- Medical Devices

- Surgical Eyeglasses Market

Surgical Eyeglasses Market Size, Share, and Growth Forecast, 2026 – 2033

Surgical Eyeglasses Market by Product Type (Prescription Surgical Eyeglasses, Non-Prescription Surgical Eyeglasses), Application (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Others), Frame Material (Metal Frames, Plastic Frames, Others), and Regional Analysis for 2026-2033

Surgical Eyeglasses Market Share and Trends Analysis

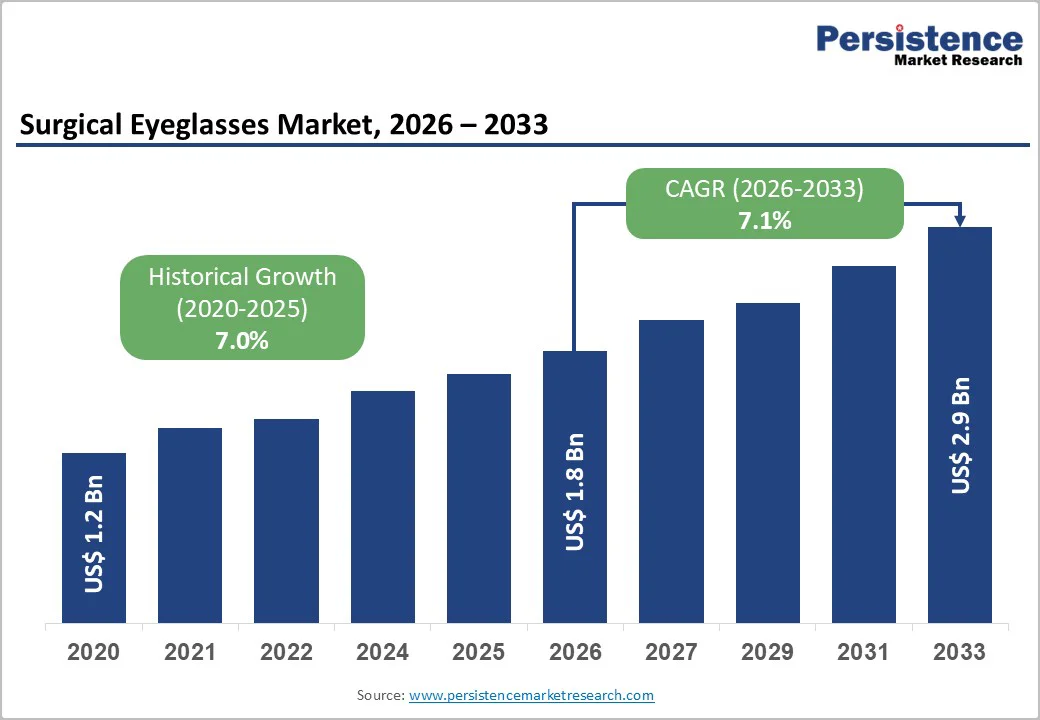

The global surgical eyeglasses market size is likely to be valued at US$ 1.8 billion in 2026, and is projected to reach US$ 2.9 billion by 2033, growing at a CAGR of 7.1% during the forecast period 2026−2033. The market demonstrates steady, non-cyclical growth driven by the rising volume of surgical procedures, stricter occupational safety standards for healthcare professionals, and increasing adoption of precision-enhancing medical accessories. Surgical eyeglasses play a critical role in improving visual acuity, reducing eye fatigue, and protecting surgeons from biological hazards, particularly during long-duration or high-risk procedures. Growth is further reinforced by the global expansion of ambulatory surgical centers, where cost efficiency and procedural accuracy are prioritized. Technological improvements in anti-fog coatings, lightweight frame materials, and customized prescription lenses have expanded product adoption beyond tertiary hospitals. Demographic aging, especially in North America, Europe, and Asia Pacific, continues to increase surgical demand across ophthalmology, orthopedics, and cardiovascular specialties. Regulatory emphasis on personal protective equipment compliance, especially after post-pandemic healthcare reforms, has institutionalized the use of surgical eyeglasses.

Key Industry Highlights

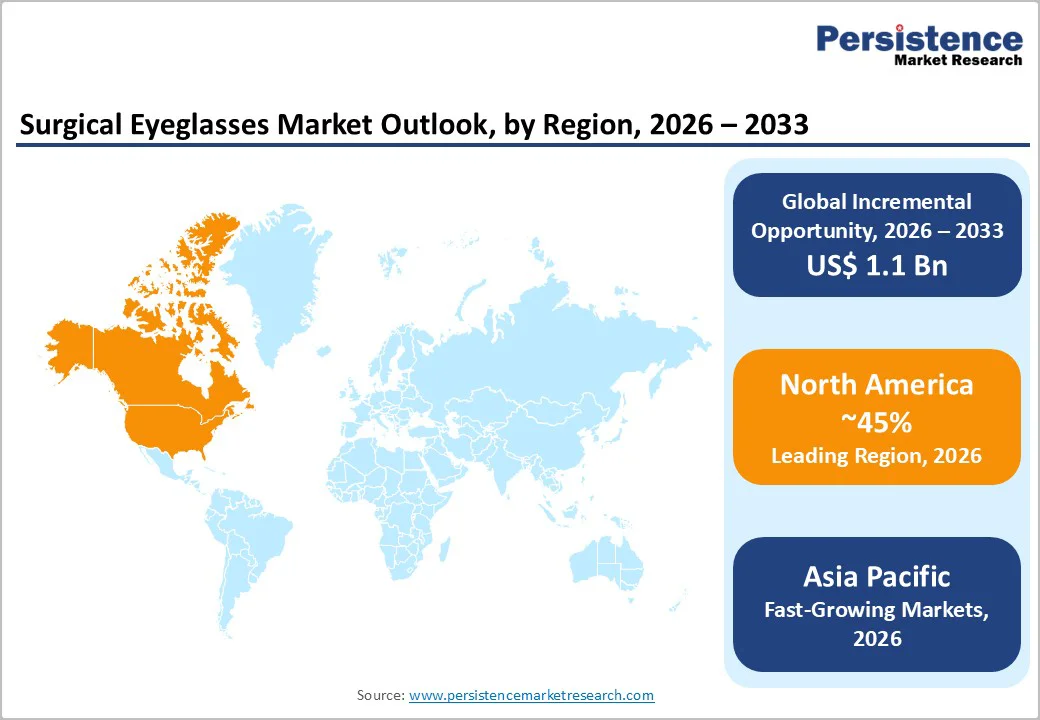

- Dominant Region: By 2026, North America is expected to lead with roughly 45% market share, driven by advanced infrastructure and availability of premium, ergonomic optical solutions.

- Fastest-growing Regional Market: Asia Pacific is estimated to be the fastest-growing market during 2026–2033 due to expanding healthcare infrastructure and rising surgical demand.

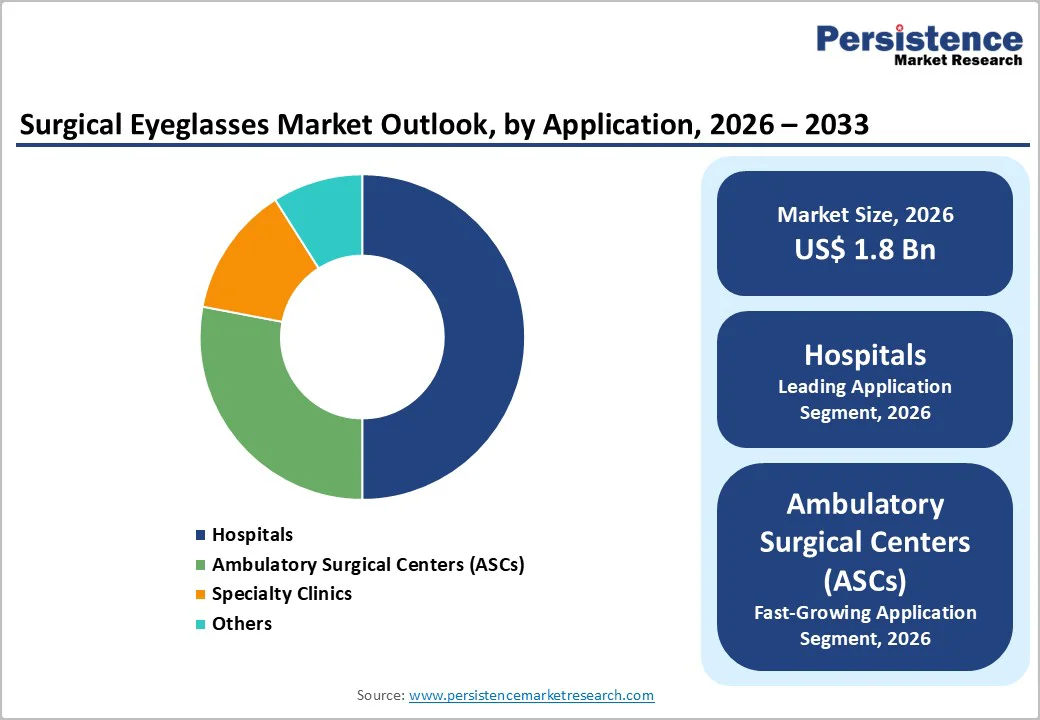

- Leading Application: Hospitals are anticipated to account for around 50% of the revenue share in 2026, as a result of high surgical volumes, centralized procurement, and efficient bulk purchasing.

- Fastest-growing Application: ASCs are expected to grow the fastest during 2026–2033, driven by a widespread demand for outpatient care, minimally invasive procedures, and efficient workflows.

| Key Insights | Details |

|---|---|

| Surgical Eyeglasses Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Optics and Ergonomics

Technological progress in optical engineering has transformed visual performance in surgical environments by delivering higher magnification accuracy, superior light transmission, and reduced visual distortion. Advanced lens coatings, anti-glare treatments, and precision optics enhance depth perception and clarity during complex procedures. These improvements support greater procedural confidence and accuracy, particularly in microsurgery and minimally invasive techniques where visual precision directly influences clinical outcomes. Integration of lightweight high-performance materials further improves optical stability during extended use, aligning with the growing demand for advanced visualization tools in operating rooms.

Ergonomic innovation strengthens adoption by addressing physical strain associated with prolonged surgical procedures. Optimized frame geometry, adjustable working distances, and balanced weight distribution reduce neck fatigue and postural stress. Enhanced comfort supports sustained concentration and operational efficiency during lengthy interventions. Compatibility with headlights, face shields, and other surgical equipment increases functional versatility within sterile settings. These ergonomic refinements align with evolving occupational health standards in healthcare facilities, reinforcing preference for technologically advanced solutions that improve performance, safety, and long term practitioner wellbeing.

Regulatory Approval and Standardization Challenges

Regulatory approval and standardization challenges act as a significant restraint due to the stringent requirements for medical device compliance. Surgical eyeglasses must meet specific safety and quality standards to ensure protection against biological hazards and maintain optical precision during medical procedures. The process involves extensive testing, documentation, and certification across multiple regions, each with its own regulatory framework. Delays in approval can extend product launch timelines, increase development costs, and reduce the ability to respond quickly to technological advancements or market demand shifts. Manufacturers must allocate substantial resources to adhere to these standards, which can limit innovation and operational flexibility.

Lack of global standardization further complicates market entry and scalability. Different countries enforce varying criteria for material quality, lens performance, and protective features, creating barriers for uniform production and distribution. Compliance requires adaptation of designs and manufacturing processes to meet local regulations, resulting in increased complexity and cost. This fragmented regulatory environment reduces efficiency in supply chains and limits partnerships with international distributors. Companies face challenges in achieving widespread adoption while maintaining adherence to safety and quality benchmarks, which constrains growth opportunities and slows expansion into new markets.

Integration of Advanced Features

The integration of advanced features represents a transformative opportunity for surgical eyeglasses, driven by the demand for enhanced precision and efficiency during procedures. Innovations such as high-definition optics, augmented reality overlays, and digital measurement tools enhance visualization and improve procedural outcomes. Real-time data display and connectivity with imaging systems streamline decision-making and support complex surgeries, enabling medical teams to operate with higher accuracy. These technological capabilities reduce the risk of errors, optimize workflow, and elevate the overall quality of care delivered within surgical environments.

Advanced features also enable differentiation in a competitive landscape, offering a value proposition that extends beyond standard visual aids. Lightweight materials, ergonomic designs, and adaptive lens technologies increase comfort and reduce fatigue during extended procedures, improving user experience. Integration with smart devices and software solutions allows seamless interaction with patient data and procedural guidance systems. Hospitals and surgical centers benefit from tools that enhance operational efficiency while maintaining stringent safety standards. The combination of precision, efficiency, and user-centric design positions these innovations as a critical factor in driving adoption and supporting next-generation surgical practices.

Category-wise Analysis

Product Type Insights

Prescription surgical eyeglasses are poised to dominate, with a forecasted market share of 60% in 2026, due to their ability to provide precise, individualized vision correction during prolonged procedures. Customization ensures optimal visual clarity, minimizes fatigue, and enhances accuracy in critical surgeries such as neurosurgery and ophthalmology. Through-the-lens (TTL) designs integrate prescriptions seamlessly, supporting high-precision requirements as hospitals and surgical centers increasingly prioritize surgeon performance and procedural efficiency. For instance, specialized eye hospitals use TTL surgical eyeglasses to maintain consistent visual standards during extended operations.

Non-prescription surgical eyeglasses are estimated to be the fastest-growing segment from 2026 to 2033, propelled by versatility and shareability across multiple users. Features such as anti-fog coatings, adjustable frames, and lightweight designs improve usability for general procedures, training environments, and high-volume surgical centers. Adoption is anticipated to accelerate in regions prioritizing operational efficiency and standardized surgical protocols, particularly in Asia Pacific. Hospitals and teaching institutions benefit from cost-effectiveness, rapid deployment, and simplified maintenance, supporting wider use across diverse medical applications.

Application Insights

Hospitals are anticipated to secure around 50% of the surgical eyeglasses market revenue share in 2026, driven by high-volume surgical activities and large-scale institutional procurement. Centralized purchasing and standardized equipment requirements allow hospitals to adopt surgical tools efficiently, ensuring consistent availability for various procedures. For instance, tertiary care hospitals performing multiple daily surgeries leverage bulk procurement to maintain supply continuity, reduce operational costs, and support high procedural throughput across diverse specialties.

Ambulatory surgical centers are expected to be the fastest-growing segment during the 2026-2033 forecast period, supported by the shift to outpatient care and minimally invasive procedures. These centers benefit from efficient workflows, shorter patient stays, and reduced operational overhead, making them attractive for day surgeries. Adoption is anticipated to accelerate in regions emphasizing outpatient infrastructure, particularly in North America and Asia Pacific. Facilities gain advantages from streamlined operations, rapid turnover, and targeted procedural specialization, positioning ambulatory centers as a critical growth area within the surgical services landscape.

Frame Material Insights

Metal frames (titanium) are projected to hold a 50% market share in 2026, owing to exceptional durability and stability, particularly for high-magnification use of 4.0x and above. Long-term structural integrity ensures consistent performance during prolonged procedures, reducing adjustment requirements and minimizing fatigue. Wider adoption is expected as surgical centers increasingly prioritize reliability and precision in demanding specialties such as neurosurgery and ophthalmology. For instance, tertiary care hospitals use titanium frames to maintain consistent optical alignment during extended operations, enhancing procedural accuracy and supporting efficient surgical workflows.

Plastic frames are set to represent the fastest-growing segment through 2033, driven by affordability and versatility in entry-level applications. Materials such as TR90 offer lightweight, flexible designs suitable for diverse procedures and multi-user environments. Adoption is anticipated to accelerate in emerging regions emphasizing cost-effective solutions and rapid deployment, particularly in Asia Pacific. Hospitals and teaching centers benefit from ease of replacement, adaptability across multiple surgical specialties, and suitability for training environments, positioning plastic frames as a critical growth area within the surgical eyeglasses market.

Regional Insights

North America Surgical Eyeglasses Market Trends

By 2026, North America is expected to lead with an estimated 45% of the surgical eyeglasses market share, propelled by advanced surgical infrastructure and high-volume surgical facilities. Hospitals and specialized surgical centers conduct a large number of complex procedures, including neurosurgery, ophthalmology, and cardiovascular interventions, creating sustained demand for precision optical equipment. Adoption of high-magnification eyeglasses is reinforced by sophisticated operational protocols, where surgical accuracy and procedural efficiency are critical. Investment in ergonomic designs and surgeon-focused customization enhances usability and reduces fatigue during prolonged procedures. Regulatory standards for optical quality in the region favor premium and technologically advanced solutions capable of meeting rigorous procedural requirements.

Integration with digital surgical ecosystems is a key factor reinforcing market leadership. Surgical eyeglasses are increasingly synchronized with real-time imaging, augmented reality overlays, and intraoperative guidance systems, improving workflow and decision-making efficiency. Medical training programs and academic hospital networks encourage early adoption among residents and fellows, embedding high-quality optical solutions into standard practice. Collaboration between manufacturers and hospital networks accelerates deployment of innovative designs across multiple specialties. This combination of technological advancement, procedural standardization, and institutional adoption underpins the dominant position of North America in the surgical eyeglasses market.

Europe Surgical Eyeglasses Market Trends

Europe holds a strong position in the surgical eyeglasses market, supported by advanced healthcare systems, high surgical procedure volumes, and integration of precision optical tools in operating theaters. Hospitals and specialty surgical centers use high-magnification and ergonomically designed eyewear to improve procedural accuracy and reduce fatigue during prolonged surgeries. Regulatory standards for medical equipment ensure adoption of high-quality optical solutions. Well-established medical infrastructure and advanced training programs in teaching centers contribute to steady demand for reliable and innovative surgical eyeglasses.

Minimally invasive and outpatient procedures increase the need for lightweight and adjustable surgical eyeglasses suitable for multi-user environments and high-throughput operations. Integration with imaging systems, augmented reality-assisted platforms, and training programs enhances usability across specialties such as ophthalmology, neurosurgery, and cardiovascular surgery. Collaboration between manufacturers and healthcare institutions helps deploy innovative designs efficiently, improves workflow, and strengthens Europe as a significant market for surgical eyeglasses.

Asia Pacific Surgical Eyeglasses Market Trends

Asia Pacific is estimated to be the fastest-growing market for surgical eyeglasses during 2026-2033, supported by expanding healthcare infrastructure, rising surgical volumes, and increasing adoption of advanced optical solutions. Rapid development of tertiary care hospitals and teaching centers, combined with growing investments in surgical technologies, is creating a strong demand for precision eyewear. Entry-level and cost-effective solutions, such as lightweight frames and adjustable designs, support adoption in high-volume and multi-user environments. Urban centers and emerging healthcare markets are increasingly equipped to handle complex procedures, accelerating uptake.

Key factors contributing to growth include increasing awareness of ergonomic and high-clarity optical solutions and integration with modern surgical workflows. Hospitals and training institutions utilize surgical eyeglasses to enhance procedural accuracy, reduce fatigue, and improve efficiency in day surgeries and minimally invasive procedures. Collaboration between manufacturers and regional healthcare networks facilitates deployment of innovative designs across multiple facilities.

Competitive Landscape

The global surgical eyeglasses market structure is moderately fragmented, with key players such as EssilorLuxottica, ZEISS, Johnson & Johnson Vision, Alcon, STAAR Surgical, collectively accounting for around 45% of total revenue. Competition is driven by product quality, adherence to regulatory standards, pricing strategies, and distribution capabilities. Established optical brands coexist with specialized medical device manufacturers, creating a diverse and dynamic competitive environment. Companies continuously focus on innovation in lens clarity, frame durability, and ergonomic designs to meet the evolving demands of surgical professionals.

Market players strengthen their presence through global distribution networks and partnerships with hospitals, surgical centers, and training institutions. Differentiation is achieved via high-precision optics, lightweight frame materials, and customization options tailored for various specialties. Emphasis on reliability, comfort, and performance during prolonged procedures allows companies to maintain a competitive edge while addressing the critical needs of surgical teams and supporting improved procedural outcomes.

Key Industry Developments

- In December 2025, Glass Lewis, a leading proxy advisory firm, has reiterated its recommendation for STAAR Surgical shareholders to support the company's US$ 2.19 billion acquisition by Sight Sciences. The endorsement escalates the ongoing battle between deal proponents and activist investors who oppose the merger, citing concerns over valuation and deal terms.

- In November 2025, Snke introduced SnkeXR medical augmented reality glasses in collaboration with Lumus, integrating waveguide optics to deliver real-time surgical visuals and hands-free data access, supporting improved precision and workflow efficiency in operating room environments.

- In January 2025, Vuzix unveiled AI-powered smart glasses at CES 2025, including the Ultralite Pro and Audio OEM platforms powered by Qualcomm's Snapdragon AR1. The glasses feature advanced waveguide technology for AR applications including real-time translation, voice assistance, and medical applications such as knee surgery alignment.

Companies Covered in Surgical Eyeglasses Market

- EssilorLuxottica

- ZEISS

- Johnson & Johnson Vision

- Alcon

- STAAR Surgical

- Hoya Corp

- Topcon

- NIDEK

- Lumenis

- Cynosure

- Santen

Frequently Asked Questions

The global surgical eyeglasses market is projected to reach US$ 1.8 billion in 2026.

Increasing surgical volumes, demand for enhanced visual precision, focus on surgeon comfort during prolonged procedures, and adoption of advanced optical and ergonomic designs are driving the market.

The market is poised to witness a CAGR of 7.1% from 2026 to 2033.

Integration of advanced optical technologies, growing adoption in outpatient and training environments, and rising demand for ergonomic, cost-effective surgical eyewear across expanding healthcare facilities are creating high-value opportunities for market players.

Some of the key market players include EssilorLuxottica, ZEISS, Johnson & Johnson Vision, Alcon, STAAR Surgical, and Hoya Corp.