- Medical Devices

- Gastric Electrical Stimulators Market

Gastric Electrical Stimulators Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Gastric Electrical Stimulators Market by Type (High Frequency and Low Frequency), by Application (Gastroparesis, Obesity, Chronic Nausea, and Others), End-user (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Others), and Regional Analysis from 2026 to 2033

Gastric Electrical Stimulators Market Share and Trends Analysis

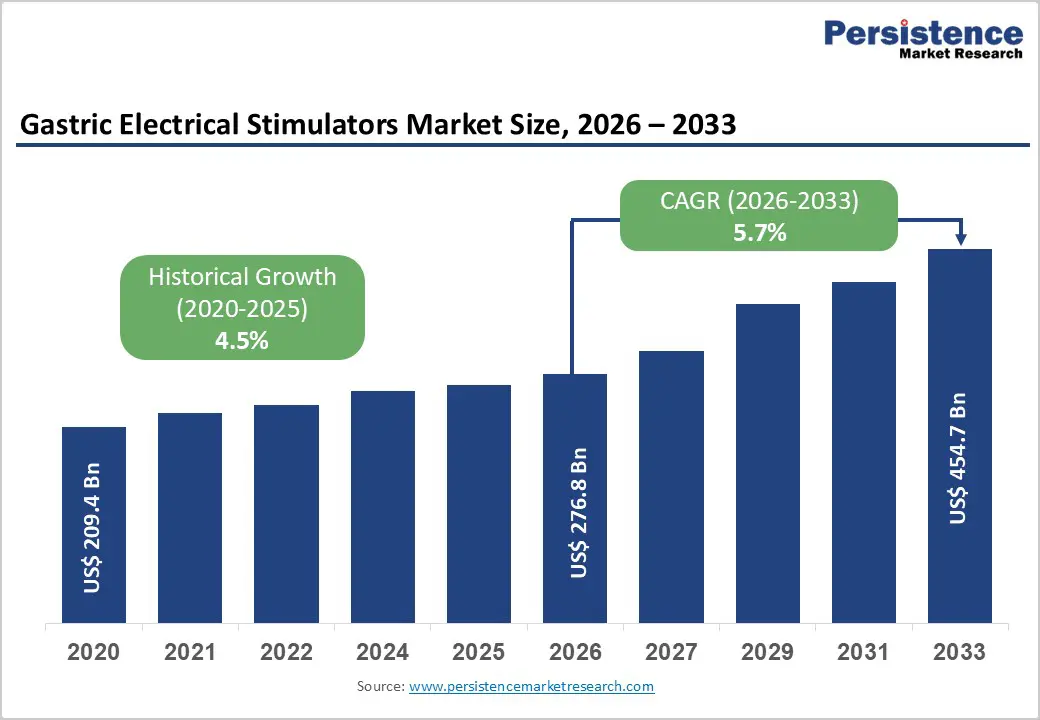

The global gastric electrical stimulators market size is estimated to grow from US$ 276.8 million in 2026 to US$ 454.7 million by 2033 growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

Global demand for gastric electrical stimulators is increasing steadily, driven by the rising prevalence of gastroparesis and other gastric motility disorders, particularly among diabetic, post-surgical, and neurologically affected patient populations. Growing awareness of gastrointestinal health as a critical component of overall quality of life is supporting wider adoption of advanced therapeutic solutions. Lifestyle changes, increasing diabetes incidence, obesity, aging populations, and improved diagnostic rates are contributing to a larger addressable patient pool, sustaining long-term market growth.

Limited efficacy and side effects associated with conventional pharmacological therapies are accelerating the shift toward non-pharmacological, device-based gastric neuromodulation. Increasing preference for long-term symptom management solutions with consistent clinical outcomes is strengthening adoption across hospitals and specialty care settings. Rising healthcare expenditure, improved access to advanced gastrointestinal procedures, and expanding physician awareness further reinforce market expansion. Continuous innovation in implantable device design, stimulation algorithms, battery longevity, and therapy personalization is improving treatment effectiveness and patient outcomes. Additionally, growing focus on chronic disease management, minimally invasive interventions, and expansion of advanced gastroenterology services are propelling the global gastric electrical stimulators market.

Key Industry Highlights:

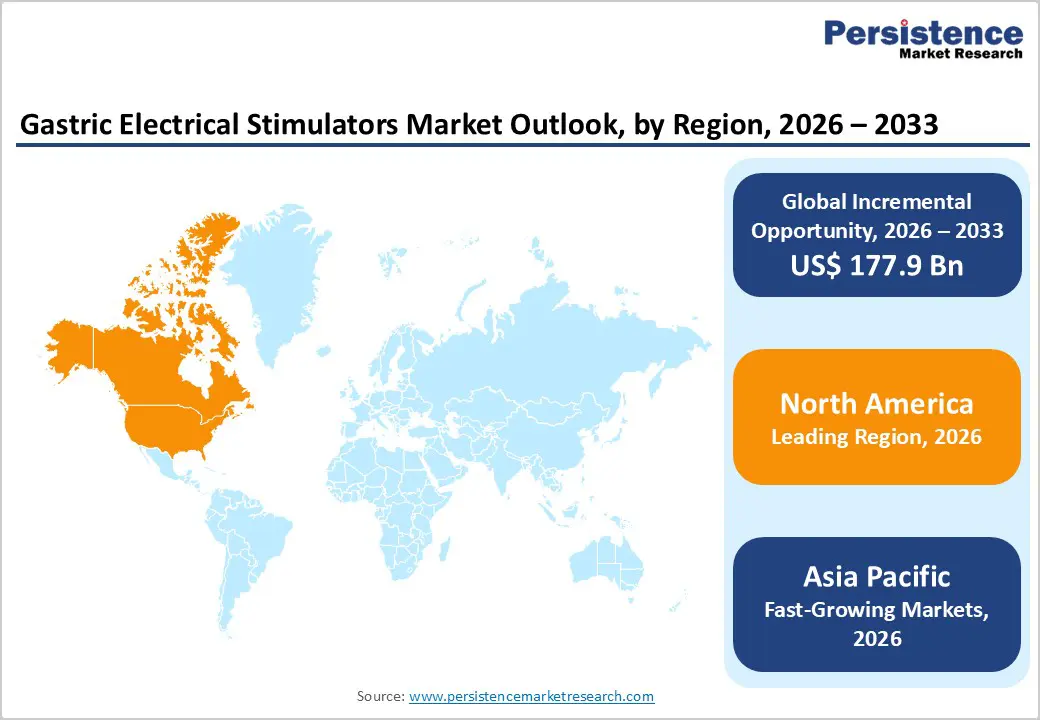

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high prevalence of diabetes-related gastroparesis, strong physician awareness, favorable reimbursement frameworks, and widespread availability of specialized gastroenterology and surgical centers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large patient base, rising incidence of diabetes and obesity, improving healthcare infrastructure, increasing access to advanced gastrointestinal treatments, and growing awareness of neuromodulation-based therapies.

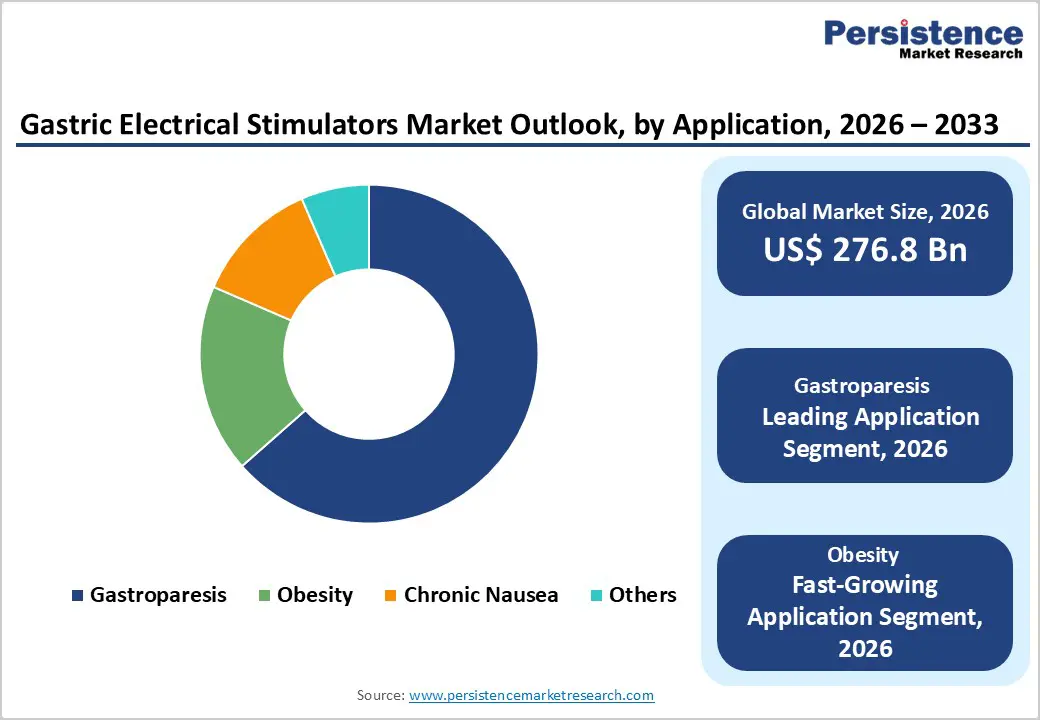

- Leading Application Segment: Gastroparesis dominates the market due to its high global prevalence, significant unmet clinical need, limited effectiveness of drug therapies, and increasing adoption of gastric electrical stimulation for long-term symptom control.

- Fastest-Growing Application Segment: Obesity is expanding rapidly as interest grows in neuromodulation-based approaches that support appetite regulation, weight management, and improved metabolic outcomes.

- Leading End-user Segment: Hospitals remain the top segment, driven by surgical implantation requirements, availability of advanced diagnostic capabilities, multidisciplinary expertise, and high patient volumes for complex gastric disorders.

- Fastest-Growing End-user Segment: Specialty clinics are scaling quickly as focused gastroenterology centers expand, offering targeted, minimally invasive gastric stimulation therapies with improved patient access and follow-up care.

| Key Insights | Details |

|---|---|

| Gastric Electrical Stimulators Market Size (2026E) | US$ 276.8 Mn |

| Market Value Forecast (2033F) | US$ 454.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Dynamics

Driver – Growing Prevalence of Gastroparesis and Shift Toward Device-Based Neuromodulation

The increasing incidence of gastroparesis and other gastric motility disorders is a primary factor supporting sustained market expansion. Rising diabetes prevalence, post-surgical complications, neurological disorders, and idiopathic gastric dysfunction have significantly increased the population suffering from chronic nausea, vomiting, bloating, and delayed gastric emptying. Conventional pharmacological therapies often provide limited or inconsistent relief and are associated with long-term side effects, leading clinicians to seek alternative treatment approaches. This has accelerated the adoption of gastric electrical stimulation as a non-pharmacological, long-term symptom management solution for refractory patients.

Advancements in neuromodulation technology are further strengthening adoption. Improvements in implantable device reliability, stimulation precision, battery longevity, and programmability allow for more personalized and effective therapy. Growing clinical evidence demonstrating symptom reduction and quality-of-life improvement is increasing physician confidence. Additionally, expanding awareness among gastroenterologists and surgeons, along with inclusion of gastric electrical stimulation in advanced treatment pathways, is driving procedural volumes. Increasing focus on chronic disease management and long-term gastrointestinal care continues to position device-based gastric stimulation as a critical therapeutic option.

Restraints – High Procedure Costs, Limited Awareness, and Reimbursement Challenges

Market growth is constrained by several clinical, economic, and systemic barriers. One of the primary limitations is the high overall cost associated with gastric electrical stimulation therapy, including device pricing, surgical implantation, follow-up programming, and long-term monitoring. These costs can restrict access, particularly in price-sensitive and emerging healthcare markets. In addition, reimbursement policies remain inconsistent across regions, with limited coverage in certain countries, slowing adoption despite clinical need.

Another challenge is limited awareness and familiarity among general practitioners and non-specialist clinicians, which can delay diagnosis and referral of eligible patients. Gastric motility disorders are often underdiagnosed or misattributed to functional gastrointestinal conditions, reducing the pool of patients considered for advanced therapies. Procedural complexity and the need for specialized surgical expertise further limit availability outside tertiary care centers. Concerns related to device-related complications, variable patient response, and the need for ongoing device management may also deter adoption. In developing regions, gaps in healthcare infrastructure, lack of trained specialists, and limited access to advanced diagnostic tools continue to restrain broader market penetration.

Opportunity – Expansion into Emerging Markets and Advancements in Next-Generation Stimulation Systems

Significant growth opportunities exist through geographic expansion and technological innovation. Emerging economies across Asia Pacific, Latin America, and the Middle East present substantial untapped potential due to rising diabetes incidence, improving healthcare infrastructure, and increasing awareness of advanced gastrointestinal therapies. Expansion of private hospitals and specialty gastroenterology centers is improving access to surgical interventions, supporting wider adoption.

Technological advancements also create strong future opportunities. Development of next-generation gastric electrical stimulators with enhanced programmability, longer battery life, smaller form factors, and minimally invasive implantation techniques is expected to improve patient outcomes and procedural efficiency. Integration of digital platforms for remote monitoring and therapy optimization can further enhance long-term disease management. Manufacturers also have opportunities to expand indications beyond gastroparesis into obesity management and functional gastric disorders as clinical evidence evolves. Strategic collaborations with hospitals, research institutions, and reimbursement authorities, along with localized manufacturing to reduce costs, are expected to unlock sustained growth potential over the forecast period.

Category-wise Analysis

By Product Insights

High-frequency gastric electrical stimulators are projected to dominate the global gastric electrical stimulators market in 2026, accounting for a revenue share of 65.0%. This leadership is primarily driven by their established clinical effectiveness in managing refractory gastroparesis, particularly in reducing chronic nausea and vomiting. High-frequency stimulation protocols are widely supported by clinical evidence and physician familiarity, making them the preferred choice in hospital and specialty care settings. These systems enable consistent neuromodulation of gastric motility with programmable parameters that support personalized therapy optimization. Their compatibility with implantable platforms, longer device lifespan, and improving battery technologies further strengthen adoption. Additionally, regulatory approvals in key markets and inclusion in treatment guidelines support wider clinical use. As device manufacturers continue to refine stimulation algorithms and enhance long-term reliability, high-frequency gastric electrical stimulators remain the leading product segment globally.

By Application Insights

The gastroparesis segment is projected to dominate the global gastric electrical stimulators market in 2026, capturing a revenue share of 63.5%. This dominance is driven by the rising prevalence of diabetic and idiopathic gastroparesis and the limited effectiveness of conventional pharmacological treatments. Gastric electrical stimulation is increasingly adopted for patients with refractory symptoms, particularly chronic nausea, vomiting, and delayed gastric emptying. Growing awareness among gastroenterologists regarding neuromodulation-based therapies has accelerated clinical adoption. The increasing burden of diabetes globally further expands the patient pool, especially in developed and emerging economies. Hospitals and specialty clinics increasingly recommend gastric electrical stimulators as an adjunct or alternative when drug therapies fail. Long-term symptom management requirements and improving clinical outcomes continue to reinforce gastroparesis as the leading application segment in the global market.

By End-user Insights

Hospitals are expected to dominate the global gastric electrical stimulators market in 2026, accounting for a revenue share of 45.0%. This leadership is attributed to hospitals being the primary centers for surgical implantation, post-operative care, and long-term management of gastric electrical stimulation therapy. Hospitals manage a high volume of complex gastroparesis and obesity-related gastrointestinal cases that require multidisciplinary expertise, including gastroenterologists, surgeons, and neurologists. Availability of advanced diagnostic tools, such as gastric emptying studies and motility testing, supports appropriate patient selection. Hospitals also benefit from reimbursement-backed procedures, structured clinical protocols, and higher patient trust for implantable therapies. As gastric electrical stimulation increasingly integrates into advanced gastrointestinal care pathways, hospitals continue to remain the dominant end-user segment globally.

Region-wise Insights

North America Gastric Electrical Stimulators Market Trends

North America is expected to dominate the global gastric electrical stimulators market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a highly developed healthcare infrastructure, strong clinical awareness of gastroparesis, and early adoption of implantable neuromodulation technologies. High prevalence of diabetes and obesity significantly contributes to gastroparesis incidence, driving sustained demand for gastric electrical stimulation therapies. Favorable reimbursement policies for implantable devices and surgical procedures further support market penetration.

The presence of leading manufacturers, ongoing clinical trials, and continuous product innovation strengthens regional leadership. Academic medical centers and specialty hospitals actively participate in advancing gastric neuromodulation research, accelerating therapy acceptance. Additionally, strong physician training programs and patient advocacy efforts enhance diagnosis rates. As focus on chronic gastrointestinal disorder management increases, North America continues to maintain a dominant position in the global gastric electrical stimulators market.

Europe Gastric Electrical Stimulators Market Trends

Europe gastric electrical stimulators market is expected to grow steadily, supported by increasing diagnoses of gastrointestinal motility disorders and an expanding aging population across countries such as Germany, the U.K., France, Italy, and Spain. Strong public healthcare systems enable access to advanced diagnostic and surgical treatments for gastroparesis and obesity-related gastric dysfunction. European clinicians increasingly recognize gastric electrical stimulation as a viable option for refractory cases, particularly where pharmacological therapies show limited efficacy.

Regulatory frameworks emphasizing clinical validation, device safety, and post-market surveillance strengthen physician and patient confidence. Growth is further supported by rising diabetes prevalence, improved referral pathways, and integration of neuromodulation therapies into tertiary care centers. Increasing healthcare digitalization and cross-border clinical research collaborations also support adoption. Overall, Europe is expected to demonstrate stable, long-term growth in the gastric electrical stimulators market.

Asia Pacific Gastric Electrical Stimulators Market Trends

The Asia Pacific gastric electrical stimulators market is expected to register a relatively higher CAGR of around 7.5% between 2026 and 2033, driven by rapid healthcare infrastructure development and a large, increasingly diagnosed patient population. Countries such as China, India, Japan, South Korea, and Australia are witnessing rising prevalence of diabetes, obesity, and functional gastrointestinal disorders due to urbanization and lifestyle changes. Improving access to advanced gastroenterology care, expansion of private hospitals, and growth of specialty clinics are accelerating adoption of gastric electrical stimulation therapies. Increasing physician awareness, supported by international guidelines and training programs, is improving diagnosis and treatment rates.

Government investments in healthcare modernization and medical device manufacturing further support market expansion. Additionally, cost-effective device production and strategic entry by global players enhance affordability, positioning the Asia Pacific as the fastest-growing regional market globally.

Competitive Landscape

The global gastric electrical stimulators market is highly competitive, with strong participation from companies such as Medtronic, Koninklijke Philips N.V., Enterra Medical, Inc., IntraPace, Inc., and ReShape Lifesciences, Inc. These players leverage established global distribution networks, strong brand recognition, and diversified medical device and digital health portfolios to address the rising demand for non-pharmacological treatment of gastroparesis, obesity, and other gastric motility disorders.

Their offerings focus on advancements in stimulation precision, implantable device reliability, battery longevity, minimally invasive implantation techniques, therapy effectiveness, patient safety, and ease of long-term management, supporting adoption across hospitals, specialty clinics, and ambulatory surgical centers. Continuous product innovation, regulatory compliance, and adherence to international quality standards remain critical to sustaining competitive positioning in the global gastric electrical stimulators market.

Key Industry Developments:

- In January 2026, Enterra Medical, Inc. announced the launch of Enterra ReliaStim, a next-generation stimulation lead developed to enhance the precision, consistency, and efficiency of Gastric Electrical Stimulation (GES) lead placement. Designed and manufactured in-house, Enterra ReliaStim underscores the company’s continued commitment to advancing GES technology. The new lead represents a meaningful step in Enterra Medical’s strategic evolution from a single-therapy provider toward a broader platform of innovative solutions aimed at improving care for patients suffering from chronic nausea and vomiting.

- In April 2025, Good Samaritan Medical Center raised awareness for Gastroparesis Awareness Month, highlighting an advanced treatment option available for patients living with this often-debilitating condition, with a focus on improving symptom control and overall quality of life through innovative gastric electrical stimulation therapy.

- In April 2023, researchers at NYU Abu Dhabi developed a first-of-its-kind ingestible electroceutical capsule designed to non-invasively modulate the gut–brain axis. Developed in collaboration with MIT researchers, including Prof. Giovanni Traverso, the device enables precise neuromodulation to influence hunger signaling and shows potential for treating metabolic and neurological disorders.

Companies Covered in Gastric Electrical Stimulators Market

- Medtronic

- Koninklijke Philips N.V.,

- Enterra Medical, Inc.

- IntraPace, Inc.

- ReShape Lifesciences, Inc.

- EnteroMedics Inc.

- Rishena Co., Ltd.

- Stryker

- Abbott

- Nevro Corp

- Synapse Biomedical, Inc

Frequently Asked Questions

The global gastric electrical stimulators market is projected to be valued at US$ 276.8 Mn in 2026.

Rising prevalence of gastroparesis and obesity, coupled with increasing adoption of minimally invasive neuromodulation therapies.

The global gastric electrical stimulators market is poised to witness a CAGR of 5.7% between 2026 and 2033.

Expansion of gastric electrical stimulators into obesity management and emerging markets supported by advancing device technologies.

Medtronic, Koninklijke Philips N.V., Enterra Medical, Inc., IntraPace, Inc., and ReShape Lifesciences, Inc. are some of the key players in the gastric electrical stimulators market.