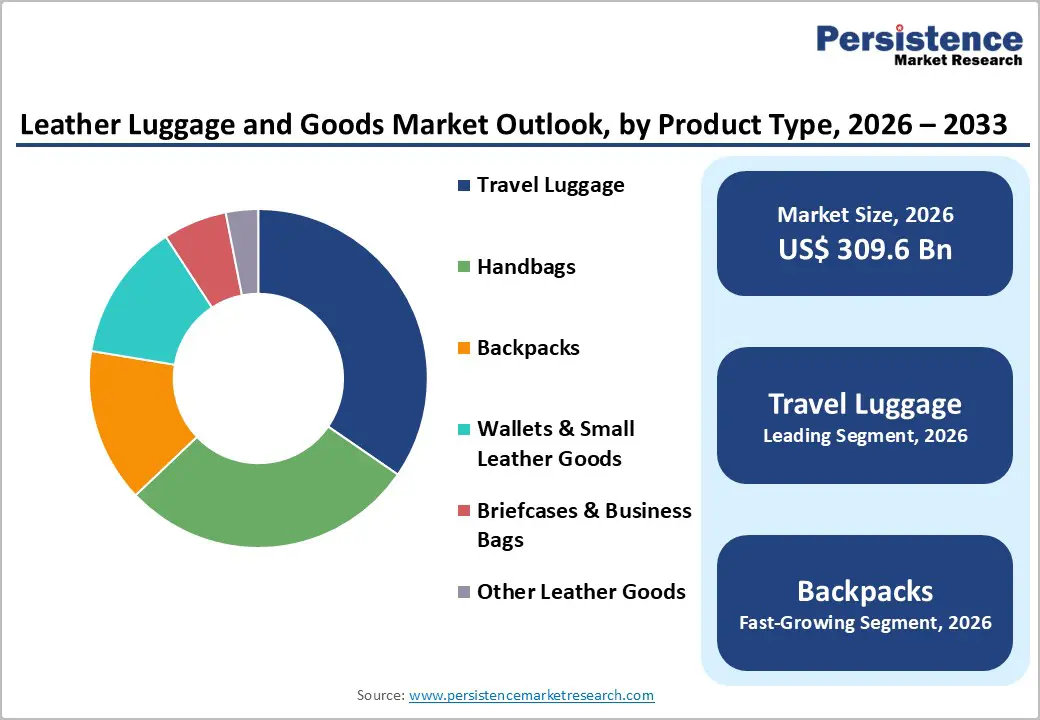

- Travel Luggage leads the product segmentation with 35% market share; Backpacks are the fastest-growing, with a 7.5% CAGR, reflecting evolving consumer preferences for versatile, functional designs that appeal to digital nomads and adventure travelers.

- Genuine Leather maintains 32% market leadership; Top-Grain Leather is the fastest-expanding leather type at 7.0% CAGR, driven by superior durability and cost-effectiveness for middle-market premium segments.

- Online Retail dominates at 29% share with fastest growth trajectory; Single-Brand Stores expanding at 5.9% CAGR, reflecting luxury brand investment in controlled premium retail environments and omnichannel strategies.

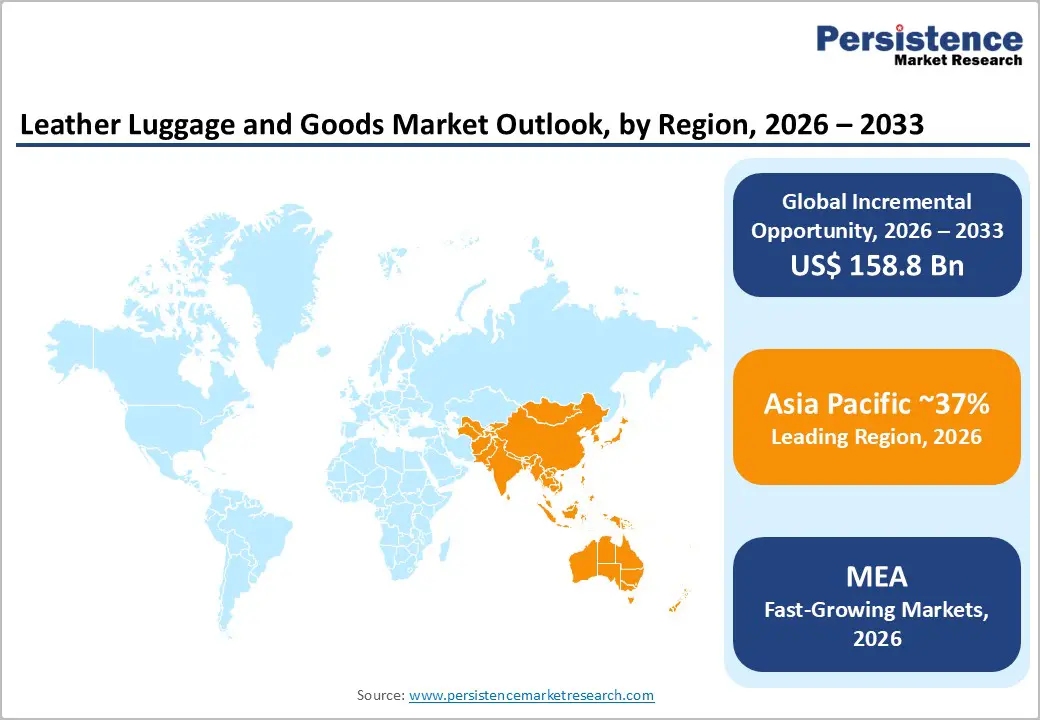

- Asia Pacific holds dominant 37% regional share with exceptional growth momentum; North America growing at 5.4% CAGR; Europe maintaining 24% share with 4.9% growth, supporting balanced geographic market expansion.

- Middle East & Africa emerges as the fastest-growing region at 6.3% CAGR, driven by rising luxury consumption in GCC economies, expanding tourism and aviation hubs, increasing expatriate populations, and growing preference for premium travel luggage and leather goods supported by modern retail and e-commerce expansion.

- Strategic developments emphasize sustainable manufacturing, smart technology integration, geographic expansion into emerging markets, and direct-to-consumer platform investment, positioning industry leaders to advantage in the evolving market.

| Key Insights | Details |

|---|---|

|

Leather Luggage and Goods Market Size (2026E) |

US$ 309.6 billion |

|

Market Value Forecast (2033F) |

US$ 468.3 billion |

|

Projected Growth CAGR (2026-2033) |

6.1% |

|

Historical Market Growth (2020-2025) |

5.4% |

Market Dynamics Analysis

Market Drivers

Escalating Disposable Income and Rising Living Standards

Rising disposable income, particularly across developing economies in Asia Pacific and Latin America, represents the primary catalyst for leather goods market expansion. The Asian middle-class population has grown exponentially, with per capita income in nations like India and China increasing substantially, enabling consumers to allocate greater spending toward premium, long-lasting products. Leather goods, traditionally positioned as luxury or aspirational items, are increasingly transitioning into accessible premium categories as consumer purchasing power strengthens. This income growth correlates directly with increased demand for high-quality travel luggage, designer handbags, and business accessories. Supporting data reveals that Asia Pacific households with incomes exceeding $35,000 annually expanded by 18% between 2022 and 2024, directly translating into heightened leather goods consumption. Furthermore, improved living standards encourage lifestyle upgrades, with leather products serving as visible status indicators and investment assets that retain value across generations.

Unprecedented Growth in International Travel and Tourism

Global tourism recovery post-2020 has reached unprecedented levels, with international arrivals exceeding 1.4 billion annually by 2024, substantially surpassing pre-pandemic volumes. This expansion directly stimulates demand for functional, durable travel luggage and accessories capable of withstanding repeated transit cycles. Both the leisure and business travel segments are experiencing accelerating growth, necessitating reliable luggage solutions and compact leather accessories. Airlines have collectively reported 12% year-over-year passenger growth, directly correlating with increased luggage sales volumes. Notably, emerging markets contribute 65% of incremental tourism growth, with Asia Pacific accounting for 38% of global leisure travel spending. Additionally, the recovery of business travel has reignited demand for professional briefcases, laptop bags, and compact business leather goods, capturing significant market share from traditional office supply segments. Premium travelers prioritize durable, elegant luggage that aligns with their personal brand positioning.

Market Restraints

Economic Volatility and Discretionary Spending Compression

Macroeconomic uncertainty, inflationary pressures, and weakened consumer confidence directly constrain discretionary spending on luxury leather goods. When households prioritize essential commodities over lifestyle accessories, demand for premium leather products contracts significantly. Consumers indicate 23% reduced willingness to purchase luxury items during periods of economic instability, directly impacting high-margin leather product categories. Luxury brand executives acknowledge that inflationary environments disproportionately affect aspirational and premium segments, prompting inventory adjustments and reductions in production scale. Supply chain disruptions during economic downturns further compress margins, as manufacturers struggle with volatile raw material costs and variable procurement cycles. This cyclical vulnerability represents a structural market constraint, particularly affecting emerging market consumers who demonstrate greater price elasticity.

Competitive Pressure from Synthetic and Vegan Leather Alternatives

Synthetic leather alternatives, including polyurethane (PU) and plant-based materials, increasingly compete for market share with genuine leather products. The global synthetic leather market is expanding at a 5.9% CAGR through 2035, capturing environmentally conscious consumers and price-sensitive segments. Technological advances have substantially improved the aesthetics and tactile properties of synthetic leather, reducing its differentiation from genuine leather. Additionally, regulatory restrictions on animal-hide production in certain jurisdictions and accelerating consumer demand for cruelty-free alternatives create structural headwinds for traditional leather manufacturers. Brands launching vegan leather collections capture younger demographics, prioritizing ethical consumption, fragmenting traditional leather market share.

Market Opportunities

Sustainability Innovation and Eco-Conscious Product Development

The consumer shift toward sustainable, environmentally responsible leather goods presents substantial growth avenues. Vegetable-tanned and eco-certified leather products command a premium of 15-25% over conventional leather, enabling margin expansion for manufacturers embracing sustainability. Emerging innovations, including lab-grown leather, mushroom-derived alternatives, and recycled leather composites, appeal to environmentally-conscious luxury consumers. The market for sustainable luxury goods is expanding at 8.2% CAGR, capturing significant wallet share from traditional leather segments. Additionally, circular economy business models, including resale platforms and refurbishment services, create supplementary revenue streams while reinforcing brand loyalty and customer lifetime value.

Emerging Market Expansion and Rapidly Urbanizing Consumer Base

Emerging markets, particularly India, Southeast Asia, and Latin America, offer expansive growth opportunities driven by urbanization and the expansion of the middle class. India's urban population is projected to reach 880 million by 2033, directly expanding leather goods consumer bases. Rising urban professionals increasingly demand premium accessories, while improvements in retail infrastructure and digital penetration enable market access. Regional luxury brands are establishing manufacturing and distribution networks, capturing local preferences while leveraging cost advantages, enabling competitive market participation.

Segmentation Analysis

Product Type Analysis

Travel luggage, encompassing suitcases, trolley bags, and duffel bags, maintains market leadership with 35% global share and dominant revenue contribution. Demand remains resilient, supported by rising international travel, expanding business mobility, and growing domestic tourism in emerging economies. Premium manufacturers differentiate through advanced materials, ergonomic design, durability and construction, sustaining premium pricing. Hard-shell luggage leads volumes, while soft-sided and hybrid designs gain traction. Established brands such as Samsonite, Delsey, and RIMOWA retain leadership through innovation, brand equity, and distribution networks.

Backpacks are the fastest-expanding category, registering 7.5% CAGR through 2033, outpacing overall market growth. Demand accelerates as consumers favor versatile designs for work and leisure. Younger demographics, adventure tourism, e-sports, and digital nomad lifestyles further stimulate volume growth across premium and aspirational price segments globally and within urbanizing emerging economies.

Leather Type Analysis

Genuine leather maintains market leadership with 32% global share, reflecting consumer preference for authentic, durable materials with inherent quality perception and longevity. Genuine leather products command premium pricing and sustained demand, particularly within luxury segments where craftsmanship and heritage narratives reinforce brand positioning. Full-grain and top-grain leather categories, representing natural material authenticity, dominate premium positioning within the genuine leather segment. Consumer perception of genuine leather as a reliable, long-lasting investment continues to support market dominance despite competitive synthetic alternatives.

Top-grain leather exhibits the highest growth trajectory within leather-type segmentation, expanding at 7.0% CAGR, driven by superior durability, aesthetic appeal, and cost-effectiveness relative to full-grain alternatives. This category appeals to middle-market consumers seeking quality without premium luxury positioning. Top-grain leather's responsiveness to finishing treatments enables diverse aesthetic variations, appealing to varied consumer preferences and fashion-forward positioning.

Sales Channel Analysis

Online retail maintains dominant positioning with 29% market share and continues as the fastest-growing distribution channel, driven by convenience, product selection transparency, and competitive pricing. Digital-native luxury brands increasingly allocate resources to proprietary e-commerce platforms and third-party marketplace participation, capturing direct consumer relationships and first-party data. Omnichannel retail strategies integrating online and offline touchpoints reflect industry best practices, enabling seamless customer experiences and sustained brand loyalty. Major luxury houses, including LVMH subsidiaries and independent premium brands, demonstrate heightened digital investment velocity.

While online retail dominates growth dynamics, single-brand retail stores are expanding, growing at a 5.9% CAGR, reflecting luxury brand strategies prioritizing controlled brand environments and premium customer experiences. Flagship store openings in major metropolitan centers reinforce brand prestige and enable direct consumer engagement, supporting elevated pricing and brand heritage communication.

Regional Market Insights

North America

North America commands global market positioning with revenue contribution, driven by high consumer purchasing power, established luxury brand infrastructure, and comprehensive premium retail networks. The United States dominates regional performance, supported by international travel activity, robust business travel ecosystems, and brand consciousness. Consumers show sustained willingness to spend on premium leather goods, particularly designer handbags and travel luggage. The region’s mature retail ecosystem, spanning specialty multi-brand stores, single-brand boutiques, and expanding e-commerce, enables market penetration. Regulatory emphasis on product quality and consumer protection reinforces market credibility, while innovation ecosystems support product development. Market growth at a 5.4% CAGR reflects maturity alongside wealth accumulation and international mobility expansion. Strategic investments focus on retail optimization and digital commerce enhancement, while competitive intensity remains high among established luxury houses and emerging digital-native brands.

Europe

Europe maintains a substantial global market share of approximately 24%, supported by heritage craftsmanship, established luxury brand dominance, and sophisticated consumer preferences. Germany, Italy, France, and Spain act as primary growth centers, with Italy renowned for exceptional leather manufacturing expertise and artisanal capabilities. Regulatory harmonization across the European Union, including sustainability mandates and environmental standards, creates a competitive framework that favors innovation-led manufacturers. Strong tourism flows and affluent demographics sustain premium demand across travel luggage, handbags, and business accessories. Regional growth at a 4.9% CAGR reflects market maturity with selective expansion in sustainable leather and technology-integrated products. Italian clusters in Tuscany and Puglia uphold global excellence, supplying premium materials. France anchors heritage luxury headquarters, Germany supports engineering-led luggage innovation, and Europe leads circular economy adoption, strengthening long-term competitiveness.

Asia Pacific

Asia Pacific commands dominant global positioning with 37% market share, driven by rapidly expanding consumer bases, accelerating urbanization, rising disposable incomes, and abundant manufacturing resources. China and India represent primary growth engines, with China maintaining mature market characteristics and India demonstrating emerging market expansion trajectories. Japan and South Korea contribute to premium market segments, with affluent consumers exhibiting elevated purchasing preferences for designer leather goods. Cost-competitive manufacturing advantages, raw material availability, and expanding e-commerce infrastructure enable rapid regional penetration. India’s leather manufacturing sector offers competitive cost positioning and skilled labor, supporting domestic and export demand. Tourism growth, improved transport infrastructure, and visa liberalization stimulate demand for travel luggage. Asia Pacific offers the highest long-term growth potential, supported by urbanization, infrastructure investment, and middle-class expansion, sustaining market momentum through 2033 across key product categories.

Competitive Landscape

Business Strategies

Market-leading manufacturers employ integrated strategies emphasizing innovation, brand heritage storytelling, and omnichannel distribution excellence. Sustainability integration, technology-enabled product development, and direct-to-consumer investment dominate priorities. Differentiation relies on artisanal craftsmanship, exclusivity, and premium experiences. Emerging competitors leverage digital-native models, social commerce, and customization, while luxury houses blend heritage narratives with contemporary design to successfully engage younger, global consumers.

Strategic Developments

- In July 2024, Away Debuts Soft-Sided Luggage Collection – Away expanded its luggage portfolio with soft-sided offerings featuring consistent design elements, including smooth-rolling wheels and interior compression systems, diversifying its product range.

- In March 2024, Hermès opened an exclusive leather goods store in Mumbai – Hermès established India's first dedicated leather goods retail location, signifying strategic geographic expansion into rapidly expanding Asia Pacific luxury markets.

Companies Covered in Leather Luggage and Goods Market

- Louis Vuitton Malletier S.A.

- Hermès International S.A.

- LVMH Moët Hennessy

- Prada S.p.A.

- Gucci (Kering SA)

- Coach Inc.

- Samsonite International S.A.

- Delsey S.A.

- VIP Industries Limited

- Christian Dior SE

- Burberry Group Plc

- Fendi

- Tumi Holdings, Inc.

- Montblanc (Richemont Group)

- Michael Kors Holdings Ltd.

Frequently Asked Questions

The global Leather Luggage and Goods Market is projected at US$ 309.6 Billion in 2026 and anticipated to expand to US$ 468.3 Billion by 2033.

Primary drivers include escalating disposable income across emerging economies, unprecedented international tourism growth, e-commerce penetration acceleration, and technology-enabled product innovation, complemented by shifting consumer preferences toward premium, sustainable, and functionally-advanced products.

The market is projected to expand at 6.1% CAGR between 2026 and 2033.

Substantial opportunities exist in sustainable leather innovation, smart technology integration for premium positioning, emerging market geographic expansion particularly in Asia Pacific and Latin America, customization-driven product development, and direct-to-consumer platform expansion capturing digital-native consumer demographics.

Market leadership includes Louis Vuitton, Hermès, LVMH, Prada, Gucci, Coach, Samsonite, Delsey, VIP Industries, Christian Dior, Burberry, and Fendi, representing diversified positioning across luxury, accessible premium, and travel specialization categories with established global distribution networks.