- Off-Road Equipment & Machinery

- Timber Harvesting Equipment Market

Timber Harvesting Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Timber Harvesting Equipment Market by Product Type (Chainsaws, Harvesters, Feller Bunchers, Forwarders, and Skidders), Harvesting Mode (Full Tree, Cut-To-Length, and Tree Length), and Regional Analysis

Timber Harvesting Equipment Market Size and Share Analysis

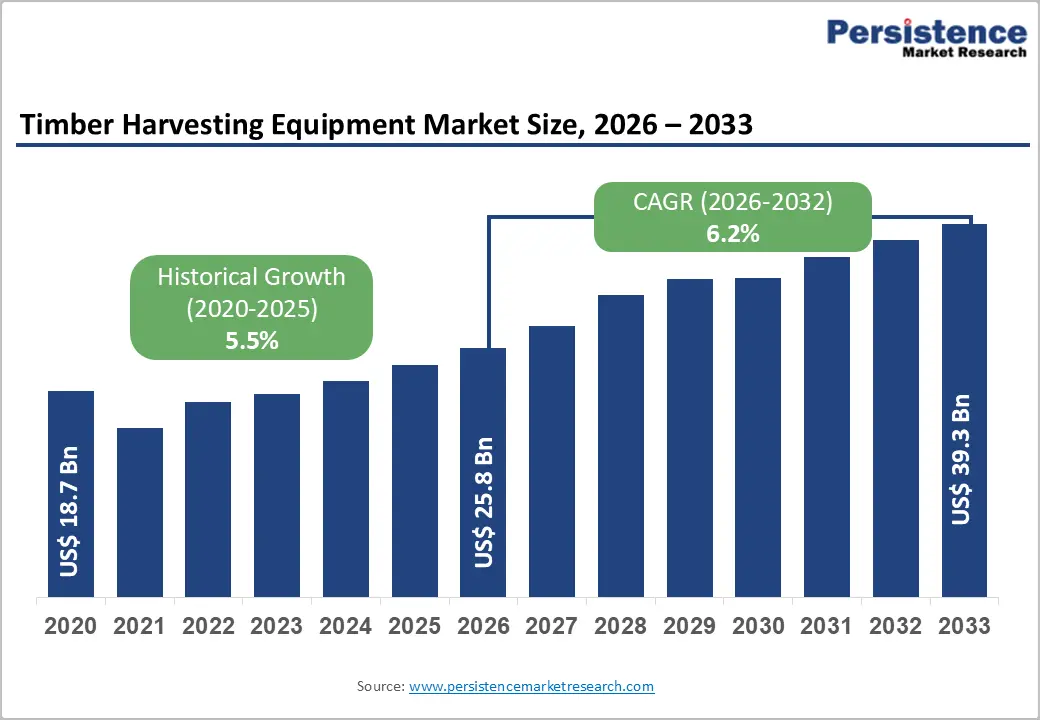

The global timber harvesting equipment market size is likely to be valued at US$ 25.8 billion in 2026 and is projected to reach US$ 39.3 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

The market is experiencing robust expansion driven by the increasing mechanization of forestry operations amid acute labor shortages, with forestry professionals, including heavy equipment operators and logging laborers at high risk for critical shortages over the next decade. Technological innovations in automation, GPS-enabled precision forestry systems, and telematics solutions are enhancing equipment productivity by up to 30% compared to traditional methods, further accelerating market adoption.

Key Highlights:

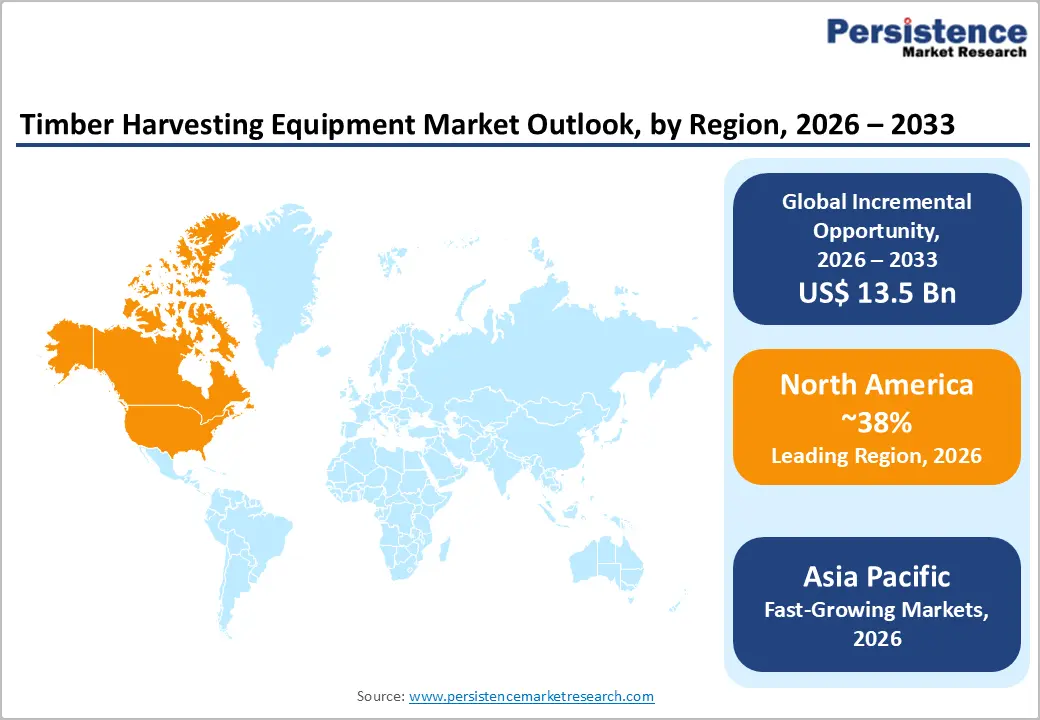

- Leading Region: North America leads the global timber harvesting equipment Market driven by extensive commercial forestland base, advanced mechanization rates, and strong government reforestation incentives including federal Environmental Quality Incentive Program funds and tax deductions that encourage equipment investment among family forest owners and commercial operators.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market with rapid mechanization adoption across China, Japan, India, and Southeast Asia as forestry operations transition from manual methods to fully mechanized Cut-to-Length (CTL) systems, supported by Komatsu's trial programs in Japan starting May 2025 and robust infrastructure development driving timber demand.

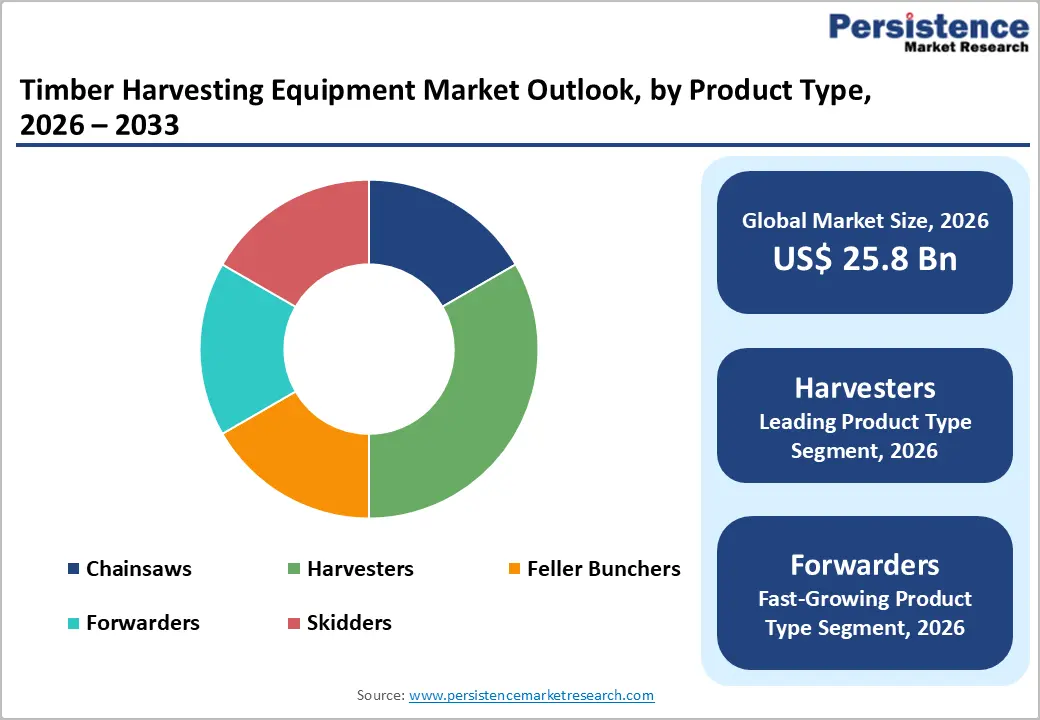

- Leading Product Type: Harvesters dominate the Product Type category with 38% market share, driven by their critical role in modern Cut-to-Length (CTL) operations, with manufacturers like Ponsse Oyj and Deere & Company launching advanced models featuring enhanced automation, GPS integration, and improved power-to-weight ratios that significantly enhance operational productivity.

- Leading Harvesting Mode: Cut-to-Length (CTL) harvesting mode leads with 42% market share due to superior efficiency and reduced environmental impact, enabling completion of all timber production processes with fewer machines and operators while meeting sustainable forest management requirements mandated by Sustainable Forestry Initiative (SFI) and Forest Stewardship Council (FSC) certification bodies.

- Key Market Opportunity: Electrification and hybrid powertrain development represent the key market opportunity, with government initiatives expected to add +1.0% growth particularly in Europe and Scandinavia over 2-4 years, as operators seek to reduce carbon emissions by at least 32 million tonnes annually in compliance with the EU Deforestation-free Products Regulation (EUDR).

| Key Insights | Details |

|---|---|

| Global Timber Harvesting Equipment Market Size (2026E) | US$ 25.8 Bn |

| Market Value Forecast (2033F) | US$ 39.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.2% |

| Historical Market Growth (2020 - 2025) | 5.5% |

Market Dynamics

Drivers - Critical Labor Shortages Accelerating Mechanization Adoption

The forestry and logging sector faces unprecedented workforce challenges that are fundamentally transforming operational practices across North America, Europe, and Asia Pacific. According to the Forest Resources Association, H-2B forestry workers plant more than 85% of trees on public and private forestland annually, amounting to 1.5 billion trees across nearly 2.2 million acres, yet demand for seasonal visas exceeds the Congressionally mandated cap of 66,000 by two to three times. The Canadian Forest sector warns that forestry technologists, logging truck drivers, and heavy equipment operators are at high risk for critical shortages over the next decade, creating an alarming disparity between workers leaving the industry and those being recruited.

This labor crisis is compelling forestry companies to rapidly adopt mechanized harvesting systems, particularly Cut-to-Length (CTL) methods that enable completion of all timber production processes with fewer machines and operators, thereby improving productivity, safety, and cost efficiency while addressing workforce constraints.

Technological Advancements in Automation and Precision Forestry Systems

The integration of advanced automation technologies, GPS tracking systems, Internet of Things (IoT) sensors, and telematics solutions is revolutionizing timber harvesting operations by significantly enhancing equipment efficiency and operational precision. Modern forestry equipment now incorporates GPS-enabled harvesting solutions that allow operators to see precise machine and harvester head locations in real-time map views, with every stump location saved in production files for optimal routing during forwarding operations. According to industry assessments, automation in timber harvesting can improve efficiency by up to 30% compared to traditional methods, while remote monitoring and fleet management systems enable off-site access to telematics data, allowing forestry operators to manage workflow and maximize performance from virtually anywhere.

Komatsu Ltd. began trials in May 2025 in Japan to evaluate ICT-based forestry solutions by combining machine data, including GPS location, production planning, and results with forest stand distribution information to optimize routing and improve productivity through efficient operation management. These technological innovations are reducing human error, minimizing environmental impact, and delivering substantial cost savings that justify higher initial equipment investments.

Restraints - High Capital Investment and Equipment Acquisition Costs

The substantial upfront capital required for purchasing modern timber harvesting equipment represents a significant barrier to market entry, particularly for small and medium-sized logging contractors operating in rural forestry communities. New forestry machinery typically commands premium pricing due to the incorporation of advanced technologies, including automated hydraulic systems, telematics platforms, and precision control mechanisms, with tracked harvesters and feller bunchers requiring especially significant investments. While financing options and government incentives exist in certain regions, such as North America and Europe, many smaller operations struggle to access capital or justify return-on-investment timelines, leading to continued reliance on aging equipment fleets.

The Forest Resources Association notes that smaller forestry operations are declining in number across many parts of the country, partly attributable to difficulties in modernizing equipment portfolios. Additionally, maintenance and service costs for sophisticated equipment can strain operational budgets, particularly in remote harvesting locations with limited access to authorized service networks and genuine replacement parts.

Environmental Regulations and Operational Compliance Requirements

Increasingly stringent environmental regulations governing forestry operations are imposing additional operational constraints and compliance costs on timber harvesting equipment users across major markets. The European Union's Deforestation-free Products Regulation (EUDR) aims to reduce greenhouse gas emissions and biodiversity loss by ensuring products consumed in the EU do not contribute to global deforestation, targeting carbon emission reductions of at least 32 million tonnes per year. The UK Forestry Standard (UKFS) sets comprehensive benchmarks for sustainable forest management, including biodiversity protection, soil health, water protection, and landscape conservation, with compliance mandatory for government grants and felling permissions.

The EU Nature Restoration Regulation entered into force in August 2024, requiring Member States to draw up national restoration plans within two years and establishing strict protection requirements for primary and old-growth forests. These regulations necessitate investments in eco-friendly equipment featuring reduced emissions, lower noise levels, and minimized soil disturbance capabilities, while operational planning must account for protected zones, water crossings, and habitat preservation requirements that can constrain harvesting efficiency and productivity.

Opportunities - Electrification and Hybrid Powertrain Development for Off-Highway Forestry Machinery

The global transition toward sustainable energy sources and carbon emission reduction targets presents substantial growth opportunities for manufacturers developing electric and hybrid-powered timber harvesting equipment. Government re-afforestation incentives and electrification initiatives for off-highway machinery fleets are expected to add +1.0% growth, particularly in Europe, North America, and Scandinavia over the medium term of 2-4 years. Electric and hybrid-powered forestry machines offer significantly lower emissions and reduced noise levels compared to conventional diesel equipment, aligning with corporate sustainability goals and enabling operations in environmentally sensitive areas with strict emission restrictions.

Grant requirements in regions such as North Carolina typically include fuel consumption limits and digital reporting requirements, actively encouraging adoption of hybrid drives and telematics systems. While battery technology and charging infrastructure challenges remain for heavy forestry applications, incremental hybridization of hydraulic systems and auxiliary power functions represents an accessible entry point for manufacturers and operators seeking to reduce carbon footprints while maintaining operational productivity and reliability in demanding forestry environments.

Expansion of Cut-to-Length Harvesting Methods in Asia Pacific Markets

The Asia Pacific region, particularly Japan, China, and India, represents a high-growth opportunity for timber harvesting equipment manufacturers as these markets transition from traditional manual and excavator-based methods toward mechanized Cut-to-Length (CTL) systems. Komatsu Ltd. initiated trials of CTL methods at customer job sites across Hokkaido, Honshu, and Kyushu starting in May 2025, utilizing the Komatsu 931XC harvester (operating weight: 21.9 tons) and Komatsu 855 forwarder (maximum load capacity: 14 tons), with the trial continuing for approximately one year, including comparative studies with traditional methods. Japan boasts expansive forested area comparable to Nordic forestry nations with strong timber production potential, yet excavator-based machines and multi-machine processes have been mainstream amid labor shortages and a declining forestry workforce.

The CTL method enables completion of all timber production processes with fewer machines and operators, creating potential improvements in productivity, safety, and cost efficiency that address acute workforce constraints. Technological advancements in automation and digitalization are reshaping industry demand across the Asia Pacific, with the integration of advanced machinery and data analytics enabling mills to optimize supply chains, reduce waste, and accelerate production cycles, creating favorable conditions for market expansion.

Category-wise Analysis

Product Type Insights

Harvesters dominate the Product Type category with an estimated market share of 38%, driven by their critical role in modern mechanized forestry operations, particularly for Cut-to-Length (CTL) harvesting methods prevalent across Europe, Scandinavia, and increasingly in emerging markets. Ponsse Oyj showcased its new H7 harvester head featuring powerful feed and excellent power-to-weight ratio at FinnMETKO 2024 exhibition in Jämsä, with the advanced PONSSE Active Speed function allowing speed adjustment according to tree species and stem diameter to make harvesting quicker and more productive. Deere & Company launched its large-size H Series wheeled machines in June 2025, including the 1270H and 1470H Harvesters featuring enhanced hydraulic systems, advanced automation, and ergonomic operator enhancements that redefine modern logging operations by combining powerful performance with sustainability-focused fuel economy.

Contract logging firms held 41.5% of the forest machinery market share in 2025, with these professional operators preferring harvesters for their ability to fell, delimb, and buck trees into specified lengths in a single operation, significantly reducing processing time and labor requirements compared to traditional methods. The tracked harvester segment is experiencing particularly strong growth, with John Deere expanding tracked harvester production at its John Deere Specialty Products facility in Langley, British Columbia, with 900-Series machines beginning production in late 2024, followed by 800-Series models in early 2025.

Harvesting Mode Analysis

The Cut-to-Length (CTL) harvesting mode holds the leading position in the Harvesting Mode category with approximately 42% market share, attributed to its superior efficiency, reduced environmental impact, and compatibility with sustainable forest management practices mandated by certification bodies such as the Sustainable Forestry Initiative (SFI) and Forest Stewardship Council (FSC). CTL methods involve felling standing trees, delimbing, and bucking them into logs of specified lengths in the forest using two types of machines: a harvester for felling and processing, and a forwarder for transporting logs, representing the most common forestry approach in Europe and Scandinavia. This system enables completion of all timber production processes with fewer machines and fewer operators compared to Full Tree or Tree Length methods, creating potential improvements in productivity, safety, and cost efficiency that address workforce shortage challenges.

Life cycle assessment studies indicate that fully-mechanized CTL systems perform best for final felling treatments in terms of greenhouse gas emissions, particulate matter emissions, and non-renewable energy consumption when compared to motor-manual and semi-mechanized alternatives. Komatsu Forest AB's extensive lineup of products and solutions tailored for the CTL method has been highly praised by European customers, driving the company's trial introduction of these systems in Japan starting May 2025 to assess effectiveness in Japanese forestry operations. The growing adoption of GPS and High-Precision Positioning solutions enables CTL operators to see precise locations of machines and harvester heads, with every stump location saved in production files allowing forwarder operators to clearly identify harvester trails and optimize routing efficiency.

Regional Insights

North America Timber Harvesting Equipment Trends

North America maintains market leadership driven by the United States and Canada's extensive commercial forestland base, advanced mechanization rates, and strong regulatory frameworks promoting sustainable forest management practices. The U.S. Forest Service has mechanically treated fuels since 1905, with harvesting operations playing a crucial role in forest restoration and wildfire risk mitigation, though treatment acres have fluctuated significantly due to social, economic, and ecological factors. The region faces acute workforce challenges, with the Forest Resources Association reporting that demand for H-2B seasonal forestry workers exceeds the Congressionally mandated cap of 66,000 visas by two to three times, creating urgent need for mechanized solutions.

Deere & Company announced the expansion of forestry equipment production at its John Deere Specialty Products facility in Langley, British Columbia in November 2024, with tracked harvester and feller buncher production of 900-Series machines beginning late 2024 and 800-Series models in early 2025, bringing new job opportunities to the Langley facility in Canada. Government reforestation incentives provide significant market support, with North Carolina offering reimbursement to landowners for planting while permitting use of federal Environmental Quality Incentive Program funds for precision thinning equipment, and federal tax deductions for reforestation expenses improving after-tax returns that encourage family forest owners to purchase midsize forwarders. The Bureau of Labor Statistics reports median annual wages in the forestry and logging sector of US$ 56,980 in 2024, with first-line supervisors earning US$ 73,850 annually, reflecting the skilled nature of mechanized equipment operation.

Europe Timber Harvesting Equipment Trends

Europe represents the most mature market for advanced timber harvesting equipment, characterized by high Cut-to-Length (CTL) method adoption rates, stringent environmental regulations, and leadership in sustainable forestry innovation across Germany, France, United Kingdom, and Scandinavia. The European Union's Deforestation-free Products Regulation (EUDR) adopted in 2023 aims to reduce greenhouse gas emissions by at least 32 million tonnes per year by ensuring products consumed in the EU do not contribute to global deforestation or forest degradation, compelling equipment users to adopt eco-friendly machinery. The EU Nature Restoration Regulation entered into force in August 2024, requiring Member States to draw up national restoration plans within two years and establishing comprehensive requirements for habitat restoration and forest indicators.

The UK Forestry Standard (UKFS) sets clear principles for sustainable forest management and timber harvesting covering biodiversity, soil health, water protection, landscape conservation, and climate resilience, with compliance mandatory for government grants and felling permissions. The standard limits single-species planting to 65% to steer forestry away from monoculture plantations, encouraging mixed woodlands that support greater biodiversity and climate resilience. Ponsse Oyj demonstrated new solutions for sustainable harvesting at the FinnMETKO 2024 exhibition in Jämsä, showcasing new forwarders Elk and Wisend and the H7 harvester head for the first time, featuring High-Precision Positioning solutions using industry-leading navigation tools and advanced technologies such as Active Crane. Government incentives for electrification of off-highway machinery fleets are expected to add +1.0% growth in Europe over the medium term of 2-4 years, particularly in Scandinavia, where environmental standards are most stringent.

Asia Pacific Timber Harvesting Equipment Trends

Asia Pacific is emerging as the fastest-growing regional market for timber harvesting equipment, driven by rapid mechanization adoption in China, Japan, India, and Southeast Asian nations where forestry operations are transitioning from manual and excavator-based methods to fully mechanized systems. Japan boasts expansive forested areas comparable to Nordic forestry nations with strong timber production potential, yet excavator-based machines have long been mainstream, with multi-machine processes representing the norm despite labor shortages. Komatsu Ltd. began the trial introduction of forestry machines manufactured by its wholly owned subsidiary Komatsu Forest AB at customer job sites in Japan starting May 2025, assessing the effectiveness of Cut-to-Length (CTL) methods with the Komatsu 931XC harvester and Komatsu 855 forwarder across Hokkaido, Honshu, and Kyushu for approximately one year.

Technological advancements are reshaping the landscape, with automation and digitalization enhancing operational efficiency and product quality through the integration of advanced machinery and data analytics that enable mills to optimize supply chains, reduce waste, and accelerate production cycles. The region benefits from local timber availability reducing reliance on imports and lowering logistics costs, while forest certification programs such as the Forest Stewardship Council (FSC) and Programme for the Endorsement of Forest Certification (PEFC) equip the region to produce sustainable timber meeting international standards. Manufacturing hubs for mass timber components are growing rapidly, with techniques like CNC milling and robotic assembly helping reduce waste and enhance accuracy, allowing manufacturers to adopt technologies enabling faster project turnaround and customized structural solutions.

Competitive Landscape

The Timber Harvesting Equipment Market demonstrates moderate concentration with the top five players holding a majority market share in 2025, creating a competitive yet consolidated landscape where established manufacturers leverage extensive dealer networks and technological capabilities. Market leaders pursue expansion strategies through geographic production diversification, new product line introductions, and strategic acquisitions in complementary equipment segments such as material processing systems. Key differentiators employed by market leaders include proprietary automation technologies, telematics platforms for fleet management, operator-centric ergonomic designs, and comprehensive aftermarket support networks ensuring parts availability in remote forestry locations.

Emerging business model trends focus on equipment-as-a-service offerings, subscription-based telematics solutions, and integrated digital ecosystems connecting forestry planning software with machine performance data. Research and development investments concentrate on electrification and hybrid powertrains, autonomous operation capabilities, precision forestry integration, and enhanced fuel efficiency, meeting stringent emission standards while maintaining operational productivity in demanding harvesting applications.

Key Developments:

- In June 2025, Deere & Company launched its large-size H Series wheeled machines including the 1270H and 1470H Harvesters and 2010H and 2510H Forwarders, featuring enhanced hydraulic systems, advanced automation, and ergonomic operator enhancements that combine powerful performance with sustainability-focused fuel economy to redefine modern logging operations.

- In February 2025, Caterpillar Inc. unveiled the FM528 forest machine, a versatile triple grouser tracked unit engineered for land clearing, fire clean-up, chipping, grinder loading, mulching, and processing, featuring both fixed and live heel and blade configuration as a first for Caterpillar's forest machine line while sharing common parts with Next Generation excavators.

- In November 2024, Deere & Company announced expansion of tracked harvester and feller buncher production to the John Deere Specialty Products facility in Langley, British Columbia, with 900-Series machines beginning production late 2024 followed by 800-Series models in early 2025, strategically positioning the facility as the center of excellence for manufacturing purpose-built tracked forestry equipment.

Companies Covered in Timber Harvesting Equipment Market

- Deere & Company

- Komatsu Ltd.

- Ponsse Oyj

- Caterpillar Inc.

- Tigercat International Inc.

- Logset Oy

- Eco Log Sweden AB

- Rottne Industri AB

- Husqvarna AB

- Andreas Stihl AG & Company KG

- Stanley Black & Decker, Inc.

- Hitachi Ltd.

- Kesla Oyj

- Barko Hydraulics L.L.C

- Volvo AB

Frequently Asked Questions

The global Timber Harvesting Equipment Market is projected to reach US$ 39.3 Bn by 2033, growing from US$ 25.8 Bn in 2026 at a compound annual growth rate of 6.2% during the forecast period, driven by increasing mechanization adoption, labor shortages, and stringent environmental regulations promoting sustainable forestry practices.

Critical labor shortages with forestry workforce demand exceeding supply by two to three times are accelerating mechanization adoption, while technological advancements in automation and GPS-enabled precision forestry systems are improving operational efficiency by up to 30% compared to traditional methods, compelling forestry operators to invest in advanced harvesting equipment.

Harvesters hold the leading position with approximately 38% market share, driven by their critical role in modern Cut-to-Length (CTL) harvesting operations that enable felling, delimbing, and bucking trees into specified lengths in a single operation, with recent innovations from Ponsse Oyj and Deere & Company featuring enhanced automation and power-to-weight ratios.

North America maintains market leadership driven by the United States and Canada's extensive commercial forestland base, advanced mechanization rates exceeding 41.5% among contract logging firms, and strong government reforestation incentives including federal tax deductions and Environmental Quality Incentive Program funds that encourage equipment investment.

Electrification and hybrid powertrain development presents substantial growth opportunities, with government initiatives expected to add +1.0% growth particularly in Europe and Scandinavia over 2-4 years, as operators seek to reduce carbon emissions by at least 32 million tons annually in compliance with the EU Deforestation-free Products Regulation (EUDR) adopted in 2023.

Leading companies include Deere & Company, Komatsu Ltd., Ponsse Oyj, Caterpillar Inc., and Tigercat International Inc.