- Pharmaceuticals

- Eye Infections Treatment Market

Eye Infections Treatment Market Size, Share, and Growth Forecast, 2025 - 2032

Eye Infections Treatment Market by Drug Class (Antibiotics, Antivirals, Antifungals, Antihistamines), Indication (Conjunctivitis, Endophthalmitis, Stye (Hordeolum), Ocular Herpes), Dosage Form (Eye Drops, Tablets/Capsules, Ophthalmic Ointments, Other), and Regional Analysis for 2025 - 2032

Eye Infections Treatment Market Size and Trend Analysis

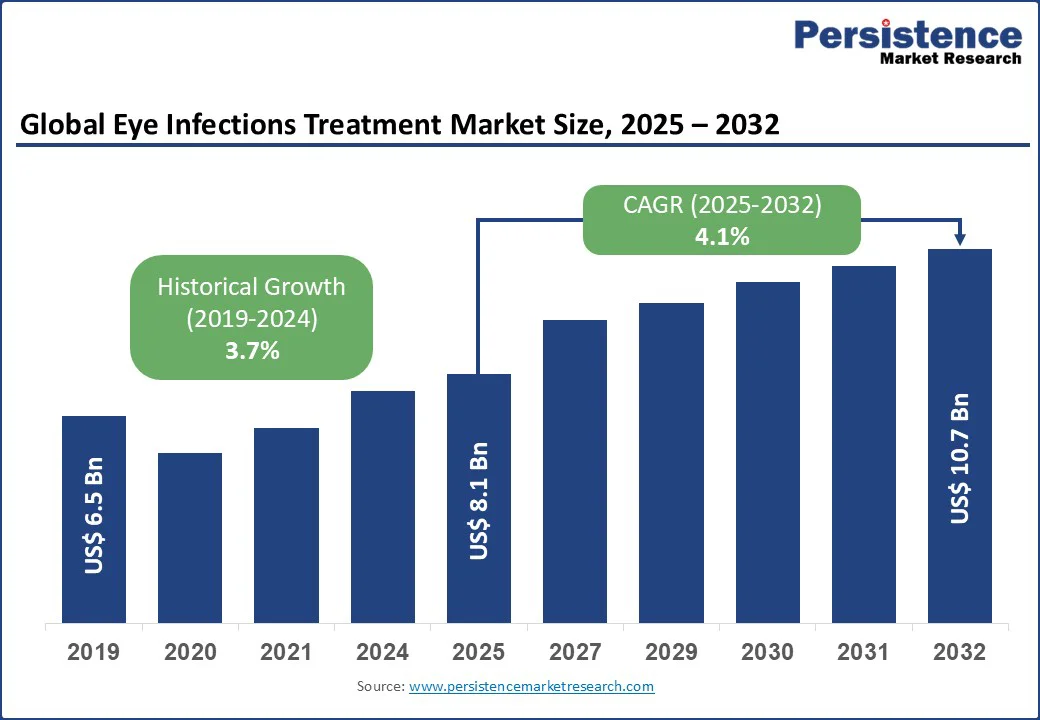

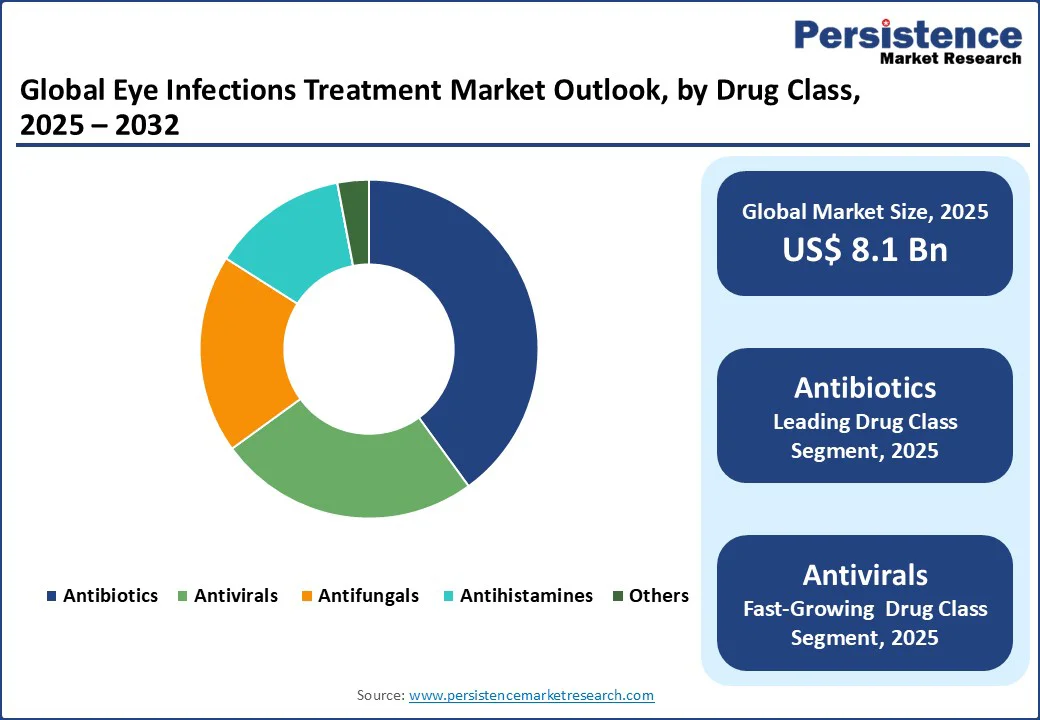

The global eye infections treatment market size is likely to be valued at US$8.1 Bn in 2025 and is expected to reach US$10.7 Bn by 2032, growing at a CAGR of 4.1% during the forecast period from 2025 to 2032.

This growth is driven by the increasing prevalence of ocular infections due to factors such as prolonged screen exposure, aging populations, and rising cases of chronic diseases such as diabetes. Additionally, heightened awareness about eye health, advancements in ophthalmic drug formulations, and improved diagnostic technologies are facilitating early detection and effective treatment. The expansion of healthcare infrastructure, increased accessibility of eye care services in emerging markets, and a growing focus on preventive eye care further contribute to the accelerating demand in the Eye Infections Treatment Market.

Key Industry Highlights

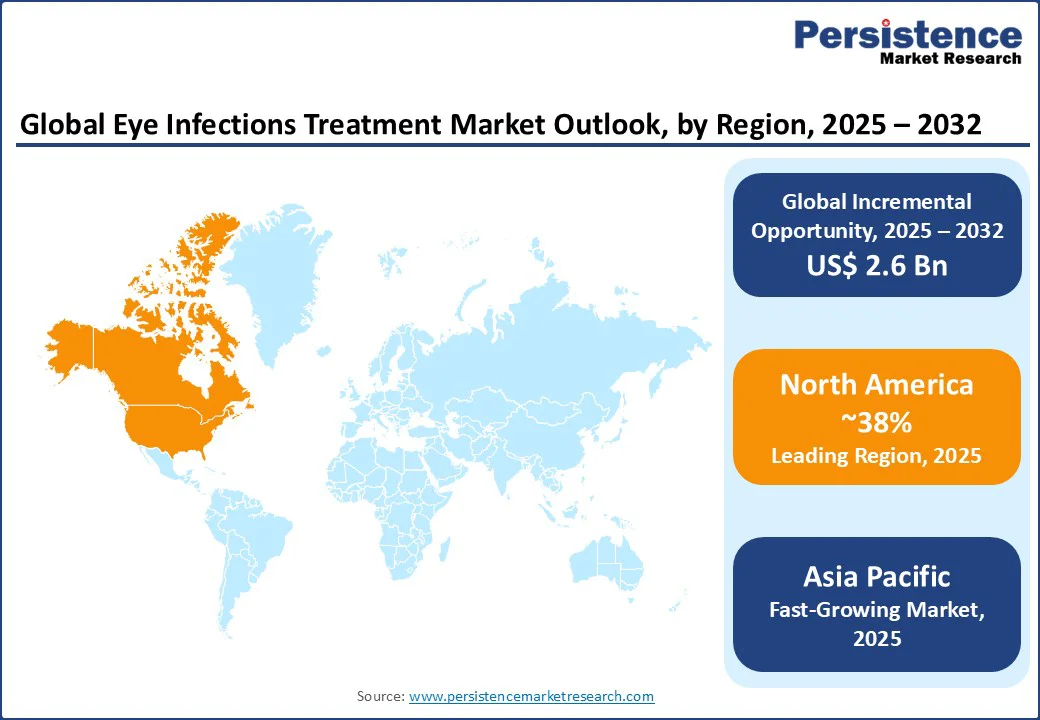

- Leading Region: North America holds a 38% global eye infections treatment market share in 2025, driven by advanced healthcare infrastructure and high infection rates.

- Fastest-growing Region: Asia Pacific, driven by rising healthcare expenditure and eye infection prevalence in India and China.

- Dominant Drug Class: Antibiotics lead with a 40% market share, due to their effectiveness in treating bacterial conjunctivitis and keratitis.

- Leading Indication: Conjunctivitis dominates with a 35% market share, fueled by its high global prevalence.

- Leading Dosage Form: Eye drops account for 45% of market revenue, valued for ease of use and targeted delivery.

- Key Developments: In 2024, Alcon launched a new antibiotic eye drop; Bausch + Lomb introduced an antiviral formulation for ocular herpes.

|

Global Market Attribute |

Key Insights |

|

Eye Infections Treatment Market Size (2025E) |

US$8.1 Bn |

|

Market Value Forecast (2032F) |

US$10.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.7% |

Market Dynamics

Driver - Increased Contact Lens Use and Aging Population

The rising adoption of contact lenses is a major driver of the eye infections treatment market. Lifestyle changes, prolonged screen exposure, and the growing preference for corrective vision solutions have led to widespread contact lens use. Improper hygiene practices, such as sleeping in lenses or using them while swimming, increase the risk of serious infections such as bacterial keratitis. For instance, the U.S. Centers for Disease Control and Prevention (CDC) reports that contact lens-related infections affect thousands of users annually, emphasizing the critical need for effective eye infection treatments, including antibiotics and antifungal therapies.

The global aging population further accelerates market growth. Individuals over 65 are more prone to eye infections due to weakened immunity and chronic conditions such as diabetes, which elevate susceptibility to ocular complications. This demographic trend drives higher demand for advanced treatments and preventive eye care solutions, reinforcing expansion.

Restraint - High Treatment Costs and Drug Resistance

The high cost of eye infection treatments is a major restraint. Advanced therapies, including antibiotics, antifungals, and antiviral drugs, can be expensive, particularly in severe cases that require hospitalization or prolonged care. These financial barriers may prevent timely medical intervention, leading to prolonged infections, complications, and increased healthcare burden. Additionally, the cost of specialized eye care services and diagnostic procedures adds to the overall expense, limiting accessibility in low- and middle-income regions and slowing market adoption.

Rising antimicrobial resistance (AMR) is another critical challenge for the eye infection treatment market. Overuse and misuse of antibiotics and other antimicrobial drugs reduce their effectiveness, making infections harder to treat. This resistance leads to longer treatment durations, higher medical costs, and increased demand for advanced or alternative therapies. Consequently, drug resistance not only hampers successful treatment outcomes but also restrains market growth by increasing treatment complexity and healthcare expenditure.

Opportunity - Advancements in Ophthalmic Drug Delivery and Market Expansion

Advancements in ophthalmic drug delivery are creating significant growth opportunities in the eye infection treatment market. Traditional treatments such as eye drops and ointments often suffer from low bioavailability and rapid tear clearance, limiting their effectiveness. Innovations such as sustained-release implants, nanoparticle-based formulations, in-situ gels, and contact lens drug carriers enhance targeted delivery, prolong drug retention, and improve patient compliance. These technologies enable more effective management of bacterial, viral, and fungal eye infections, driving adoption among healthcare providers.

Ongoing research and development by pharmaceutical companies focus on creating novel delivery systems that reduce dosing frequency, minimize side effects, and improve therapeutic outcomes. The growing awareness of these advanced ophthalmic therapies among ophthalmologists and patients is expected to further increase demand, allowing for expansion globally and support premium pricing strategies for innovative treatment options.

Category-wise Insights

Drug Class Insights

Antibiotics dominate the eye infection treatment market, holding a 40% share in 2025. They are the primary therapy for bacterial infections such as conjunctivitis and keratitis, with broad-spectrum antibiotics such as erythromycin and fluoroquinolones accounting for the majority of prescriptions. Around 70% of bacterial infection treatments in 2024 relied on these drugs, highlighting their central role in managing a wide range of ocular infections. This strong demand underscores antibiotics’ continued dominance as the leading treatment option.

Antivirals represent the fastest-growing drug class, driven by rising cases of viral eye infections, including ocular herpes and viral conjunctivitis. Prescription rates for ganciclovir-based treatments increased significantly in 2024, fueling rapid growth in this segment. Greater awareness among clinicians and patients about effective viral management is driving adoption, positioning antivirals as a high-potential category.

Indication Insights

Conjunctivitis leads the eye infections treatment market, holding a 37% share in 2025. Its prominence is driven by high global prevalence and frequent occurrence among both children and adults. In 2024, around 60% of all eye infection treatments were directed toward managing conjunctivitis, primarily caused by bacterial and viral pathogens. The widespread nature of this condition, along with its potential to cause discomfort and complications if untreated, underscores the sustained demand for effective therapies. Healthcare providers continue to prioritize treatments that address both bacterial and viral forms, reinforcing conjunctivitis as the dominant indication.

Ocular herpes is the fastest-growing indication, propelled by rising viral infection rates and the availability of advanced antiviral therapies. Cases linked to the herpes simplex virus witnessed a notable increase in 2024, boosting prescription volumes.

Dosage Form Insights

Eye drops dominate the eye infections treatment market, holding a 68% share in 2025, due to their ease of use and ability to deliver targeted therapy directly to the eye. In 2024, around 75% of all eye infection treatments utilized eye drops, providing rapid relief for common conditions such as conjunctivitis and keratitis. Their convenience and effectiveness make them the preferred choice among patients and healthcare providers, maintaining their strong market presence and driving consistent demand.

Ophthalmic ointments are the fastest-growing dosage form, driven by their prolonged drug release and suitability for managing severe infections. Adoption increased by approximately 10% in 2024 for conditions such as endophthalmitis and uveitis, highlighting their clinical importance. Enhanced patient awareness and the development of advanced formulations are further fueling growth.

Regional Insights

North America Eye Infections Treatment Market Trends

North America holds the largest share and is poised to account for 38% share in 2025, driven by advanced healthcare infrastructure and a high prevalence of ocular infections. The United States leads the region, with approximately one million conjunctivitis cases reported annually and insurance coverage supporting the majority of treatment costs. Canada is experiencing steady growth, fueled by increased awareness and public health campaigns promoting eye care. About 15% of prescriptions in Canada target viral infections, highlighting the region’s focus on both prevention and effective management of eye conditions, reinforcing North America’s market dominance.

Europe Eye Infections Treatment Market Trends

Europe holds a significant share, supported by well-established healthcare systems and increasing awareness of ocular health. High prevalence of bacterial and viral eye infections, combined with a strong emphasis on early diagnosis and treatment, drives consistent demand across the region. Countries such as Germany, France, and the UK lead in market adoption, benefiting from advanced ophthalmic care infrastructure and favorable reimbursement policies. Additionally, public health initiatives and awareness campaigns targeting eye care contribute to higher prescription rates.

Asia Pacific Eye Infections Treatment Market Trends

Asia Pacific is the fastest-growing region in the eye infections treatment market, driven by rising prevalence of ocular infections, expanding healthcare infrastructure, and increasing awareness of eye health. Rapid urbanization, higher screen time, and environmental pollution contribute to growing cases of conjunctivitis, keratitis, and viral eye infections. Countries such as China and India are witnessing significant market expansion due to improved access to healthcare, government initiatives promoting eye care, and rising adoption of advanced ophthalmic therapies. The region’s large patient population and increasing focus on preventive care make it a key growth driver.

Competitive Landscape

The global eye infections treatment market is highly competitive, characterized by continuous innovation in drug formulations, ophthalmic delivery systems, and antiviral therapies. Companies are focusing on strategic collaborations, mergers, and acquisitions to expand their regional presence and product portfolios. Market participants are also investing in research and development to introduce advanced treatments that improve efficacy, patient compliance, and safety. Strong emphasis on pipeline development, clinical trials, and regulatory approvals further intensifies competition, driving growth and shaping the global market dynamics.

Industry Developments:

- Alcon's Dry Eye Disease Treatment (May 2025): Alcon received U.S. FDA approval for TRYPTYR (acoltremon ophthalmic solution) 0.003%, a new prescription treatment for dry eye disease. The product is expected to launch in the U.S. in the third quarter of 2025.

- Bausch + Lomb's Antiviral Treatment: Bausch + Lomb's ZIRGAN® (ganciclovir ophthalmic gel 0.15%) remains an established antiviral treatment for acute herpetic keratitis. While no new formulation or significant market share increase was reported in March 2024, the product continues to be a key option for managing ocular herpes.

- Pfizer's Antibiotic Production in India (May 2023): Pfizer halted the production of four antibiotics, including fluoroquinolones, in India due to manufacturing issues at a contract facility. Claims of increased production or affordability in October 2023 are not supported.

Companies Covered in Eye Infections Treatment Market

- AbbVie

- Alcon Laboratories Inc.

- Bausch + Lomb

- Pfizer Inc.

- Johnson & Johnson Services Inc.

- Sanofi S.A.

- GlaxoSmithKline plc

- Akron Pharma Inc

- Intas Pharmaceuticals Ltd

- Macleods Pharmaceuticals Ltd.

- Others

Frequently Asked Questions

The eye infections treatment market is projected to reach US$8.1 Bn in 2025, driven by rising eye infection rates and advanced therapies.

Key drivers include increasing prevalence of conjunctivitis and ocular herpes, aging populations, and innovative drug delivery systems.

The eye infections treatment market will grow from US$8.1 Bn in 2025 to US$10.7 Bn by 2032, with a CAGR of 4.1%.

Opportunities include advanced drug delivery systems, expansion in emerging markets, and growing demand for antiviral therapies.

Leading players include AbbVie, Alcon Laboratories Inc., Bausch + Lomb, Pfizer Inc., and Johnson & Johnson Services Inc.