- Agrochemicals

- Agroforestry Market

Agroforestry Market Size, Share, and Growth Forecast, 2025 - 2032

Agroforestry Market by System (Agrisilvicultural, Silvopastoral, and Agrosilvopastoral), By Product (Timber, Lumber, and Fiber Crops, Fruits and Nuts, Vegetables and Herbs, Medicinal Plants, and Other) and Regional Analysis for 2025 - 2032

Agroforestry Market Size and Trends Analysis

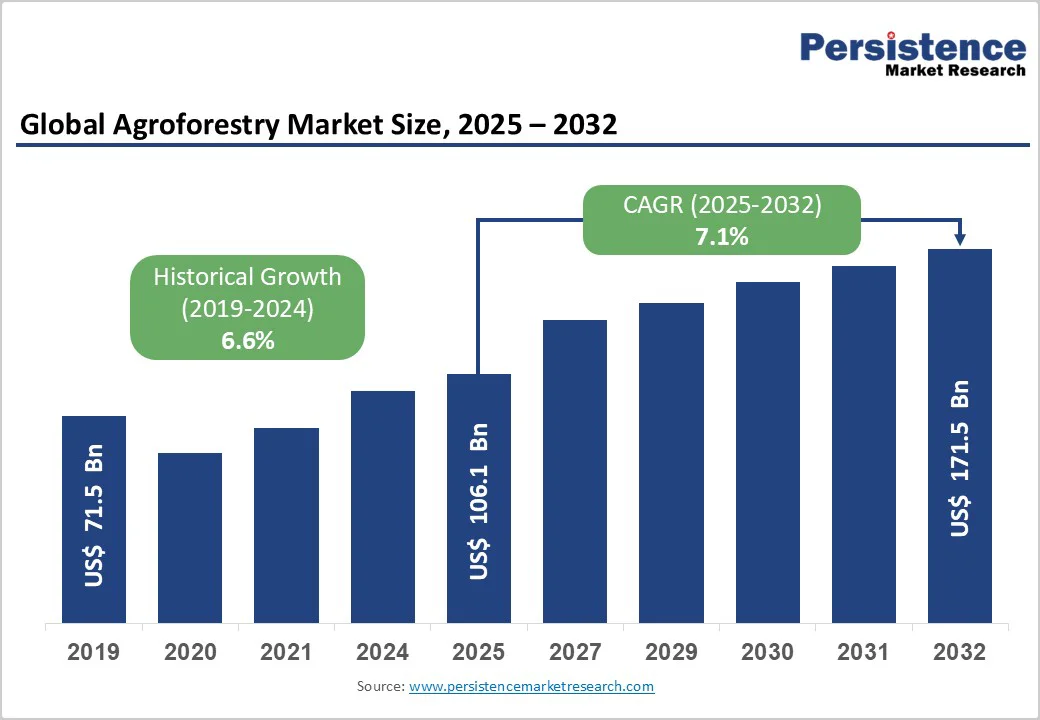

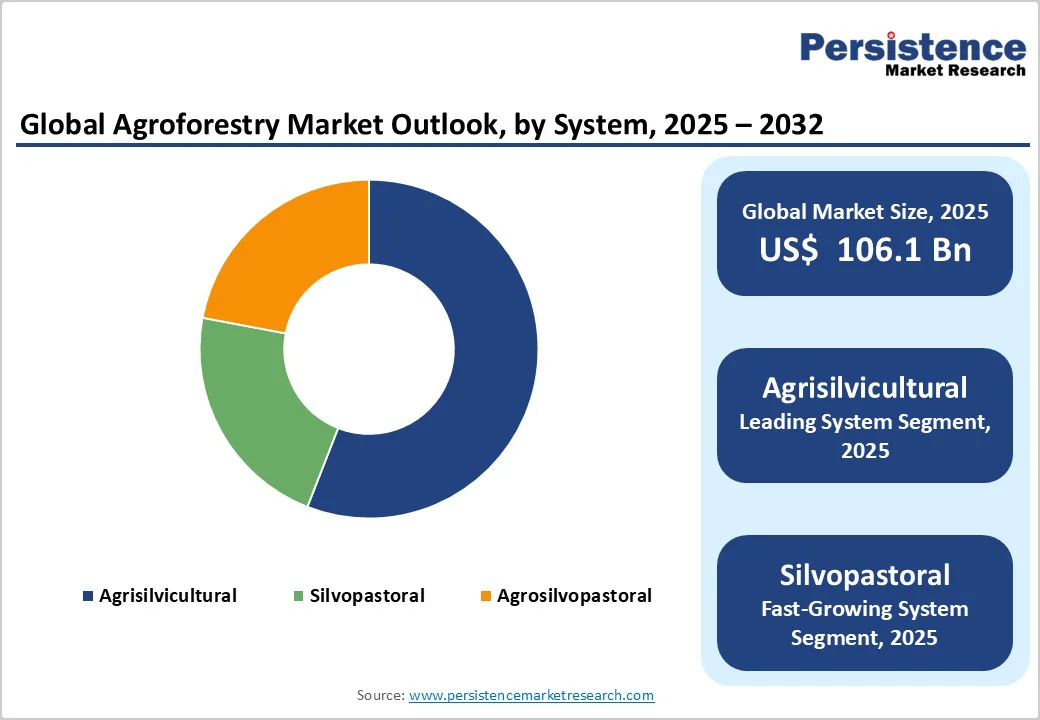

The global agroforestry market size is likely to reach US$106.1 billion in 2025 and is projected to grow to US$171.5 billion, at a CAGR of 7.1% between 2025 and 2032. Agroforestry has emerged as a transformative land-use system that integrates trees, crops, and livestock within a single management unit, offering a sustainable solution to modern agricultural challenges. Rising global concerns about climate change mitigation, biodiversity conservation, and food security drive the market's expansion.

Key Industry Highlights:

- Agroforestry Boosts Global Food Security: Supports food and nutrition security for 1.2 billion people through diversified fruit, nut, and medicinal crop systems.

- Economic Returns Drive Farmer Adoption: ICAR studies report 25–68% income growth and benefit-cost ratios up to 4.17, enhancing livelihood stability.

- Climate Resilience through Diversification: Agroforestry reduces vulnerability to crop failures by 30–35%, providing natural insurance against extreme climate events.

- Government Policy Momentum: Over US$146 million invested under India’s National Agroforestry Policy and €1.5 billion allocated by the EU (2023–2027).

- Massive Land Restoration Programs: China’s “Grain for Green” converted 32 million hectares to tree-based systems with investments exceeding US$40 billion.

- Land Tenure and Gender Barriers Persist: Insecure ownership and gender inequality—women hold only 13% of farmland—restrict large-scale adoption potential.

- Silvopastoral Systems Show Fastest Growth: Valued at US$2.1 billion in 2024, projected to reach US$4.9 billion by 2033 at 9.5% CAGR.

- Asia Pacific Leads Global Market Expansion: Holds 40% share with strong government backing, reforestation programs, and projected 8.4–9.1% CAGR through 2033.

- Corporate and Institutional Collaborations Surge: Partnerships like Nestlé–OFI (US$ 45 million) and The Nature Conservancy (US$ 60 million) fuel sustainable agroforestry growth.

| Key Insights | Details |

|---|---|

|

Agroforestry Market Size (2025E) |

US$106.1 Bn |

|

Market Value Forecast (2032F) |

US$171.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.6% |

Market Dynamics

Drivers - Food Security and Livelihood Diversification Demands

The Food and Agriculture Organization (FAO) reports that agroforestry systems support food security for approximately 1.2 billion people globally, with tree-based farming contributing to dietary diversity through the production of fruits, nuts, vegetables, and medicinal plants. Research published in the journal Frontiers in Public Health demonstrates that integrating fruit trees such as mango and avocado into agroforestry systems reduced vitamin A deficiency by 18% in Kenya, addressing public health challenges affecting 30% of sub-Saharan children.

Economic analyses conducted by the Indian Council of Agricultural Research across 24 agroforestry systems in different agro-ecological regions found internal rates of return ranging from 25% to 68% and benefit-cost ratios between 1.01 to 4.17. In India's Uttar Pradesh and Bundelkhand regions, agroforestry adoption increased farmer incomes by 25-68% through diversified revenue streams from timber, fuelwood, fodder, and intercropping activities. The World Bank estimates that agroforestry can increase smallholder farmer incomes by 40-60% compared to conventional monoculture systems, while simultaneously reducing vulnerability to climate-related crop failures by 30-35%.

Government Policy Support and Regulatory Frameworks

National agroforestry policies have proliferated globally since India became the first country to adopt a comprehensive National Agroforestry Policy in 2014, backed by a capital outlay of US$146 million through the Sub-Mission on Agroforestry. The United States Department of Agriculture (USDA) invested US$333 million in agroforestry initiatives during fiscal years 2011-2012 and has committed an additional US$60 million through the Partnership for Climate-Smart Commodities program launched in 2022. The European Union's Common Agricultural Policy (CAP) provides €200 per hectare annually for agroforestry management under eco-scheme interventions, with Member States allocating over €1.5 billion for agroforestry establishment and maintenance between 2023 and 2027.

In Asia, China's National Forestry and Grassland Administration has implemented the "Grain for Green" program, converting over 32 million hectares of marginal cropland to tree-based systems since 1999, with total government investment exceeding US$40 billion. These policy frameworks have significantly reduced regulatory barriers related to tree felling, transit permissions, and land tenure security, thereby accelerating farmer adoption rates.

Restraint - Land Tenure Insecurity and Regulatory Complexity

Insecure land and tree tenure rights represent a critical constraint to agroforestry expansion, particularly in regions where customary land management systems conflict with formal legal frameworks. The FAO emphasizes that the likelihood of farmers adopting agroforestry increases significantly when they possess long-term, secure tenure to sufficiently large land areas and ownership rights to trees planted thereon.

In many African and Asian countries, restrictive tree-felling and transit regulations, originally designed for forest conservation, inadvertently discourage farmers from planting trees on agricultural land due to fears of losing harvest rights. Research published in Ecological Indicators identifies land tenure challenges, including small plot sizes (averaging below 0.5 hectares in South Asia), clan-owned land rental systems, and the absence of village land-use plans, as the top-five constraints limiting agroforestry adoption.

Gender disparities in land access further compound these challenges, with women farmers controlling only 13% of global agricultural land despite comprising 43% of the farm labor force. Complex bureaucratic procedures for obtaining tree felling and transit permits—requiring multiple agency approvals and lengthy processing times exceeding 60-90 days—create transaction costs that reduce the net profitability of agroforestry enterprises. The lack of standardized definitions for agroforestry across different government ministries (agriculture, forestry, environment) creates jurisdictional ambiguities that complicate regulatory compliance and subsidy access.

Opportunity - Institutional and Corporate Collaboration Accelerating Global Agroforestry Expansion

The global agroforestry market is increasingly shaped by large-scale institutional and corporate collaborations aimed at enhancing sustainability, productivity, and climate resilience. Governments, research institutions, and private organizations are jointly investing in agroforestry systems as part of broader land restoration and food security goals. In 2025, Indonesia’s launch of a national agroforestry program spanning 1.1 million hectares marked a major milestone in integrating trees within agricultural landscapes to strengthen food supply and ecological balance. Similar initiatives, such as Kenya’s Bamboo Agroforestry Initiative, are promoting bamboo cultivation as a dual-benefit crop for climate resilience and rural income generation.

In developed economies, digital innovation is complementing policy efforts—the U.K.’s Land App introduced a free digital toolkit to help land managers plan and track agroforestry adoption, while Sainsbury’s and the Woodland Trust are collaborating to support farmers in integrating tree systems across farmland. Furthermore, research institutions are deepening their engagement, with the USDA and University of Maine establishing dedicated agroforestry research sites to advance knowledge on carbon sequestration, biodiversity, and economic models. Collectively, these initiatives signal a strong supply-side momentum, underscoring a global trend toward institutionalized agroforestry development supported by policy frameworks, technology integration, and private-sector participation.

Category-wise Analysis

By System Insights

In 2025, the agrisilvicultural systems segment dominated the global agroforestry market with a commanding 35.7% revenue share, reflecting the widespread adoption of crop-tree integration models that maximize land productivity while maintaining food security. These systems, which combine crops with tree species on the same land, are increasingly valued for their ability to enhance soil fertility, improve microclimates, and increase overall yields. A study in Haryana, India, found a 51% increase in barley yields under scattered-tree conditions compared to treeless fields, highlighting the agronomic advantage of scattered trees.

With shorter establishment periods of two to three years before intercrop revenues begin, agrisilvicultural systems offer faster returns and lower transition risks. Key configurations such as alley cropping, homegardens, and improved fallows remain popular globally. Meanwhile, the silvopastoral systems segment is emerging as the fastest-growing category, driven by its benefits in livestock productivity, pasture regeneration, and carbon mitigation. Valued at US$2.1 billion in 2024 and projected to reach US$4.9 billion by 2033 (CAGR 9.5%), silvopasture adoption is accelerating in North America, Latin America, and Asia-Pacific, supported by policy incentives and strong environmental co-benefits such as reduced methane emissions and improved carbon sequestration.

Application Industry Insights

The timber, lumber, and fiber crops segment dominates the global agroforestry market, accounting for over 35% of total revenue, supported by its high economic value and well-established supply chains for wood-based products. This segment includes commercial timber species such as eucalyptus, poplar, acacia, and teak, along with fuelwood and specialty woods used in furniture and construction. In India, agroforestry accounts for nearly 65% of small timber and 70–80% of wood for furniture manufacturing, underscoring its pivotal role in meeting domestic timber demand outside traditional forests.

Fast-growing hybrid poplar plantations reach maturity within 8–12 years, generating returns of US$ 8,000–15,000 per hectare, while bamboo-based agroforestry continues to expand under India’s US$ 400 million National Bamboo Mission, driven by demand from textiles, composites, and bioenergy industries. Conversely, the fruits and nuts segment represents the fastest-growing category, fueled by rising global demand for sustainably sourced, high-value food products. Supported by premium pricing of 20–40% in organic and fair-trade markets, fruit-based systems in India’s Meghalaya and Assam have boosted farmer incomes by up to threefold, while nut agroforestry (notably walnut) delivers US$3,000–6,000 per hectare annually once mature, reinforcing the sector’s profitability and resilience to climate variability.

Regional Insights and Trends

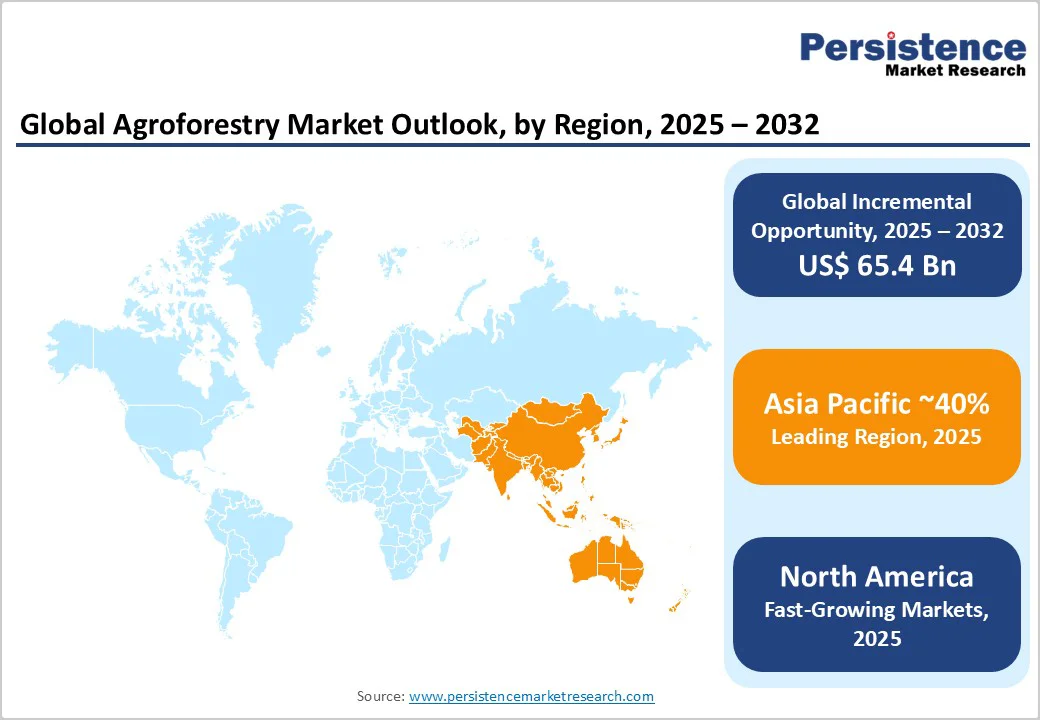

Asia Pacific Dominates the Global Agroforestry Market with Strong Policy Support, Expanding Land Integration, and Fastest Growth Outlook

Asia Pacific region dominates the global agroforestry market, accounting for over 40% of total revenue valued at US$ 42–45 billion in 2025, and is projected to record the fastest CAGR of 8.4–9.1% through 2032–2033. Growth is propelled by vast agricultural land resources, dense population driving food demand, and robust government initiatives promoting reforestation and sustainable agriculture. India remains the regional leader, with 25.3 million hectares under agroforestry (expandable to 50 million hectares) and market value expected to reach US$ 20 billion by 2032, supported by liberalized tree felling norms and seedling networks producing over 100 million plants annually.

China’s “Grain for Green” program has converted 32 million hectares into tree-based systems through US$ 40 billion in investments, while Indonesia, Vietnam, Thailand, and the Philippines integrate agroforestry into their climate commitments under the Paris Agreement. Regional growth is further supported by Japan’s research collaboration through the Asia-Pacific Forestry Commission and India’s strong policy environment in states like Punjab, Haryana, Karnataka, and Tamil Nadu. Increasing investments from governments, research institutes, and private players underscore the region’s leadership in digital agroforestry, carbon credit aggregation, and climate-resilient value chain integration.

North America Strengthens Agroforestry Adoption Through Climate-Smart Policies, Regenerative Agriculture, and Technology-Driven Investments

North America maintains a substantial regional market share, driven by established baking and food processing industries, advanced biotechnology infrastructure, and stringent regulatory frameworks supporting enzyme adoption. The United States represents the dominant market in the region, supported by significant ethanol production capacity and robust pharmaceutical research sectors, which are driving Agroforestry demand across multiple applications. The region holds approximately 39% of the global food enzymes market, reflecting mature industry development and high enzyme adoption rates across commercial food manufacturing.

Production facilities for major enzyme manufacturers, including Novozymes and DuPont, support regional supply security and rapid customer support. Government incentives promoting renewable energy and bio-based industries support bioethanol production growth, incrementally increasing Agroforestry demand for fuel ethanol applications. Regulatory frameworks, while more streamlined than European systems, maintain rigorous safety and efficacy standards supported by FDA oversight and established enzyme registration protocols. North American manufacturers prioritize innovation in specialized enzyme variants, thermostable formulations, and clean-label solutions meeting premium market segments. Investment trends reflect strong R&D spending by multinational corporations seeking novel applications and enhanced enzyme performance characteristics

Competitive Landscape

The global agroforestry market is highly fragmented, with top players accounting for only 18–22% of the total market share. Unlike conventional agriculture, leadership is distributed among research institutions, government agencies, private firms, and social enterprises offering technical support, certification, and financing. Key participants include CIFOR-ICRAF, a leading global research body coordinating agroforestry networks across 50+ countries, and Weyerhaeuser Company, integrating silvopasture systems across its 10.2 million hectares of timberland. Rainforest Alliance promotes agroforestry through certification programs impacting 2 million farmers, while EcoPlanet Bamboo manages 12,000 hectares of sustainable plantations across multiple continents.

Competitive clusters include research institutions, timber enterprises, certification organizations, technology providers, and carbon finance intermediaries such as TerraCarbon LLC. Strategic developments highlight strong corporate engagement—Nestlé and OFI’s US$45 million cocoa agroforestry partnership and The Nature Conservancy’s US$60 million incentive program underscore rising investment. Meanwhile, BNP Paribas and Domain Timber are channeling sustainable finance into agroforestry-linked assets, reflecting a growing trend toward carbon-driven investments, digital precision management, and vertically integrated value chain development.

Key Industry Developments:

- In 2025, Global adoption accelerated as Indonesia launched a 1.1 million-hectare national agroforestry program, and Kenya advanced its Bamboo Agroforestry Initiative for climate resilience and livelihoods. In the U.K., Land App introduced a free digital toolkit, with Sainsbury’s and the Woodland Trust guiding the integration of farmers. Meanwhile, the USDA and University of Maine established research sites to advance scientific collaboration, marking strong policy and technological momentum in agroforestry expansion.

Companies Covered in Agroforestry Market

- Weyerhaeuser Company

- Center for International Forestry Research and World Agroforestry (CIFOR-ICRAF)

- ArborGen LLC

- EcoPlanet Bamboo

- Green Resources AS

- Rainforest Alliance

- TerraCarbon LLC

- Center for Agroforestry (University of Missouri)

- Agroforestry Systems Inc.

- Tribmoon Agroforestry Private Limited (TreeKisan)

- Green City Biotech

- Heartland Global, Inc.

- Pachama

- DroneSeed

- Other Market Players

Frequently Asked Questions

The global biomaterials market is projected to be valued at US$ 186.3 Bn in 2025.

The growth of the global biomaterials market is primarily driven by the increasing demand for advanced biomaterials amid the rising prevalence of cardiovascular disorders, coupled with continuous technological innovations enhancing material performance and biocompatibility.

The global biomaterials market is poised to witness a CAGR of 12.9% between 2025 and 2032.

The integration of smart, digital health-enabled biomaterials and rapid expansion in emerging markets, especially the Asia Pacific, provide major future growth opportunities.

Companies such Evonik Industries AG, Medtronic plc, Carpenter Technology Corporation, Invibio Ltd., and Berkeley Advanced Biomaterials are some of the major players operating in the biomaterials market.