- Off-Road Equipment & Machinery

- Forestry Machinery Market

Forestry Machinery Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Forestry Machinery Market by Working Type(Feller Bunchers, Harvester,Skidders, Loaders, Forwarders,Swing Machines), by Power Source (Diesel,Hybrid,Electric), by Automation (Manual, Semi-automatic, Automatic), by Regional Analysis, 2025-2032

Forestry Machinery Market Size and Trend Analysis

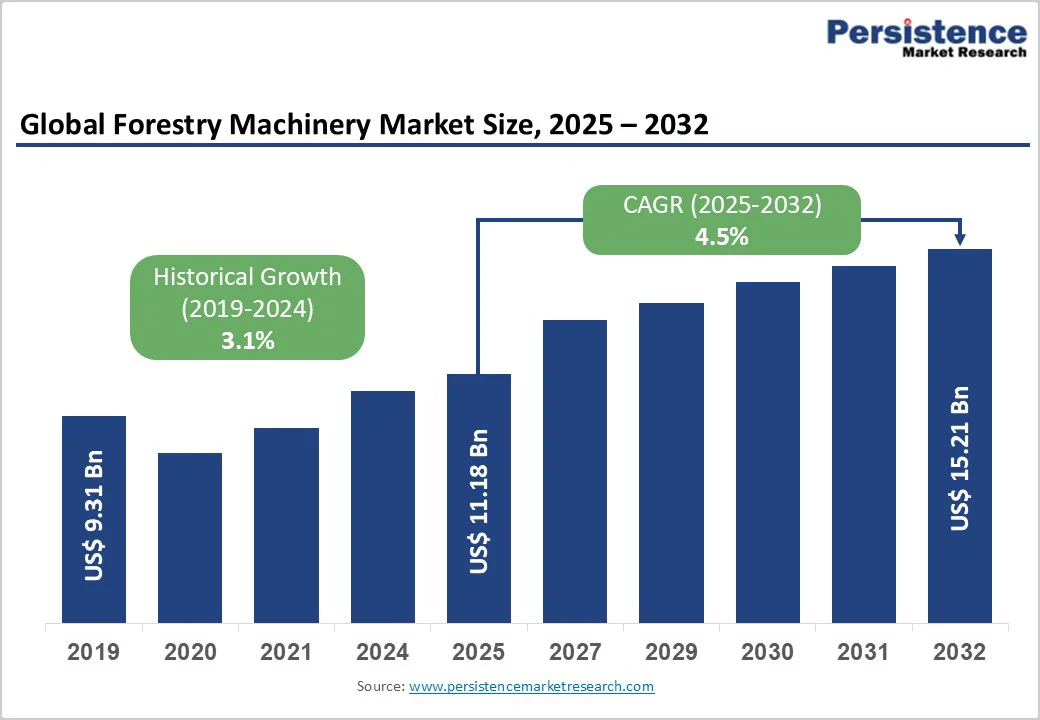

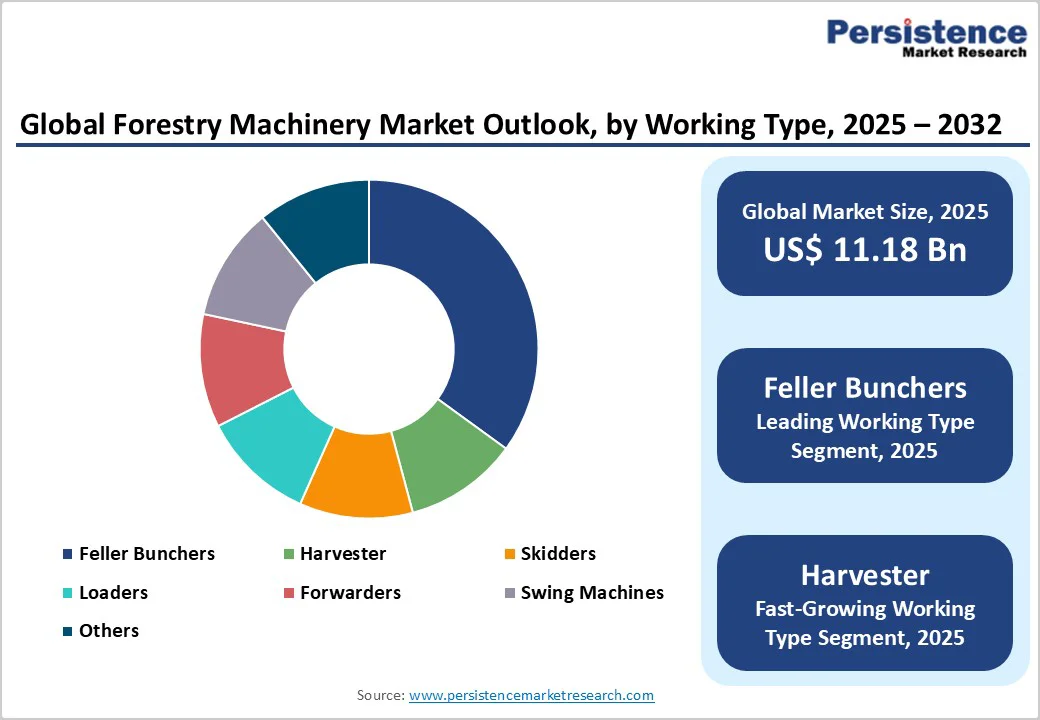

The global forestry machinery market size is likely to value at US$ 11.2 billion in 2025 and is projected to reach US$ 15.2 billion by 2032, growing at a CAGR of 4.5% between 2025 and 2032. The market is driven by rising global demand for timber and wood products amid expanding construction and bioenergy sectors, supported by advancements in mechanization that enhance efficiency and sustainability in forest operations. According to OECD-FAO Agricultural Outlook 2025-2034, demand for wood-based materials is expected to increase due to renewable energy initiatives and urbanization, necessitating advanced machinery for responsible harvesting.

Key Market Highlights:

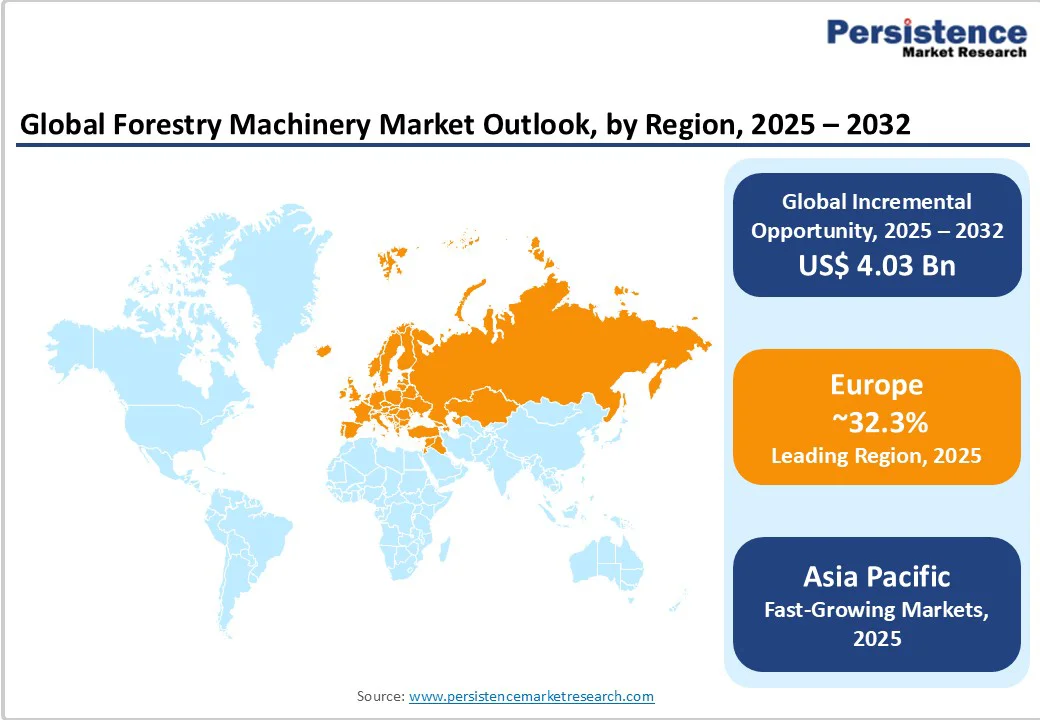

- Regional Leader: Europe leads the forestry machinery market, with 32.3% share due to stringent EU regulations and vast forest resources, ensuring sustained demand for compliant, efficient equipment.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, fueled by China's manufacturing and India's afforestation initiatives, boosting mechanization.

- Leading Segment: Feller bunchers dominate the working type segment with 35% of the market, offering efficient bunching for high-volume timber operations worldwide.

- Fastest Growing Segment: Electric power sources represent the fastest-growing segment, propelled by emission regulations and hybrid tech advancements.

- Growth Opportunities: Automation upgrades provide a key opportunity, enabling AI-driven precision to enhance safety and yield in thinning applications.

| Key Insights | Details |

|---|---|

| Forestry Machinery Market Size (2025E) | US$ 11.2 Bn |

| Market Value Forecast (2032F) | US$ 15.2 Bn |

| Projected Growth CAGR (2025-2032) | 4.5% |

| Historical Market Growth (2019-2024) | 3.1% |

Market Dynamics

Driver - Rising Demand for Wood Products

The rise in global need for wood and derived products in construction, paper, and bioenergy sectors is a primary driver for the forestry machinery market. As urbanization accelerates, timber demand surges, with Eurostat reporting a 12.5 million cubic meters surplus in EU roundwood exports in 2022, where 25% of production served as fuelwood. This trend pushes operators toward efficient machinery like harvesters and skidders to boost productivity and reduce labor costs.

Mechanized operations enable precise logging, supporting sustainable supply chains and aligning with renewable energy goals, thereby positively impacting market expansion by enhancing output without excessive deforestation.

Adoption of Sustainable Forestry Practices

Increasing emphasis on environmental conservation and regulatory compliance drives the integration of advanced machinery that minimizes soil disturbance and waste. The FAO highlights that sustainable management practices, including selective harvesting, require specialized equipment to maintain forest health amid climate challenges. For instance, precision tools reduce overharvesting by up to 30%, as per industry analyses, fostering biodiversity and carbon sequestration. This shift not only complies with global standards like the EU Green Deal but also appeals to eco-conscious markets, stimulating demand for innovative forestry solutions and contributing to long-term market growth.

Furthermore, technological integration, including AI-driven harvesters and telematics, is propelling the market by enhancing safety and productivity, with automation adoption increasing by 25% in key forestry regions, according to industry journals. These innovations enable precise tree selection and minimal environmental disruption, addressing labor shortages that affect 40% of forestry operations worldwide, as noted in World Bank analyses.

Restraint - High Initial Investment Costs

The substantial upfront costs associated with acquiring advanced forestry machinery pose a significant barrier, particularly for small-scale operators in developing regions. Modern equipment, featuring GPS and telematics, can exceed USD 200,000 per unit, deterring adoption amid limited financing options. According to Eurostat data, this financial hurdle contributes to slower mechanization rates, with employment in forestry dropping 16% since 2000 due to unaffordable upgrades.

Maintenance expenses, including specialized parts and skilled servicing, further strain budgets in developing regions, leading to prolonged reliance on outdated equipment. This cost sensitivity hampers widespread adoption, slowing market penetration and exacerbating inefficiencies in fragmented supply chains.

Maintenance and Operational Challenges

Complex machinery requires specialized maintenance, increasing downtime and costs in remote forest areas with limited service access. Safety features like guards and locking devices add 10-15% to operational expenses, as noted in industry reports, while rugged terrains accelerate wear. Regulatory frameworks from bodies such as the European Union (EU) and the United States Forest Service impose strict emission and land-use standards, complicating machinery approvals and increasing compliance costs by up to 20% for manufacturers. These lead to higher total ownership costs, discouraging investments and slowing technology uptake. Consequently, operators face reduced productivity, impacting profitability and hindering market expansion in labor-intensive sectors.

Market Opportunities

Shift Toward Electric and Hybrid Technologies

The shift toward electric and hybrid forestry machinery presents a prime opportunity, driven by global emission reduction targets under the Paris Agreement, with projections indicating 40% market penetration by 2030 in eco-focused regions. Farmonaut reports that hybrid models reduce fuel use by 25%. Developments such as Tigercat Industries' hybrid machines in 2025 align with EU carbon neutrality targets, enabling operators to access subsidies and green financing. This not only lowers long-term costs but also appeals to bioenergy firms, generating demand in the Forestry Trailers Market for compatible transport solutions and fostering innovation in low-emission segments.

Advancements in Automation and Precision Forestry

Automation, including AI and IoT integration, offers growth in semi-automatic and automatic segments, enhancing safety and efficiency in challenging terrains. FORMEC studies indicate that automated systems could require up to 100,931 machine units by 2030 under high mobilization scenarios, reducing labor needs by 40%. Precision forestry tools, integrating drones and GPS for optimized harvesting, offer vast potential in Asia Pacific and Latin America, where afforestation programs could add 50 million hectares by 2030, per FAO initiatives. In India and China, where timber demand grows at 8% annually, these technologies minimize waste and enhance yields, addressing labor shortages affecting 70% of operations.

News from John Deere's 2025 plant expansion highlights AI-enabled harvesters improving yield predictions. This opportunity targets end-users in reforestation and thinning, linking to the Agroforestry Market for integrated ecosystem management and promising significant revenue through technological upgrades.

Category-wise Insights

Working Type Analysis

Feller bunchers lead the working type category with approximately 35% market share, owing to their efficiency in high-volume clearcutting and bunching operations. Feller bunchers outperform harvesters in dense forests, enabling faster tree felling with minimal ground disturbance, as evidenced by FAO data on mechanized harvesting boosting productivity by 30% in timber-rich areas. Wheeled and tracked variants dominate due to adaptability across terrains, with tracked models preferred in soft soils for reduced compaction, supported by data showing 20% lower environmental impact compared to manual methods. Their versatility across tracked and drive-to-tree variants suits varied terrains, justifying dominance amid rising timber demands in construction.

Power Source Analysis

Diesel remains the dominant power source, capturing about 60% of the market due to its reliability and power output in demanding forestry tasks. Industry insights from Farmonaut show diesel engines powering 80% of heavy skidders and loaders, supported by widespread fuel availability and established infrastructure. Proven fuel efficiency and widespread infrastructure availability make diesel the go-to for heavy-duty tasks like skidding and loading, with statistics indicating 15% lower operational costs than alternatives in remote areas. This leadership persists despite emissions concerns, as diesel's torque handles rugged conditions better than alternatives, backed by OECD-FAO projections for sustained wood production needs.

Automation Analysis

Semi-automatic systems hold roughly 45% share, balancing human oversight with efficiency gains, as highlighted in robotics studies for forest harvesting. These systems, featuring assisted controls for boom movements, reduce operator fatigue by 30% and error rates, according to FAO productivity reports on mixed automation levels. Their adoption is justified by cost-effectiveness over full automation, ideal for varied terrains where full autonomy remains challenging.

Operation Analysis

New machinery holds the top position at approximately 75% market share, driven by technological advancements and performance guarantees. Operators favor new units for integrated features like telematics, as per CustomTruck analyses, which show new equipment improving efficiency by 20% over used models. Fresh equipment offers superior performance and integration of features like telematics, with data showing 25% higher uptime than used models in intensive operations. This dominance is supported by financing incentives and rapid depreciation of used assets in harsh environments, ensuring reliability for modern forestry demands.

Regional Insights

North America Forestry Machinery Trends

North America drives the forestry machinery adoption, with the U.S. dominating the region due to its vast timber resources and innovation ecosystem. USDA reports emphasize regulatory frameworks like the National Forest Management Act, promoting mechanized harvesting to sustain 300 million acres of forests. Recent developments, including John Deere's August 2025 USD 150 million plant expansion in Canada, focus on autonomous harvesters, enhancing efficiency amid bioenergy growth.

The region's trends highlight precision technologies, with Farmonaut noting 35% global precision forestry share driven by AI for wildfire monitoring. Government incentives under the Inflation Reduction Act support hybrid adoption, reducing emissions in operations across Canada and the U.S., fostering a robust market for sustainable equipment.

Europe Forestry Machinery Trends

Europe's market is shaped by armonized regulations like the EU Timber Regulation, emphasizing sustainable practices in Germany, U.K., France, and Spain. Eurostat data shows 40% land is forested, with machinery aiding precise logging to meet 25% fuelwood production. Ponsse Oyj's remote-service tech supports this, minimizing impact in boreal zones.

Performance analysis reveals Sweden and Finland leading mechanization, where subsidies drive 20% efficiency gains via GPS-equipped forwarders. Regulatory alignment under the Green Deal promotes low-emission models, with Volvo AB innovations enhancing cross-border compliance and boosting the Forestry Equipment Tire Market for durable treads.

Asia Pacific Forestry Machinery Trends

Asia Pacific's growth is propelled by manufacturing advantages in China, Japan, and India, with China as the largest contributor via state-led afforestation. FAO notes rapid mechanization in India's plantations, increasing productivity by 40% through harvesters amid urbanization. ASEAN dynamics favor affordable diesel units for pulp exports.

Japan's focus on automation addresses labor shortages, with Komatsu's electric prototypes aligning with emission targets. India's ASEAN ties enhance supply chains, supporting Agroforestry Market integration for mixed-use lands and driving demand in emerging economies.

Competitive Landscape

The global forestry machinery market exhibits a consolidated structure, dominated by a few global leaders holding a large share through R&D and mergers. Companies pursue expansion via electrification and AI integration, as witnessed in partnerships for telematics. Key differentiators include ergonomic designs and predictive maintenance, while emerging models emphasize leasing for SMEs. This concentration fosters innovation but challenges smaller players in fragmented regions.

Key Market Developments:

- August 2025: John Deere expanded its forestry plant in Canada with a USD 150 million investment to produce next-gen harvesters and forwarders.

- July 2025: Tigercat Industries launched hybrid-powered machines in North America, reducing fuel consumption by 25%.

- February 2025: Caterpillar unveiled the FM528 Forestry/Log Loader for mill-yard tasks, enhancing productivity.

Top Companies in Forestry Machinery Market

Caterpillar (Peoria, Illinois, USA) leads with robust portfolios in harvesters and loaders, generating high revenue through global influence and R&D in autonomous tech, ensuring market maturity and strong after-sales support.

John Deere (Moline, Illinois, USA) excels in versatile equipment like feller bunchers, leveraging telematics for efficiency. Its influence stems from extensive dealer networks and innovations in sustainable logging.

Komatsu (Tokyo, Japan) dominates via electric drives and connectivity, with portfolio strength in skidders, headquartered in Asia, it drives growth through regulatory-compliant designs and high-volume production.

Companies Covered in Forestry Machinery Market

- Caterpillar

- John Deere

- Tigercat International Inc.

- Volvo AB

- Komatsu

- Kubota Corporation

- Hitachi Construction Machinery Co., Ltd.

- Liugong Machinery Co., Ltd.

- Ponsse Oyj

- Barko Hydraulics L.L.C

- Kawasaki Heavy Industries, Ltd

- Dafo

- Rabaud

- Eco Log

- Rottne Industri AB

Frequently Asked Questions

The forestry machinery market is valued at US$ 11.2 Bn in 2025 and expected to reach US$ 15.2 Bn by 2032, growing at 4.5% CAGR.

Key drivers include rising wood product demand and sustainable practices, with mechanization improving efficiency by 30% per FAO insights.

Feller bunchers lead with a 35% share, excelling in efficient clear-cutting operations.

North America leads, supported by U.S. regulations and innovations in precision forestry.

Electric and hybrid technologies offer growth, reducing emissions by 25% via new models.

Leading players include Caterpillar, John Deere, and Komatsu, focusing on automation and sustainability.