- Automotive

- Forestry Trailers Market

Forestry Trailers Market Size, Share, and Growth Forecast 2026 - 2033

Forestry Trailers Market by Product Type (Log Trailers, Grapple Trailers, Forwarder Trailers, Multipurpose Trailers), by Trailer Capacity (Below 5 Tons, 5–10 Tons, 10–20 Tons, 20–30 Tons, Above 30 Tons), by Application (Logging & Timber Extraction, Biomass & Wood Chip Transport, Forest Management, Firewood Transport, Pulpwood Operations), End-user, and Regional Analysis, 20262033

Forestry Trailers Market Size and Trend Analysis

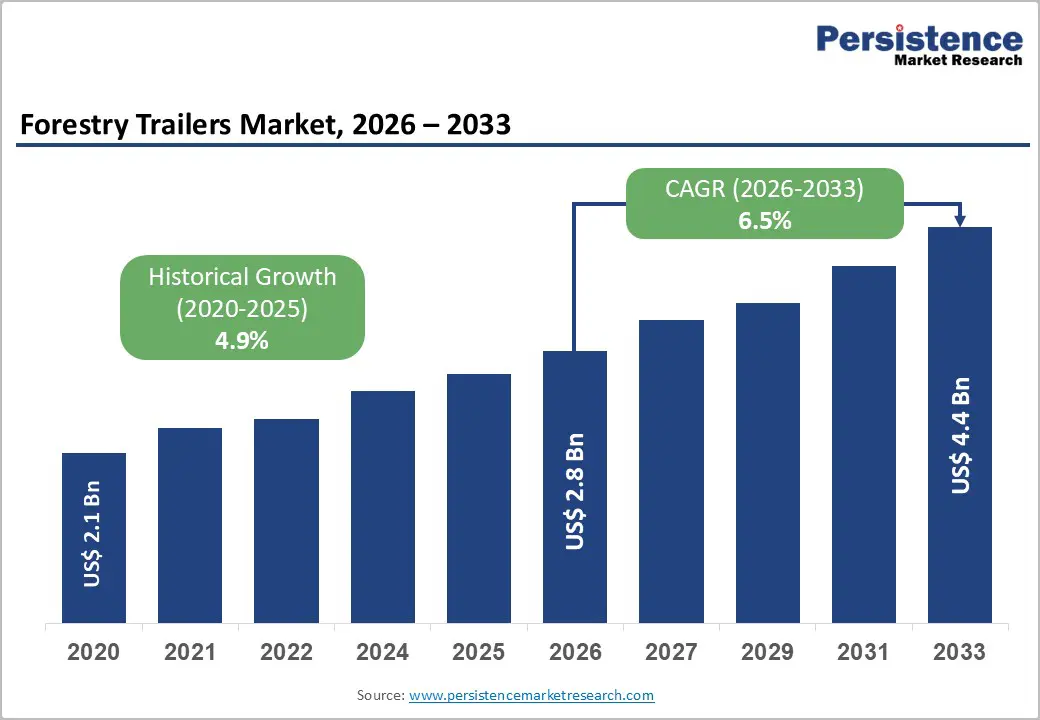

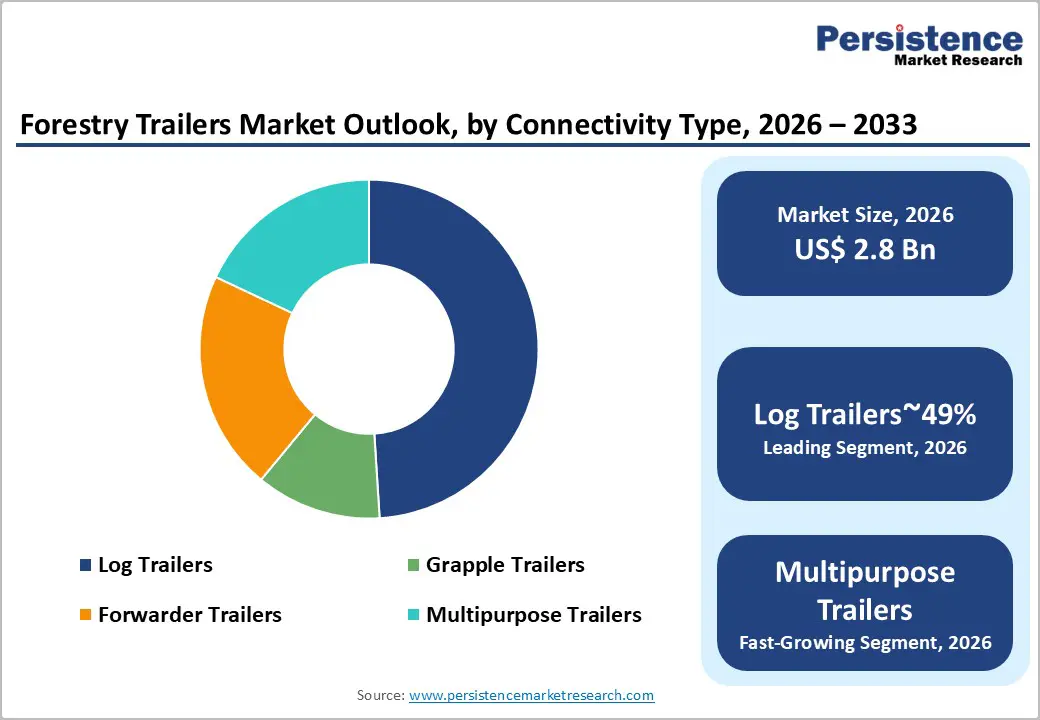

The global forestry trailers market size is likely to be valued at US$ 2.8 billion in 2026 and is expected to reach US$ 4.4 billion by 2033, growing at a CAGR of 6.5% during the forecast period from 2026 and 2033. The Forestry Trailers Market is expanding at an accelerated pace due to the convergence of rising global timber demand, the mechanization of logging operations, and government mandates promoting sustainable forest management.

Key Industry Highlights:

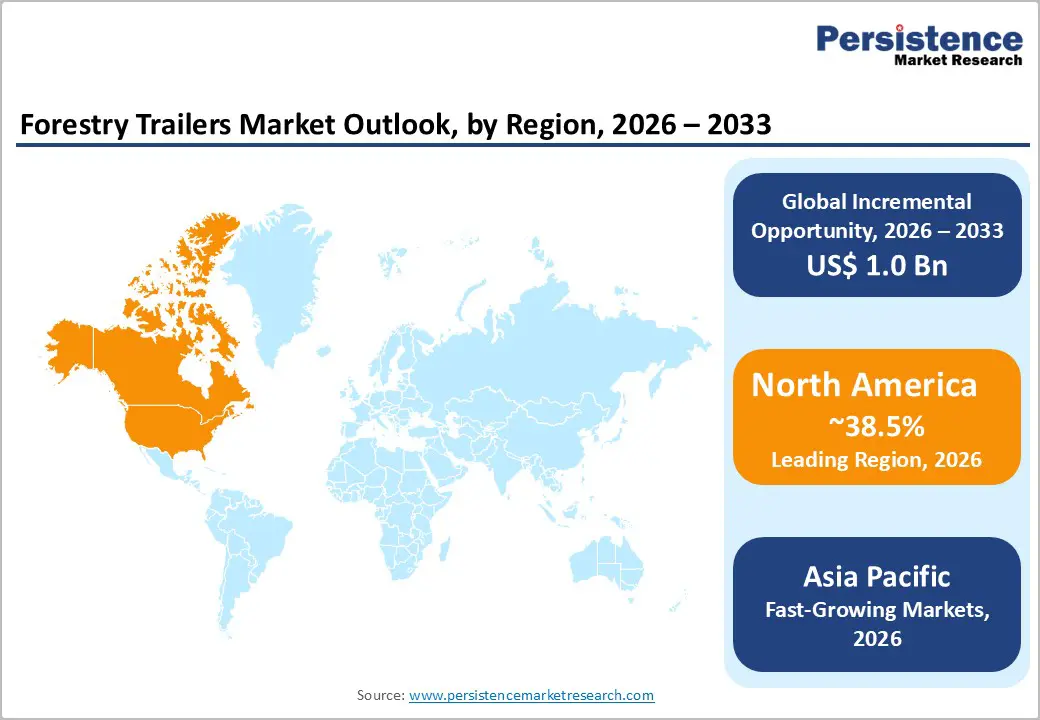

- Leading Region: North America maintains dominant market position commanding 38.5% global market share through extensive forest resources, mature logging industries, and advanced manufacturing infrastructure, with United States specifically accounting for 21.4% global share driven by large-scale commercial operations and government support programs including EQIP funding providing US$ 125 million in 2024.

- Fastest-Growing Region: Asia Pacific emerges as the fastest-growing region expanding at 7-8% CAGR through 2033, driven by mechanization of forestry operations across China, India, and ASEAN countries, with Asia Pacific Forestry Equipment Market projected to expand from US$ 2.24 Billion in 2025 to US$ 3.34 Billion by 2033.

- Leading Segment: Log Trailers maintain market dominance with 49% market share, with tandem-axle configurations representing 45% of this segment through superior weight distribution, enhanced stability on uneven terrain, and reduced environmental impact supporting forest ecosystem preservation.

- Fastest-Growing Segment: Biomass & Wood Chip Transport emerges as the fastest-growing application segment driven by accelerating renewable energy deployment and industrial bioenergy demand, with specialized trailers commanding premium pricing through integrated loading mechanisms and enclosed designs optimizing transport efficiency.

- Key Opportunity: Hybrid-electric forestry trailer technologies represent transformative market opportunity, with FPInnovations demonstrating 12% fuel savings and Nordic countries targeting 50% electric forest trucks by 2030, creating premium-pricing opportunities for manufacturers advancing electrification capabilities ahead of anticipated regulatory mandates.

| Key Insights | Details |

|---|---|

| Forestry Trailers Market Size (2026E) | US$ 2.8 Billion |

| Market Value Forecast (2033F) | US$ 4.4 Billion |

| Projected Growth CAGR(2026-2033) | 6.5% |

| Historical Market Growth (2020-2025) | 4.9% |

Market Dynamics

Drivers - Rising global timber consumption, urban infrastructure expansion, and government mechanization programs are accelerating demand for efficient forestry transportation solutions

The global timber industry is witnessing strong and sustained growth, supported by rising demand from the construction, packaging, and paper industries. According to the Food and Agriculture Organization (FAO), industrial roundwood removals reached 1.92 billion cubic meters in 2023, highlighting the expanding scale of timber production worldwide. Rapid urbanization and infrastructure development across the Asia Pacific, Latin America, and Africa are significantly increasing the consumption of forest-based materials. This expansion directly strengthens the need for efficient and reliable timber transportation systems, positioning forestry trailers as essential operational assets.

Recovery in residential and commercial real estate continues to support demand for sawnwood and structural timber products. Brazil’s eucalyptus plantation sector, holding nearly 6.9% of global share, plays a major role in the international timber trade, driving consistent cross-border transport volumes. Additionally, government-backed infrastructure and mechanization programs further stimulate equipment adoption. For example, India’s Sub-Mission on Agricultural Mechanization distributed more than 1.5 million machines between 2020 and 2023, reinforcing strong institutional support for mechanized logistics solutions.

Labor shortages and strict environmental regulations are driving rapid adoption of mechanized, low-impact, and sustainability-compliant forestry trailers

Labor shortages across key forestry regions are accelerating the shift from manual logging to mechanized operations. International studies indicate rural labor participation in Southeast Asia has declined by nearly 12% over the past decade, creating operational pressure for forestry companies. As a result, operators increasingly rely on modern forestry trailers equipped with hydraulic loading systems, advanced suspension, and load monitoring technologies to improve productivity while reducing manpower dependence.

At the same time, tightening environmental regulations are reshaping equipment procurement strategies. European Union climate targets aiming for a 55% reduction in net emissions by 2030 are encouraging investments in low-impact forestry machinery. Certification programs such as FSC and PEFC require equipment that supports selective harvesting and minimizes soil damage, further boosting demand for modern trailer designs. Additionally, the steady growth of biomass-based energy production is increasing the need for specialized trailers capable of transporting wood chips and forest residues efficiently to energy facilities.

Restraints - High equipment costs, long replacement cycles, and rising material prices limit forestry trailer adoption among small and mid-sized operators

Forestry trailers involve significant capital expenditure, particularly advanced models integrated with cranes, grapples, and complex hydraulic systems. In many cases, equipment prices exceed US$ 500,000, creating affordability challenges for small and medium-sized logging contractors and private forest owners. This high upfront investment limits adoption in price-sensitive regions and slows market penetration. Financing constraints and long replacement cycles further restrict market growth, as forestry trailers are built for durability and extended usage.

Rising raw material costs, including steel, hydraulic components, and electronic systems, have increased manufacturing expenses and final product pricing. At the same time, lingering supply chain disruptions from post-pandemic recovery periods continue to affect component availability and production timelines. These factors collectively place pressure on both manufacturers and buyers, reducing purchasing flexibility. Seasonal forestry operations also make timely equipment acquisition critical, and cost uncertainty discourages many operators from upgrading fleets, thereby moderating overall market expansion.

Poor road connectivity, remote forest locations, and limited service infrastructure restrict mechanized forestry equipment deployment in developing regions

Limited infrastructure in emerging forestry regions remains a major challenge for market development. In areas such as Sub-Saharan Africa, parts of Southeast Asia, and remote Latin American forests, inadequate road networks restrict access for heavy equipment. Many logging sites lack proper service centers, maintenance facilities, fuel supply systems, and trained technical support, reducing equipment utilization efficiency. These constraints force operators to confine mechanized operations to accessible zones, limiting broader trailer deployment.

Diverse terrain conditions, including steep slopes, soft soils, and dense forest coverage demand highly specialized equipment designs. Meeting these operational requirements increases engineering complexity and manufacturing costs. As a result, equipment prices rise further, restricting adoption among budget-conscious operators. Geographic remoteness also increases downtime during breakdowns, making investment riskier for small contractors. Collectively, infrastructure gaps and environmental constraints continue to limit market accessibility and slow mechanization progress in developing forestry economies.

Opportunities - Growing emission regulations and fuel efficiency needs are creating strong opportunities for electric and hybrid-powered forestry trailer solutions

The emergence of electric and hybrid forestry trailers represents a major growth opportunity as sustainability becomes a strategic priority. Research conducted by FPInnovations in Canada has demonstrated hybrid-electric trailer prototypes delivering fuel savings of up to 12% and reducing annual carbon emissions by nearly 23 tonnes per unit. Peak efficiency improvements of more than 17% on uphill routes highlight strong performance benefits. These developments are supported by over US$ 1.8 million in funding from Natural Resources Canada’s Clean Growth Program, validating commercial feasibility.

Nordic countries, particularly Sweden, are actively promoting electrification, targeting 50% adoption of electric forest transport vehicles by 2030 through national and EU-backed funding programs. Manufacturers integrating electric axles, regenerative braking, and battery-assisted systems into trailer platforms can command premium pricing while preparing for future emission regulations. These technologies also reduce brake wear and fuel costs, strengthening the long-term economic case for electrified forestry equipment.

Digital connectivity adoption and rapid biomass energy expansion are opening new high-value application segments for advanced forestry trailers

Digitalization is creating new value opportunities within the forestry trailers market through integration of Internet of Things (IoT) technologies. Connectivity-enabled trailers offering GPS tracking, load monitoring, predictive maintenance, and performance analytics are increasingly preferred by operators seeking cost optimization. Telematics systems improve fleet utilization, enhance safety, and reduce unplanned downtime, making them attractive for large-scale logging operations.

Precision technology adoption across Asia Pacific has grown by more than 25% over the past five years, creating a strong foundation for digitally integrated forestry equipment. Simultaneously, expansion of the biomass energy sector is opening new demand channels. Growing renewable energy targets are increasing the need for specialized wood chip and residue transport trailers. Enclosed biomass trailers with automated loading systems command higher margins and serve dedicated energy supply chains. Manufacturers offering modular designs compatible with both timber and biomass applications can access multiple revenue streams while improving production efficiency.

Category-wise Analysis

Product Type Insights

The log trailers segment continues to dominate the market, accounting for approximately 49% share due to its simplicity, affordability, and broad usability across forestry operations. Standard log haulers without onboard cranes remain particularly attractive to small and mid-sized operators aiming to reduce capital investment and operational complexity. Their simple structural design enables faster regulatory approvals and easier deployment across regions. Within this category, tandem-axle configurations represent nearly 45% market share, driven by improved weight distribution, enhanced stability on uneven forest terrain, and lower ground pressure.

These features support environmental compliance while reducing tire wear and maintenance expenses. Compared to heavier alternatives, tandem-axle designs deliver better fuel efficiency and longer service life. The sustained dominance of log hauler trailers reflects the industry’s preference for cost-effective and flexible equipment solutions. Operators continue to prioritize reliability and operational adaptability over integrated harvesting systems, particularly in regions where mechanization is still evolving.

Trailer Capacity Insights

Medium-capacity forestry trailers ranging between 5 and 10 tons are witnessing strong demand growth, capturing approximately 35% market share. These trailers offer an effective balance between payload capacity and manoeuvrability, making them suitable for complex forest environments with limited access routes. Operators increasingly favor this capacity range as it allows efficient transportation without the operational constraints associated with heavy-duty trailers. Medium-capacity designs support diverse applications, including thinning operations, selective logging, and secondary timber transport.

Regulatory advantages also support adoption, as many regions impose fewer road permit restrictions for mid-range loads. This flexibility allows more frequent deployment and reduced compliance costs. For emerging markets transitioning from manual to mechanized forestry, these trailers present an affordable entry point with manageable investment risk. Manufacturers focusing on this segment benefit from consistent demand driven by versatility, lower ownership costs, and strong suitability for mixed-terrain forestry operations.

Application Insights

Logging and timber extraction remain the primary application segment, accounting for nearly 60% of overall market demand. This dominance is supported by global industrial roundwood removals of 1.92 billion cubic meters recorded in 2023, reflecting sustained harvesting activity worldwide. The segment includes large-scale commercial logging as well as selective harvesting under certified forest management systems. Continued demand from construction and paper industries supports stable sawnwood trade volumes exceeding 129 million cubic meters annually. In parallel, the biomass and wood chip transport segment is emerging as the fastest-growing application area.

Rising renewable energy investments are increasing demand for specialized trailers designed for bulk biomass movement. Enclosed structures and automated loading systems improve transport efficiency and reduce material loss. Additional applications such as forest management, firewood transport, and pulpwood logistics are further diversifying revenue opportunities for manufacturers offering adaptable trailer platforms.

End-user Insights

Logging companies represent the largest end-user segment, holding approximately 55% market share. This group includes large integrated timber producers and independent contractors operating across diverse geographies. These users prioritize equipment durability, load efficiency, and total cost of ownership, driving demand for trailers equipped with telematics, reinforced frames, and optimized hydraulics. The rental and leasing segment is expanding rapidly, recording growth of nearly 10% CAGR. Many small and mid-sized operators now prefer rental models to avoid high capital expenditure and maintenance liabilities.

This shift reflects a broader transition toward operational expenditure-based equipment access. Forest management agencies and private landowners also show steady demand growth, supported by reforestation programs and sustainable forestry certifications. These users increasingly require modern, low-impact equipment to comply with environmental guidelines, supporting gradual but consistent expansion across non-commercial end-user categories.

Regional Insights

North America Forestry Trailers Market Trends

North America remains the largest regional market, accounting for approximately 38.5% of the global share. The region benefits from extensive forest resources across the United States and Canada, along with highly mechanized logging operations. The U.S. alone contributes nearly 21.4% of global demand, supported by strong activity in the Pacific Northwest, Southeast, and Great Lakes regions. Government initiatives promoting sustainable forestry further accelerate modernization.

In 2024, the U.S. Environmental Quality Incentives Program allocated US$ 125 million for advanced harvest-planning tools and biodiversity monitoring systems. The broader North American forestry machinery market was valued at US$ 3.1 billion in 2024 and is projected to reach US$ 4.5 billion by 2033. Manufacturers such as JPM Trailers, Pitts Trailers, and Chieftain Trailers strengthen regional leadership through lightweight designs, durability improvements, and innovation-driven product development.

Europe Forestry Trailers Market Trends

Europe accounts for approximately 25% of global market share, supported by strong sustainability frameworks and advanced manufacturing capabilities. Germany leads regional demand with nearly 19% share, benefiting from integrated forestry supply chains and engineering excellence. The European forestry equipment market was valued at US$ 4.01 billion in 2025 and is projected to reach US$ 6.34 billion by 2033, expanding at a CAGR of 5.9%. Stringent climate regulations, particularly the EU’s mandate for 55% emissions reduction by 2030, are accelerating the electrification of timber logistics.

Sweden and Finland lead pilot programs promoting electric forestry transport vehicles. Companies like Kesla Oyj demonstrate strong export-driven growth through advanced technology integration. EU timber regulations focused on traceability and legal sourcing further increase demand for compliant equipment, reinforcing Europe’s position as a premium and innovation-led market.

Asia Pacific Forestry Trailers Market Trends

Asia Pacific is the fastest-growing regional market, expected to expand at a CAGR of 7–8% through 2033. Growth is driven by increasing mechanization across China, India, Japan, and ASEAN countries. China’s government-led focus on sustainable and efficient forest management is accelerating the adoption of modern forestry equipment. India’s afforestation programs and timber industry development initiatives are generating strong demand from logging companies and forest departments.

The regional forestry equipment market was valued at US$ 2.24 billion in 2025 and is forecast to reach US$ 3.34 billion by 2033. Declining rural labor availability, estimated at around 12% over the past decade, is further pushing mechanization. Local manufacturing in India, Indonesia, and Vietnam supports cost-effective equipment supply. Japan and South Korea contribute advanced automation and precision technologies, strengthening regional innovation capabilities.

Competitive Landscape

The forestry trailers market is moderately fragmented, with competition shaped by strong regional players and a limited number of global manufacturers. European companies dominate premium segments through advanced engineering, while manufacturers in emerging markets focus on affordable, region-specific designs. Key players such as Kesla Oyj, JPM Trailers, Chieftain Trailers, and BELL Equipment pursue varied strategies including product specialization, vertical integration, and technology leadership. Kesla’s integrated forestry equipment ecosystem contrasts with Chieftain’s emphasis on lightweight, efficiency-driven designs.

Competitive strategies increasingly prioritize expansion of dealer networks, development of biomass-specific trailers, and investment in electrification technologies. Research and development efforts focus on hybrid-electric systems, IoT-enabled platforms, and modular configurations supporting multiple applications. Additionally, rental and leasing business models are gaining importance, enabling manufacturers to diversify revenue streams and improve equipment accessibility for cost-sensitive operators across global forestry markets.

Key Developments:

- In February 2025, Finnish forest technology manufacturer Kesla Oyj launched its KESLA Defence product line, repurposing its existing multi-purpose trailers to serve international defence equipment markets, signaling strategic diversification beyond traditional forestry applications and broader engagement in defence and security sectors.

- In August 2025, T-MAR Industries Ltd. unveiled the 7280E Hybrid Electric Drive Yarder, the industry’s first hybrid-electric logging machine with five electric motors producing 2,900 horsepower, significantly improving energy efficiency and attracting interest from operators in the United States, Germany, New Zealand, and Chile.

- In January 2025: FPInnovations concluded field testing of its hybrid-electric forestry trailer prototype, demonstrating approximately 12% fuel savings and potential annual CO? reductions of around 23 tonnes per vehicle, backed by funding under Canada’s Clean Growth Program and validating low-emission transport technology.

Companies Covered in Forestry Trailers Market

- JPM Trailers

- Chieftain Trailers

- B.W.S. Manufacturing Ltd

- Palmse Mehaanikakoda Ou

- Stepa Farmkran Gesellschaft M.B.H.

- Scandicon OÜ

- Kesla Oyj

- Pitts Trailers

- Kranman AB

- BELL Equipment

- Industrias Guerra, S.A.

- Kellfri

- Trejon AB

- STEPA Farmkran GmbH

- AS FORS MW

- FPInnovations

- T-MAR Industries Ltd

- Pfanzelt

Frequently Asked Questions

The global Forestry Trailers Market is valued at US$ 2.8 Billion in 2026 and is expected to reach US$ 4.4 Billion by 2033, expanding at a CAGR of 6.5% during the forecast period, driven by rising timber demand, mechanization of logging operations, and sustainable forest management mandates.

The market is driven by surging global timber demand from construction and packaging sectors, mechanization of logging operations responding to labor shortages, sustainability mandates including FSC and PEFC certifications, government support for reforestation programs, and infrastructure development in emerging markets including Asia Pacific, Latin America, and Africa.

Log Trailers command approximately 74% market share due to their simplicity, affordability, and universal applicability across logging operations of varying scales, with tandem-axle configurations representing 45% of this segment through superior stability, weight distribution, and reduced ground pressure.

North America maintains dominant market position with approximately 38.5% global market share, anchored by vast forest resources, mature logging industries, well-developed infrastructure, government environmental programs providing US$ 125 million in EQIP funding in 2024, and strong equipment manufacturing capabilities.

Hybrid-electric and electric propulsion technologies represent the most transformative opportunity, with FPInnovations demonstrating 12% fuel savings, Nordic countries targeting 50% electric forest trucks by 2030, and manufacturers integrating electrification capabilities gaining premium pricing and competitive positioning ahead of anticipated regulatory mandates.

Key market participants include JPM Trailers, Chieftain Trailers, B.W.S. Manufacturing Ltd, Palmse Mehaanikakoda Ou, Stepa Farmkran Gesellschaft M.B.H., Scandicon OÜ, Kesla Oyj, Pitts Trailers, Kranman AB, BELL Equipment, Industrias Guerra S.A., Kellfri, Trejon AB, STEPA Farmkran GmbH, and AS FORS MW, each pursuing differentiated strategies encompassing product specialization, geographic expansion, and technology advancement.