- Clothing, Footwear, & Accessories

- Hunting Apparel Market

Hunting Apparel Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Hunting Apparel Market by Product Type (Jackets, Vests, Pants, Bibs, Gloves, and Others), End-user (Men, Women), By Sales Channel (Offline, and Online), and Regional Analysis for 2026 - 2033

Hunting Apparel Market Size and Trends Analysis

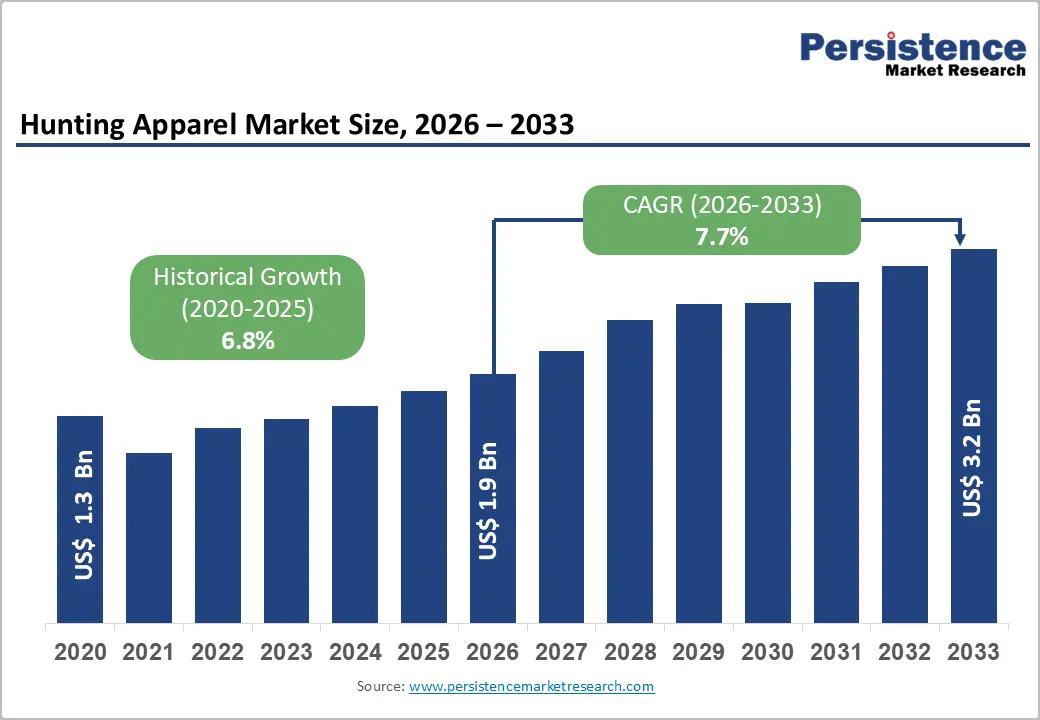

The global hunting apparel market size is likely to be valued at US$ 1.9 billion in 2026 and is expected to reach US$3.2 billion by 2033, reflecting a robust CAGR of 7.7% from 2026 to 2033. This acceleration in growth trajectory underscores strengthening market fundamentals driven by heightened participation in outdoor recreational activities, technological innovations in fabric engineering, and expanding consumer demographics.

Key Industry Highlights:

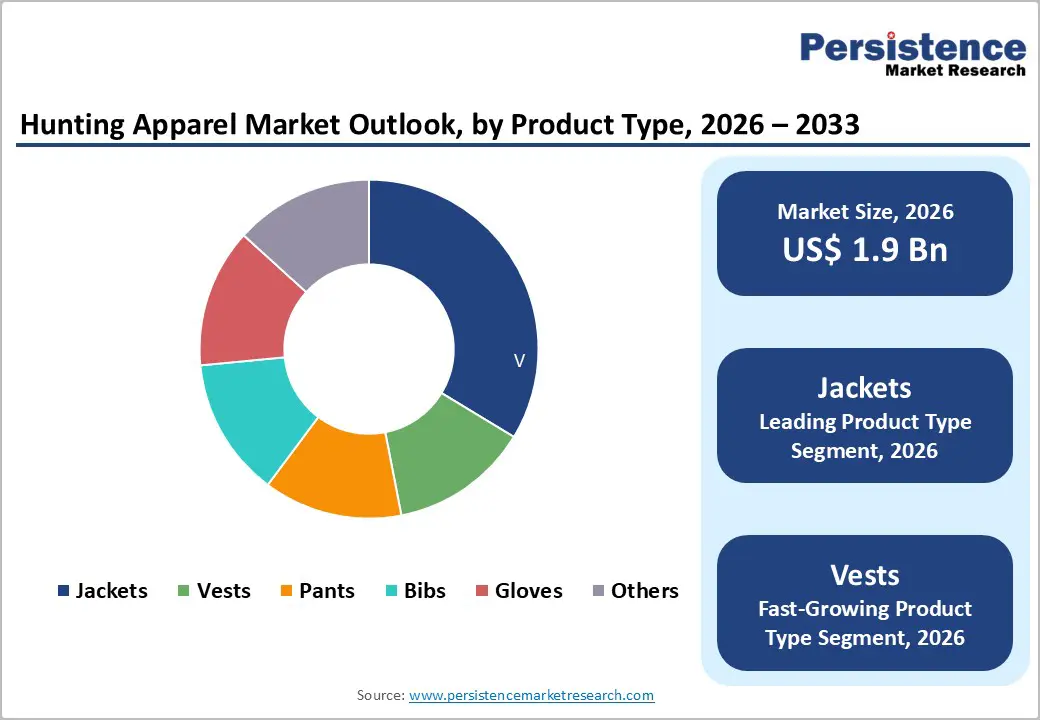

- Leading Product Type: Jackets command 38%+ revenue share as the dominant product category, while vests emerge as the fastest-growing segment, with 15-18% annual expansion driven by preferences for lightweight modular layering solutions.

- Leading End-user: Men's apparel maintains 75%+ market dominance, while women hunters are the fastest-growing end-user segment, with 25-30% annual expansion rates, establishing the highest-potential growth vector within the segmentation framework.

- Leading Sales Channel: Offline retail channels currently command 70%+ market share, while online sales channels demonstrate 18-22% annual growth rates, positioning e-commerce as the fastest-growing distribution segment with potential expansion to 40-45% of the market by 2033.

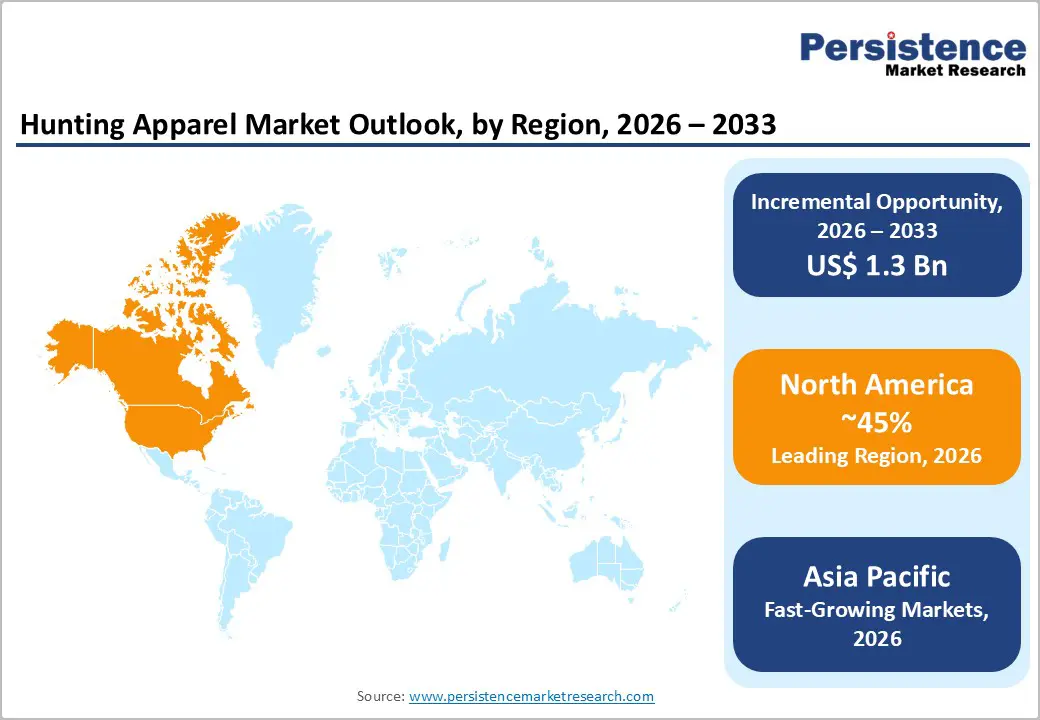

- Regional Analysis: North America dominates with 45%+ global revenue share, though Asia Pacific demonstrates the fastest regional growth with 9% projected CAGR reflecting emerging market expansion and middle-class demographic expansion.

- Strategic market developments emphasize the expansion of women's product lines, sustainability integration, and digital transformation, with major manufacturers launching dedicated women's collections, implementing eco-certification programs, and investing in DTC platforms.

| Key Insights | Details |

|---|---|

|

Hunting Apparel Market Size (2026E) |

US$ 1.9 Bn |

|

Market Value Forecast (2033F) |

US$ 3.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.8% |

Market Dynamics

Drivers - Rise in Outdoor Recreation Participation and Hunting Popularity

The global surge in outdoor recreational activities represents a primary market catalyst, with participation in hunting and related outdoor pursuits increasing substantially across developed and emerging markets. Industry data indicates that approximately 40% of outdoor enthusiasts actively participate in hunting-related activities at least seasonally, translating to expanding addressable market size. The International Association of Fish and Wildlife Agencies reports consistent growth in hunting license sales across North American jurisdictions, with particular momentum in states and provinces offering enhanced accessibility programs. This demographic expansion reflects broader lifestyle shifts emphasizing health, wellness, and nature-based recreation, particularly among younger consumer cohorts aged 25-45 years.

Market penetration in the Asia Pacific demonstrates accelerating adoption patterns, with hunting tourism emerging as a significant revenue contributor in countries including India, Indonesia, and parts of Southeast Asia. The convergence of rising disposable incomes, improved transportation infrastructure, and cultural normalization of hunting as a recreational pursuit directly correlates with an estimated 5.2% annual increase in hunting participation rates, creating proportional demand expansion for specialized apparel solutions.

Restraint - Pricing Pressure and Economic Sensitivity in Discretionary Consumer Segments

Hunting apparel pricing represents significant barrier to market penetration in emerging markets and price-sensitive consumer segments. Premium hunting jackets and specialized vests typically retail between US$150-400, positioning hunting apparel within discretionary expenditure categories vulnerable to economic downturns and income constraints. Emerging market consumers in the Asia Pacific demonstrate significant price sensitivity, with affordability constraints limiting the addressable market despite substantial population bases. The COVID-19 pandemic demonstrated pronounced market vulnerability, with discretionary spending on specialized outdoor apparel experiencing 18-22% contraction during economic uncertainty periods.

Middle-income consumer segments represent substantial untapped market potential, yet current product positioning and retail pricing structure effectively exclude large demographic cohorts. Manufacturing cost pressures, raw material volatility, and supply chain complexities create constraints on achieving cost structures compatible with emerging market price points while maintaining acceptable profitability margins. The proliferation of undifferentiated generic outdoor wear offerings from mass-market retailers creates competitive pressure reducing brand differentiation and pricing power, particularly in online distribution channels.

Opportunity - Sustainability Integration and Eco-Conscious Product Development

Consumer environmental consciousness is increasingly influencing purchasing decisions among outdoor recreation demographics, with approximately 60% of hunters believing brands should engage in conservation efforts. The shift toward sustainable materials, including recycled plastics, recycled cotton, organic fibers, and biodegradable synthetic alternatives, creates opportunities for differentiation and premium pricing. Current market data indicate that sustainable hunting apparel products command 15-25% price premiums and demonstrate 2-3x higher profit margins compared to conventional product lines.

The integration of circular economy principles including take-back programs, material recycling initiatives, and remanufacturing capabilities opens new revenue streams while strengthening brand positioning. Regulatory trends in Europe and North America increasingly mandate supply chain sustainability disclosure and environmental compliance certification, creating competitive advantages for early-adopting manufacturers establishing certifications, including B-Corp status, Bluesign® compliance, and Fair Trade certification. The convergence of hunter conservation values with environmental sustainability creates an authentic brand narrative alignment unavailable in many consumer categories.

Category-wise Analysis

Product Type Insights

Hunting jackets remain the leading product segment, commanding over 38% of total market revenue, underscoring their critical role in weather protection, camouflage performance, and all-season field usability. As essential upper-body gear, jackets provide durable weatherproofing, strategic insulation, and extensive storage capacity, making them indispensable across climates, terrains, and hunting styles. The category spans technical shells, insulated designs, and soft-shell variants, enabling hunters to adapt to temperature, wind, and precipitation shifts. Jackets also deliver the highest average selling prices (US$200–500) among apparel segments, resulting in disproportionately high revenue despite relatively similar unit volumes. Their mature design standards and consistent consumer expectations ensure stable category performance, while ongoing innovation in weight reduction, compressibility, and packability continues to enhance field efficiency and gear integration.

In contrast, hunting vests represent the fastest-growing segment, expanding at a notable 9.4% CAGR, fueled by rising demand for lightweight, mobile, and modular layering solutions. Vests offer targeted core protection without restricting arm movement, making them ideal for active hunting styles such as spot-and-stalk and upland pursuits. With accessible price points ranging from US$75 to US$200, vests attract newer hunters and buyers in developing markets. Product innovation spanning advanced insulation materials, breathable ventilation zones, safety-orange visibility, and optimized storage continues to accelerate adoption and broaden application versatility.

End-user Insights

Men remain the leading end-user segment in the hunting apparel market, commanding more than 75% of total revenue, supported by long-established participation rates and deeply ingrained purchasing behaviors. Male hunters have historically shaped the market’s product architecture, enabling decades of iterative design refinement focused on functional utility, durability, and performance optimization. This maturity results in extensive product availability, competitive pricing, and strong brand familiarity, reinforcing the segment’s sustained dominance even as demographics evolve. Traditional aesthetic preferences and consistent functional expectations further solidify men’s apparel as the foundation of overall market demand.

In contrast, women hunters represent the fastest-growing segment, expanding participation by 30–35% in recent years and projected to accelerate through 2033. Although women currently constitute only 15–20% of the total hunting population, their 40–50% higher per-capita spending on specialized apparel positions them as the market’s most attractive growth vector. Annual segment expansion of 25–30% reflects rising outdoor recreation adoption, broader empowerment trends, and substantial improvements in product availability. Manufacturers are responding with women-specific lines, advanced sizing systems, and targeted marketing addressing fit, comfort, and performance gaps. As penetration deepens, women’s hunting apparel is expected to deliver disproportionate future revenue contribution.

Sales Channel Insights

Offline channels remain the dominant revenue generator in the hunting apparel market, capturing over 70% of total sales. This leadership is driven by hunters’ strong preference for tactile product evaluation, in-store expert guidance, and immediate product availability factors especially important for technical gear selection. Specialty hunting retailers, sporting goods stores, and department stores maintain high customer loyalty through personalized recommendations, curated assortments, and trust built within local hunting communities. The widespread geographic distribution of hunting regions further reinforces offline accessibility advantages. Additionally, offline channels deliver higher profitability and stronger customer lifetime value, encouraging manufacturers to continue expanding brick-and-mortar partnerships and dedicated store footprints.

Conversely, online sales channels currently accounting for 25–30% of market revenue represent the fastest-growing segment, expanding at an annual rate of 9.5%, significantly outpacing offline growth. Younger consumer groups exhibit 2–3× higher online purchasing propensity, accelerating digital adoption. Enhanced platform capabilities such as augmented reality tools, virtual try-on features, and expert-curated product recommendations are reducing traditional e-commerce barriers for apparel categories. Direct-to-consumer digital models further improve margins and deepen brand engagement. With rapid digital transformation and improved logistics networks, online channels are projected to reach 40–45% of total market revenue by 2033, positioning them as the highest-growth distribution avenue.

Sales Channel Insights

Online retailing dominates the seamless mask market with more than 35% revenue share, establishing digital platforms as the leading commerce avenue. Consumers increasingly prefer e-commerce due to convenience, broad product variety, transparent pricing, and flexible delivery options. Direct-to-consumer models further strengthen manufacturers’ margin capture, reduce dependency on intermediaries, and build long-term customer loyalty. Digital engagement tools, social media marketing, influencer partnerships, and targeted advertising enhance brand visibility and efficiently reach core demographic groups. Consolidation around major marketplaces such as Amazon, Alibaba, and Flipkart provides massive reach but intensifies competition. Additionally, subscription-based replenishment and loyalty programs significantly improve retention and generate predictable recurring revenue.

Hypermarkets and supermarkets have emerged as the fastest-growing institutional sales channel, driven by consumers’ preference for one-stop convenience and the ability to physically evaluate products. These modern trade environments encourage impulse purchases and enable easy product comparison, supporting higher conversion rates. Their expansive geographic footprint across developed and emerging markets accelerates market penetration for Hunting Apparel. The rise of private-label programs and exclusive retail partnerships enables retailers to offer differentiated assortments with improved margins. Strong promotional capabilities, in-store visibility, and cross-merchandising further stimulate demand. Growth is particularly pronounced in the Asia Pacific, where rapid urbanization continues to expand modern retail infrastructure.

Regional Insights and Trends

North America’s Dominance Driven by Premium Spending, Regulations, and Rapid Women Hunter Growth

North America maintains clear leadership in the global hunting apparel market, capturing roughly 45% of worldwide revenue due to its large hunter base, premium spending patterns, and advanced retail ecosystem. The United States accounts for 85–90% of North American revenue, supported by 13+ million hunters and over $130 billion in annual hunting-related expenditure. This mature market grows through product innovation, premiumization, and demographic shifts rather than expanding participation. Canada contributes 8–10% of regional revenue, with growth around 6% CAGR, driven by demand for cold-weather gear and increasing participation among women hunters.

Technological enhancements, rapid women’s segment expansion (25–30% annual growth), and strong premium product adoption remain primary growth drivers. Mandatory high-visibility requirements under ANSI/ISEA 107 and CSA Z96 standards generate 8–12% of annual apparel volume, reinforcing structural demand. State and provincial Class 2/Class 3 visibility mandates further stimulate regulated purchasing.

North America also represents the most stringent regulatory and sustainability-driven region, influencing product design and supply chain decisions. The competitive landscape is defined by leading brands like Sitka Gear, KUIU, Carhartt, Browning, and Cabela’s, with the top 5–8 players controlling 40–50% of revenue and commanding 15–25% price premiums. Robust venture capital activity and 8–12% R&D spending underscore the region’s innovation intensity.

Asia Pacific’s Rapid Expansion Driving Global Hunting Apparel Market Growth Momentum

Asia Pacific has emerged as the fastest-growing regional market, currently accounting for 18–22% of global hunting apparel revenue, with its share expected to rise to 25–30% by 2033. The region spans mature markets such as Japan and Australia, rapidly expanding economies such as China and India, and developing regions across Southeast and South Asia. China leads with an expected growth of 8% CAGR, supported by a rising middle class, increased outdoor recreation, and expanding hunting tourism. India follows with 9% growth, driven by a middle-income population expected to exceed 250 million by 2030 and growing adoption of recreational hunting. Meanwhile, Japan and Australia show steady 5–8% growth, reflecting mature but premium-oriented markets.

The region’s growth is powered by expanding middle-income demographics, higher leisure spending, and increasing participation in outdoor activities. With an estimated 500+ million potential hunters, the Asia Pacific remain significantly underpenetrated in specialized apparel use. Rising sustainability awareness, prioritized by 45–55% of younger consumers, further shapes demand. Additionally, competitive manufacturing costs and strong supply chain networks enable cost-effective production and strategic pricing for market penetration.

Competitive Landscape

The global hunting apparel market demonstrates a moderately consolidated structure with significant competitive diversity, enabling multiple success strategies. The market exhibits characteristics of medium-concentration markets, with the top 5-8 brands controlling approximately 40-50% of total revenue, while the remaining market share is distributed among 50+ specialized and regional competitors. This structure contrasts with highly consolidated consumer product markets, providing substantial opportunity for specialized competitors with differentiated value propositions.

Leading market participants include established heritage brands (Sitka Gear, KUIU, Carhartt, Browning, Cabela's, Columbia Sportswear), specialty-focused manufacturers (Kryptek, Mossy Oak, ScentLok), and emerging direct-to-consumer brands capturing incremental market share through digital innovation and targeted positioning. The competitive positioning spectrum ranges from low-cost mass-market providers competing on affordability to premium-positioned heritage brands emphasizing craftsmanship, performance, and innovation. Market fragmentation reflects diverse consumer segments with varying priorities, including price sensitivity, performance requirements, aesthetic preferences, and values-based positioning around sustainability and conservation.

Key Industry Developments:

- In 2022, KUIU, a leading manufacturer of high-performance hunting gear, announced the launch of its first dedicated line of performance hunting apparel for women. The collection delivers advanced functionality, exceptional durability, and technical innovation, setting a new benchmark for women’s hunting gear. Each piece is offered in KUIU’s signature Valo, Verde, and Vias camouflage patterns and incorporates the same cutting-edge technologies used in the brand’s men’s apparel.

Companies Covered in Hunting Apparel Market

- Sitka Gear

- Kuiu

- First Lite

- Under Armour Hunt

- Browning Clothing

- Kryptek Outdoor Group

- Mossy Oak

- Realtree

- Pnuma Outdoors

- Härkila

- Other Market Players

Frequently Asked Questions

The Hunting Apparel market is estimated to be valued at US$ 1.9 Bn in 2026.

Growing participation in recreational hunting, rising outdoor sports culture, and increasing demand for high-performance, durable, and weather-resistant technical hunting clothing.

In 2026, the North America region will dominate the market with an exceeding 45% revenue share in the global Hunting Apparel market.

Among product types, Jackets have the highest preference, capturing beyond 38% of the market revenue share in 2026, surpassing other product types.

Sitka Gear, Kuiu, First Lite, Under Armour Hunt, Browning Clothing, Kryptek Outdoor Group are a few leading players in the Hunting Apparel market.